Failure to withhold personal income tax as a result of a calculation error

In case of an error with the calculation, you must withhold tax until the end of the year from the next cash payments to an individual.

If there is no such possibility before the end of the year (for example, an error in the calculations was discovered in December), the individual must be informed about the impossibility of withholding tax and his tax office (Article 216, paragraph 5 of Article 226 of the Tax Code of the Russian Federation). At the same time, they can be fined for failure to withhold only if the individual had the opportunity to withhold tax when paying income. If there was no such opportunity (for example, the income was paid in kind), then it cannot be held accountable. But if such an opportunity arose before the end of the year, and the tax agent still did not withhold the tax, in this case he also faces a fine (Article 123 of the Tax Code of the Russian Federation, paragraph 21 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 No. 57).

If personal income tax is not withheld from payments to a dismissed employee upon final settlement with him and no payments were made to him by the end of the year, the organization should also send a message about the impossibility of withholding personal income tax to the inspectorate and this employee (Article 216, paragraph 5 of Article 226 of the Tax Code of the Russian Federation ).

Deadline for filing 2-NDFL

If the 2-NDFL certificate reflects information about income from which tax is not withheld, then the deadline for its submission differs from the usual certificate, namely, until March 1 of the following reporting year (Article 216, paragraph 5 of Article 226 of the Tax Code of the Russian Federation, section II Procedure for filling out certificate 2-NDFL).

In case of violation of the deadline for submitting a certificate, inspectors may impose a fine of 200 rubles for each certificate.

If the last day of the deadline falls on a weekend, then the last day for submitting the 2-NDFL certificate will be the next next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

Help 2 Personal income tax: what will be the fine for failure to submit

Legal entities that paid wages to individuals during the reporting year. persons are required to submit report 2 to the Tax Inspectorate at the place of registration. The day of submission is determined by law in Article 230, paragraph 2; for 2021, the deadline for submitting personal income tax 2 is April 1, 2021.

If a business entity transferred profits to employees, but for unknown reasons could not withhold income tax, personal income tax certificate 2 is submitted a month earlier until March 1, this is regulated in Article 226, paragraph 5.

Otherwise, the organization faces a fine for failure to submit a 2nd personal income tax report, including account blocking. The fact that personal income tax has not been withheld is reported to the fiscal authorities and the information is forwarded to individuals. face.

In this article, we will consider the penalties and the extent to which the tax inspectorate applies to the counterparty.

Message about impossibility of withholding tax:

Fine for unreliable information in 2nd personal income tax

When creating a report, you must carefully fill out the data; before submitting it to the tax office, you should independently verify control compliance and compare the indicators with other reporting forms.

If a legal entity independently discovers an inaccuracy and submits a “clarification” to the tax office, the fine in this case will not be applied to paragraph 2 of the same article.

Remember that there are a number of points when the size of the penalty is reduced: these are technical errors that did not occur intentionally. The application of this norm is affected by the absence of debt from the counterparty to the treasury for other taxes, as well as the revision of the punishment and the business reputation of the organization.

What information is considered unreliable?

The regulations do not explain for what inaccuracies sanctions are applied to a business entity. If we approach it formally, then these are errors in the amount of earnings or income tax, and errors in the telephone number of a legal entity or the registered address of an employee, as well as for late issuance of a certificate. The situation is similar with the indication of incorrect abbreviations in Form 2 of the personal income tax.

The following information presented in 2 personal income tax is considered unreliable:

The details indicated in declaration 2 are incorrect and untrue; errors in the formation of information; incorrect financial information regarding accrued income, applicable rates, deductions, codes; errors in calculating income tax.

Legal entities must report to the tax office on time, and first carefully check the information for each employee and the completion of the report fields. This will prevent the application of a fine to the counterparty of the management person.

Who and how to send a message about the impossibility of retention

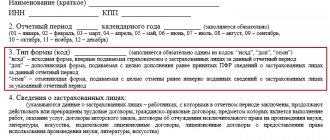

The peculiarity of issuing a 2-NDFL certificate when it is impossible to withhold tax is only that:

— in the “Sign” field, code 2 is indicated instead of the usual code 1. Sign “2” means that certificate 2-NDFL is submitted as a message to the tax inspectorate that income has been paid to an individual, but tax has not been withheld from it (clause 5 of Art. 226 Tax Code of the Russian Federation);

— in section 3 – the amount of income from which tax is not withheld;

- in section 5 - the amount of tax calculated but not withheld.

The form must be sent to:

- an individual from whose income personal income tax is not withheld;

- to the tax authority (clause 5 of article 226 of the Tax Code of the Russian Federation).

