Regulatory regulation of commissioning

Federal Law dated December 6, 2011 N 402-FZ defines accounting

Resolution of the State Statistics Committee of the Russian Federation dated January 21, 2003 N 7 establishes unified documents

Order of the Ministry of Finance of Russia dated July 29, 1998 N 34n approves the Regulations on accounting and reporting in the Russian Federation

Order of the Ministry of Finance of Russia dated March 30, 2001 N 26n PBU 6/01

Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 N 94n approved the chart of accounts

Order of the Ministry of Finance of the Russian Federation dated October 13, 2003 N 91n regulates accounting through methodological instructions

Decree of the Government of the Russian Federation dated January 1, 2002 N 1 provides the classification of fixed assets for the purpose of depreciation

The Tax Code of the Russian Federation, Part 2, determines the initial cost of more than 100,000 rubles for tax purposes

Moment of inclusion of an asset in fixed assets

16.05.2011

Estimated reading time: 6 minutes.

The accrual of property tax is associated with the fact that property is reflected in accounting as a fixed asset. However, the legislation on accounting (PBU 6/01) does not give an exact answer at what point property should be recognized as a fixed asset.

Based on an analysis of judicial practice, the article examines various approaches to determining the moment of inclusion of a capital construction project in the composition of fixed assets.

Real estate is put into operation from the date of receipt of permission to put the facility into operation

In accordance with clauses 1, 2 of Art. 55 of the Town Planning Code of the Russian Federation, a permit to put an object into operation is a document that certifies the completion of construction […] in full in accordance with the construction permit, the compliance of the constructed […] capital construction project with the town planning plan of the land plot and design documentation and is the basis for putting the facility into operation.

Consequently, in order to comply with the requirements of urban planning legislation, the moment of completion of construction and the moment of putting the facility into operation is the date of receipt of permission to put the facility into operation. It is after this date that it is allowed to operate the facility in accordance with the norms of urban planning legislation.

An analysis of tax and accounting legislation and judicial practice confirms that, as a general rule, it is obtaining permission to put a property into operation that is the basis for including the cost of a fixed asset in the tax base for property tax.

In accordance with Art. 374 of the Tax Code of the Russian Federation, the objects of taxation for Russian organizations are movable and immovable […] taken into account on the balance sheet as fixed assets in the manner established for accounting.

The Regulations on Accounting of Fixed Assets (PBU 6/01) provide 4 conditions for including an asset in fixed assets (clause 4 of PBU 6/01):

- The purpose of the asset for use in the organization’s activities (production or rental);

- Operation for a period exceeding 12 months;

- The purpose of the asset is for the organization to obtain economic benefits in the future;

- The organization does not plan to sell the asset.

As can be seen from the above conditions, the main substantive criterion for including an asset in fixed assets is its purpose for use in production or transfer for temporary use (rent).

Typically, a completed building or structure is intended to be used for its intended purpose only after receiving permission to put it into operation, since the operation of the building without permission is not allowed.

The courts are guided by this logic when considering the issue of when an asset should be included in fixed assets and, consequently, in the property tax base.

For example, the Federal Antimonopoly Service of the North-Western District, in its Resolution dated December 17, 2008 in case No. A21-1145/2008, considered the following situation.

On September 30, 2005, a real estate lease agreement was concluded between the taxpayer and the tenant; the acceptance committee act was signed in November 2005. The taxpayer included real estate in fixed assets starting from December 1, 2005, and began calculating property tax from the same date. The tax inspectorate considered that it was necessary to begin paying tax from October 2005, i.e. after the conclusion of the lease agreement. The court recognized the taxpayer’s position as legitimate, stating the following:

“Buildings can be included in fixed assets only after they have been accepted into operation in the prescribed manner. According to paragraph 8 of the resolution of the Council of Ministers of the USSR dated January 23, 1981 N 105 “On the acceptance into operation of completed construction facilities,” the date of commissioning of the facility is considered the date of signing the act by the state acceptance commission. Thus, the Company leased out objects that were legally accounted for in account 01 after the execution and approval of the act dated November 10, 2005” [1].

A similar conclusion can be drawn from the analysis of the Methodological Recommendations for Accounting of Fixed Assets (approved by Order of the Ministry of Finance of the Russian Federation dated October 13, 2003 No. 91n).

