What kind of document is this?

This book reflects similar operations that have a certain economic essence and justification. They are associated with the moment of transfer of cash and monetary documents from one official to another: from the chief (senior) cashier to an ordinary cashier - at the beginning of the work shift, and in the reverse order - at the end of the shift .

The journal is filled out in order to record as accurately as possible the direct fact of the transfer of the specified material assets, and is used only when there is a central cash desk and departmental cash desks. Naturally, if the organization’s staff includes only one cashier, then the specified register does not need to be maintained.

You can see the procedure and sample for filling out the cash book in this article. How to properly maintain a general ledger in accounting - read here.

Who fills out form KO-5 and when?

Accounting for received and issued funds in the standard KO-5 form is usually practiced by an organization that has a complex internal structure with a large number of divisions (departments, divisions, subdivisions, sectors), each of which has its own separate cash desk.

In the KO-5 book, cash is recorded, which the chief (senior) cashier provides for reporting to other (junior) cashiers.

The same reporting form reflects information about the actual facts of the return of previously provided funds to the chief (senior) cashier.

As a rule, each employee of an organization who personally manages the cash register entrusted to him is assigned a separate KO-5 book, designed to record cash flow.

In KO-5, the chief cashier of the business entity makes the appropriate entries. This accounting register regularly reflects information about the actual procedures for the provision and return of funds carried out between the chief cashier of the organization and the lower-level cashiers responsible for maintaining the cash register in individual structural divisions of this organization.

Thus, the KO-5 form regularly records the following operations:

- At the very beginning of each operating day, the senior (chief, leading) cashier provides certain amounts of money to junior cashiers responsible for maintaining the cash register in individual departments. This money is usually issued to complete expense transactions. Having received these funds, the responsible junior cashier certifies this fact with his own signature, affixed to the KO-5 form itself.

- When the operating day in the organization ends, the responsible junior cashier, who previously received the accountable funds, sums up the results and returns to the chief cashier the unused amount of the cash balance, as well as other cash credited to his cash desk during this operating day. This fact is also recorded in the KO-5 book and certified by the personal signature of the chief cashier, affixed directly to the same accounting form.

How to fill out a journal of cash receipts and expenditures?

Filling out KO-5 is carried out by the chief cashier of a business entity according to a unified form approved by decree of the official statistical agency of the Russian Federation number 88 of 08/18/1998.

The sample provides for entering the necessary information into the appropriate columns of the table.

The accounting book itself consists of a title part, which is filled out according to an established template, and sheets containing tables with the necessary data and details.

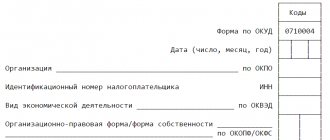

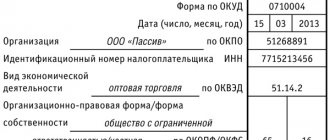

The title part of KO-5 provides for the following details:

- Name of the business entity filling out this form (name of organization, full name of individual entrepreneur).

- If a business entity has structural divisions, you should indicate exactly the division for which this book is being compiled. If there are no structural units, a dash is simply drawn.

- OKPO code of an economic entity according to Rosstat.

- The time period during which it is planned to fill out this book (for example, 2021).

- Full name of the chief (leading, senior) cashier, who is personally responsible for maintaining this form and, accordingly, regularly filling it out.

The KO-5 tabular form is regularly filled in in the appropriate columns (columns) with the following information:

- The date indicating the day when the chief cashier of a business entity and the junior cashier of the corresponding division transferred certain amounts of cash to each other (issuance/return).

- The cash balance available at the beginning of a particular trading day.

- The amount of money directly provided to the junior cashier (indicated in numbers/words).

- Signature of the junior cashier certifying the receipt of cash from the main person.

- The amount received in cash, recorded by a specific junior cashier and confirmed by PKO orders.

- Cash (amount) transferred by the junior cashier to the chief cashier at the end of this operating day. This includes the balance of unused funds accepted by the junior cashier at the beginning of the operating day, as well as the amount received in his cash desk and capitalized by PKO orders during the same day.

- The amount of cash paid by cash documents handed over to the chief cashier by the junior.