A message can be sent to an individual in any way that can confirm the fact and date of sending the message. The specific method is not defined by tax legislation. We recommend sending it by a valuable letter with a description of the attachment, or handing it in person and receiving a receipt on a copy of the document indicating the date of delivery.

The message is sent to the tax authority (clause 5 of Article 226, clause 2 of Article 230, clause 1 of Article 83 of the Tax Code of the Russian Federation):

- organization - at its location, and if the message is submitted in relation to a person working in its separate division - at the location of this division;

- individual entrepreneurs - to the inspectorate at their place of residence, and in relation to employees engaged in activities subject to UTII or PSN - to the tax authority at the place of registration in connection with the implementation of such activities.

The message can be submitted in the form of a paper document (in person or by post with a list of attachments) or in electronic form via telecommunication channels (clause 3 of the Procedure approved by Order of the Federal Tax Service of the Russian Federation dated September 16, 2011 No. ММВ-7-3 / [email protected] ) .

After sending a message to the tax authority in form 2-NDFL with attribute “2”, at the end of the year, in general order, it is necessary to submit a certificate 2-NDFL with attribute “1” (Article 216, paragraph 2 of Article 230 of the Tax Code of the Russian Federation, paragraphs 1.1 clause 1 of the Order of the Federal Tax Service of the Russian Federation dated October 30, 2015 No. ММВ-7-11/ [email protected] , section II of the Procedure for filling out the 2-NDFL certificate, letter of the Federal Tax Service of the Russian Federation dated March 30, 2016 No. BS-4-11/5443).

If the 2-NDFL certificate will be submitted by the successor for the reorganized organization, then in accordance with the changes made by Order of the Federal Tax Service of the Russian Federation dated January 17, 2018 No. ММВ-7-11 / [email protected] , in the “Sign” field he should indicate “4” ( Chapter II of the Procedure for filling out the 2-NDFL certificate).

General information ↑

The abbreviation personal income tax stands for quite simply - personal income tax. That is, from a certificate issued in form 2-NDFL, you can find out all the information about the income of a particular individual.

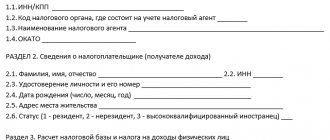

A standard certificate must contain the following sections:

- complete information about the employer who is a tax agent (all details, official name);

- all data regarding the employee (last name, first name and patronymic, as well as other data necessary for reporting);

- income taxed at a rate of 13% (income tax);

- various types of deductions, marked with the appropriate digital code;

- the entire amount of income received by an individual for which the certificate is drawn up.

Who rents

All organizations, regardless of their form of ownership and type of activity, that pay wages to employees, submit a certificate of this kind to the tax authorities at the place of registration.

Also, individual entrepreneurs are subject to the law obliging to tax the income of individuals.

Regardless of how many workers are hired and how much wages are paid.

The following are required to report accrued or withheld personal income tax:

- all organizations that are residents of the Russian Federation;

- notaries practicing privately;

- lawyers who have created their own law offices;

- various types of foreign divisions of large companies, if any personal income tax payer received profit from them in any form.

Foreign companies are covered regardless of whether they are permanent establishments or not.

The legal basis for this is letter of the Ministry of Finance of Russia No. 03-04-06-01/299 (dated November 18, 2009).

If foreign companies have the status of separate divisions, then 2-NDFL certificates are submitted to the Federal Tax Service at the place of their actual location.

There is no requirement to submit information on individuals receiving wages from tax agents in the following cases:

- Payments are made to employees who are required to independently pay personal income tax (notaries, lawyers - according to Article No. 227 of the Tax Code of the Russian Federation).

- An individual received income that was not subject to any tax (listed in Article No. 217 of the Tax Code of the Russian Federation).

In all other cases, the employer is required to submit a 2-NDFL certificate within the period established by law. Otherwise, penalties will be applied to him in accordance with the relevant articles of the Code of Administrative Offences.

Due dates

In accordance with the Tax Code of the Russian Federation, or rather clauses. 5 p. 1 art. No. 21, organizations are required to provide the tax service with a certificate in the prescribed form no later than 90 days after the end of the year for which they must report.

It is very important to remember that various types of commercial enterprises that use the simplified tax system and pay UTII must also report in the prescribed form. The deadlines for submitting 2-NDFL vary depending on the purpose for which it is being done:

The deadlines for submitting 2-NDFL vary depending on the purpose for which it is being done:

- The tax return (in form 2-NDFL) is submitted to the relevant authorities no later than April 1 of the year following the reporting year (Article No. 230 of the Tax Code of the Russian Federation).

- If a certificate is submitted in the form in question to formalize a deduction on an application, then it must be submitted no later than April 1.

