An individual paid for the organization

admin05/06/2021 02/15/2018 In practice, situations often arise when the General Director or any other employee of the company would like to pay for a legal entity. Since November 30, 2021, such an opportunity has appeared, and Article 45, paragraph one of the Tax Code of the Russian Federation states that tax payment can be made by another person.

By the way, insurance contributions for compulsory pension insurance, the Federal Compulsory Medical Insurance Fund and the Social Insurance Fund (except for the Social Insurance Fund from the National Insurance Fund and the Pension Fund) can also be paid by another person from January 1, 2021. So, we propose to consider an example and fill out with us a receipt for payment of the trade fee for the 4th quarter of 2021 for the organization of DomUyut LLC by an individual Levashov M.

A. Strictly in accordance with the Rules for indicating information in the details for transferring funds from the Federal Tax Service of Russia. Details of DomUyut LLC: TIN 7718346970 KPP 771801001 Details Levashov Maxim Alekseevich: TIN 772516010145. Address:

Payment of travel for individuals who are not employees of the organization

The list of compensation payments exempt from personal income tax is established by paragraph 3 of Article 217 of the Tax Code of the Russian Federation. Reimbursement of travel payments to persons under the authority or administrative subordination of the organization is not subject to personal income tax.

When it comes to reimbursement of travel expenses to the place of business trip for non-employees of the company, the “exempt” norm of paragraph 3 of Article 217 of the Tax Code of the Russian Federation does not apply to these payments. After all, persons who are not in an employment relationship with the company are not its employees.

Judicial practice shows the following. Inspectors charge additional personal income tax if the company does not withhold it from amounts paid to an individual who is not an employee to reimburse travel expenses.

Labor relations arise between an employee and an employer on the basis of an employment contract concluded by them in accordance with the Labor Code of the Russian Federation. The parties to the labor relationship are the employee and the employer.

Based on Article 164 of the Labor Code of the Russian Federation, compensations are monetary payments established to reimburse employees for costs associated with the performance of their labor or other duties provided for by the Labor Code of the Russian Federation and other federal laws.

Therefore, the provisions of paragraph 3 of Article 217 of the Tax Code of the Russian Federation regarding compensation payments for travel and accommodation expenses apply to individuals who are in an employment relationship with an organization on the basis of employment contracts concluded with them. Within the framework of other contractual relations, including civil law, the amounts of such expenses are not compensatory and are subject to personal income tax (Resolution of the Federal Antimonopoly Service of the Volga District dated June 1, 2009 No. A12-15743/2008).

A similar conclusion that compensation for travel expenses of persons who are not employees of the organization is recognized as income of an individual subject to personal income tax is presented in the decision of the Twelfth Arbitration Court of Appeal dated August 15, 2014 No. A12-1984/2014. Thus, the appellate court recognized that if the payment of expenses of individuals for their travel and accommodation during the provision of services under civil contracts is carried out in the interests of these individuals, including if such payment is part of the individual’s remuneration for work performed (work , services), then payment of these costs is recognized as income received in kind, and the amounts of such payment are subject to personal income tax.

EAT. Yudakhina

, for the magazine “Regulatory Acts for Accountants”

Professional press for accountants

For those who cannot deny themselves the pleasure of leafing through the latest magazine and reading well-written articles verified by experts. Select a magazine >>

If you have a question, ask it here >>

The organization pays for the individual

Payment is recommended to be made on behalf of the individual in whose name the services are registered.

For individuals, payment for services is possible by receipt through Sberbank of the Russian Federation, WebMoney, Yandex.Money, ROBOKASSA, QIWI Wallet.

In case of payment through a bank, if the Payer does not coincide with the Client (customer of services), you will need to provide an application addressed to the General Director of Komtet LLC from the person who made the payment about the purpose of the payment (see sample). Dear Alexander Vladimirovich, I ask you for the payment made by “NAME OF THE PAYING ORGANIZATION” (TIN/KPP) from (xx.xx.xxxx) in the amount of ... rubles (indicate the account number or billing account number), to be counted against the payment for Petrov Petrovich.

Number. Seal. Signature. The letter must be submitted by mail to our address: 440600, Penza, st. Suvorova, 92, or a scanned electronic version with your signature by e-mail to the Contents of transactions ¦Debit ¦Credit¦ Amount,¦ Primary ¦¦ ¦ ¦ ¦ rub.

How to understand that the company’s manager is paying for it

The director is the only one in the enterprise who can act without a power of attorney. How can a supplier understand who is in front of him? If payments are made cashless without the participation of an ESP, you can do without an online cash register. The exception to clause 9 of Article 2 of Law 54-FZ on CCP applies here. When money arrives to the supplier’s account, you can see for what and from whom the funds are coming. If there is an agreement, it is easy for the seller to identify the payer as the head of the buyer enterprise.

