Types of reports, sanctions and fines

All mandatory reports that businessmen submit can be divided into the following groups:

- Financial statements.

- Tax reporting.

- Reporting to extra-budgetary funds.

- Statistical reporting.

Each category has its own measures of influence on violators. Sanctions can be of the following types:

- Fixed fines.

- Fines depending on reporting indicators.

- Blocking of accounts.

Responsibility for the violation lies with both the organization and the guilty official. Usually this is the manager, but the chief accountant can also be punished.

Financial statements

Legal entities must submit financial statements for 2021 to the Federal Tax Service and statistics authorities.

Therefore, if a businessman does not meet the deadline, he will be punished twice. In addition, the guilty officials will be fined separately.

- If the report is not submitted to the Federal Tax Service, the fine will be 200 rubles for each reporting form (clause 1 of Article 126 of the Tax Code of the Russian Federation). In this case, small enterprises will have an “advantage”, because for them the mandatory “set” of financial statements is limited to the balance sheet and form No. 2.

- For failure to submit financial statements to statistics, a larger fine is provided - from 3,000 to 5,000 rubles, regardless of the number of forms (Article 19.7 of the Code of Administrative Offenses of the Russian Federation).

- In both cases, the guilty officials will be fined from 300 to 500 rubles. (Articles 15.6 and 19.7 of the Code of Administrative Offenses of the Russian Federation).

The procedure described above is valid for the last time when submitting reports for 2021.

Next, the changes introduced by the law of November 28, 2018 No. 444-FZ will come into effect.

- Accounting statements will need to be submitted only to the Federal Tax Service.

- The “electronic” delivery format will become mandatory. An exception is made only for small enterprises, which can still report for the last time “on paper” for 2021.

The question arises: since there will be no need to submit financial statements to statistics in the future, then for violation of deadlines there will only be a “symbolic” fine in the amount of 200 rubles. for a document?

But everything is not so simple... The bill provides for a sharp tightening of sanctions for late submission of financial statements. Fines imposed on organizations and officials will amount to tens and even hundreds of thousands of rubles.

Sanctions will depend on the length of the delay and whether the unsubmitted reports are subject to mandatory audit.

The maximum fine provided for by the bill will be up to 700,000 rubles. for organizations and up to 50,000 rubles. - for officials.

It is assumed that the new law will come into force on January 1, 2021, i.e. will apply to violations committed upon submission of reports for 2021 and later.

Sanctions for failure to submit reports to the tax authorities

The fine for failure to submit reports is established under Articles 119 and 126 of the Tax Code of the Russian Federation and Articles 15.5 and 15.6 of the Code of Administrative Offenses of the Russian Federation.

Please note that if the deadline for submitting reports falls on a weekend or holiday, the reports must be submitted on the first working day after the weekend (holiday).

If an organization does not operate, it must still submit reports established by the Tax Code of the Russian Federation. Usually such reporting is called “zero”. The penalty for failure to submit “zero” reporting is the same as in all other cases.

It should be taken into account that if an organization does not conduct business, it does not have cash flows through the current account and cash desk of the organization, it can submit a single simplified declaration, thus reducing the number of “zero” reports and the amount of possible sanctions in cases where reporting on some or for some reason it will not be delivered. If the violation is committed for the first time, liability under the Code of Administrative Offenses may be replaced by a warning.

Information on fines for failure to submit reports is presented in Table 1: (click to expand)

| Reporting type | Type of violation Fine | Regulatory document | ||

| minimum | calculation | maximum | ||

| Declaration, calculation of insurance premiums | 1,000 rub. | 5% for a full or partial month | 30% of the tax amount according to the declaration | Article 119 of the Tax Code of the Russian Federation |

| 300 – 500 rub. | – | – | Article 15.5 of the Code of Administrative Offenses of the Russian Federation | |

| Calculation of advance payments, information on the average number of employees | 200 rub. | – | – | Article 126 of the Tax Code of the Russian Federation |

| 300 – 500 rub. | – | – | Article 15.6 of the Code of Administrative Offenses of the Russian Federation | |

| Calculation of 6-NDFL | 1,000 rub. | For each full or incomplete month | – | Article 126 of the Tax Code of the Russian Federation |

| 300 – 500 rub. | – | – | Article 15.6 of the Code of Administrative Offenses of the Russian Federation | |

| Financial statements | 200 rub. | – | – | Article 126 of the Tax Code of the Russian Federation |

| 300 – 500 rub. | – | – | Article 15.6 of the Code of Administrative Offenses of the Russian Federation | |

An additional sanction for failure to submit a declaration is the suspension of transactions on all accounts of the taxpayer (Read also the article ⇒ Procedure and deadlines for preparing consolidated financial statements for 2021).

Suspension of operations is carried out if the declaration is not submitted within a period exceeding 10 days from the date established for submitting the declaration.

