KBK for 2012

BCC for 2012, taking into account the changes that the Ministry of Finance of Russia reported in letter dated October 6, 2011 No. 02-04-09/4467.

| Payment Description | KBK for transfer of tax (fee, other obligatory payment) | KBK for transferring penalties for taxes (fees, other obligatory payments) | KBK for transferring a fine for a tax (fee, other obligatory payment) |

| VAT | |||

| VAT on goods (work, services) sold in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| VAT on goods imported into Russia (payment administrator – Federal Tax Service of Russia) | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| VAT on goods imported into Russia (payment administrator - Federal Customs Service of Russia) | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

| Excise taxes | |||

| Excise taxes on ethyl alcohol (including raw ethyl alcohol) from food raw materials produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on ethyl alcohol (including raw ethyl alcohol) from all types of raw materials, with the exception of food, produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcohol-containing products produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on tobacco products produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on motor gasoline produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on straight-run gasoline produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on motor gasoline, diesel fuel, motor oils for diesel and (or) carburetor (injection) engines produced in Russia (in terms of repayment of debt from previous years accrued before January 1, 2003) | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on passenger cars and motorcycles produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on diesel fuel produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on motor oils for diesel and (or) carburetor (injection) engines produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on wines produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on beer produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol over 25 percent (except for wines) produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol over 9 to 25 percent inclusive (except for wines), produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol up to 9 percent inclusive (except for wines), produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol over 9 percent (except for wines) when sold by producers, with the exception of sales to excise warehouses, in terms of amounts calculated for 2003 | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol over 9 percent (except for wines) when sold by producers to excise warehouses in terms of amounts calculated for 2003 | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol over 9 percent (except for wines) when sold from excise warehouses in terms of amounts calculated for 2003 | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Personal income tax | |||

| Personal income tax on income received by residents in the form of dividends from equity participation in the activities of organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Personal income tax on income received by non-residents in the form of dividends from equity participation in the activities of Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Personal income tax on income taxed at a rate of 13 percent, with the exception of income received by citizens registered as: – entrepreneurs; – private notaries; – other persons engaged in private practice | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Personal income tax on income taxed at a rate of 13 percent and received by citizens registered as: – entrepreneurs; – private notaries; – other persons engaged in private practice | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Personal income tax on income received by citizens who are not tax residents of Russia | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Personal income tax on income received in the form of: – winnings and prizes in competitions, games and other events for the purpose of advertising goods (works, services); – interest income on deposits in banks (except for time pension deposits made for a period of at least 6 months); – material benefits from saving on interest when receiving borrowed (credit) funds | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Personal income tax: – on income received in the form of interest on mortgage-backed bonds issued before January 1, 2007; – from the income of the founders of the trust management of mortgage coverage, which were received on the basis of the acquisition of mortgage participation certificates and issued by the mortgage coverage manager before January 1, 2007 | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Personal income tax on income received by non-residents, in respect of which tax rates established in agreements for the avoidance of double taxation are applied | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| UST paid for 2009 (including advance payment for December 2009) | |||

| Unified social tax credited to the federal budget | 182 1 0900 110 | 182 1 0900 110 | 182 1 0900 110 |

| UST, credited to the FSS of Russia | 182 1 0900 110 | 182 1 0900 110 | 182 1 0900 110 |

| Unified social tax included in the Federal Compulsory Compulsory Medical Insurance Fund | 182 1 0900 110 | 182 1 0900 110 | 182 1 0900 110 |

