Calculation of insurance premiums to the Federal Tax Service 2021 - current form

The report Calculation of insurance premiums in 2021, adopted relatively recently (from 01/01/17), is valid according to Order No. ММВ-7-11 / [email protected] dated 10/10/16. The document is filled out according to the amounts of remuneration accrued in favor of citizens, and also for SV (insurance premiums) for the period. At the same time, data must be submitted quarterly for all types of insurance, except for injuries. An updated ERSV form is currently under development, but it is not yet known when exactly the changes will be adopted.

You can download the unified calculation of insurance premiums 2021 here:

(Form) Unified calculation of insurance premiums

There were no changes

Apparently, starting from 2021, insurance premium payments will have to be submitted on an updated form. Let's say right away that these adjustments are mainly not related to changes in tax legislation. The Federal Tax Service of Russia simply decided to finalize some calculation indicators, as well as clarify its electronic version.

| № | Content |

| 1st | Accumulates data on what obligations the payer has. This section is the most informative. It contains information about the estimated amounts for all contributions: compulsory social insurance, compulsory medical insurance, compulsory social insurance (except for injuries). |

| 2nd | Contribution obligations, who heads the peasant farm |

| 3rd | Individual credentials of insured persons. Information for each person is filled out separately. |

| Who rents | What does it rent? | |||

| Title page | Sections | Subsections | Applications | |

| All employers | 1 and 3 | 1.1 1.2 | 2nd to first section | |

| If there are reduced or additional contributions. tariffs | 1 and 3 | 1.3.1 1.3.2 1.4 | 2nd, 5–10th to the first section | |

| Who had to make payments for illness and maternity | 1 and 3 | Of necessity | 3rd and 4th to the first section | |

The form under consideration for a single calculation of insurance premiums for 2018 consists of:

- from the title page;

- a sheet with information about an individual who does not have the status of an individual entrepreneur;

- Section 1 (summary data on the obligations of the payer of contributions) 10 appendices to it;

- Section 2 (summary data on obligations for insurance premiums of heads of peasant farms) 1 appendix;

- Section 3 (information about insured persons).

Let us say right away that you do not need to include absolutely all sheets and applications in the generated report. So, in most cases, employers who paid income to individuals should only fill out:

- title page;

- Section 1 (subsections 1.1 and 1.2) of Appendix No. 1 and 2 thereto;

- Section 3.

Let us immediately note that a new form of calculation for insurance premiums has not been introduced since 2021. Therefore, the previous form applies.

For sending calculations of contributions to the tax office electronically, the requirements have also not changed. They are established by Appendix No. 3 to the mentioned order of the Federal Tax Service No. ММВ-7-11/551.

The developer of the software with which the policyholder generates the calculation always takes into account the format of the file with the report regulated by the Federal Tax Service of Russia and the ensuing issues.

Also see “How to fill out the calculation of insurance premiums for the 1st quarter of 2021: sample.”

The form of a single calculation for insurance premiums 2021 has been changed. An absolutely new form was not developed. It’s just that the current form was slightly adjusted and supplemented with new columns.

The second application, in which the amounts of contributions for mandatory social services are calculated. insurance

Let's look at some more changes in terms of insurance premiums:

- Some companies under the simplified tax system must now calculate a share of income to take advantage of the reduced premium rate. This amendment adjusted the principles for calculating the share of income to recognize the company's main activity. The amount of such income, as before, must be divided by the total amount of income received. However, now the total amount of income must include those that do not form the tax base.

- Contributions from private entrepreneurs are no longer related to the minimum wage and tariff rate. Now the legislation has established specific amounts of contributions:

- If your income is less than 300 thousand rubles, contributions for pension insurance will be 26,545 rubles, and for medical insurance – 5,840 rubles;

If your income for the year is more than 300 thousand rubles, you will need to make additional deductions in the amount of 1%.

You can find out about other changes in accounting and tax legislation in our review article Changes in accounting and tax accounting in 2021.

The calculation form for insurance premiums 2021 was approved by order of the Federal Tax Service dated October 10, 2016 No. ММВ-7-11/551, KND code - 1151111. It is called “Calculation of insurance premiums” (DAM, ERSV).

The RSV contains information on payments for compulsory insurance:

- compulsory pension insurance (OPI), incl. at an additional tariff, as well as at additional social security;

- compulsory health insurance (CHI);

- compulsory social insurance in case of temporary disability and in connection with maternity (VNIM).

READ MORE: Personal income tax from the salary of a deceased employee in 2021

The report in KND form 1151111 consists of the following information blocks.