If settlements are carried out with the participation of ESP or in cash, then there is not much difference who is in front of you. The benefit of paragraph 9 of Article 2 of Law 54-FZ ceases to apply in any case, even if the head of the payer enterprise submits an order for his approval for the position. And the supplier will have to use CCP.

If cash was used in payments between organizations and (or) individual entrepreneurs and (or) an electronic means of payment was presented, then the cash receipt, in addition to the mandatory details (specified in paragraph 1 of Article 4.7 of Law 54-FZ), must contain additional details: name buyer (client) (name of organization, full name of individual entrepreneur) and TIN of the buyer (client).

But if the supplier was unable to establish the accountable status at all during settlement, then he will have to use the online cash register in the manner prescribed for settlements with an ordinary individual. This is stated in paragraph 2 of the letter of the Federal Tax Service of the Russian Federation No. AS-4-20 / [email protected] (LINK).

Payment by a third party for services provided to a company by an individual

published: 06/13/2016 The law directly provides for the possibility of a company paying for the services of an individual by a third party.

This follows from paragraph 1 of Art. 313 of the Civil Code of the Russian Federation, according to which the fulfillment of an obligation may be entrusted by the debtor to a third party if the law, other legal acts, the terms of the obligation or its essence do not imply that the debtor is obliged to fulfill the obligation personally. In this case, the creditor is obliged to accept the performance offered for the debtor by a third party. A contract for the provision of paid services (performance of work) is not an obligation that requires personal performance by the debtor.

We recommend reading: Material damage after a fire, what is included

Thus, the obligation can be fulfilled by a third party. In this case, the performer of the obligation can be either a legal entity or an individual. Fulfillment of obligation

Civil relations

Under a contract for the provision of services for a fee, the contractor undertakes, on the instructions of the customer, to provide services (perform certain actions or carry out certain activities), and the customer undertakes to pay for these services (clause 1 of Article 779 of the Civil Code of the Russian Federation).

The customer is obliged to pay for the services provided to him within the time frame and in the manner specified in the contract for paid services (clause 1 of Article 781 of the Civil Code of the Russian Federation).

In the situation under consideration, the price of the contract for the provision of paid services includes compensation for the contractor’s expenses for travel to the place of provision of services and the remuneration due to him, which is provided for in paragraphs 1, 2 of Art. 709, art. 783 of the Civil Code of the Russian Federation. Consequently, the compensation in question is part of the contract price for services provided by the contractor.

We also note that the trip of the contractor under a civil contract to the place of provision of services is not a business trip in relation to Art. 166 of the Labor Code of the Russian Federation, since it is carried out by an individual within the framework of civil law, and not labor relations with an organization.

Payment by an individual for a legal entity

Question: Currently the organization does not have a settlement account.

You may be interested in: Recovering private debts.

Is it possible to pay for your service to an individual (founder) for an organization? Can I pay in cash at your office cash desk? Answer: You can pay for the service for the organization from an individual’s personal account or an individual’s bank card, but only if you are an employee of an LLC, for example, a director, and not just the founder of this LLC. So, if you are an employee of an LLC, then You can pay for the service as an individual, and then the organization will reimburse you for the money spent when such an opportunity arises.

You can do this as follows: First, create an expense report.

In the service, in the Documents tab, add an Advance Report, but in the “Advance Report Type” field, you need to select “payment to supplier.” - Do not fill in the “Advance Payment Document” field. Such a receipt can be taken to the bank and paid in cash for the organization.

Payment for individuals face for legal face

Question: Currently the organization does not have a settlement account. Is it possible to pay for your service to an individual (founder) for an organization?

Can I pay in cash at your office cash desk? Answer: You can pay for the service for the organization from an individual’s personal account or an individual’s bank card, but only if you are an employee of an LLC, for example, a director, and not just the founder of this LLC.

So, if you are an employee of an LLC, you can pay for the service as an individual, and then the organization will reimburse you for the money spent when the opportunity arises. You can do this as follows: First, create a . In the service, in the Documents tab, add an Advance report, and in the “Advance report type” field, you need to select “payment to supplier.”

— do not fill in the “Document for advance payment” field.

Next, you continue to register a joint stock company to pay the employee the money he spent on paying for the service.

Specify the counterparty and the service certificate. The field “Document for issuance of overexpenditure” should be filled in if there was no issue for the report and the money will be reimbursed to the employee later. Indicate the method of payment to the employee (by order - in cash from the cash register or by order - in cashless form to the employee’s card).