- If the deduction is required in an organization, then you can submit it to the tax certificate within a year - just receive a notification from the tax office and provide it at your place of work.

The deadline for submitting the certificate in form 2-NDFL must be observed. Thus, failure to provide information is punishable by quite serious fines.

Normative base

Payment of personal income tax is carried out in accordance with current legislation. There is a fairly extensive regulatory framework that regulates the amount of this tax. As well as a reporting form (including 2-NDFL certificate).

The main document that serves as the basis for paying tax is the order of the Federal Tax Service SAE-3-04/706 dated October 13, 2006.

This order fully complies with the provisions present in clauses 2 and 3 of Art. No. 230 Tax Code of the Russian Federation. Its main provisions include:

- certificate form No. 2-NDFL approved at the legislative level (a sample is available in special annexes and recommendations);

- approved format of the certificate in form 2-NDFL in electronic form (based on XML);

- a recommendation for tax agents to promptly report to the tax authorities about the impossibility of withholding tax.

This order also cancels the one previously in force under the number SAE-3-04/616 (dated November 25, 2005). All its provisions are considered invalid.

A fine will be imposed for any errors in 2-NDFL

Good afternoon, dear readers. The next tax year has ended, according to the results of which the company reports for all its employees to the Federal Tax Service.

And today we will talk about 2-NDFL certificates (When there are more than 25 employees, certificates are provided electronically. If there are less than 25 people, you can submit them on paper), more precisely, about the mistakes and mistakes made when submitting these certificates.

Types of errors in the 2-NDFL certificate

The first option is being late.

If the first of April has passed and you have not submitted certificates to the tax office (they are accepted by the Federal Tax Service according to the attached register), prepare to pay a fine.

If your certificates do not pass the entrance control for any reason (whether in paper or electronic form you report to the tax office) and there is no time left to correct the documents on time, then these 2-NDFL certificates will also be considered not provided.

During incoming control, the completion of all required fields of the document is checked.

Based on the results of the inspection, a protocol is issued or sent through the electronic document management operator, indicating the not accepted certificates and errors found in them.

The second option is, in fact, errors.

For example:

- There is a TIN, but for another person;

- A letter is missing from the surname;

- The street was renamed last year;

- Errors in rounding of income received, etc.

The 2-NDFL certificates accepted from you (entrepreneurs) are then subjected to a second (office) inspection. Tax inspectors check documents against databases to identify all inaccuracies and violations. Previously, it was enough to simply submit corrected documents. Since 2021, an accountant’s mistake began to cost 500 rubles for each certificate.

How to avoid fines

So what should we do? Wait for the desk audit report? Of course not. We submitted the initial certificates and met the allotted deadline. This means that two hundred rubles have already been “saved” for each employee.

Now, without haste, we check each document again. There is no specific deadline for submitting adjustments, but you must meet the deadline before receiving the results of the tax inspector’s desk audit.

Since 2021, there are two types of clarifying certificates:

- Cancelling;

- Corrective.

Canceling clarifying certificates

From the name itself it is clear that the meaning of this certificate is to cancel the one submitted earlier (the initial certificate 2-NDFL was simply superfluous). The updated certificate form now includes the “adjustment number” field.

When submitting the initial certificate, “00” is entered in the field. When submitting a cancellation certificate “99”. Next, you need to fill out section 1 “Data about the tax agent” and section 2 “Data about the individual - recipient of the income.” The remaining help topics are left blank

Corrective clarifying certificates

To correct the information submitted in the initial certificate, you need to submit a corrective one. In the “adjustment number” field, in this case, the numbers from “01” to “98” are entered, depending on what kind of correction is being made on the account.

The number of the corrective certificate corresponds to the primary one, but the date will be new. Any inaccuracy in the provided certificate leads to a whole chain of violations, and as a result, correctional documents.

Let's look at some of them:

Example 1. Field “taxpayer status”.

It would seem like such a small thing, because the amounts are written down, the tax is withheld, why bother? The “status” sign in the certificate is indicated as “1”, i.e. resident and employee tax is withheld at a rate of 13%.

note

We submit a corrective certificate 2-NDFL with attribute 1 and “non-resident taxpayer status (2).” But not only. The accountant cannot withhold the remaining 17% of personal income tax from the employee, since the reporting period has ended. Therefore, a certificate with attribute “2” is submitted. In which fields 1 and 2 are filled in similarly.

Field 3 indicates income that was not previously included in the tax base. In field five - the amount of calculated and not withheld tax.

Example 2. After submitting 2-NDFL reports, the accounting department discovered its mistake.