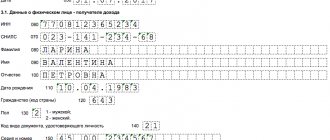

1. General information about the policyholder (organization, individual entrepreneur or individual who is not an individual entrepreneur).

2. Section 1.

Contains basic information for payment:

- KBK;

- amounts payable for the billing period (including for the last 3 months);

- the amount of excess expenses for VNiM contributions.

Subsection 1.1 includes information on OPS:

- total insured individuals since the beginning of the year, including over the last 3 months;

- the number of individuals to whom payments were made and contributions were accrued, including in amounts that exceed the maximum base value;

- the amount of all payments and other remuneration in favor of individuals;

- amounts of non-taxable payments;

- the basis for calculating insurance premiums, including in amounts exceeding the limit;

- the calculated amount, including from amounts that exceed and do not exceed the base limit.

Subsection 1.2 includes information on compulsory medical insurance similar to subsection 1.1.

Subsection 1.3 contains:

- OPS at an additional tariff (subsection 1.3.1);

- OPS at an additional tariff for certain categories of payers (“harmfulness”) specified in clause 3 of Art. 428 Tax Code (subsection 1.3.2).

Download

In order to dispel doubts about how to fill out the form for calculating insurance premiums, you should refer to the order that approved the form for the unified calculation of insurance premiums (you can download it from the link given above).

The calculation of insurance premiums for 2021 based on the results of 2021 must be submitted by the organization (IP) to its Federal Tax Service no later than January 30, 2018 (clause 7 of Article 431 of the Tax Code of the Russian Federation).

Let us remind you that it is in electronic form that the calculation of insurance premiums in 2021 is submitted if the average number of persons who received payments and remunerations from the organization (IP) for the previous billing period exceeded 25 people (clause

10 tbsp. 431 of the Tax Code of the Russian Federation). Otherwise, you can submit the report on paper.

Calculation of insurance premiums 2021: download form

You can calculate insurance premiums for free in the ConsultantPlus system.

Where to submit calculations for insurance premiums 2021

The control body for submitting the ERSV is a territorial division of the Federal Tax Service. In this case, the submission of the form is carried out by legal entities at the location of the company, and by individuals (individual entrepreneurs) - at the address of residence. Separate delivery regulations are provided for companies with OP (separate divisions).

Payments for insurance premiums of a separate division in 2018 are submitted by the OP independently only in cases where settlements with citizens are carried out by the branch. If all payments are accrued and issued at the parent company, the preparation and submission of the ERSV is also carried out at the Federal Tax Service Inspectorate at the address, regardless of whether the OP has its own bank account, as well as a balance sheet.

Where to submit the report

This report is submitted to the tax office at the place of registration of the individual entrepreneur or the place of registration of the LLC. It happens that the report must be submitted not to the tax office at the legal address of the company, but to the tax office at the place of registration of the separate division. This may occur if the parent organization gives the Separate Unit the right to independently calculate and assess insurance premiums. This rule is approved by order of the manager, about which the tax inspectorate is informed in any form.

Calculation of insurance premiums 2021 – due date

The generally accepted deadlines for calculating insurance premiums in 2021 are approved in paragraph 7 of the article. 431. It is determined here that the deadline for submitting data is the 30th day of the month following the period. That is, whether a company reports for a year or a quarter, the ERSV is submitted strictly before the 30th. A transfer is possible if the deadline for submitting the form coincides with official holidays and/or weekends.

When is the calculation of insurance premiums 2021 submitted - deadlines:

- Final ERSV for 2021 – until 01/30/18.

- Quarterly calculation of insurance premiums for the 1st quarter of 2021 – until 05/03/18 due to the postponement of weekends and May holidays.

- Semi-annual calculation for the 1st half of 2021 – until 07/30/18.

- Nine-month payment for 9 months. 2021 – until October 30, 2018

- Final ERSV for 2021 – until 01/30/19.

Please keep in mind that for violating the regulatory deadlines for filing the ERSV, the company/individual entrepreneur may be fined by the tax authorities. Responsibility is provided for by the state in paragraph 1 of Art. 119 NK. The minimum sanction is 1,000 rubles, the maximum is 30% of the amount of CB payable under the report. In this case, the usual fine is equal to 5% of the specified amount of fees for all full and partial months of non-payment of fees.