| UST included in the TFOMS | 182 1 0900 110 | 182 1 0900 110 | 182 1 0900 110 |

| Income tax | |||

| Income tax credited to the federal budget | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Profit tax credited to the budgets of constituent entities of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax for agricultural producers who have not switched to paying the unified agricultural tax, credited to the federal budget | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax for agricultural producers who have not switched to paying the Unified Agricultural Tax, credited to the budgets of the constituent entities of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax upon implementation of production sharing agreements concluded before the entry into force of Law No. 225-FZ of December 30, 1995 and which do not provide for special tax rates for crediting the specified tax to the federal budget and the budgets of constituent entities of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on the income of foreign organizations not related to activities in Russia through a permanent establishment, with the exception of income received in the form of dividends and interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received by Russian organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received by foreign organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received by Russian organizations in the form of dividends from foreign organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received in the form of interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Fee for the use of aquatic biological resources | |||

| Fee for the use of aquatic biological resources (excluding inland water bodies) | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Fee for the use of objects of aquatic biological resources (for inland water bodies) | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Fee for the use of fauna objects | |||

| Fee for the use of fauna objects | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Water tax | |||

| Water tax | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| MET | |||

| Oil | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Combustible natural gas from all types of hydrocarbon deposits | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Gas condensate from all types of hydrocarbon deposits | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Extraction tax for common minerals | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Anthracite | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Coking coal | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Brown coal | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Coal, excluding anthracite, coking coal and brown coal | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Other minerals | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Tax on the extraction of mineral resources on the continental shelf of Russia, in the exclusive economic zone of the Russian Federation, when extracting mineral resources from the subsoil outside the territory of Russia | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Mining tax on natural diamonds | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

| Unified agricultural tax | |||

| Unified agricultural tax | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Single tax with simplification | |||

| Single tax with simplified income | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Single tax simplified from the difference between income and expenses | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Minimum tax for simplification | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Tax in the form of the cost of a simplified patent | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| UTII | |||

| UTII | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Transport tax | |||

| Transport tax for organizations | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Transport tax for individuals | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Gambling tax | |||

| Gambling tax | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Organizational property tax | |||

| Property tax of organizations on property not included in the Unified Gas Supply System | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Property tax of organizations on property included in the Unified Gas Supply System | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Property tax for individuals | |||

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of intra-city municipalities of the federal cities of Moscow and St. Petersburg | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Property tax for individuals, levied at rates applicable to taxable objects located within the boundaries of urban districts | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Property tax for individuals, levied at rates applied to taxable objects located within the boundaries of inter-settlement territories | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Property tax for individuals, levied at the rates applied to taxable objects located within the boundaries of settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Property tax | |||

| Real estate tax levied on real estate located within the boundaries of the cities of Veliky Novgorod and Tver | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax | |||

| Land tax levied at a rate of 0.3 percent and applied to taxable objects located within the boundaries of intra-city municipalities of the federal cities of Moscow and St. Petersburg | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax levied at a rate of 0.3 percent and applied to taxable objects located within the boundaries of urban districts | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax levied at a rate of 0.3 percent and applied to tax objects located within the boundaries of inter-settlement territories | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax levied at a rate of 0.3 percent and applied to taxable objects located within the boundaries of settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax levied at a rate of 1.5 percent and applied to taxable objects located within the boundaries of intra-city municipalities of the federal cities of Moscow and St. Petersburg | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax levied at a rate of 1.5 percent and applied to taxable objects located within the boundaries of urban districts | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax levied at a rate of 1.5 percent and applied to tax objects located within the boundaries of inter-settlement territories | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax levied at a rate of 1.5 percent and applied to taxable objects located within the boundaries of settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Government duty | |||

| State duty on cases considered in arbitration courts | 182 1 0800 110 | 182 1 0800 110 | 182 1 0800 110 |

| State duty on cases considered by the Constitutional Court of the Russian Federation | 182 1 0800 110 | 182 1 0800 110 | 182 1 0800 110 |

| State duty on cases considered by constitutional (statutory) courts of constituent entities of the Russian Federation | 182 1 0800 110 | 182 1 0800 110 | 182 1 0800 110 |

| State duty on cases considered in courts of general jurisdiction by magistrates (with the exception of the Supreme Court of the Russian Federation) | 182 1 0800 110 | 182 1 0800 110 | 182 1 0800 110 |