- You should display the total amount of money that the junior cashier transferred to the chief cashier at the end of the next operating day.

- Signature of the chief cashier, certifying the receipt of cash from the junior.

- The cash balance available at the end of a particular business day.

and sample filling

Download the accounting book for accepted and issued funds KO-5 – form.

Sample of filling out form KO-5 – .

Other forms of cash documents:

- KO-4 - cash book;

- KM-6 - certificate-report of the cashier-operator.

Instructions for filling

As for the procedure for filling out the book, it is quite simple and does not cause any particular difficulties for workers. On the front side of the document is the name of the organization, for which year this accounting register is maintained, the surname and initials of the cashier.

On the inner sheets, the journal is divided into two parts - incoming and outgoing :

- The receipt table (on even pages) contains information about the amount of money received by an ordinary cashier. Each operation is reflected by day, respectively, all of them have their own date. The second column reflects the amount of cash that is available as a balance at the department's cash desk. Then the amount of money transferred to the employee for cash transactions is written down and secured with his own signature. In addition, this part reflects data on receipt transactions that were carried out by the cashier of the structural unit throughout the day.

- The expense table (on odd-numbered pages) shows data related to the expenditure of funds on any operations. The most important columns in it are how much cash and paid documents were handed over by an ordinary cashier to a senior one, indicating the total amount for these two columns. These figures are checked and signed by the chief cashier. The last column contains the balance of available cash, which will be in the employee’s hands at the end of the working day. It is calculated as the balance at the beginning plus the amount of funds received and minus the amount of returned money and payment documents. The balance at the end of the day is exactly transferred to the receipt at the beginning of the next working day.

Here you can download the book form and a sample of how to fill it out for free.

It should be noted that this accounting register is compiled separately for each year , and balances from the previous year are transferred to the next.

Concept

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem , contact a consultant:

8 (800) 700 95 53

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FREE !

Information about financial transactions is entered into the cash book. The displayed data records all facts of transfer and reception of material assets between officials of the enterprise.

An example of such a transfer could be a department cashier receiving money from the head cashier at the beginning of the working day, and returning it at the end of the day. The accounting book is kept to maximum reflect the movement of material assets between officials. This form of accounting is widely used if the enterprise has several structural cash desks and one central one.

Rules for filling out a cash book

Even a novice cashier should not have any significant difficulties in filling out the accounting log.

Title

The title page contains information about:

- Business name;

- journal period;

details of the person responsible for filling it out.

The internal part of the journal consists of two parts - incoming and outgoing.

Sheet 1

Entrance area, which contains information about:

- about the amount of money received by the cashier;

- time and date of arrival;

- the amount that is added up to the final total for the day at the cash register;

- the amount transferred for cash transactions by the cashier with the obligatory presence of his signature;

- data on receipt transactions during the day;

Leave a comment on the document

Do you think the document is incorrect? Leave a comment and we will correct the shortcomings. Without a comment, the rating will not be taken into account!

Thank you, your rating has been taken into account. The quality of documents will increase from your activity.

| Here you can leave a comment on the document “Sample. Book of accounting of money accepted and issued by the cashier. Form No. ko-5", as well as ask questions associated with it. If you would like to leave a comment with a rating , then you need to rate the document at the top of the page Reply for |

Comment on the rating

Thank you, your rating has been taken into account. You can also leave a comment on your rating.

Is the sample document useful?

If the document “Sample.

Book of accounting of money accepted and issued by the cashier. Form No. ko-5" was useful for you, we ask you to leave a review about it. Remember just 2 words:

Contract-Lawyer

And add Contract-Yurist.Ru to your bookmarks (Ctrl+D).

You will still need it!

For questions regarding maintaining the valuables storage book 0402118

Answer Opinion of consultants.

The Bank correctly understands that when organizing the work of an additional office with two employees responsible for the safety of valuables and a cashier, the fulfillment of the obligation to reconcile accounting data with the data reflected in book 0402118 and the corresponding signing of book 0402118 cannot be assigned to the employees responsible for the safety of valuables and the cashier.