In accordance with clause 23 of the Methodological Recommendations, fixed assets are accepted for accounting at historical cost. The initial cost includes costs associated with bringing the asset into a condition suitable for use (clause 32 of the Methodological Recommendations).

Therefore, until the measures related to bringing the asset into a condition suitable for use are completed, its transfer to fixed assets will not be legal, since the initial cost has not been formed. In particular, such measures should include obtaining all permits that remove legal obstacles to the use of fixed assets.

***

However, the date of receipt of permission to put a facility into operation is not an absolute basis for the occurrence of tax consequences.

An analysis of judicial practice shows that the inclusion of a building in fixed assets at the time of obtaining permission to commission is only a legal presumption [2] of determining the moment of commissioning (and the assessment of property taxes).

As judicial practice shows, this presumption can be rebutted in two cases:

- if the object began to be actually used before the date of receipt of permission for commissioning, or

- if the object cannot be used for its intended purpose after receiving permission to operate.

The actual moment of commissioning occurs before obtaining permission

Judicial practice of applying tax legislation is based on the principle of autonomy of tax legislation [3] and the concept of priority of substance over form.

Neither tax nor accounting laws link the transfer of an asset to account 01 (inclusion in fixed assets) with whether the requirements of industry legislation have been met (for example, in the construction industry). The only meaningful criterion for transferring an asset to fixed assets, as indicated above, is its readiness (purpose) for use in the organization’s activities. If the asset began to be operated before the date of receipt of the commissioning permit, then it is obvious that this asset is ready for use in the organization's activities.

Therefore, from the point of view of accounting and tax legislation, in the situation considered, it is the date of actual entry that should have legal significance for the calculation of property tax.

Since such a conclusion (about the actual operation of the object before receiving permission for its operation) indicates a violation by the taxpayer of the norms of urban planning legislation, the fact of operation of the object before the date of receipt of the permission must be proven by the tax authority.

In some cases, this will not pose much difficulty for the inspectorate. For example, in a situation where an organization created only for the purpose of operating an asset begins to record revenue from the sale of goods (services) produced using this asset.

In this situation, in our opinion, an additional argument in favor of the fact that the asset is not a fixed asset will be a documented argument that the asset is used in commissioning work associated with testing under load, for example, load-bearing structures, foundation , equipment. In this case, the asset is not actually used as a fixed asset, but work is carried out to bring the asset to the condition necessary for use.

The actual moment of commissioning occurs after obtaining permission

As a general rule, the obligation to pay property tax cannot depend on the discretion of the taxpayer on the issue of when exactly to begin the actual operation of the property.

However, situations are possible when obtaining permission to put an object into operation does not indicate an objective possibility of using the asset for the purposes specified in subclause. 1 clause 4 PBU 6/01. In particular, if, after receiving permission to put the facility into operation, the real estate property cannot be used for its intended purpose.

This situation was assessed by the Presidium of the Supreme Arbitration Court of the Russian Federation in Resolution No. VAS-4451/10 dated November 16, 2010.

From the circumstances of the case it follows that the taxpayer received permission to put the facility into operation and registered ownership of the hotel and administrative complex. However, after obtaining permission (and registering ownership), the building required significant capital investments (in finishing of the premises). In this regard, the taxpayer believed that the building was objectively unable to be used in the organization’s activities, since it did not correspond to its purpose.

The court of first instance satisfied the taxpayer's demands, stating the following:

“The construction of the building shell and its subsequent interior decoration should be considered as a single process of creating a hotel and administrative complex, upon completion of which an object that meets the characteristics of a fixed asset appears.”

However, the Federal Antimonopoly Service of the North-West Zone considered it legal to charge additional property tax from the moment of registration of ownership of the real estate property in July 2007.

As a result of the consideration of this case, the Presidium of the Supreme Arbitration Court of the Russian Federation supported the conclusions set out in the Decision of the Arbitration Court of First Instance.

