All cash transactions of organizations must be carried out through cash register equipment. Strict reporting forms (SSR) are required for those institutions that accept cash directly, without using cash registers (Article 2 54-FZ of May 22, 2003). Budgetary institutions are no exception in this matter. All cash movements made without the use of cash registers are necessarily reflected in a special book - a journal of strict reporting forms, a sample of which we will consider step by step.

Who has the right to work without using a cash register?

The legislation limits the range of organizations that have the right to operate without the use of cash register equipment, but it is still quite wide. In particular, the following can carry out activities without using a cash register:

- individual entrepreneurs,

- enterprises providing services to the population

- companies organizing meals in schools, trading in kiosks, accepting glass containers, selling non-food products at markets, exhibitions, fairs, etc.

If an organization has exercised the right to work without cash register equipment, it must use strict reporting forms.

BSO storage

A specially equipped room is allocated for storing strict reporting forms. The BSO storage location is sealed (sealed) at the end of the working day.

It is best to store BSO in safes or in special rooms - this will avoid their theft or damage.

Each form must have a copy that is kept for five years.

The originals of strict reporting forms are also stored for at least five years.

Storage of BSO using automated systems

When registering BSO using an automated system, there is no need for all of the above operations when storing ordinary BSO. The automated BSO system must meet the criteria of clause 11. Decree of the Government of the Russian Federation No. 359 of 05/06/2008 (last edition of 04/15/2014).

These criteria include:

- the ability to protect the system from unauthorized access;

- the ability to identify and record transactions with BSO for 5 years;

- the ability to save data on BSO in the speaker’s memory.

However, BSOs printed using an automated system, but damaged, should, by analogy with printing BSOs, be stored in the organization’s safe.

What are forms and what are they for?

Strict reporting forms mean receipts that certify the receipt of funds from individuals. Each form always has two copies :

- one after filling is given to the client,

- the second remains in the organization.

The forms are relevant only for cash payments; for non-cash transfers, the use of such forms is impossible, as in relations between legal entities.

At their core, forms are an alternative to a cash receipt. At the same time, the use of forms is most interesting for small companies, since they allow them to save money spent on the purchase and maintenance of cash register equipment.

Forms are usually purchased in specialized stores, developed by organizations independently, or printed in printing houses in certain editions. All forms are included in the circulation in a certain chronology, numbered and registered in the accounting book.

How to take into account forms for an individual entrepreneur

In 2021, an individual entrepreneur no longer has to keep a cash book, since the device itself transmits the necessary data. But this does not mean that the individual entrepreneur should abandon the accounting journal: when receiving and issuing sheets, it is necessary to make appropriate notes. This applies to all types of activities of an individual entrepreneur, especially if he works under USO, UTII or a patent.

Beginning entrepreneurs often wonder: what is better to issue, forms or a cash register? The answer to this question cannot be unambiguous. Of course, a cash register is more practical and convenient, but you need to take into account that, firstly, it costs money, secondly, it needs to be registered with the tax office, thirdly, staff must be trained, and fourthly, an additional service agreement must be concluded with the central service center. and monitor the condition of the device. This is a rather complicated and costly procedure; moreover, in the end, the cash register will need to be submitted by contacting both the tax office and the central service center, collecting documents, etc. If you work exclusively with individuals and sales volumes are small, then it may be wiser to register BSO accounting book (we will provide a sample of filling out for individual entrepreneurs below). Despite the apparent complexity of working with sheets, everything is actually simple: you order them from a printing house, put them in a safe, keep a journal and give them out to sellers or managers as needed.

There is one more advantage that concerns individual entrepreneurs who are not tied to one point (providing field services) - it is not always possible or safe to carry a cash register with them. Forms are another matter - they can simply be stored in a vehicle and issued at the customer/buyer’s site. Using this link, you can fill out form 0504045 - fill in your data and enter it in the BSO accounting journal.

What to put in the book

This document contains all information regarding the forms, including their receipt (purchased or printed) and consumption (used for their intended purpose or damaged, unreliable, written off).

Representatives of some organizations mistakenly believe that information on the receipt and expenditure of funds, including specific amounts, must be entered into the form book. This is wrong.

This includes only data on the movement of forms (receipt at the printing house, registration of printed internal templates, issuance to financially responsible employees, etc.) and their quantity.

And everything related to the money received from their use is entered into another document - a book of income and expenses.

BSO logbook: filling rules

The journal is used to record the presence and movement of these forms. More specifically, the number of forms is indicated:

- received from the printing house

- spent (issued to the financially responsible person who is responsible for filling them out and issuing them to clients)

- spoiled (damaged or filled out with errors)

- written off (destroyed according to the rules established by law)

Some clarification is required here. As you know, the forms must indicate their number and series. When ordering from a printing house, the range of numbers and required series are usually determined by the customer. In most cases, the type of conventional BSO in the printing house has already been determined.