We believe that reconciliation of the amount of cash balance indicated in book 0402118 with accounting data should be carried out no later than the morning of the next business day.

Justification of the consultants' opinion.

According to Article 22 of Law No. 395-1, the internal structural unit of a credit organization (its branch) (hereinafter referred to as VSP) is its (his) unit located outside the location of the credit organization (its branch) and carrying out banking operations on its behalf, list which are established by regulations of the Bank of Russia, within the framework of the license of the Bank of Russia issued to the credit organization (regulations on the branch of the credit organization).

Part one of Article 5 of Law No. 395-1 includes, among other things, cash services for individuals and legal entities as banking operations.

The procedure for conducting cash transactions with the currency of the Russian Federation in cash, as well as the rules for storing, transporting and collecting cash in credit institutions on the territory of the Russian Federation are defined in Regulation No. 630-P, according to paragraph 1.11 of which employees of a credit institution and VSP must use document forms established by Directive No. 3352-U, as well as these Regulations, drawn up on paper or in the form of electronic documents using technical means, an automated system of a credit institution.

When registering on paper the book of the storage of valuables 0402118 (hereinafter referred to as book 0402118), the book of accounting of accepted and issued valuables 0402124 (hereinafter referred to as book 0402124), the control log of acceptance from protection and delivery to the protection of the storage of valuables 0402162 (hereinafter - journal 0402162), the sheets of the specified books and journal, before they begin to be maintained, are bound and numbered by an employee of the credit institution, VSP. Certification notes on the number of sheets in book 0402118, book 0402124, journal 0402162 must be signed by the manager (his deputy), the chief accountant (his deputy ) by the credit institution (or by authorized persons specified in the administrative document of the credit institution), as well as by the cash register manager (VSP cashier) and sealed with a seal (if any) or stamp of the credit institution, VSP. The storage of book 0402118 during the working day must be carried out by the cash register manager, the VSP cash employee, and at the end of the working day - in a storage room, a specially equipped safe room (hereinafter referred to as the valuables storage room), a VSP safe.

Documents used in cash transactions, executed in the form of electronic documents, must be signed by an employee (employees) of the credit institution, VSP, and the client using electronic signatures in accordance with Article 5 of Law No. 63-FZ. If it is not possible to sign with an electronic signature, documents used in cash transactions must be printed on paper by an employee of the credit institution, VSP and signed with the handwritten signatures of the employee (employees) of the credit institution, VSP, and the client, taking into account the requirements of these Regulations.

Registration of documents used in cash transactions in the form of electronic documents, their transfer between employees of the credit institution, VSP, as well as to the client, verification of the data contained in them, as well as storage of documents in the form of electronic documents, with the exception of documents provided for in Appendix 1 to Directive No. 2346-U, must be carried out by the credit institution, taking into account ensuring the storage of data contained in the automated system of the credit institution, and excluding the possibility of making corrections and unauthorized access to them.

In accordance with clause 17.7 of Regulation No. 630-P, upon completion of cash transactions, the cash register manager or VSP cash employee must reflect in book 0402118 the amount of the balance of cash located in the valuables vault, VSP safe

at the end of the working day,

taking into account the data from the cash turnover certificate 0402114

.

Before closing

vault of valuables, VSP safe

, officials responsible for the safety of valuables, VSP cashier must verify the actual availability of cash located in the vault of valuables, VSP safe with the data reflected in book 0402118

,

and certify

the amount of cash balance in book 0402118 with their signatures . Corrections in book 0402118 are certified by the signatures of the indicated persons (clause 17.8 of Regulations No. 630-P).

Balance amount

cash

indicated in book 0402118

,

the chief accountant (his deputy) (the employee keeping accounting records of transactions carried out in VSP) must check with the accounting data

and sign in book 0402118. If a discrepancy is detected between the actual availability of cash and the data in book 0402118 and accounting data, the head (his deputy) of the credit organization and the chief accountant (his deputy) must carry out the actions provided for in paragraph two of clause 1.10 of these Regulations [1] (clause 17.11 of Regulation No. 630-P).