General tariff extended for 2021

From January 1, 2021, Law No. 335-FZ dated November 27, 2017 (hereinafter referred to as Law No. 335-FZ), with amendments to the Tax Code of the Russian Federation, obliged some simplified organizations to count the share of income in a new way for applying a reduced tariff of insurance premiums.

These changes in insurance premiums from 2021 have adjusted the rules for calculating the share of income for recognizing the type of activity of an organization as the main one (clause 6 of Article 427 of the Tax Code of the Russian Federation as amended).

It is still necessary to divide the amount of such income by the total amount of income. But an important clarification has been made: the total amount of income (i.e., the denominator of the calculation formula) must include income that is provided for in Art. 251 Tax Code of the Russian Federation.

That is, they do not form the tax base.

Let's say right away that insurance premium rates in 2021 remained at the same level (Articles 425 and 426 of the Tax Code of the Russian Federation). This is 30 percent, which includes:

- 22% – contributions to compulsory pension insurance;

- 5.1% – contributions to compulsory medical insurance;

- 2.9% – social security contributions.

The change from 2021 is that, based on Law No. 361-FZ dated November 27, 2017, the general rate of 30% will be valid until 2020 inclusive (Articles 425, 426 of the Tax Code of the Russian Federation).

Also see 2021 Premium Rates: Rate Table.

| Line | Index |

| 210 | The amount of payments and other remuneration for each of the last 3 months of the reporting or billing period |

| 220 | The base for contributions to compulsory pension insurance within the limits for the same months |

| 240 | Calculated contributions to compulsory social security within the limits for the same months |

| 250 | Result for lines 210, 220 and 240 |

| 280 | Base for calculating pension contributions at the additional tariff for each of the last 3 months of the reporting or billing period |

| 290 | The amount of calculated pension contributions at the additional tariff for the same months |

| 300 | Result on lines 280 and 290 |

Please note that the total indicators in the listed lines for all individuals must correspond to the summary data in Subsections 1.1 and 1.3 of the calculation of contributions.

Also see “Submission of calculations for insurance premiums in 2021: deadlines.”

Based on the Decree of the Government of the Russian Federation dated December 11, 2017 No. 1514 from January 1, 2021

The Social Insurance Fund pilot project for direct payments has been extended until 2021 inclusive. However, new regions, as originally planned, will not be included in it. The reasons for this decision are unknown.

Thus, the expansion of the FSS pilot project has been suspended. Direct payments from the fund remain only in 33 regions of Russia, and in the rest the offset scheme continues to operate.

New edition of clause 2 of Art. 432 of the Tax Code of the Russian Federation (Law No. 335-FZ) establishes a new deadline for the transfer of pension contributions to individual entrepreneurs without staff and private practice specialists with incomes of 300,000 rubles.

Previously, this deadline was no later than April 1 of the following year. But it was postponed from reporting for 2021 to July 01.

For more information, see “Deadline for payment of individual entrepreneur insurance premiums for 2021.”

Based on the Law of November 27, 2021 No. 353-FZ, reduced insurance premium rates from 2021 are valid for residents of the special economic zone in Kaliningrad (for compulsory health insurance - 6%, for social insurance - 1.5%, for compulsory medical insurance - 0.1%). This is a new paragraph 11 of Article 427 of the Tax Code of the Russian Federation.

They can be used for 7 years from the month following the month of inclusion in the register of SEZ residents. This benefit will be valid until 2025 inclusive.

In lines 160 – 180 of Subsection 3.1, enter the code for the types of compulsory insurance:

- “1” – if the individual for whom Section 3 is being filled out is an insured person;

- “2” – the individual is not insured.

Line 060 of Appendix No. 6 indicates the amount of income determined in accordance with Article 346.15 of the Code on an accrual basis from the beginning of the reporting (calculation) period.

Line 070 of Appendix No. 6 indicates the amount of income from the sale of products and (or) services provided in the main type of economic activity, determined for the purpose of applying subparagraph 3 of paragraph 3 of Article 427 of the Code.

Line 080 of Appendix No. 6 indicates the share of income determined for the purposes of applying paragraph 6 of Article 427 of the Code. The indicator value is calculated as the ratio of the values of lines 070 and 060, multiplied by 100.

In order to comply with the conditions specified in paragraph 7 of Article 427 of the Code, payers fill out lines 010 - 050, column 1 of Appendix No. 7 when submitting a calculation for each reporting period, lines 010 - 050, column 2 of Appendix No. 7 when submitting a calculation for the billing period.

Line 010 of Appendix No. 7 reflects the total amount of income determined in accordance with Article 346.15 of the Code, taking into account the requirements specified in paragraph 7 of Article 427 of the Code.