BSO accounting

In some cases, there are special forms for certain types of services. In others, it is said that the form must contain a certain set of details, but its form remains at the discretion of the entrepreneur. In the latter case, although your own version may be proposed that satisfies the requirements of the law, usually the printing house has already generated sample forms.

The journal does not record the issuance of completed forms to specific clients. At an enterprise, as a rule, a financially responsible person is appointed, who is given a certain number of forms, he fills them out and gives them to clients as needed. The company enters into a liability agreement with such a person. Damaged forms, as well as copies or stubs of used receipts, are stored in sealed bags for five years. Damaged forms are not allowed to be thrown away.

Write-off of those forms that have already been used is permitted after five years of storage. Usually it is customary to do this after five years and one month. However, they are not allowed to simply be destroyed. For this purpose, a commission is created at the enterprise, which carries out the destruction, drawing up an appropriate act about this and indicating the series and numbers of the destroyed documents.

The journal does not indicate data on income that was received in the process of providing services accompanied by the issuance of such forms. Only their quantitative movements and the remaining balance are reflected here.

Drawing up an accounting book

There is currently no single, mandatory form of book of accounting for strict reporting forms. Organizations have the right to develop it independently or use a unified template previously recommended for use (form 0504045). The second option is good because you don’t need to rack your brains over the structure and content of the book - all the necessary data is already included in it.

Filling out the accounting book and strict reporting forms

- The following are included in the document in order:

- date of book opening and closing (at the right time),

- name of company,

- its OKPO code,

- name of the form (receipt, sales receipt, etc.),

- conditional price per unit in rubles,

- account number through which the funds are transferred,

- form code.

- Next comes the main part, which contains a table of several columns and rows. It includes:

- date of data entry,

- from whom the forms were received or to whom they were issued (name of the organization or full name of the individual),

- the name of the document that served as the basis for their acceptance or issuance.

- Then there are the columns “receipt” and “expense” - information about the forms received by the organization, spent and written off is entered here, and the balance is entered at the end.

- Also, the person who handed over the forms or received them in their hands must put their signature in the book.

How are they used?

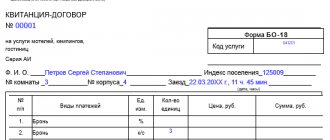

Legislation allows entrepreneurs and organizations to both use standard BSO forms and create them themselves. The standard form contains everything you need for proper formatting, so we recommend using it. However, nothing prevents you from creating it yourself. To do this, the document must indicate the following points:

- Full document name, series and number.

- Full name of the company (LLC), full name of the individual entrepreneur.

- For companies - legal address.

- Individual tax number for individual entrepreneurs or LLCs.

- Type of service provided or name of product.

- The cost of a service or product (each item separately and the total amount).

- Payment amount.

- The date the BSR was compiled or the transaction was completed.

- Full name of the individual entrepreneur or employee who is responsible for such operations.

- Wet printing (if available), other types of details.

This form can be ordered from a printing house. If printing is carried out in a printing house, then the paper must also contain information about the order:

- Circulation, year of issue.

- TIN and name of the printing house.

- Printing house address and order number.

Forms can also be produced using so-called “automated systems,” but the problem is that a regular printer cannot be used for this. The Russian Ministry of Finance puts forward the following requirements for automated systems:

- Protection of equipment from unauthorized use by third parties.

- Storing the series and number of the BSO form.

- Recording and identification of actions performed with BSO for 5 calendar years.

The book is bound and signed, the sheets are necessarily numbered.

In fact, only printing houses fall under these requirements - there are practically no automated systems in Russia that meet such requests. Forms printed in the printing house are handed over to the responsible employee before the commission. Acceptance is carried out by the financially responsible person appointed by the relevant order for the enterprise on the day the documents are received. The order also indicates the chairman and members of the commission; it is signed by the individual entrepreneur or the head of the LLC. After this, a procedure is carried out for reconciliation with invoices upon receipt (you need to count the exact number of forms and check their series numbers). Upon completion of acceptance, an act is drawn up, on the basis of which they are registered by registering in the appropriate book. Storage of received and registered papers is carried out:

- In locked safes.

- In metal cabinets.

- In equipped rooms.

The owner must organize such storage conditions under which damage or loss of strict reporting documents will be impossible. At the end of the working day, the safe or room must be sealed and sealed to prevent access by unauthorized persons.

Please note that copies of the BSO and their tear-off spines must also be preserved under special conditions. Usually they are put into special bags and sealed, after which they are stored for 5 years (if necessary, they will need to be presented to the inspection authorities). At the end of this period, a separate act for writing off the papers is drawn up, after which they are destroyed. Damaged forms are subject to the same procedure. To draw up the act, a commission is also involved, which is appointed by the relevant order. After the destruction procedure, a corresponding entry is made in the accounting journal.