Based on clause 16.1

Provisions No. 630-P, upon completion of cash transactions, cash register and supervisory employees must hand over to the cash register manager cash, questionable Bank of Russia banknotes, insolvent Bank of Russia banknotes, empty bags, reporting certificates 0402112 (certificates

0402114

), magazines 0402301, certificates 0402302, Registers of transactions with cash currency and checks, registers of transfers, documents on transactions made using payment cards, announcements 0402001, cash checks, cash orders 0401106, incoming cash orders 0402008, outgoing cash orders 0402009, statements for bags 0402300, invoices bags 0402300, printouts of automatic devices, receipt parts, expenditure parts of cash receipt orders 0402007, inventories of transported cash, control sheets 0402010, acts 0402145, acts of recalculation, statements for the exchange of cash, orders for the transfer of valuables 0402102, certificates 0402159, applications for the acceptance of questionable banknotes and an inventory of questionable banknotes.

In a credit institution, VSP, the cash register manager must draw up a certificate 0402114 according to the reporting certificates 0402112, certificates 0402302, taking into account cash receipt orders 0402008, cash outflow orders 0402009, receipts, expenditure parts of cash inflow orders 0402007 for transactions carried out by the cash register manager, certificate ki on documents in electronic form, acts 0402145 for identified surpluses, shortages of cash, dubious banknotes of the Bank of Russia, insolvent banknotes of the Bank of Russia. The VSP cash employee at the end of the working day in accordance with clause 6.1 of these Regulations must draw up certificate 0402114. Reconciliation of the amounts of cash turnover indicated in certificate 0402114 with accounting data must be certified by the signature of the chief accountant (his deputy) of the credit organization or the employee maintaining the accounting accounting of transactions carried out in VSP in certificate 0402114 (clause 16.2 of Regulation No. 630-P).

The documents listed in clause 16.1 of these Regulations must be generated no later than the next working day

or the first working day after a day off, a non-working holiday

in the file with cash documents

for the corresponding operational day (clause 16.3 of Regulation No. 630-P).

In accordance with paragraph 1.1 of Part III of Regulation No. 579-P, accounting transactions

performed by employees for whom the performance of such operations is specified in job descriptions (included in their job responsibilities).

This category includes workers engaged in receiving, processing, monitoring

settlement,

cash

and other

documents

, reflecting banking transactions on accounting accounts, with the exception of workers processing information using automation tools and not included in the structure of the accounting apparatus.

All accounting employees regarding the performance of accounting operations

and accounting

are subordinate to the chief accountant

of the credit institution.

Based on clause 1.2 of Part III of Regulation No. 579-P, the organization of the work of the accounting apparatus is based on the principle of creating one accounting unit (department, management), forming specialized departments, uniting employees in departments into operational teams, granting employees the rights of responsible executors, who are entrusted with the sole responsibility of filing and sign documents on the range of operations being performed, with the exception of documents on operations subject to additional control.

Clause 1.8 of Part III of Regulation No. 579-P defines the features of organizing accounting work when performing cash transactions

, including the monitoring by the controlling employee of cash transactions performed by accounting employees, with the exception of the case provided for in clause 2.5 of Regulation No. 630-P[2] (subclause 1.8.1), as well as the maintaining by the controlling employee of a cash journal for expense 0401705.

By virtue of subclause 1.9.8 of clause 1.9 of Regulation No. 579-P, the right of control

(first)

signatures

without limiting the amount of transactions on settlement and

cash documents

subject to additional control are ex officio managers and

chief accountants of credit institutions or authorized representatives on their behalf

.

Granting control rights

The (first)

signature

a particular

official does not exclude the possibility of this person

(with the exception of the chief accountant)

the functions of a responsible executor for a certain range of operations

.

In this case, he controls the documents on operations performed by other employees.

Due to the requirements of Article 24 of Law No. 395-1, a credit organization

(the parent credit organization of the banking group)

is obliged to create

risk and capital management systems,

internal control

, corresponding to the nature and scale of the operations carried out, the level and combination of risks accepted, taking into account the requirements established by the Bank of Russia for risk and capital management systems, internal control of the credit organization, banking groups.