[1] The Federal Antimonopoly Service of the Ural District came to a similar conclusion in Resolution dated September 30, 2009 No. Ф09-7348/09-С3

[2] That is assumption of the presence of any fact (in our case, the fact of putting the facility into operation) with proof of another fact (in our case, the fact of issuing a permit

[3] For example, this principle was the basis for the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation in case No. 5600/07 of September 18, 2007, adopted in favor of the taxpayer

Basis for commissioning

According to clause 8 of PBU 6/01, the initial cost of fixed assets acquired for a fee is recognized as the amount of the organization's actual costs for their acquisition, construction and production, excluding VAT and other refundable taxes.

Expert of the Legal Consulting Service GARANT E. Lazukova

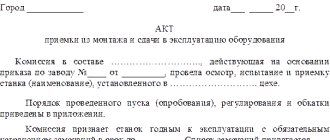

Commissioning must be documented with primary documents, which indicates readiness for its use. From January 1, 2013, it is not necessary to use forms of primary documents from albums of unified forms. Commissioning can be done using the following forms:

- OS-1 – for 1 object (except buildings)

- OS-1a – for buildings and structures

- OS-1b – for groups of objects (except buildings)

If the document is developed independently, then it is necessary to keep in mind that the form is approved by the accounting policy and contains mandatory details (Part 2 of Article 9 of Law 402-FZ):

- Name

- date of compilation

- name of the organization making the document

- reflects the fact of activity

- natural and monetary meter (indicating units of measurement)

- positions of persons responsible for registration

- signatures with transcript to identify responsible persons

Important! When purchasing, manufacturing or constructing a fixed asset in one month, and reflected in account 01 in another, it is necessary to draw up documents reflecting its unreadiness for use.

The readiness of the facility for operation can be determined by a special commission for the acceptance of acquired fixed assets, making a conclusion that is indicated in the commissioning act.

An inventory card or book must be prepared for the fixed asset (depending on the accounting used). In this case, you can use the following forms: No. OS-6, OS-6a, OS-6b.

How to properly put an operating system into operation: documents and date of acceptance for accounting

To document the process of commissioning fixed assets, enterprises can use standard forms No. OS-1 (a, b) or independently develop the form of this document. It is important that the act contains all the necessary details:

- date and number;

- information about the organization transferring the OS;

- information about the enterprise receiving the object;

- accounting information: initial cost, useful life, etc.;

- characteristics of the fixed asset, etc.

Read more about the preparation of this document in the article “Unified Form No. OS-1 - Certificate of Acceptance and Transfer of OS”.

To determine the readiness of the facility for operation, the manager issues an order to create a special commission. Its members will make a conclusion about the OS’s compliance with the technical specifications or the need for improvement. And based on the data received, the commission makes a conclusion and reflects it in the act.

Often an accountant is faced with the question: how to put into operation a fixed asset that the organization does not yet plan to use? To answer this, you need to decide what is considered the date of commissioning of fixed assets.

This date is the day when the fixed asset is completely ready for use, regardless of the moment when it actually begins to be used. After all, it is necessary to calculate depreciation according to the accounting book of the OS capitalized to the accounts. And until the fixed asset is put into operation, it will not be possible to charge depreciation.

Important! Hint from ConsultantPlus SITUATION: Is it necessary to include in fixed assets and tax property that is suitable for use, but has not been put into operation?

The organization includes property as part of fixed assets and accepts it for accounting if the object is suitable for use (clause 4 of PBU 6/01). That is, when the property is ready for use for the purposes for which it is intended. Should an organization pay tax on property that has been brought into such condition but has not yet been put into operation? Analysis of judicial practice allows us to identify several typical situations. See K+ for more details. Trial access is available for free.

Documents required for commissioning of real estate

To commission constructed real estate, the developer must obtain a special permit issued by the institution that authorized the construction (according to paragraph 2 of Article 55 of the Town Planning Code of the Russian Federation). To obtain a permit, the following documents are required:

- documents granting the right to a plot

- urban plan

- permission

- object acceptance certificate

- conclusion of Gosstroynadzor

- technical plan

Commissioning and posting must coincide.

Establishment of useful life (SPI)

The commission for accepting fixed assets for accounting establishes the SPI required for calculating depreciation from the month following registration. The period during which the original cost is written off is established based on the depreciation group, respectively, and the SPI, i.e. time of use for generating income, mode, number of shifts and operating conditions, repairs and other restrictions (for example, rental period). The SPI must be issued by order of the manager (in any form), and which can be revised as a result of reconstruction, retrofitting, etc. fixed asset.