Save. After payment for the service is reflected in these methods, the costs of the service will be correctly taken into account in your accounting and tax records. Unfortunately, there is no cash payment for using the service.

Payment methods for the service are specified in: 5.3.

The license fee is paid by the Licensee in one of the following ways: 5.3.1. by bank transfer to the Licensor's bank account based on the invoice issued by the Licensor;5.3.2. using electronic payment systems specified on the Licensor’s website in the Licensee’s Personal Account. and clause 5 of the Offer Agreement for the provision of paid services: 5.3.

The tariff is paid by the Customer in one of the following ways: 5.3.1.

by bank transfer to the Contractor's bank account based on the invoice issued by the Contractor;5.3.2. using electronic payment systems indicated on the Contractor’s website in the Customer’s Personal Account.

Payment for another legal entity: how to process it, sample

.

The company's supplier requested that payment for the shipment of goods be transferred not to his bank account, but to his landlord.

He explains this by saying that he must pay off his rent arrears, but currently has no available funds. Can a company in such a situation make payment for another legal entity? Yes, today there is nothing unusual in such a request.

After all, the law allows business entities to pay their obligations not only directly. It is quite acceptable that another organization transfers funds on behalf of the debtor. The right of the debtor to transfer the obligation to pay for it to a third party is provided for by the Civil Code. This is stated in Article 313.

A reservation is also made that this is legal in the event that any other laws or conditions of the paid obligation do not require that the debtor fulfill them strictly independently.

Payment by an individual to a legal entity to a bank account

As a general rule, all organizations and entrepreneurs are required to use cash register systems when making payments (clause

1 tbsp. 1.2 of the Federal Law of May 22, 2003 No. 54-FZ).

According to the amendments in force from July 3, 2021, a deferment was provided for the use of online cash registers in terms of non-cash settlements with individuals who are not individual entrepreneurs (Clause 4, Article 4 of Federal Law dated 07/03/2021 No. 192-FZ ). According to such calculations, the online cash register will be used only from July 1, 2021.

In accordance with banking legislation, non-cash settlements include settlements by payment orders, letters of credit, collection orders, checks, electronic funds, as well as settlements by transferring funds at the request of the recipient of funds (direct debit) (clause 1.1 of the Regulations, approved. Bank of Russia dated June 19, 2012 No. 383-P). The deferment provided does not apply to electronic means of payment.

We recommend reading: Cancellation of discounts on legal entity cards

Accounting upon receipt of payment for goods from a third party

The basis for settlements is a payment order from an individual, in which the purpose of payment (field 24) must indicate: the purpose of the payment, the goods (work, services) to be paid, details of the contract, commodity documents, invoices to be paid, VAT amount, name the organization for which the payment is made (Appendix 1 to Bank of Russia Regulations dated June 19, 2012 N 383-P “On the rules for transferring funds”).

For example: “Payment for goods for Alpha LLC under agreement dated 01/08/2019 No. 1 according to invoice dated 05/23/2019 No. 123 in the amount of 120,000 rubles. 00 kop. (one hundred twenty thousand rubles 00 kopecks), including VAT - 20,000 rubles. 00 kopecks.” According to the Instructions for the application of the Chart of Accounts for accounting financial and economic activities of organizations, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n, account 62 “Settlements with buyers and customers” is intended to summarize information on settlements with buyers and customers. This account is credited in correspondence with the accounts for cash accounting, settlements for the amounts of received payments (including the amounts of advances received), etc.

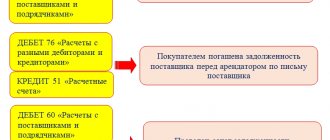

If the supplier has received an advance for the upcoming delivery of goods (transfer of work, services) to the buyer (customer) from a third party, then the following entries can be made in the accounting records of the supplier (performer):

- Debit 51 Debit 62.02 - reflects the obligation to supply goods in the amount of the advance received;

- Debit 76.AB Debit 68.02 - VAT is charged on the advance received.

If payment is received for the delivery of goods (transfer of works, services) to the buyer (customer) from a third party, an entry is made in the accounting records of the creditor (supplier, contractor) for the repayment of the buyer's (customer's) receivables:

- Debit 51 Credit 62 - payment received for goods (work, services).

After receiving payment from an individual, the supplier (performer) needs to issue a statement of reconciliation of settlements with the buyer (customer).

Payment for an individual by a legal entity

However, this is only possible if the money went there directly from the bank account of the company or individual entrepreneur:

- when carrying out transactions with securities;

- conducting activities related to organizing and conducting gambling;

- issuance/repayment of loans and interest on them.

