List of codes in the 2-NDFL certificate in 2021. Explanation.

The main information contained in the certificate is salary calculations by types that have a special coding. The list of such codes can be found in Order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/ [email protected] (as amended on October 24, 2017). In addition, this legal document also contains codes for deductions provided in accordance with the law, which must also be included in the certificate.

The most common codes:

- code 1010 - dividends;

- code 126 - deduction for the first child;

- code 127 - deduction for the second child;

- code 2000 - remuneration for labor activity;

- code 2002 - bonuses;

- code 2003 - remuneration from profit;

- code 2010 - remuneration under civil and process agreements;

- code 2012 - vacation payments;

- code 2013 - compensation for vacation not provided;

- code 2300 - sick leave benefits (except for maternity benefits);

- code 2510 - payment by the employer of property rights or services for an employee;

- code 2720 - gifts;

- code 2760 - financial assistance to employees and retired employees;

- code 2762 - one-time assistance from the employer at the birth (adoption) of a child;

- code 4800 - other income;

- code 503 - deduction from financial assistance to employees and retired employees.

- code 501 - deduction indicates receiving a gift from an organization or entrepreneur

How to fill out income codes

An individual’s income includes all payments in cash and in kind, as well as material benefits.

Income in the 2-NDFL certificate is indicated in the context of each month. If the employee had several types of income

paid by the enterprise, then each income is indicated under its own code given in Appendix No. 1 to the Order of the Federal Tax Service of the Russian Federation dated September 10, 2015 No. ММВ-7-11 / [email protected] (the most common):

- dividends – “1010”;

- salary – “2000”;

- production award – “2002”;

- payment under a civil contract – “2010”;

- vacation pay – “2012”;

- sick leave benefit – “2300”.

This is not the final list of income codes for the 2-NDFL certificate. But Appendix No. 1 lists only the main types of income. If the company pays income for which there is no code

(additional payments up to the amount of salary or minimum wage when paying benefits for temporary disability or an increased amount of daily payments), then in 2-NDFL the code “4800” is indicated - other income.

If an employee is paid tax-free income within the limit, then this amount is not indicated in the 2-NDFL certificate. If the amount exceeds the non-taxable limit

, then the full amount is indicated in the personal income tax reporting using the appropriate code.

What are the differences between the 2021 certificate and the 2021 certificate?

In 2021, to generate 2-personal income tax for 2021, you need to use the certificate form approved by the Order of the Federal Tax Service of the Russian Federation dated October 2, 2018 No. ММВ-7-11/ [email protected] It differs from the form that was used for certificates created in 2021 for 2021

The main changes in the certificate include the following points:

- The document form has two forms depending on who the user is - the tax office or an employee. At the same time, employees are presented with a form that is similar to the 2017 form, but information is excluded from it - the certificate number, its sign, adjustment number, Federal Tax Service code, information about confirming the right to reduce personal income tax, fixed advance payments. It’s called “Certificate of income and tax amounts of an individual.”

For the Federal Tax Service, a modified form on two sheets is used:

- the first sheet is called “Certificate of income and tax amounts of an individual (form 2-NDFL)”;

- the second sheet is called “Appendix. Information on income and corresponding deductions by month of the tax period";

- the first sheet contains basic information about the certificate, personal information about the employee and employer, general data on the amount of accrued income and withheld tax. The second sheet is intended for monthly reflection of information on income and deductions according to the corresponding codes;

- Some columns were added to the document for the Federal Tax Service, namely information about the reorganized company, taxpayer status, deductions provided by the employer;

- columns concerning the taxpayer’s registration address were removed from the document for the Federal Tax Service;

- in the certificate, all deductions, including standard ones, are combined into one block;

- the certificate for the Federal Tax Service must indicate a document according to which the powers of the signing official are confirmed.

Attention! According to the certificate for employees, the information was reduced by removing unnecessary fields, and for the Federal Tax Service, the information was combined, which, by changing the structure, is now contained not in 5, but in 3 blocks and an Appendix.

New form, rules and form 2 personal income tax in 2021

The certificate in 2021 has a new format according to Order of the Federal Tax Service of the Russian Federation dated 10/02/2018 No. ММВ-7-11/ [email protected] , which is applied from the moment it comes into force, namely from 01/01/2019.