Important! It is better to set the SPI for accounting and tax accounting purposes to be the same so as not to reflect temporary differences.

SPI is important for property taxation: the larger it is for accounting purposes, the longer the organization pays property tax. But this needs to be justified in the order.

Commissioning accounting

In accounting, the initial cost of purchased fixed assets is the sum of all expenses of the organization, except for VAT and other refundable taxes.

The cost of these funds is reimbursed by calculating depreciation based on SPI, i.e. The more SPI, the slower its cost decreases.

In accounting (not in tax accounting) you can set any period and when determining it you can, but not necessarily, be guided by the Classification. But this period must be justified by the presented indicators, documentation, etc.

Accounting for the input of fixed assets

Accounting for the costs of commissioning a fixed asset must be carried out in the manner established by the organization.

| Operation | Debit | Credit |

| Receipt from the founders | ||

| Founders' debt | 75-1 | 80 |

| Receipt on account of contribution to the authorized capital | 08 | 75-1 |

| Construction by contract (third-party organization) | ||

| Formation of the cost of contract work | 08 | 60 |

| Construction in an economic way (by the organization itself) | ||

| Write-off of materials for construction | 08 | 10 |

| Payroll for employees (builders) | 08 | 70 |

| Purchase (without installation) | ||

| Accrual of payment amounts to the supplier | 08 | 60 |

| Delivery accounting | 08 | 76,60,23… |

| Purchase (with installation) | ||

| Accrual of payments to the supplier for equipment | 07 | 60 |

| Transfer of equipment for installation | 08 | 07 |

| Write-off of installation costs | 08 | 10,70,69… |

| Receive for free | ||

| Acceptance of fixed assets for accounting (account 91) | 01 | 91 |

| Putting the facility into operation | 01 | 08 |

At the same time, VAT is a refundable tax and is not taken into account in the initial cost.

Accounting for the receipt of fixed assets by the enterprise in 2021

> fixed assets and intangible assets > Accounting for the receipt of fixed assets by an enterprise in 2021

In the previous article we got acquainted with fixed assets, here we will figure out how accounting is kept when they arrive at the enterprise, what documents are used to document this, and what entries are reflected in accounting.

The process as a result of which fixed assets appear in an enterprise is called long-term investment.

Primary documents upon admission

Receipt of a fixed asset item is accompanied by the execution of one of the following documents:

- acceptance certificate: three forms are provided: OS-1, OS-1a and OS-1b; the first form is intended for the acceptance of any OS object with the exception of buildings and structures, the second form is filled out when accepting buildings and structures, and the third when receiving a group of OS objects.

- equipment acceptance certificate, has a unified form OS-14;

- certificate of acceptance and transfer of equipment for installation OS-15.

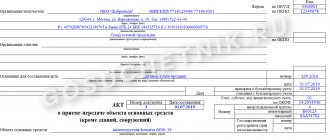

Based on the act of acceptance of the OS, an inventory card is filled out for each object; there are three standard forms:

- OS-6 is issued for one object;

- OS-6a is issued for a group of objects;

- OS-6b – inventory book.

Methods of joining the organization

OS objects can arrive at the enterprise in one of the following ways:

- capital construction,

- acquisition for a fee (purchase),

- free admission,

- capital contribution,

- acquisition under a barter agreement.

Capital construction

The construction of the OS can be carried out in-house or by contract.

The contracting method implies the construction of a facility using the services of third-party organizations. The basis for such cooperation is a contract concluded between the supplier and the customer.

The economic method involves construction by the enterprise itself, without the involvement of third parties.

In this case, all actual expenses are posted to the debit of account 08.3 “Construction of fixed assets”, and the initial actual cost is reflected in account 01 “Fixed assets”.

Postings during construction (creation):

Acquisition for a fee (purchase)

When purchasing a fixed asset, debit account 08 collects all the actual costs of purchasing the asset: the cost itself according to the supplier’s documents, transportation costs, installation costs and other costs minus VAT. All these actual costs will constitute the initial cost of the object, at which it will be recorded in account 01.