In honor of his fiftieth birthday, the employee was presented with a valuable gift in the amount of 5,000 rubles (exceeding the limit of 4,000 rubles). But the amount is 1000 rubles. was not taken into account as income and no tax was assessed. This means we submit a corrective certificate 2-NDFL with attribute “1”, where in the “income…” field we add the amount of this gift.

We recalculate the amount of the taxable base and calculated tax. We indicate the amount of personal income tax not withheld. Since you did not withhold tax for the gift, you need to fill out a certificate with attribute “2”, which also indicates the amount of personal income tax not withheld.

Example 3: Your company issued an interest-free loan (or simply forgave an unpaid statement) to an individual who is not an employee (maybe a contractor).

In this case, you must submit a 2-NDFL certificate with sign “2” for the amount of income received by this individual. And also inform the taxpayer in writing about his debt to the budget. However, it is necessary to clarify that there are no penalties for failure to report.

Example 4. It turns out that the accountant did not indicate the benefits available to the employee (deduction for minor children).

Thus, he withheld excess personal income tax from the employee. In this situation, you need to submit a corrective certificate, from which the amount of tax overpaid to the budget will be visible.

Example 5. An employee applied to his Federal Tax Service for a personal income tax refund.

After conducting a desk check, he was refused. The reason for the refusal is a discrepancy in the address. As a result, the employee did not receive his money on time. And you will have to pay a fine and submit a corrective certificate.

Fine for unreliable information in 2nd personal income tax

When creating a report, you must carefully fill out the data; before submitting it to the tax office, you should independently verify control compliance and compare the indicators with other reporting forms.

If an inspector finds false information in the certificate, sanctions in the amount of 500 rubles will be applied to the counterparty, this is reflected in Article 126.1, paragraph 1.

If a legal entity independently discovers an inaccuracy and submits a “clarification” to the tax office, the fine in this case will not be applied to paragraph 2 of the same article.

Remember that there are a number of points when the size of the penalty is reduced: these are technical errors that did not occur intentionally. The application of this norm is affected by the absence of debt from the counterparty to the treasury for other taxes, as well as the revision of the punishment and the business reputation of the organization.

Signs in form 2-NDFL

Let’s assume that the company reporting personal income tax issued in 2021, i.e. in the reporting period, any non-cash prize to an individual. It is not possible to withhold tax in this case. How can this be reflected in the 2-NDFL certificate to avoid a fine? It is necessary no later than March 1, 2021 to submit to the Federal Tax Service and send to the individual a certificate in form 2-NDFL with sign 2 noted in it. It means that the tax agent organization failed to withhold the required amount from the payer. If tax is withheld, then indicator 1 is indicated.

What is the fine for failure to provide 2-personal income tax in 2020

If you do not follow the rule for submitting a 2-NDFL certificate established by the current legislation of the Russian Federation, then the consequences can be quite serious.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem, contact a consultant:

+7 (St. Petersburg)

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and!

General information ^

The abbreviation personal income tax stands for quite simply - personal income tax. That is, from a certificate issued in form 2-NDFL, you can find out all the information about the income of a particular individual.

A standard certificate must contain the following sections:

complete information about the employer who is a tax agent (all details, official name); all data regarding the employee (last name, first name and patronymic, as well as other data necessary for reporting); income taxed at a rate of 13% (income tax); various types of deductions, marked with the appropriate digital code; the entire amount of income received by an individual for which the certificate is drawn up.

Who rents

All organizations, regardless of their form of ownership and type of activity, that pay wages to employees, submit a certificate of this kind to the tax authorities at the place of registration.

Also, individual entrepreneurs are subject to the law obliging to tax the income of individuals.

Regardless of how many workers are hired and how much wages are paid.

The following are required to report accrued or withheld personal income tax:

all organizations that are residents of the Russian Federation; notaries practicing privately; lawyers who have created their own law offices;

The procedure for correcting errors in Help 2-NDFL

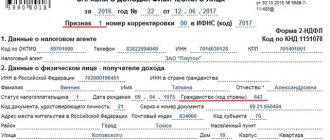

The procedure has established new rules for correcting errors, for which the “Adjustment number” field is provided in the header of the 2-NDFL Certificate:

- when drawing up the primary form of Certificate 2-NDFL, “00” is entered;

- when drawing up a corrective Certificate 2-NDFL, instead of the previously submitted one, a value one more than that indicated in the previous Certificate in form 2-NDFL (“01”, “02” and so on) is indicated;

- when drawing up a canceling Certificate 2-NDFL, the number “99” is entered instead of the previously submitted one.

The corrective form of Certificate 2-NDFL is submitted to correct errors in the primary form. And canceling - to cancel information that did not need to be submitted at all.