- payment of real estate rental;

To do this, it is often necessary to use the following scheme: money is handed over from the cash desk to the bank, and then returned back to the cash desk, after which settlements with individuals are made.

Are there any restrictions on amounts when settling payments between a legal entity and an individual? In addition to the fact that Directive No. 3073-U of the Central Bank of the Russian Federation contains a list of permitted grounds for cash settlements between legal entities and individual entrepreneurs and individuals, it directly states that such settlements can be carried out without restrictions on the amount both in rubles and in foreign currency (p .

Using an online cash register when the accountable individual is the manager

According to clause 6.3 of the Directive of the Central Bank of the Russian Federation No. 3210-U dated March 11, 2014 (LINK), any employee of the organization (individual entrepreneur) has the right to receive money against the report. Accountable money is issued to cover expenses associated with the activities of a given employer (organization or individual entrepreneur). Moreover, both an ordinary employee of the company and its manager can become an accountable person. And here it does not matter what kind of agreement was concluded with these employees. Directive No. 3210-U allows for the conclusion of both a civil law and an employment contract with an employee acting as an accountable person (clause 5 of the Directive). This is confirmed, among other things, by letter of the Central Bank of the Russian Federation No. 29-R-R-6/7859 dated 10/02/2014 (LINK).

Thus, the head of a legal entity (or individual entrepreneur) can, along with other employees, act as an accountable person and pay the expenses of the enterprise. At the same time, the supplier of goods, works or services, in favor of which such an accountable person makes a payment, must apply cash register in the general manner, if he is obliged to do so by Law No. 54-FZ. Those. if the supplier does not fall under the exceptions or benefits provided for by law 54-FZ. In particular, one of the exceptions is the settlement between organizations and (or) individual entrepreneurs, prescribed in paragraph 9 of Article 2 of Law 54-FZ on CCP (LINK). If settlements between these participants are carried out by bank transfer, but without presenting an electronic means of payment (ESP), then the supplier will not need an online cash register.

[adsp-pro-1]

In order for the supplier to take advantage of this exception, he must identify the accountable entity with the paying enterprise (an individual entrepreneur or a legal entity). For this, an agreement between the payer company and the supplier, and a power of attorney from the payer’s accountable person, are sufficient. The specified power of attorney indicates the right of this accountable to act on behalf of the enterprise. And, as the Federal Tax Service of the Russian Federation points out in paragraph 2 of its letter No. AS-4-20/ [email protected] dated 08/10/2018 (LINK), an agreement between the payer and the supplier and a power of attorney from the payer’s representative are sufficient for non-cash payments to be recognized as complying with the provisions of paragraph 9 Article 2 of Law 54-FZ. If the ESP is not presented during such calculations, then an online cash register is not needed here at all.

A legal entity pays for an individual

an individual entered into an agreement with a developer (legal entity) for the purchase of a house under construction, i.e.

5). List of messages IP/Host: 85.21.83. payment for an individual Guys, someone tell me.

e. an agreement for shared participation in construction, but the payment to the developer for an individual was made by another legal entity.

The payment document states payment under such and such an agreement for I.I. Ivanov. Is this legal? March 27, 2014, 1:36 p.m., question No. 408813 Svetlana,

St. Petersburg 500 cost of the issueissue resolved Collapse Online legal consultation Response on the website within 15 minutes Answers from lawyers (5) 603 answers 308 reviews Chat Free assessment of your situation Lawyer, St. Petersburg

Moscow Free assessment of your situation There are no prohibitions here. This is legal. It is simply necessary to prepare some kind of agreement between this individual and the legal entity-payer in which this would be spelled out - the procedure for payment by the legal entity for the physicist, the procedure for returning money to the legal entity, etc.

An individual pays a receipt for a legal entity

In practice, situations often arise when the General Director or any other employee of the company would like to pay for a legal entity.

Since November 30, 2021, such an opportunity has appeared, and Article 45, paragraph one of the Tax Code of the Russian Federation states that tax payment can be made by another person. By the way, insurance contributions for compulsory pension insurance, the Federal Compulsory Medical Insurance Fund and the Social Insurance Fund (except for the Social Insurance Fund from the National Insurance Fund and the Pension Fund) can also be paid by another person from January 1, 2021. So, we propose to consider an example and fill out with us a receipt for payment of the trade fee for the 4th quarter of 2021 for the organization of DomUyut LLC by an individual Levashov M.

A. Strictly in accordance with . Details of DomUyut LLC: TIN 7718346970 KPP 771801001 Details Levashov Maxim Alekseevich: TIN 772516010145.

Address: Moscow, st. Velozavodskaya, d.