Main changes in the new form:

- for the tax inspectorate, the form is divided into two sheets, and for employees the document is formed on one sheet;

- the field for entering the name of the tax agent has been expanded, and his TIN and KPP have been moved to the “header” of the document;

- New columns have been added to information about the employer regarding its reorganization or liquidation. The legal successor of the business entity must also indicate its information, namely the name, TIN and KPP;

- the block was modified to reflect personal information about the employee, and the columns that indicated information about the place of registration were excluded from the information;

- detailed information on the amounts of income and deductions for each month is transferred to a separate sheet as an appendix;

- the block concerning information on standard, social and property deductions has been expanded;

- A change has been made to the certificate barcode.

Thus, the form of the certificate for submission to the inspection has undergone significant changes, and for transmission to employees the form of the document has been slightly shortened. The coding for income and deductions remains the same for 2021 compared to 2021.

Where do you need Form 2-NDFL?

2-NDFL is needed by different users, including:

- employers who report to the tax office on accruals and deductions made for each employee. The provided certificates indicate that the business entity has entered into official labor relations with its employees and pays the amounts due to them in accordance with the requirements of labor legislation. In addition, the document confirms the 2-NDFL income codes for 2021, the calculation of personal income tax on them and its payment to the state budget;

- tax inspectorate, which checks employers' compliance with labor and tax laws. According to regulatory legal acts, the employer must submit the 2-personal income tax forms generated for employees within the established time frame. If the employer does not do this, the inspectorate applies penalties to him;

- employees who have the right to a tax deduction and use 2-NDFL with deduction codes for children to generate a 3-NDFL declaration. In addition, they need the document when applying for a loan, since many banks require salary information on this form. A certificate is also needed when applying for a new job, since the new employer needs data to provide deductions.

Document type code “Russian Federation passport” for tax authorities

in the rhetoric of the government of the Russian Federation there is no word “state” Russia and the word “system” of the Russian Federation, system of power, etc. is everywhere present. In fact, in my opinion, the system of the Russian Federation is being built on the territory of the USSR/RSFSR since: 14. there are no documents transferring the territory and resources from the USSR/RSFSR to the Russian Federation; 15. SBERBANK OF THE USSR has its own website on which currency quotes are regularly posted. 16. Order No. 311 dated November 5, 2001 was issued in the Russian Federation, where on page 59 it is said about the introduction of a chip into the brain of a Human-bio-object and its connection with all electronic media... and about the complete chipization of all citizens of the Russian Federation, non-citizens, by 2025 Russia, and citizens of the Russian Federation, who were forced and unknowingly imposed Russian passport forms and we were all misled and forced to sign; 17. The Constitution of the Russian Federation has the force of a Draft and there are no fundamental documents confirming a popular vote for the Constitution of Russia. However, we only have what we have and I am referring specifically to the articles of what we have. and so on... Based on the above and the documents I have studied and the above, Guided by the Universal Declaration, which is dominant over the laws of the Russian Federation, the Universal Declaration of Human Rights (UN), realizing the rights and freedoms of the Constitution of the Russian Federation - Art. 2, art. 3, art. 7 p. 1, art. 15 p. 1., p. 4, art. 17 p. 1, p. 2, art. 18, art. 19 p. 2, art. 21 p .1, Article 22, paragraph 1, Article 23, paragraph 1, paragraph 2, Article 24, Article 29, paragraph 1, paragraph 3, paragraph 4, Art. 33, art. 45 clause 1.clause 2, as well as International Law, which is dominant over the laws of the Russian Federation:

This is interesting: Transfer of inseparable improvements to the lessor documents

BY THIS STATEMENT I Abramenko Lyudmila Valentinovna revoke MY PERSONAL SIGNATURE under the column “personal code” because I believe that when receiving the RF passport FORM I was misled by the employees of the Migration Service that the Russian Federation is a commercial company LLC of the Russian Federation registered on the international website for the registration of foreign companies upik.de in the USA, in a state that has officially declared Russia hostile. I am a Person, I DEMAND: 1. Indicate the grounds for issuing a passport form by a commercial company of the Russian Federation whose director is a citizen of the USSR D.A. Medvedev by the Migration Service - to a Person and a citizen de jure and de facto of the existing State of the USSR 2. Consider the original passport issued to me in 1976 in the USSR with an identity document.