If, after sending Certificate 2-NDFL via telecommunication channels, it was not accepted by the tax authority (a protocol containing a description of format control errors was received), then it is necessary to submit not an adjustment, but a new certificate with the same number, indicated in the “Adjustment number” field. the value “00”, but indicating the new date. That is, there is no need to submit a correcting Certificate 2-NDFL, since for this individual the Certificate 2-NDFL was not accepted by the tax inspectorate and it is necessary to re-send the data (clause 14 of the order of the Federal Tax Service of Russia dated September 16, 2011 No. ММВ-7-3/ [email protected] ).

Responsibility for submitting certificates in Form 2-NDFL with errors

Organizations that are tax agents are required to submit to the tax authority at the place of their registration (clause 2 of Article 230 of the Tax Code of the Russian Federation) a certificate in form 2-NDFL (approved by Order of the Federal Tax Service of Russia dated October 2, 2018 N ММВ-7-11/ [email protected] ) annually no later than March 1 of the year following the expired tax period.

For the submission by a tax agent to the tax authority of documents containing false information, liability is provided in the form of a fine in the amount of 500 rubles. for each submitted document containing false information.

This responsibility also applies when submitting information in Form 2-NDFL with distorted amounts of income, taxes and tax deductions (clause 1 of Article 126.1 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service of Russia dated December 9, 2016 N SA-4-9/ [ email protected] , clause 3 of Letter of the Federal Tax Service of Russia dated 08/09/2016 N GD-4-11/14515).

Thus, if a tax agent does not submit an updated certificate in time to the tax authority in Form 2-NDFL, he may be issued a fine of 500 rubles. for each submitted document containing false information.

However, if unreliable information in the 2-NDFL certificate did not lead to non-calculation or incomplete calculation of the tax, adverse consequences for the budget, or violation of the rights of individuals, the tax agent may apply to the application of mitigating circumstances to him in accordance with clause 1 of Article 112 of the Tax Code of the Russian Federation (Letter of the Federal Tax Service dated 08/09/2016 No. GD-4-11/14515).

HELP! FAILURE TO DELIVERY 2-NDFL ON TIME

Dear Irina, the answer to your question:

Tax liability for violation of deadlines for submitting tax returns (Article 80 of the Tax Code of the Russian Federation), which is established by the legislation on taxes and fees, provides for the following types of sanctions:

Sanctions applied to the organization: fine 100 rubles. for each submitted declaration in violation of the established deadline and (or) unsubmitted tax return, if submitted within a period not exceeding 180 calendar days from the deadline for its submission established by tax legislation, and if the organization conducted activities and its reporting is not zero, then the fine will be 5 % of the amount of tax subject to payment (surcharge) on the basis of this declaration, for each full or partial month from the day established for its submission. In this case, the total amount of penalties cannot exceed 30% of the amount specified in the declaration and be less than 100 rubles. (Clause 1 of Article 119 of the Tax Code of the Russian Federation) If a zero declaration is submitted within a period exceeding 180 calendar days after the expiration of the deadline established by tax legislation for the submission of such a declaration, then penalties are not applied to the organization, however, if the organization conducted activities and its reporting is not zero, then the fine will be equal to 30% of the amount of tax payable (additional payment) on the basis of the declaration, plus 10% of the amount of tax for each full or partial month of delay starting from the 181st day. (Clause 2 of Article 119 of the Tax Code of the Russian Federation)

But even in case of violation of the deadlines for submission or failure to submit reports, you should understand that you will still have to submit the declarations, since without providing a complete set of reports you will not be able to contact the tax office and reconcile with the tax authorities, obtain the necessary certificates (including and about the absence of debts on taxes and fees), register cash register equipment, switch to registration with another tax authority, and much more! Administrative liability for violation of the deadlines for submitting a tax return established by the legislation on taxes and fees entails the imposition of an administrative fine on the head and chief accountant of the organization. (Article 15.5 of the Code of Administrative Offenses of the Russian Federation) The amount of the fine is from 3 to 5 minimum wages (300 - 500 rubles).

Suspension of transactions on bank accounts. If the delay in filing a tax return exceeds two weeks, then in addition to tax and administrative responsibility, the tax authority has another tool in its arsenal to influence the taxpayer who did not submit the tax return on time. The tax authority may make a decision on the taxpayer to suspend transactions on his bank accounts. (Clause 2 of Article 76 of the Tax Code of the Russian Federation) Such a decision paralyzes the activities of the organization for a significant period of time.