| State duty on cases considered by the Supreme Court of the Russian Federation | 182 1 0800 110 | 182 1 0800 110 | 182 1 0800 110 |

| State duty for state registration of: – organizations; – individuals as entrepreneurs; – changes made to the constituent documents of the organization; – liquidation of the organization and other legally significant actions | 182 1 0800 110 | 182 1 0800 110 | 182 1 0800 110 |

| State duty for the right to use the names “Russia”, “Russian Federation” and words and phrases formed on their basis in the names of legal entities | 182 1 0800 110 | 182 1 0800 110 | 182 1 0800 110 |

| State duty for carrying out actions related to licensing, with certification in cases where such certification is provided for by the legislation of the Russian Federation, credited to the federal budget | 182 1 0800 110 | 182 1 0800 110 | 182 1 0800 110 |

| Pension contributions | |||

| Insurance contributions for compulsory pension insurance, paid in 2010 and credited to the Pension Fund of the Russian Federation to pay the insurance part of the labor pension | 392 1 0200 160 | 392 1 0200 160 | 392 1 0200 160 |

| Insurance contributions for compulsory pension insurance, paid in 2010 and credited to the Pension Fund of the Russian Federation for the payment of the funded part of the labor pension | 392 1 0200 160 | 392 1 0200 160 | 392 1 0200 160 |

| Insurance contributions for compulsory pension insurance in the amount determined based on the cost of the insurance year, paid in 2010 and credited to the Pension Fund of the Russian Federation for payment of the insurance part of the labor pension | 392 1 0200 160 | 392 1 0200 160 | 392 1 0200 160 |

| Insurance contributions for compulsory pension insurance in the amount determined based on the cost of the insurance year, paid in 2010 and credited to the Pension Fund of the Russian Federation for the payment of the funded part of the labor pension | 392 1 0200 160 | 392 1 0200 160 | 392 1 0200 160 |

| Insurance contributions for compulsory pension insurance paid for December 2009 and credited to the Pension Fund of the Russian Federation to pay the insurance part of the labor pension | 182 1 0200 160 | 182 1 0200 160 | 182 1 0200 160 |

| Insurance contributions for compulsory pension insurance, paid for December 2009 and credited to the Pension Fund of the Russian Federation for the payment of the funded part of the labor pension | 182 1 0200 160 | 182 1 0200 160 | 182 1 0200 160 |

| Contributions to compulsory social insurance | |||

| Insurance contributions for compulsory social insurance against industrial accidents and occupational diseases | 393 1 0200 160 | 393 1 0200 160 | 393 1 0200 160 |

| Insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity | 393 1 0200 160 | 393 1 0200 160 | 393 1 0200 160 |

| Contributions for compulsory health insurance | |||

| Insurance premiums for compulsory health insurance of the working population, credited to the budget of the Federal Compulsory Health Insurance Fund | 392 1 020 160 | 392 1 020 160 | 392 1 020 160 |

| Insurance premiums for compulsory medical insurance of the non-working population, credited to the budget of the Federal Compulsory Medical Insurance Fund | 392 1 0200 160 | 392 1 0200 160 | 392 1 0200 160 |

| Payments for subsoil use | |||

| Regular payments for the use of subsoil for the use of subsoil (rentals) on the territory of the Russian Federation | 182 1 1200 120 | 182 1 1200 120 | 182 1 1200 120 |

| Regular payments for the use of subsoil (rentals) for the use of subsoil on the continental shelf of the Russian Federation, in the exclusive economic zone of the Russian Federation and outside the Russian Federation in territories under the jurisdiction of the Russian Federation | 182 1 1200 120 | 182 1 1200 120 | 182 1 1200 120 |

| Payments for the use of natural resources | |||

| Payment Description | KBK for payment transfer | ||

| Payment for negative impact on the environment | 498 1 1200 120 | ||

| Payment for the use of aquatic biological resources under intergovernmental agreements | 076 1 1200 120 | ||