DUE TO THE FEAR FOR YOUR LIFE, HEALTH AND SAFETY ON THE TERRITORY OF THE COMMERCIAL COMPANY LLC RF, THIS STATEMENT, WHICH IS A KIND OF PROTECTION, IS PLACED ON THE INTERNET PAGES.

L.V. Abramenko December 27, 2017

When to submit your certificate for 2021?

The deadline for submitting 2-NDFL depends on the characteristics of the document. Certificates for 2018 are submitted to:

- until 04/01/2019 for documents with attribute “1” (issued for all employees);

- until 03/01/2019 for documents with sign “2” (issued if there is income for which personal income tax is not withheld).

If the organization does not submit the certificate within the specified period, the tax authorities impose a fine. According to Article 126, Part 1 of the Tax Code of the Russian Federation, if information necessary for control is not provided, a fine will be issued to the legal entity. face 200 rub. and 300-500 rub. to the official for each document not submitted. In addition, a fine of 500 rubles may be imposed on the employer. for a document if it contains false information.

Important! It will be possible to avoid penalties only if the employer independently finds an error in the certificate and submits a corrective version before the start of an audit by the tax service.

How and where to submit a certificate for 2021

The form for 2021 is regulated by Order of the Federal Tax Service of the Russian Federation dated October 2, 2018 No. ММВ-7-11/ [email protected] , and it is mandatory for use by all employers. A different form of certificate will be considered erroneous, since the officially registered sample is a unified reporting form.

The legislation provides two ways to submit certificates to the tax office:

- on paper, if the employer made payments to employees of less than 25 people;

- in electronic format through telecommunication channels, if the employer has made payments to 25 employees or more.

In the second case, the organization must enter into a formal agreement with the data transmission operator and obtain an electronic signature indicating the accuracy of the information and the signature of documents by an official of the company. In such a situation, it is considered that the certificates are transmitted via the Internet through a specialized company.

Important! Documents must be sent to tax authorities at the registered address of the business entity, where other reporting is also submitted.

Codes of types of taxpayer identification documents

For persons applying for recognition as a refugee on the territory of the Russian Federation (Resolution of the Government of the Russian Federation of May 28, 1998 N 523)

12 Resident card. Residence permit in the Russian Federation for stateless persons

14 Temporary identity card of a citizen of the Russian Federation. Temporary identity card of a citizen of the Russian Federation in form 2P

15 Temporary residence permit in the Russian Federation. Temporary residence permit for a stateless person in the Russian Federation (for persons who do not have identity documents)

21 Passport of a citizen of the Russian Federation. Passport of a citizen of the Russian Federation, valid on the territory of the Russian Federation since October 1, 1997

This is interesting: Convention abolishing the requirement of legalization of foreign official documents

23 Birth certificate issued by an authorized body of a foreign state. For foreign citizens under 16 years of age

91 Other documents. Other documents provided for by the legislation of the Russian Federation or international treaties as identification documents

Certificate 2-NDFL for tax authorities

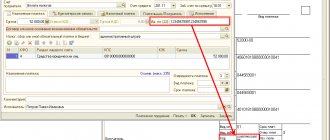

Certificate form

The document for the tax office contains information of a different nature, divided into blocks:

First sheet:

- “document header”, in which the tax agent’s tax identification number and checkpoint are entered. It is especially important that the order on the basis of which this form was put into effect must be indicated in the right corner;

- information about the document - number, year of submission, sign, correction number, inspection number;

- information about the tax agent by which the business entity is identified (name, OKTMO code, INN and KPP of the reorganized organization, telephone number);

- information about the employee, including full name, tax identification number, date of birth, taxpayer status, citizenship, document type code, series and number;

- generalized information on the amount of income received for the entire period, the amount of calculated, withheld and transferred tax, the amount of excessively withheld and not withheld personal income tax, the amount of advance payments;

- information about standard, social and property deductions received through the employer. This also includes information about the notification received from the tax office;

- information about the agent (full name of the manager, information about the document confirming authority, date and signature);

Second sheet:

- indicate the TIN and checkpoint of the agent;

- information is provided about the certificate number, reporting period, personal income tax rate, as well as specific information by month about income or deduction codes and the amounts for them.