Line 020 of Appendix No. 7 reflects the amount of income in the form of targeted revenues for the maintenance of non-profit organizations and their conduct of statutory activities, named in subparagraph 7 of paragraph 1 of Article 427 of the Code, determined in accordance with paragraph 2 of Article 251 of the Code.

Line 030 of Appendix No. 7 reflects the amount of income in the form of grants received for the implementation of activities named in subparagraph 7 of paragraph 1 of Article 427 of the Code, determined in accordance with subparagraph 14 of paragraph 1 of Article 251 of the Code.

Line 040 of Appendix No. 7 reflects the amount of income from the types of economic activities specified in paragraphs seventeen - twenty-one, thirty-four - thirty-six of subparagraph 5 of paragraph 1 of Article 427 of the Code.

Line 050 of Appendix No. 7 reflects the share of income determined for the purposes of applying paragraph 7 of Article 427 of the Code, which is calculated as the ratio of the sum of lines 020, 030, 040 to line 010, multiplied by 100.

The Federal Tax Service has developed a new form of DAM (calculation of insurance premiums). The draft order was published on the Unified Portal for posting draft regulatory legal acts.

The draft order stipulates that it comes into force on January 1, 2021 and will be applied starting with reporting for the 1st quarter of 2021. But at the beginning of the reporting company’s 1st quarter of 2018, the order to amend the DAM form is at the stage of public discussion.

We will write in more detail about the new DAM form when the draft order with changes to the current DAM form is finally approved and published.

Thus, to submit the report for the 1st quarter of 2021, the previously valid form is used, approved by order of the Federal Tax Service of Russia dated October 10, 2016 No. ММВ-7-11 / [email protected] Last day for submitting the DAM form (calculation of insurance premiums) for the 1st quarter of 2021 year - May 3, 2018, since 04/29-05/02/2018 are holidays.

Absolutely all policyholders, when submitting the DAM (calculation of insurance premiums) form, fill out the following parts of the report:

- title page;

- subsection 1.1 of Appendix No. 1 of Section 1 – pension contributions;

- subsection 1.2 of Appendix No. 1 of Section 1 – contributions to compulsory medical insurance;

- Appendix No. 2 of Section 1 – social insurance contributions in case of temporary disability and in connection with maternity;

- section 3 - personalized information about insured persons.

Despite the fact that the 2021 Insurance Premium Calculation form cannot be called new, some changes in its completion for residents of the Special Economic Zone in the Kaliningrad Region need to be taken into account. How to fill out the Calculation form for insurance premiums by SEZ resident organizations in the Kaliningrad region when they apply reduced rates of insurance premiums in accordance with paragraphs.

14 clause 1 art. 427 of the Tax Code of the Russian Federation?.

| Insured person category code | In relation to which insured individuals is indicated |

| KLN | Individuals who are subject to the OPS, including persons employed in a workplace with special (difficult and harmful) working conditions |

| VPKL | Foreign citizens or stateless persons (with the exception of HQS) temporarily staying in the territory of the Russian Federation |

| VZHKL | Persons insured in the OPS system from among foreign citizens or stateless persons temporarily residing in the territory of the Russian Federation, as well as foreign citizens or stateless persons temporarily residing in the territory of the Russian Federation who have been granted temporary asylum |

MORE DETAILS: Name of the medical insurance organization (branch), other organization The

above recommendations must be taken into account by SEZ resident organizations in the Kaliningrad region when filling out the form for Calculation of insurance premiums for the 1st quarter of 2018 and subsequent reporting periods

The income tax return has been changed from the reporting for 2017. That is, now you will need to report for the year using a new declaration form. The draft changes are available on the website regulation.gov.ru.

There are no major changes expected, so this declaration is unlikely to cause any difficulties. The 2021 tax amendments will mainly be taken into account. In particular, a rule appears in the declaration: it is possible to reduce the profit base for losses of previous years only within 50 percent. Also, sheets for consolidated groups of companies and controlled organizations will be updated.

For 2021, you will need to submit a new property tax return form. The form and procedure for filling it out were approved by order of the Federal Tax Service of Russia dated March 31, 2021 No. ММВ-7-21/ [email protected] , which came into force on June 13, 2021.

The new declaration now includes section 2.1 “Information on real estate objects taxed at the average annual value.” It provides lines for entering the cadastral number, OKOF code, and the residual value of the real estate property.