The answer is on the company’s website: https://www.bs-st.ru/answers/?r45_id=363

How to avoid liability for submitting false certificates in Form 2-NDFL

A tax agent is exempt from liability if he independently identifies errors and submits updated documents before the moment he learns that the tax authority has discovered that the information is unreliable.

That is, updated documents must be submitted by the tax agent before the tax authority requests explanations regarding the discovery of errors in the certificate in Form 2-NDFL (clause 2 of Article 126.1 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of Russia dated June 30, 2016 N 03-04-06/38424 , Federal Tax Service of Russia dated July 19, 2016 N BS-4-11/13012).

In what form should the 2-NDFL adjustment be submitted?

The adjusted (updated) certificate 2-NDFL must be submitted in the form that was in force in the tax period for which the corresponding changes are made and this certificate is submitted (clause 5 of the Procedure for submitting information on the income of individuals and the amount of tax on personal income and messages about the impossibility of withholding tax, about the amounts of income from which tax was not withheld, and the amount of unwithheld tax on personal income, approved by Order of the Federal Tax Service of Russia dated October 2, 2018 N ММВ-7-11/ [email protected] ).

For example, if in 2021 you need to submit an adjustment for 2-personal income tax for 2021, then you must submit the corrective certificate in the form that was in force in 2017.

What can you be fined for?

A tax agent (organization or individual entrepreneur) may be held liable in the form of fines in two cases related to the timing:

- the calculation is not presented at all,

- payment was submitted late.

Tax penalties for organizations and individual entrepreneurs

The amount of financial sanctions for 2021 is 1 thousand rubles for each month of late payment. Thus, the fine for late submission of 6-NDFL, if the delay is 6 months, will be equal to 6 thousand rubles. This mechanism for calculating sanctions is specified in paragraph 1.2 of Article 126 of the Tax Code of the Russian Federation.

Tax inspectors will impose a fine within 10 working days from the date the tax agent submitted the report. They are not required to wait until the end of the desk audit.

If you do not submit the payment within 10 days from the due date, the tax inspectorate also has the right to block the bank account of the tax agent (clause 3.2 of Article 76 of the Tax Code of the Russian Federation). The Federal Tax Service of Russia clarified this in a letter dated August 9, 2021 No. GD-4-11/14515.

If there is false information in 6-NDFL

The fine for each payment with false information is 500 rubles. But if you discovered an error and submitted an updated calculation before the tax inspectors noticed it, there will be no sanctions (Article 126.1 of the Tax Code of the Russian Federation).

Inspectors may impose a fine due to any error in the calculation in Form 6-NDFL. Inaccuracy in income and deduction codes, total indicators. But in some cases, inspectors reduce the fine, citing mitigating circumstances (clause 1 of Article 112 of the Tax Code of the Russian Federation). These are cases when the tax agent, due to an error (Letter of the Federal Tax Service of Russia dated August 9, 2021 No. GD-4-11/14515):

- did not underestimate the tax;

- did not create adverse budgetary consequences;

- did not violate the rights of individuals.

Responsibility for failure to issue a certificate

The employer is obliged to hand over the certificate to the employee on the day of his dismissal from work. But if the employee continues to work, then in this case the tax code does not provide for the deadline for issuing this certificate. But the labor code still stipulates the deadline for issuing a document to an employee if an application has been received from him. This should take no more than 3 days from the date of receipt of the application.

The tax office does not have the right to punish an employer for lately issuing a certificate. But the labor inspectorate has the power to bring the employer to administrative responsibility. To do this, the employee must apply to the labor inspectorate to protect his rights.

In some organizations, the accounting department independently issues these documents to its employees almost immediately after the reporting period. The employee has the right to further dispose of it at his own discretion. Others practice storing these documents in the archives of the enterprise and handing them over to employees only after the employee applies for a 2-NDFL certificate.

This video will tell you about the possibility of recovery for errors in 2-NDFL:

What is considered as failure to submit a report?

Failure to submit a report will be considered if:

- failure by the employer to comply with such an obligation, including failure to submit separate reports for separate divisions>;

- delivery after the due date.

In relation to 6-NDFL, violations (not regarded as failure to submit) will also be considered:

- Inclusion of false information in the report. Responsibility for it will arise if the reporting person does not correct the report before the tax authority identifies this error (clause 2 of Article 126.1 of the Tax Code of the Russian Federation).

- Violation of the method of reporting. Only those employers whose number of employees is less than 25 people can submit it on paper (Clause 2 of Article 230 of the Tax Code of the Russian Federation). The rest must report electronically.

Sanctions for failure to submit a report

The fine for 6-NDFL, not submitted or submitted late, is determined according to the rules of clause 1.2 of Art. 126 of the Tax Code of the Russian Federation. Its text prescribes a fine of 1,000 rubles. for each full or partial month, counted from the last day of the due date.