| Payment for the use of federally owned water bodies | 052 1 1200 120 | ||

| Income from auctions for the sale of shares in the total volume of quotas for catching (extraction) of aquatic biological resources newly permitted for use for industrial purposes, as well as in newly developed fishing areas | 076 1 1200 120 | ||

| Income received from the use of a market mechanism for the turnover of shares determined by federal executive authorities in the total volume of quotas for catch (production) of aquatic biological resources | 076 1 1200 120 | ||

| Income from the provision of paid services and compensation of state costs | |||

| Payment Description | KBK for payment transfer | ||

| Fee for providing information contained in the Unified State Register of Taxpayers | 182 1 1300 130 | ||

| Fee for providing information and documents contained in the Unified State Register of Legal Entities and the Unified State Register of Individual Entrepreneurs | 182 1 1300 130 | ||

| Fines, sanctions, payments for damages | |||

| Monetary penalties (fines) for violation of the legislation on taxes and fees provided for in Articles 116, 117, 118, paragraphs 1 and 2 of Article 120, Articles 125, 126, 128, 129, 129.1, 132, 133, 134, 135, 135.1 of the Tax Code of the Russian Federation | 182 1 1600 140 | ||

| Monetary penalties (fines) for violation of legislation on taxes and fees provided for in Article 129.2 of the Tax Code of the Russian Federation | 182 1 1600 140 | ||

| Monetary penalties (fines) for administrative offenses in the field of taxes and fees provided for by the Code of Administrative Offenses of the Russian Federation | 182 1 1600 140 | ||

| Monetary penalties (fines) for violation of legislation on the use of cash register equipment when making cash payments and (or) payments using payment cards | 182 1 1600 140 (to the Federal Tax Service of Russia) 188 1 1600 140 (to the Ministry of Internal Affairs of the Russian Federation) | ||

| Monetary penalties (fines) for administrative offenses in the field of state regulation of the production and turnover of ethyl alcohol, alcohol, alcohol-containing and tobacco products | 141 1 1600 140 (to Rospotrebnadzor) 182 1 1600 140 (to the Federal Tax Service of Russia) 188 1 1600 140 (to the Ministry of Internal Affairs of the Russian Federation) | ||

| Monetary penalties (fines) for violation of the procedure for handling cash, conducting cash transactions and failure to fulfill obligations to monitor compliance with the rules for conducting cash transactions | 182 1 1600 140 (to the Federal Tax Service of Russia) 188 1 1600 140 (to the Ministry of Internal Affairs of the Russian Federation) | ||

For information:

Directory of budget classification codes KBK for 2013, approved by order of the Ministry of Finance of Russia dated December 21, 2012 No. 171n Quick search for KBK codes for legal entities (LLC, CJSC) for 2013 Quick search for KBK codes for individual entrepreneurs for 2013

Which KBK to use in 2021

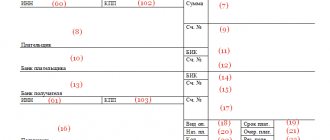

When filling out a payment slip for personal income tax, KBC is required to indicate the correct codes in order to avoid the accrual of penalties for late fulfillment of financial obligations. To avoid mistakes when filling out a payment order, check the table.

| Type of tax, payment | Code in 2021 |

| Personal income tax on employee income | 182 1 0100 110 |

| Penalty | 182 1 0100 110 |

| Fines | 182 1 0100 110 |

| Collection from individual entrepreneurs to OSN | 182 1 0100 110 |

| Penalty | 182 1 0100 110 |

| Fines | 182 1 0100 110 |

BCC “Penalty Tax Penalties”, as well as BCC for fines, differ from the basic values.

Code values often change (in this case, the Ministry of Finance issues an explanatory order), but sometimes they are retained for a longer period. Thus, in 2021, the same BCCs for personal income tax apply as in 2021, in accordance with Order of the Ministry of Finance No. 132n dated 06/08/2018.