Under internal control

in accordance with paragraph 1.1 of Regulation No. 242-P, we mean

activities

carried out by a credit institution (its management bodies, divisions and employees) and

aimed at achieving

the goals defined by paragraph 1.2 of this Regulation:

— efficiency and effectiveness of financial and economic activities when carrying out banking operations and other transactions, efficiency of asset and liability management, including ensuring the safety of assets

, banking risk management (subclause 1.2.1);

— reliability

,

completeness

, objectivity and timeliness of preparation and presentation of financial, accounting, statistical and other

reporting

(for external and internal users), as well as information security (protection of the interests (goals) of a credit organization in the information sphere, which is a set of information, information infrastructure, subjects carrying out the collection, generation, distribution and use of information, as well as systems for regulating the relations arising in this case) (subclause 1.2.2);

— exclusion of involvement

credit organization and the participation of its

employees in carrying out illegal activities

, including legalization (laundering) of proceeds from crime and the financing of terrorism, as well as timely submission of information in accordance with the legislation of the Russian Federation to government authorities and the Bank of Russia (subclause 1.2. 4).

The internal control system of a credit institution must include control over the distribution of powers when carrying out banking operations and other transactions (clause 3.1 of Regulation No. 242-P). The credit institution must ensure the distribution of job responsibilities of employees in such a way as to eliminate conflicts of interest

(a contradiction between the property and other interests of a credit organization and (or) its employees and (or) clients,

which may entail adverse consequences for the credit organization

and (or) its clients) and the conditions for its occurrence, the commission of crimes and the implementation of other illegal actions when carrying out banking operations and other transactions, as well as

granting the same division or employee the right to carry out banking operations and other transactions and register them and (or) reflect them in accounting

(subclause 3.4.2 of clause 3.4 of Regulation No. 242-P).

In addition, the Recommendations of the Basel Committee on Banking Supervision “Internal control system in banks: fundamentals of the organization” (brought to credit institutions by Letter No. 87-T) indicate that “an effective internal control system presupposes a clear division of responsibilities of employees and the exclusion of situations where the scope employee responsibility allows for a conflict of interest. Areas of potential conflict

interests

must be

identified, minimized and

brought under

strict and independent

control

”

(principle 6).

By virtue of clause 3.8 of Regulation No. 242-P, a credit institution must adopt internal documents on the main issues related to the implementation of internal control, among which Appendix 2 to this Regulation names the performance of cash transactions, collection of funds and other valuables.

According to clause 1.3 of Part III of Regulation No. 579-P, the accounting department of a credit organization must have employees who are responsible for subsequent control of completed accounting, including cash, transactions.

All accounting transactions made on the previous day must be fully verified within the next business day.

based on primary documents, records in personal accounts and in standard forms of analytical and synthetic accounting.

For personal accounts, it is checked whether all entries are confirmed by relevant documents that have been checked by authorized employees of the credit institution and signed by them when processing transactions, whether the relevant details and amounts of documents have been correctly transferred to personal accounts, whether incoming balances have been correctly transferred from the previous day and outgoing balances have been withdrawn balances - their compliance with the statement of account balances, the correctness of the execution of documents that served as the basis for reflecting account transactions, compliance with the rules for issuing account statements to clients, the correctness of making corrective entries, if they were made.

Based on clause 2.2 of Part III of Regulation No. 579-P, the daily balance sheet

, which

must be compiled

for transactions performed by the head office of the credit institution for the past day,

before 12 o'clock local time of the next business day

.

The organization of internal control and daily monitoring of its implementation in all areas of accounting and cash work is assigned to the chief accountant

. The methods and technical means used to implement internal control are determined by the credit institution itself, based on specific operating conditions, the nature of operations and their volume (clause 3.2 of Part III of Regulation No. 579-P).

According to paragraph 6 of Appendix 2 to Regulation No. 579-P, additional offices, according to an established schedule, transmit to the credit institution (branch) using automation tools the details of documents for reflection in account accounting with subsequent delivery of documents. Accounting documents on paper are generated in the prescribed manner and delivered to the credit institution (branch) in the manner and within the time frame determined by the credit institution (branch). The credit institution (branch) verifies the data recorded in the records with the documents. If errors are identified, corrections are made in accordance with the established procedure.