However, if the delay exceeds 10 working days, the violator may also be deprived of the opportunity to use a current account (clause 3.2 of Article 76 of the Tax Code of the Russian Federation).

For unreliability of the data included in the calculation, the report submitter will be fined 500 rubles. in relation to one report with such data (clause 1 of Article 126.1 of the Tax Code of the Russian Federation).

Violation of the method of submitting a report will result in a fine of 200 rubles. for each such report (Article 119.1 of the Tax Code of the Russian Federation).

In addition, it is possible to apply administrative sanctions to officials of the employer-organization. Their value will be from 300 to 500 rubles. for one person (Article 15.6 of the Code of Administrative Offenses of the Russian Federation).

Penalty for failure to submit 2-NDFL

If the Federal Tax Service records the absence of final information on the income of one or more employees from a tax agent, the company or individual entrepreneur will be held accountable - they will be fined for each missing form. The 2-NDFL certificate does not apply to tax returns, therefore, in its absence, movement through the accounts of the tax agent cannot be stopped.

The fine for a 2-NDFL certificate that the tax agent forgot/did not want to submit, or submitted with a delay, is established by clause 1 of Art. 126 of the Tax Code of the Russian Federation. Its size is 200 rubles. for each document not submitted. For example, an employer forgot to generate a certificate for two employees dismissed at the beginning of the year, and their data was not included in the register. If discrepancies are detected, the Federal Tax Service will issue a fine in the amount of 400 rubles. (200 rub. x 2).

If the certificates were submitted, but the inspectors found inaccuracies in them, the tax agent will have to pay 500 rubles to the budget. for each unreliable document (justification - Article 126.1 of the Tax Code of the Russian Federation). The situation can be resolved without a fine if the enterprise or individual entrepreneur identifies the error before the tax authorities do it, that is, before the end of the desk audit. In this case, you must submit a corrective certificate.

The fine for 2-NDFL (2018) may be an element of administrative punishment of officials. In Art. 15.6 of the Code of Administrative Offenses of the Russian Federation provides for penalties for:

- untimely transmission of information to the tax authority;

- refusal to notify the Federal Tax Service about the results of activities;

- incompleteness of the information displayed in the submitted documents.

The amount of material sanctions within the framework of administrative measures for officials is in the range of 300-500 rubles. If the offense was the result of the action or inaction of a government employee or a notary, then they will be subject to a fine in the amount of 500 to 1000 rubles.

If, based on the results of the declaration, you have tax to pay

If, based on the results of the declaration, you have tax to pay, but you have not filed a declaration, then:

1. According to Article 119 of the Tax Code of the Russian Federation (“Failure to submit a tax return”), you face a fine of 5% of the tax amount for each month of delay (starting from May 1), but not more than 30% of the total amount.

2. If you have not filed a declaration and also have not paid the tax by July 15, then you face a fine of 20% of the tax amount under Article 122 of the Tax Code of the Russian Federation (“Non-payment or incomplete payment of tax amounts (fees)”).

It is important to note here that this penalty can only be applied if the tax office has discovered non-payment of tax. If, before notifying the tax authority, you discovered it yourself, paid the tax and penalties, then the tax authority does not have the right to apply this fine to you.

Note: this same article of the tax code may entail a fine of 40% of the tax amount (instead of 20%) if the failure to pay was committed intentionally. However, in practice, it will be quite difficult to prove the intentionality of non-payment to the tax authority.

Please note that this fine can only be issued if the tax authority itself discovers that you have not filed a return. If you filed a declaration and paid the tax and penalties before he sent you a notice, he has no right to issue a fine for concealing income.

3. If you did not file a declaration and also did not pay the tax by July 15, then you will also have to pay an income tax penalty in the amount of 1/300 of the refinancing rate of the Central Bank of the Russian Federation for each overdue day (after July 15).

4. If you had to pay tax in the amount of more than 900 thousand rubles. (for example, you sold an apartment received as an inheritance), but did not file a declaration and did not pay the tax by July 15, then you may also fall under Article 198 of the Criminal Code of the Russian Federation (Evasion of taxes and (or) fees from an individual).

Example: in 2021 Muromtsev A.I. inherited an apartment and immediately sold it for 3 million rubles. The amount of tax that Muromtsev had to pay upon sale: 3 million rubles x 13% = 390 thousand rubles. Muromtsev did not know that he had to file a return with the tax authority and pay income tax and, accordingly, did nothing.

At the end of July 2021, Muromtsev received a notification from the tax office that he must declare the sale of the apartment.