Important! The main information in the document is the codes in the 2-NDFL certificate, which are directly related to filling out 2-NDFL according to the rules and reflecting the calculation of wages in accounting.

Rules for filling out the certificate

(Appendix No. 2 to the order of the Federal Tax Service of Russia dated October 2, 2018 N ММВ-7-11/ [email protected] )

The stages of filling out a certificate to the inspectorate can be presented in the following order:

- indicate basic information regarding the certificate itself, the tax agent and the taxpayer;

- enter general information about income, personal income tax and deductions provided by the employer;

- sign the first page of the certificate;

- enter monthly information about the codes and amounts of income and deductions;

- sign the second sheet of the certificate.

Sample filling for the Federal Tax Service

Certificate 2-NDFL for individuals

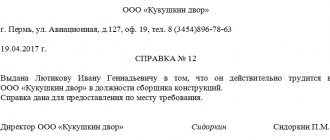

Certificate form for issue upon request

If an employee requests a 2-NDFL certificate from the accounting department for 2018 or 2021, it must be generated according to the following rules:

- indicate the date of the certificate and the year for which it was generated;

- indicate the details of the tax agent (employer), including OKTMO code, name, INN, KPP, telephone number, information on the reorganized company;

- enter personal information about the employee (full name, tax identification number, status, citizenship, date of birth, passport details)

- reflect the codes and amounts of income and deductions by month;

- enter information on the provided standard, social and property deductions;

- reflect the total amounts of accrued income, calculated, withheld and transferred personal income tax amounts;

- sign the certificate and indicate the name of the signatory.

Rules for filling out a certificate in 2019

The stages of filling out a certificate for an employee can be presented in the following order:

- enter basic information on the certificate, employer and employee;

- fill out information about income;

- reflect data on tax deductions received;

- enter general information about income and personal income tax;

- sign a document.

Sample of filling out a certificate for employees

General filling requirements

The information is reflected in a special form approved by the Federal Tax Service of Russia. It has details - number and date of issue.

One of two values is entered in the “sign” field:

- 1 – indicated in most cases when filling out a taxable income certificate;

- 2 – if it contains information about remuneration from which, for one reason or another, personal income tax cannot be withheld (such certificates must be submitted no later than March 1).

- 3 – when the tax is fully withheld by the legal successor of the organization;

- 4 – tax was not withheld by the successor.

The correction number shows how many times corrections were made to the original certificate; for the initial submission, it is set to 00.

The form includes five sections:

- Information about the employer - name, tax identification number, checkpoint, OKTMO and contact phone number.

- Information about an individual – full name, date of birth, citizenship, TIN, passport and its details, taxpayer status. Previously, information about the place of residence was filled out, which included the address and code of the subject (for example, in Moscow it was 77, and in the Moscow region it was 50), but from 2021, filling out these columns was canceled.

- Rewards received by an employee during the calendar year. Each income has its own designation and is shown by month of payment. The third section contains the rate where the income is taxed. It also reflects professional deductions (if the employee has them).

- Tax deductions. This section reflects other deductions (except for professional ones). Each tax benefit has its own digital designation.

- Generalized information. In the fifth section, income and personal income tax are shown in total amounts for the reporting period. The amounts of calculated, withheld and transferred tax are reflected in different fields.

The certificate is signed by the head of the organization or his authorized representative and certified by a seal.

Regulations for submitting to the tax office

The regulations for submitting a certificate to the inspection are enshrined in Appendix 4 to the Order of the Federal Tax Service of the Russian Federation dated October 2, 2018 No. ММВ-7-11/ [email protected] It contains the following information:

- who submits the documents;

- how they can be transmitted;

- what is the date of submission of certificates to the Federal Tax Service;

- how to submit certificates on paper;

- how to transmit certificates in electronic format via telecommunication channels.

In what cases is it not necessary to submit

For some employees, the employer does not have to file 2-personal income tax, which is specifically stated in the regulations. So, documents do not need to be sent:

- if the employee received payments not subject to personal income tax. According to Art. 217 of the Tax Code of the Russian Federation, an employee may be paid income that is not subject to taxation, and, accordingly, if only such accruals are present, then a certificate is not submitted to the tax authorities. Such income can be state benefits (unemployment benefits, child care benefits, maternity benefits), compensation for harm, pensions, benefits in kind, payment for food or accommodation, etc.;

- if an individual in accordance with Art. 227, 228 of the Tax Code of the Russian Federation are obliged to calculate and pay personal income tax themselves - individual entrepreneurs, notaries, lawyers, etc.;

- if the individual received payments specified in Art. 226.1 Tax Code of the Russian Federation. This point concerns income from transactions with securities, financial instruments, repo transactions and securities lending.