Based on the above, we come to the following conclusions.

Cases of assigning the duties of an accounting employee to a cash employee in the VSP of a credit organization are named in paragraph 2.5 of Regulation No. 630-P and do not provide for the registration of book 0402118.

Employees of the credit institution, certifying the amount of the cash balance with their signatures in book 0402118, confirm the completion of certain actions to reconcile the data reflected in book 0402118:

— officials responsible for the safety of valuables, the VSP cashier, check the actual availability of cash located in the valuables storage room, the VSP safe, with the data reflected in book 0402118. These persons are responsible for the safety of valuables;

— the chief accountant (his deputy) (the employee who keeps accounting records of transactions carried out in VSP) compares the accounting data with the data reflected in book 0402118. The chief accountant (his deputy) (the employee who keeps accounting records of transactions carried out in VSP) carries out control function.

With this division of powers, a conflict of interest between the performance of banking operations and their registration in accounting is eliminated.

When combining the responsibilities of an accounting and cash employee, conditions are created for concealing possible losses, their non-reflection in accounting accounts, and for the preparation of unreliable reports.

We believe that reconciliation of the amount of cash balance indicated in book 0402118 with accounting data should be carried out no later than the morning of the next business day. Such deadlines ensure proper control of the reflection of cash transactions on accounting accounts and allow you to draw up a balance on transactions for the past day before 12 o'clock local time on the next business day.

Documents and literature.

1. Law No. 395-1

– Federal Law of the Russian Federation dated December 2, 1990. No. 395-1 “On banks and banking activities”;

2. Law No. 63-FZ

— Federal Law of the Russian Federation dated April 6, 201. No. 63-FZ “On Electronic Signature”;

3. Regulation No. 630-P

— Regulations of the Bank of Russia dated January 29, 2018. No. 630-P “On the procedure for conducting cash transactions and the rules for storage, transportation and collection of banknotes and coins of the Bank of Russia in credit institutions on the territory of the Russian Federation”;

4. Regulation No. 242-P –

Regulations of the Bank of Russia 12/16/2003 No. 242-P “On the organization of internal control in credit institutions and banking groups”;

5. Instruction No. 2346-U -

Directive of the Bank of Russia dated November 25, 2009. No. 2346-U “On storing in a credit institution in electronic form certain documents related to the execution of accounting, settlement and cash transactions when organizing accounting work”;

6. Letter No. 87-T -

By letter of the Bank of Russia dated July 10, 2001. No. 87-T “On the recommendations of the Basel Committee on Banking Supervision.”

[1] In case of detection of surpluses, shortages of cash that raise doubts about the solvency of banknotes of the Bank of Russia (hereinafter referred to as dubious banknotes of the Bank of Russia), insolvent banknotes of the Bank of Russia during acceptance and processing at a credit institution, VSP cash generated and packaged cashiers, collectors in disposable safe packages, collection bags, special bags, cases, cassettes and other means for packaging cash, ensuring the safety of cash and not allowing it to be opened without visible signs of damage to the integrity of the packaging (hereinafter referred to as the bag), cash , formed and packaged by cashiers in packs of banknotes, bags with coins, cassettes with packs (spoons, banknotes), bags with coins, as well as identifying discrepancies between the actual availability of cash and the data of cash documents, accounting data (hereinafter referred to as the discrepancy between the amounts of cash) credit The organization must establish the reasons for the discrepancy in cash amounts and take measures to eliminate the discrepancy in cash amounts.

[2] An administrative document of a credit organization may assign to a cash employee the duties of an accounting employee in terms of drawing up and processing:

incoming and outgoing cash document;

currency cash order 0401106;

orders for the transfer of valuables 0402102;

cash register for receipt 0401704;

log books for accepted bags and empty bags 0402301;

certificates of accepted bags and empty bags 0402302.

When assigning the duties of an accounting employee to a cash employee

operations on a bank account or a client's deposit account must be carried out by this cashier using computer equipment in which a

control system is installed that excludes the cashier's sole access to transactions on a bank account

or a client's deposit account without the client's order.

Answers to the most interesting questions on our telegram channel knk_banki

Back to section