Just in case, let us remind you that for failure to submit financial statements to the statistical authorities there is even more punishment - a warning or the imposition of an administrative fine on the organization in the amount of 3,000 to 5,000 rubles. (Article 19.7 of the Code of Administrative Offenses of the Russian Federation).

Tax reporting

Sanctions for late tax reports depend on their category:

- Tax returns and calculation of mandatory insurance contributions (DAM).

In this case, the amount of the fine is “tied” to the amount of tax (contribution) indicated in the report. For each full or partial month of delay, the violator will pay 5% of the amount due to the budget or payment fund (Clause 1 of Article 119 of the Tax Code of the Russian Federation).

If the declaration reflects an insignificant amount, or the report is generally “zero”, then a fixed minimum fine is applied - 1000 rubles.

The upper limit is 30% of the amount indicated in the report, i.e. In case of long delays (more than six months), the fine will no longer increase.

However, if the delay exceeded 10 days, then penalties will not be the biggest problem for a businessman. Indeed, in this case, tax authorities have the right to block his accounts (clause 1, clause 3 and clause 3.2, article 76 of the Tax Code of the Russian Federation)

- Other tax calculations.

These are mandatory tax reports and are not declarations. It must be borne in mind that the declaration is submitted at the end of the tax period, and all “interim” reports, even if they have a similar form, do not apply to declarations.

This applies, for example, to quarterly reports on income or property taxes, because For both of these payments, a one-year tax period is established. But quarterly forms for VAT and UTII are already declarations, because The tax period for them is a quarter.

The calculations also include Form 2-NDFL and information about the average number of employees.

The fine for failure to submit payments is 200 rubles. for each document (clause 1 of article 126 of the Tax Code of the Russian Federation). Account blocking does not apply in this case.

- Form 6-NDFL.

Separately, sanctions have been established for failure by tax agents to submit income tax calculations in Form 6-NDFL.

The fine in this case will be 1000 rubles. for each month of delay (clause 1.2 of Article 126 of the Tax Code of the Russian Federation). If the delay exceeds 10 days, then the tax authorities can block the accounts, as in the case of violations of declarations (clause 3.2 of Article 76 of the Tax Code of the Russian Federation).

As for responsible officials, for them fines for violation of deadlines for all types of tax reports will be the same - from 300 to 500 rubles. (Article 15.5, 15.6 of the Code of Administrative Offenses of the Russian Federation).

Forgot to send a declaration

If a company or entrepreneur misses the deadline for submitting a tax return, it will be punished. Moreover, the type of fiscal obligation for which a report has not been submitted does not matter to representatives of the Federal Tax Service.

The fine for failure to submit reports to the tax service is equal to 5% of the unpaid amount of the fiscal obligation, which is subject to payment to the state budget, for the unsubmitted declaration. Moreover, 5% will be charged for each month of delay, full and incomplete.

However, the maximum amount of penalties cannot exceed 30% of the amount of unpaid tax. But there are also minimal restrictions. Even if all obligations to the budget are repaid, the inspectorate will impose a penalty of 1,000 rubles. That is, if there is a failure to submit tax reports, a fine of 1000 rubles is the minimum punishment.

There are exceptions! So, how much will an organization or entrepreneur have to pay for late submission of reports to the tax office? If the income tax return for the reporting period is not submitted on time, you will be fined 200 rubles. A similar penalty awaits for failure to provide calculations for advance payments of property taxes. Such norms are enshrined in paragraph 1 of Art. 126 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service dated August 22, 2014 No. SA-4-7/16692.

Reporting to extra-budgetary funds

All employers must report quarterly to the Federal Social Insurance Fund of the Russian Federation on contributions “for injuries”. The sanctions here are similar to those applied for violations when filing tax returns: 5% of the amount payable is taken for each overdue month. The minimum is also 1000 rubles, and the maximum is 30%.

The only difference is that the basis for calculating the fine will not be the entire amount indicated in the calculation, but only that accrued over the last three months (Article 26.30 of the Law of July 24, 1998 No. 125-FZ “On Compulsory Social Insurance...”) .

In addition, employers - legal entities must annually send confirmation of their main type of activity to the Federal Social Insurance Fund of the Russian Federation in order for the fund to establish a contribution rate for them “for injuries”.

There is no penalty for late payment in this case. However, the fund then has the right to set a tariff for the violator at the maximum rate, based on all types of activities that are indicated for this organization in the state register (clause 13 of the Russian Government Resolution No. 713 dated December 1, 2005).

All employers must submit personal information about insured persons to the Pension Fund using the SZV-M and SZV-experience forms.

Fines for violation of deadlines are the same and amount to 500 rubles. for each employee included in the report (Article 17 of the Law of April 1, 1996 No. 27-FZ “On individual (personalized) accounting...").