If Muromtsev immediately after receiving the notification files a declaration and pays the tax and penalties, then he only faces a fine of 5% of the tax for each overdue month after filing the declaration: 3 months (May, June, July) x 5% x 390 thousand rubles = 58,500 rubles.

If Muromtsev does not submit a declaration, then the tax authority will have the right to hold him accountable under Article 122 of the Tax Code of the Russian Federation and collect an additional fine of 20% of the tax amount (78 thousand rubles).

Mitigating circumstances to reduce the fine

According to the provisions of paragraph 1 of Art. 114 of the Tax Code of the Russian Federation, a tax sanction is a measure of responsibility for committing a tax offense. If there is at least one mitigating circumstance, the amount of the fine shall be reduced by no less than two times compared to the amount established by the relevant article of the Tax Code of the Russian Federation.

In this case, the following circumstances are recognized as mitigating liability for committing a tax offense:

- committing an offense due to a combination of difficult personal or family circumstances; - committing an offense under the influence of threat or coercion or due to financial, official or other dependence;

- difficult financial situation of an individual held accountable for committing a tax offense;

- other circumstances that the court or tax authority considering the case may be recognized as mitigating liability (clause 1 of Article 112 of the Tax Code of the Russian Federation).

Thus, the list of mitigating circumstances is open-ended; they include any circumstances that the court or tax authority considering the case may be recognized as mitigating liability (Article 112 of the Tax Code of the Russian Federation).

From the analysis of this norm it follows that circumstances mitigating liability can be recognized as those that prevent a person from fulfilling the obligations assigned to him by the Tax Code of the Russian Federation (a combination of difficult personal or family circumstances, threat, coercion, difficult financial situation, etc.).

According to the explanations of financiers, the qualification of the actions of a tax agent who made an error when filling out form 2-NDFL depends on the actual circumstances. The issue of bringing to liability must be considered taking into account all circumstances, including mitigating liability (Letter of the Ministry of Finance of the Russian Federation dated April 21, 2016 No. 03-04-06/23193).

Important!

The presence of such circumstances should not be typical under normal conditions of business of the company. Tax officials must take into account the presence of mitigating circumstances in the event of providing false information, which did not lead to non-calculation or incomplete calculation of personal income tax, adverse consequences for the budget, violation of the rights of individuals (Clause 1 of Article 112 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service of the Russian Federation dated 08/09/2016 No. GD-4-11/14515).

Why you shouldn’t be fined for 2-NDFL

According to the legislation of the Russian Federation, the Federal Tax Service does not have the right to apply penalties to tax agents who incorrectly indicated the employee’s passport number in the report if it is possible to identify an individual by full name and tax identification number, as well as other information.

Fines are provided for the following violations:

- the report contains incorrect amounts of calculated and withheld income tax;

- an incorrect PFDL rate was applied to the taxpayer;

- violation of the rights of an individual to receive tax deductions;

- difficulty in identifying employees due to incorrectly entered TIN, full name, etc.

It is worth considering that if an employee does not have a tax identification number (he is a non-resident of the Russian Federation), it is not indicated in the report. And this is not considered an error.

Tags: accountant, job description of the general director, tax, personal income tax, order

2-NDFL: fine for late submission

Reports to the Federal Tax Service in Form 2-NDFL are submitted within the following deadlines:

- Until April 1 of the year following the reporting year, if income tax was withheld from the employee’s income.

- Until March 1 of the year following the reporting year, if personal income tax was not withheld from the employee’s income.

Violating these deadlines is prohibited.

According to the Tax Code of the Russian Federation, Art. 126 clause 1, if 2-NDFL reporting is submitted untimely, a fine of 200 rubles is provided. for each document.

It is worth considering that for untimely submission or failure to provide a report at the request of the Federal Tax Service of Russia, the court may hold the violator administratively liable:

- in the amount of 100-300 rubles. — for individuals;

- in the amount of 300-500 rubles. — for officials (managers, their deputies and others).

Therefore, you should not neglect the rules specified in the legislation of the Russian Federation,

Sanctions for failure to provide a certificate

Employers with hired employees are considered tax agents and therefore it is their responsibility to provide 2-NDFL certificates for their employees within the time limits established by law. And also maintain accounting records for the enterprise in accordance with legal requirements.

If, nevertheless, for various reasons, the organization was unable to provide information on all employees or did not report at all, then monetary penalties should be imposed on officials. The amount of such a penalty is quite high and depends on the degree of violation.

- For example, a fine of 300-500 rubles may be imposed on an official.

- If such an employee works in local government bodies, then the fine will be 500 - 1000 rubles.

- In cases where penalties are imposed on an individual, their amount can range from 100 to 300 rubles.