maturity date

The maturity date is the date on which the note must be paid. It is either directly indicated in the promissory note or determined in some other way. The most common ways to indicate the maturity date are:

- A specific date, for example: “November 14, 20xx.”

- A certain number of months from the date of execution of the bill, for example: “3 months from the date of execution.”

- A certain number of days from the date of execution of the bill, for example: “60 days from the date of execution.”

If you directly indicate the maturity date of the bill of exchange, no difficulties arise. If the repayment date is determined by the number of months from the date of execution of the bill, the same date of the corresponding next month is taken. For example, a bill dated January 20 with a maturity date of 2 months from the date of execution must be paid on March 20.

If the maturity date occurs after a certain number of days from the date of execution of the bill, then it can be calculated by adding the exact number of days. It is important to exclude the date of execution of the bill and include the date of its repayment. For example, a bill dated May 20 with a maturity date of 90 days, in accordance with the above calculation, must be paid on August 18:

| Remaining days in May (31 – 20) | 11 |

| Days in June | 30 |

| Days in July | 31 |

| Days in August | 18 |

| Total days | 90 |

Bill of exchange

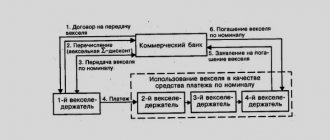

A bill of exchange differs from a simple bill in that the payer under it is not the drawer of the bill, but the person indicated by the drawer. Thus, three persons participate in the circulation of a bill of exchange:

drawer - the person who writes a bill in the form of an offer to the intended payer to pay on that bill;

intended payer - the person indicated by the drawer as the payer under it;

holder of a bill - a person who purchases a bill of exchange and receives payment on it.

In business practice, a bill of exchange is usually used to replace debt transfer operations. For example , the Alpha organization has accounts payable to the Beta organization for a delivered batch of goods. Organization Beta has outstanding obligations to pay for goods supplied to organization Vega. The Beta organization issues a bill of exchange, indicating the Alpha organization as the payer, and transfers it to the Vega organization in payment for the goods supplied. Thus, “Beta” transfers “Alpha’s” debt to “Vega” and pays off its debt. "Alpha" becomes Vega's debtor.

When reflecting these transactions in accounting, it is necessary to pay attention to the following circumstance: a bill of exchange at the time of issuance represents only an offer by the drawer to the intended payer to repay the bill and does not in any way oblige the organization specified in the bill to pay under the document. Such an obligation arises only after the bill of exchange is accepted or officially accepted for payment by the payer organization specified in the bill. At the same time, in accordance with the Regulations on bills of exchange and promissory notes, the drawer of the bill of exchange is responsible for acceptance and payment. It follows that when issuing a bill of exchange before its acceptance, the payer of the bill is the organization that issues the bill. Thus, until the moment of acceptance, accounting for a bill of exchange is no different from accounting for a promissory note. From the moment of acceptance, the acceptor assumes the bill of exchange obligation, becoming the principal debtor. The obligation of the drawer also remains in force, which after acceptance is conditional, i.e. he will be obliged to pay the bill if the accepting organization does not repay it.

Term of the bill

The duration of the bill in days or the term of the bill can be determined in the opposite way to how we determine the maturity date. Its calculation is important because interest income is calculated based on the exact number of days. If the maturity date of the bill is determined by the number of days from the date of execution of the bill, problems with calculation do not arise. If a specific repayment date is established or it is determined by the number of months from the date of issue of the bill, then the exact number of days should be calculated.

Let's assume that the bill is issued for the period from May 10 to August 10. Having carried out the following calculations, we can establish that its validity period is 92 days:

| Remaining days in May (31 – 10) | 21 |

| Days in June | 30 |

| Days in July | 31 |

| Days in August | 10 |

| Total days | 92 |

Types of bills

Differences in the rights of the owner of debt registration determine the classification into the following types:

- nominal;

- order;

- to bearer.

Type 1 documents contain information about the person who is given the right to demand the return of money from the drawer. In the second case, such a right is granted to the person who currently owns the document. His details are not written down on paper. The order obligation is drawn up in the name of the first owner and can be transferred to another person by making an endorsement. Selling and buying are carried out with each type of this financial instrument. A bank bill may be for collection. Then a transfer inscription in favor of a specific bank is recorded.

- Onion pie - recipes with photos. How to prepare dough and onion filling for aspic and classic baking

- The most delicious turkey marinade recipes

- Draniki with minced meat - recipes step by step with photos. How to cook potato pancakes with minced meat in the oven or in a frying pan

Personal bill

If the form of a financial instrument indicates the surname, name, patronymic of the owner, then such an obligation is defined as personal. The specified person has the right to demand payment of the debt in accordance with the concluded document. A registered promissory note is the most common type of debt obligation. You can change the holder by applying an endorsement on the back of the paper. The record contains the name of the next owner and the signature of the previous one.

Bill of exchange payable to bearer

The order bill does not contain information about the holder of the bill. The paper states the amount of the debt, the date and place of settlement, and the debtor’s details. The right to receive a debt under an order form has the person who currently owns it. During its validity, the document may change several owners (especially if the amount is large), and the last holder demands payment of the debt.