Officials for delaying any reports sent to extra-budgetary funds will be punished with a fine of 300 to 500 rubles. This is provided for in Art. 15.33 and 15.33.2 of the Code of Administrative Offenses of the Russian Federation.

Fines for failure to submit reports

If tax reporting is not received on time, tax authorities will issue fines to the company in accordance with Art. 119 Tax Code of the Russian Federation:

- if the tax is transferred in full, but the declaration for it is not submitted, a fine of 1,000 rubles is provided;

- If the tax is not paid in full or at all, a fine of 5% of the amount owed is issued for each month of delay. In this case, the fine cannot be more than 30% of this amount and must not be less than 1,000 rubles;

- if the taxpayer has not submitted a zero return, the fine is 1,000 rubles.

Statistical reporting

In addition to financial statements, businessmen must submit various specialized forms to the statistical authorities. Their list will be determined by Rosstat and depends on the type of activity and scale of the business.

The fines in this case are much higher than for failure to submit financial reports. In case of a primary violation, the organization will be fined in the amount of 20,000 to 70,000 rubles, and the official - in the amount of 10,000 to 20,000 rubles.

If the delay is repeated, then the organization may be charged an amount from 100,000 to 150,000 rubles, and from the official - from 30,000 to 50,000 rubles. (Article 13.19 of the Code of Administrative Offenses of the Russian Federation).

In addition, if the delay led to a distortion of the results of Rosstat’s consolidated reporting, then the violator may be required to compensate for the damage incurred by the department (Article 3 of Law No. 2761-1 of May 13, 1992 “On Liability ...”).

It should be noted that in accordance with Art. 2.4 of the Administrative Code of the Russian Federation, individual entrepreneurs “by default” (unless otherwise specified in a specific article of the Administrative Code) bear administrative responsibility as officials.

Tax penalties

To begin with, let us determine that the nature of such a violation depends on what kind of reporting was untimely submitted to the competent authorities. Tax fines are a type of tax sanctions that are applied in accordance with Art. 114 of the Tax Code of the Russian Federation to taxpayers for offenses committed in this area. Such fines are paid by the enterprise solely on the basis of the decision of the Federal Tax Service, and the costs of paying for such a violation in accounting are included in the expenses of the reporting period.

The amount of fines is presented in Table 1.

Table 1 – Calculation of the amount of penalties for late submission of reports (click to expand)

| Situation | What does NK say? |

| The tax on the declaration was paid on time, but the declaration itself was submitted in violation of the deadlines | The fine in this case for any type of tax is 1000 rubles. This is the minimum size. Paid for every month |

| The tax was paid partially or not in full, the declaration was not submitted on time | The amount of penalties is calculated based on the difference between the amount that was paid and what should have been paid. Interest is paid for each full or partial month of delay. The percentage is 5%. But the fine cannot exceed 30% of the total tax amount. |

The main thing to understand is that the amount of the fine, despite being an expense, does not reduce the size of the tax base. The correspondence of accounts itself takes place using accounts 99, 68 and 69.

An example of a cycle of transactions that an enterprise must make as a result of paying a fine for late filing of an income tax return:

- Calculation of VAT fine: D-t 99, K-t 68;

- The accrued fine has been paid: D-t 68, K-t 51;

Important: the amount of penalties accrued for taxes cannot be attributed to tax sanctions in accordance with the Tax Code, therefore, to reflect entries for penalties, not 99, but 91 accounts are used.

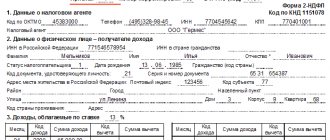

Form 6-NDFL

Legal entities and individuals may be fined for late submission of a report in Form 6-NDFL, which reflects all the employee’s income tax accruals. And the minimum amount of the fine in accordance with the Tax Code is 1000 rubles for each month. And even if the reporting, for example, is overdue by 5 months and 2 days, then you will have to pay the fine in 6 months.

But such a fine is charged monthly in case of failure to submit reports. The following question arises: what if the reporting is submitted, but incorrectly, and it needs to be clarified? In this case, the amount of the fine will not be 1000, but 500 rubles for each month of an incorrectly submitted form.

The costs of paying the fine will also be charged to account 99, expenses (

Conclusion

For violation of reporting deadlines, the law provides mainly for various penalties. They are imposed both on the organization and on the responsible officials.

Fines can be either fixed or calculated based on the amounts reflected in the declarations or the number of individuals included in the report

In addition, accounts may be blocked for delays in a number of tax reports.

Today, maximum fixed fines (up to 150,000 rubles) are established for violations of deadlines for submitting statistical reports.

But if the bill developed by the Ministry of Finance is adopted, then fines for delays in accounting statements in some cases will amount to up to 700,000 rubles.