Recommendation! It is necessary to clearly determine what type of income it is, and whether it is necessary to withhold and transfer tax on it, and, accordingly, submit a 2-NDFL certificate to the tax office. If you have any doubts on this issue, it is better to contact the hotline in order to take action in accordance with the legislation of the Russian Federation and not receive a fine.

Filling rules

Issuing a personal income tax certificate 2 is a common matter, but sometimes it is not at all easy. An inexperienced accountant may have problems.

Feature selection

The first thing a specialist faces is identifying the sign. There are two types of signs:

- Filling out occurs for any employee receiving wage payments from the enterprise and deductions from them. This also includes funds protected from personal income tax withholding. A certificate with this indication must be submitted to the tax office no later than April 1.

- All other situations when it is impossible to deduct taxes from certain material assets. For example, if you need to pay for a gift for a person who is not an employee of the company. Temporary dates: until the first of March. In addition, you must indicate the amount of income that is not subject to taxation and the possible amount of tax.

Usually in the second case you have to make two certificates with different characteristics at once. The first is all income in aggregate, the second is the amounts protected from withholding.

Code of the country

The second task is to indicate a reliable country code. Today there is an OKSM classifier of country codes. It was approved on December 14, 2001 by Gosstandart under number 529-ST. Information from it can be found for free on many legal Internet resources, but it is important to remember that the database is constantly updated and subject to adjustments. Therefore, it is necessary to monitor the relevance of the information that comes across on sites and weed out outdated versions. For example:

- Russian citizenship code for personal income tax certificate 2 is 643.

- Belarus - 112.

- Uzbekistan - 860.

- Kazakhstan - 400.

- Armenia - 051.

- Ukraine - 804, etc.

The original classifier is located directly on the official website of Gosstandart. You can also find its changes there, but they are all located separately, which creates a number of inconveniences when searching for the necessary information.

Example document

The standard certificate form has several parts to fill out. The first part includes:

- Full legal name of the organization that was involved in issuing this certificate.

- 1st or 2nd sign indicating the possibility of collecting tax deductions.

- Document data: number, date of completion, what time frame was taken as the basis for the calculation.

- Territorial code of the tax service with which the enterprise is registered.

- The serial number of the adjustments made. If there were none, you must enter the number 0.

- Landline telephone number of the work organization. Required with area code.

- Payment details of the enterprise: taxpayer identification number (TIN), All-Russian Classifier of Municipal Territories (OKTMO) and reason for registration code (KPP). For individual entrepreneurs, it is permissible to put a dash.

- Personal data of the employee for whom the certificate is issued: last name, first name and patronymic, tax identification number, residential address.

- Official taxpayer status. Usually for a Russian resident there is only one.

- State code from classifier 529-ST. This can be either the Russian Federation or any other country from which the employee arrived.

- Code of the employee’s personal identification document, as well as its number and series. Russian passport code is 21.

The second part is further divided into three more sections. Here they describe monthly material income, tax and other deductions, the amount of actual tax and that already paid.

The third part displays income in coded form.

For example, salary code is 2000, vacation payments are 2012, other one-time amounts are 2720. All this is subject to personal income tax. The fourth is coded deductions. For example, code 126 is a deduction for a minor child.

The fifth part is the total amount of personal income tax. To calculate, you need to add up the income for the entire previous year and subtract deductions. From the amount received, calculate 13 percent (if the rate is for the first taxpayer status).

Additional points

There are several additional points regarding 2-NDFL:

- the validity period of the deduction certificate is 3 years, since it is during this period that the taxpayer can exercise his right to the benefit;

- the validity period of the loan certificate is set by the bank itself, and, as a rule, this period is no more than six months;

- if the employee does not have taxable income, he does not need to submit a certificate to the tax office. In addition, such an employee will not be able to receive a deduction;

- certificate of income of an individual 2-NDFL - the main document reflecting final information on income and deductions for a specific employee.