Interest and interest rate

Depending on whether a person is a borrower or a lender, interest represents either the cost of borrowing or the income received for the loan provided. The amount of interest depends on three factors: the principal amount (the amount borrowed or lent), the interest rate, and the period for which the funds are lent. The following formula is used to calculate interest:

Principal amount of the bill * interest rate * time = interest

Interest rates are usually fixed for a year. For example, interest on a note with a principal amount of 1,000 due in one year at an interest rate of 8% would be 80 (1,000 * 8/100 * 1 = 80). If the bill was issued not for a year, but for 3 months, the interest would be 20 (1,000 * 8/100 * 3/12 = 20).

If the term of a bill is specified in days, the exact number of days must be used when calculating interest. To simplify the calculations, we will take a year consisting of 360 days as the basis for calculating interest. So, if the bill specifies a period of 45 days, the interest will be: 1,000 * 8/100 * 45/360 = 10.

The essence of market and nominal interest rates is described here: CFA - How to interpret interest rates?

Payments by bill of exchange

Payments by bill of exchange are mutual settlements between suppliers of goods (services) and payers, the peculiarity of which is deferred payment. The possibility of this deferment is provided for by a special document - a bill of exchange.

Such payments are one of the forms of non-monetary payments that are characteristic of a market economy. Transactions with bills of exchange are regulated by special bill legislation.

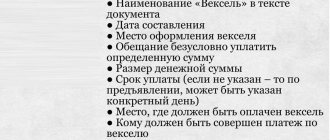

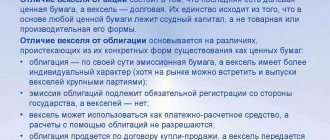

For a long time, a promissory note was understood exclusively as a promissory note. However, today this term has acquired a new meaning. A bill of exchange in the modern sense is a document drawn up strictly in the form established by the law adopted in June 1930 by the Geneva Convention. At its core, a bill of exchange is a written promissory note that gives the drawer (its owner) the right to demand payment by the debtor of the amount specified in the document.

There are promissory notes and bills of exchange. Promissory notes are unconditional obligations to pay the drawer a certain amount on time. Such bills cannot be transferred to third parties. If the bill is transferable, then it is possible to transfer funds to the creditor by collecting them from the debtor. To carry out this operation, a special endorsement is required.

Today, the most common means of payment is the bank bill. Payments by bill of exchange involve the participation of banking institutions in all transactions involving their use. In other words, bills must be collected by banks, which means that they must fulfill the instructions of the bill holders.

Bills of exchange transferred to the bank must be provided with a guarantee inscription “for collection” or “to receive payment”. Thus, by collecting a bill of exchange, the bank accepts responsibility for presenting the bill of exchange to the debtor, as well as for receiving the payment due from it. After accepting the bill for collection, the bank forwards the papers to the bank branch at the place of payment, simultaneously notifying the payer of the receipt of documents by summons. After the bank receives payment on the bill, the funds are credited to the client’s personal account with notification of the latter about the execution of the order.

Payments by bill of exchange are carried out based on payment terms, which are set individually depending on the type of transaction, the nature of the relationship between the seller and the buyer, etc. Deadlines can be set for a specific day (the date is indicated), for a specific period from the date of drawing up the document, for the period “until presentation” and for a certain time (payment must be made no later than the hour specified in the document).

For the banking intermediation that he provides when settlements are made by bill of exchange, the client pays a commission (percentage of the amount), and also covers all costs of sending documents and accompanying bills of exchange. However, this mediation is beneficial for the client, since it allows the bank to shift responsibility for meeting payment deadlines and guarantees the quick and reliable receipt of funds from debtors.

Bills of exchange have (in almost all cases) real security, so they are not only a means of payment. They are securities that are accepted as collateral.

Bills of exchange in the form of collection can be interest-bearing (involves payment of not only the debt, but also interest on it) and discount (discount on a bill means that the difference between the price of its sale and repayment is included in the document).

Accounting for bills of exchange is carried out according to their types, paying enterprises, amounts of receipts, and terms that require settlements with bills of exchange. Postings reflecting transactions with bills of exchange differ in debit and credit, depending on the characteristics of the transactions. For example, when purchasing a bill of exchange from a third party, postings D58.2, K78 are made, when paying a bill of exchange - D76, K51, and so on.

Repayment amount

The total amount paid on the note on the maturity date is called the maturity amount. It consists of the principal amount of the bill and interest. The repayment amount of a 1,000 note issued for 90 days at an interest rate of 8% is calculated as follows:

| Repayment amount | = principal + interest |

| = 1 000 + (1,000 * 8/100 * 90/360) | |

| = 1 000 + 20 | |

| = 1 020 |

Sometimes an interest-free promissory note is issued. In this case, the redemption amount is the same as the face value or principal amount of the note, which includes implied interest costs.

Accounting for bills of exchange

Simple interest-free bill of exchange

We suggest starting the conversation by considering the following situation: an organization selling goods receives its own simple interest-free bill of exchange from the buyer as payment for the goods.

In accounting, proceeds from the sale of products and goods, receipts associated with the performance of work, provision of services (in this case we are talking about the sale of goods) are income from ordinary activities ( clause 5 of PBU 9/99 “Income of the organization” ). Revenue is recognized when the conditions listed in clause 12 of PBU 9/99 . In this case, the amount of revenue is reflected in the credit of account 90 “Sales” and the debit of account 62 “Settlements with buyers and customers”. At the same time, the cost of goods sold is written off from the credit of account 41 “Goods” to the debit of account 90 “Sales” ( Instructions for using the Chart of Accounts ).