A new form must be submitted for transport tax reporting for 2021. It was approved by order of the Federal Tax Service of Russia dated December 5, 2016 No. ММВ-7-21/ [email protected]

The new declaration form now has special lines where you need to indicate the amount of the “Platonic” fee, by which the transport tax can be reduced from January 1, 2021. In section 2 of the declaration, you must indicate in separate lines: “Date of registration of the vehicle”; “Date of termination of registration of the vehicle (deregistration)” and “Year of manufacture of the vehicle.”

On our website we have already written about the new Calculation of insurance premiums for premiums for the first quarter of 2021. We emphasize that this Calculation will have to be submitted only in April 2021.

We will return to this topic closer to the 1st quarter reporting. And now, briefly about the changes in the calculation of insurance premiums.

Amendments will be in section 3 of the calculation, which is intended for personalized information. A new attribute “Adjustment type” will appear there.

You will need to check which form you are submitting: original, corrective, or canceling. And in Appendix 2 to Section 1 a new detail “Payer’s tariff code” will be added.

The procedure for filling out the unified ERSV calculation

Tax calculations for SV are compiled according to the type of declaration. Consequently, the document has a title page, as well as sections for calculating the base for assessing contributions and reflecting charges. There is no data on incoming/outgoing balances and amounts paid, as was the case in 4-FSS. General requirements for the reflection of all information are given in Appendix 2 to Order No. ММВ-7-11/ [email protected] Let's consider common questions when drawing up the ERSV:

- How to indicate payment characteristics in the calculation of insurance premiums 2021 - the corresponding code (1 or 2) is given on page 001 Appendix. Section 2 1 to indicate the method of settlements with citizens. For the direct system, 1 is indicated, for the credit system, 2.

- Is it necessary to reflect dividends in the calculation of insurance premiums for 2018 - since such amounts are not included in the base for taxation of SV according to stat. 420, as well as are not mentioned in non-taxable amounts according to the norms of stat. 422, this type of remuneration to citizens is not required to be indicated in the ERSV.

- How to indicate the tariff code in the calculation of insurance premiums 2021 - the meaning of this code in terms of the tariff applied by the payer is given on page 001 of the Appendix. 1 to section 1. And according to page 270 section. 3. The current coding is given in Appendix 5 to the Order. For example, for payers of contributions at the basic tariff and in the general mode, code 01 is intended, and for simplifiers - 02, etc. If during the period the company used different tariffs, it is required to create the number of sheets of Appendix 1 according to the number of tariffs applied.

- Should the calculation of insurance premiums for 2021 contain Appendix 3 - these sheets are generated only in situations where the employer incurs VNIM costs. In other cases, this section is not submitted.

How to fill out calculations for insurance premiums 2018

How to adjust the calculation of insurance premiums 2018

An updated calculation of insurance premiums for 2021 is required if accountants discover inaccuracies in the primary document, leading to an underestimation of the taxable base for insurance and amounts payable. At the same time, there is no need to include Section 3 in the calculation of insurance premiums for 2021 if there were no errors in the personal data of citizens. If such discrepancies are made, it is required to submit an adjustment based on personalized information in relation to the individuals for whom errors were found. Read more about the clarifications on the ERSV here.

How to calculate insurance premiums for individual entrepreneurs in 2021

Businessmen with hired individuals report in accordance with the general procedure. If an entrepreneur is engaged in business alone, he is not required to submit an ERSV to the control authorities. But he retains the obligation to pay fixed contributions to the state. The amount of such amounts can be easily determined independently or with the help of special services.

To ensure that you have the correct calculation of insurance premiums in 2021, there is a calculator for calculating fixed payments. In the process of determining the amounts, the current federal minimum wage is used to calculate insurance premiums for individual entrepreneurs for 2021. The entrepreneur should transfer obligations “for himself” to the budget before the end of the year.

Conclusion - in this article we figured out what form the ERSV report for 2021 is generated on in 2021. Separately, it is shown how to check the CS contributions and how to submit a corrective calculation for insurance premiums 2021. In order not to face the need to pay fines, you should not only comply with the deadlines for submitting data approved by law, but also check the report before sending it to the Federal Tax Service in order to identify possible errors, inaccuracies and inconsistencies.

Who rents

All legal entities, as well as individual entrepreneurs with employees, are required to submit a declaration. To accurately determine the need to submit reports, you can refer to the table.

| Organizations that have hired employees | Organizations that do not operate and do not have employment contracts with employees | Individual entrepreneurs with employees | Individual entrepreneurs without employees |

| Required to submit | Required to submit form zero | Required to submit | Not required to submit |