To find out what the codes in the 2-NDFL certificate mean and in general what codes are present in the 2-NDFL certificate, see the link.

2-NDFL for tax deduction

To receive a deduction through the tax office, for example, property or social, you need to take 2-NDFL from the employer and submit it to the tax authorities. Information from this document is entered into the 3-NDFL declaration indicating the employing organization, its tax identification number and checkpoint, as well as monthly information about income. In addition, data on deductions provided directly by the employer must also be reflected in the declaration for the correct calculation of personal income tax for refund.

The tax office compares the information from the submitted document with information previously received from the employer and identifies any inaccuracies or establishes the accuracy of the document.

Attention! Tax authorities do not accept a paper declaration unless 2-NDFL is attached to it, and this must be the original document, and not a copy. If a taxpayer submits an electronic calculation through his personal account on the Federal Tax Service website, then, as a rule, the 2-NDFL certificate is uploaded automatically when the employer submits it in accordance with the submission deadlines. In this case, tax authorities may not request 2-NDFL from the person himself.

Why do you need 2-NDFL when applying for another job?

When applying for a new job, it is necessary to submit 2-NDFL from the previous place to the accounting department, and at the same time it must be formed for the calendar year, that is, from the beginning of the year until the employee’s dismissal.

The need to transfer the document is due to the fact that this information is needed to provide a person with standard deductions for himself or for children, social or property deductions, if the person has such a right. According to Art. 218 of the Tax Code of the Russian Federation, standard deductions are provided to the employee until his total income for the calendar year reaches 350 thousand rubles. When the specified limit is reached, no deduction is provided, and therefore the accountant needs to know exactly what payments and in what amount the employee received at his previous job.

If a person does not claim deductions, then 2-NDFL does not need to be submitted to the accounting department at the new location.

2-NDFL and credit

When receiving a loan, many banks require official confirmation of income - either 2-NDFL, or a certificate in the form of the credit institution itself. If it is necessary to submit 2-NDFL, then it is ordered from the accounting department in the usual manner, and there is no need to enter any additional information into it, since it is a unified accounting register.

Based on the information from the certificate, the loan officer calculates the likely amount of the loan provided and also assesses the client’s solvency. At the same time, banks check and analyze the accuracy of the information contained in the certificate using the following methods:

- clarify information about the organization through official sources of information. For example, to determine whether a given organization really exists, you can request an extract from the Unified State Register of Legal Entities, which is provided free of charge to any user;

- information regarding the employee is checked, that is, his full name, passport details, TIN;

- Information related to income reflected on certificates is especially carefully checked and analyzed. In this case, the decoding of income codes in the 2-NDFL certificate is taken into account, allowing you to understand exactly what payments the employee received from the employer. Information related to a sharp increase or decrease in wages is subject to careful analysis, and then an employee of a credit institution may ask for an explanation from the employer as to what is causing such a change in wages;

- banks have the opportunity to request information from inspection authorities and check certificates for the accuracy of the information entered. Employees submit an official request, to which they also receive an official response from the tax service;

- To confirm the amounts specified in 2-NDFL, banks can request from the organization other accounting registers for payroll, for example, pay slips, personal accounts, the availability of writs of execution for the employee, etc.

Common mistakes when filling out

Experts identify the following most common mistakes:

- erroneous indication of the income code in the 2-NDFL certificate. The accountant may make a mistake and assign the wrong number to the code, which will result in an incorrect accrual position being indicated in the certificate;

- for one month, the salary can be divided into two amounts. This error occurs because the employer is obliged to pay the employee at least 2 times a month (advance and basic salary). However, both of these amounts must be summed up and entered as a total for each month;

- errors in the OKTMO organization. If the employer has divisions, then they are assigned their own OKTMO numbers. The certificates must indicate the OKTMO corresponding to the specific department in which the employee works;

- errors in reflecting the amounts of remuneration under GPC agreements. Income must be reported in the month in which it was actually paid, not accrued. This point is one of the main differences between employment contracts and GPC;

- errors in indicating the basic details of the organization or employee, for example, change of name or surname, incorrect TIN, change of passport data.

Important! Identified errors can be corrected by the employer by submitting corrective reports, but this must be done before the tax service checks, so as not to receive a fine.