Postings upon purchase:

Free admission

The value of a donated asset is determined based on the market value on which value added tax is charged. The market value established for the object must correspond to the date of its acceptance by the enterprise and be documented; these documents must be attached to the acceptance certificate.

Fixed assets received as a gift are recognized as non-operating income of the enterprise.

The entries for accounting for gratuitous receipt of fixed assets are as follows:

- D08 K98.2 – the object is accepted for accounting;

- D01 K08 – OS put into operation.

Depreciation on such assets is written off from the debit of account 98.2 and recognized as other income of the organization - entry D98.2 K91.1.

Contribution to the authorized capital

Fixed assets can also come to the organization from the founder as a contribution to the authorized capital. In this case, the initial cost of the fixed asset is calculated based on the value determined by the founders themselves and is called agreed upon, and is stated in the constituent documents. If the cost is over 200 minimum wages, then an independent assessment by an expert is necessary.

Postings when contributing fixed assets to the authorized capital:

Purchase under an exchange agreement

As a rule, the acquisition of fixed assets under an exchange agreement is quite rare, but causes great difficulties for accountants. The Civil Code of the Russian Federation specifies the procedure for drawing up an exchange agreement. It stipulates that each party to legal relations is obliged to transfer one object into the ownership of a third-party organization in exchange for another. Concluding such a transaction assumes that the objects are of equal value. If the price of one of the objects is lower, its owner is obliged to compensate the counterparty for the difference in cost.

The procedure for accounting for the disposal of fixed assets can be found here.

We also offer tasks with answers on the topic “Accounting for fixed assets.”

: postings upon receipt of OS using examples

Rate the quality of the article. We want to be better for you:

fixed assets and intangible assets

Source: https://buhland.ru/uchet-postuplenie-osnovnyx-sredstv-na-predpriyatie/

Example of transactions when purchasing fixed assets

Alpha and Omega LLC acquired a fixed asset for 236,000 rubles from Beta and Gamma LLC. (including VAT 36,000 rubles) for use in production activities. Both organizations are VAT payers. The transactions will be reflected in the accounting records as follows:

| Operation | Debit | Credit | Sum | Base |

| Fixed asset has arrived | 08 | 60 | 200000 | Acceptance certificate |

| VAT on fixed assets is reflected | 19 (VAT subaccount) | 60 | 36000 | Invoice |

| Payment for fixed assets (including VAT) | 60 | 51 | 236000 | Payment order |

| Submission of VAT for deduction | 68 | 19 (VAT subaccount) | 36000 | Book of purchases |

| Commissioning | 01 | 08 | 200000 | Act OS-1 |

Tax accounting of introduced fixed assets

The procedure for calculating the initial cost of an introduced fixed asset does not depend on whether new fixed assets are being introduced or used ones and the entire amount of costs for the acquisition (manufacturing), delivery, repair (modernization) is taken into account, minus VAT and excise taxes, but when purchasing a fixed asset that has already been used by the seller, the reflection of the residual value according to the supplier’s documents and already accrued depreciation should not be taken into account.

When commissioning, it is necessary to establish a period of use as in accounting, determined independently on the date of commissioning, taking into account the classification. But for used fixed assets, the depreciation rate should take into account the SPI, when operated by previous owners based on their useful life:

- by classification (also applies to the acquisition of property from individuals - not individual entrepreneurs)

- established by classification and reduced by the period of use by the former owners in fact

- established by the previous owner and reduced by the period of use by the previous owners in fact

Reflection of interest on credits (loans) used for the purchase of fixed assets

When creating entries to reflect interest accrued on loans and credits used to purchase fixed assets, special attention should be paid to the difference in requirements for accounting for these transactions in accounting and tax accounting: Accounting

— the amounts of interest accrued before the facility was put into operation increase the cost of the non-current asset (entry Dt 08 - Kt66, 67).

Interest accrued after commissioning is included in other expenses of the organization (entry Dt 91 - Kt 66.67). Tax accounting

- for tax accounting purposes, the amount of accrued interest is included in the expenses of the reporting period, within the limits established by Article 269 of the Tax Code of the Russian Federation.

| Account Dt | Kt account | Wiring Description | Transaction amount | A document base |

| Postings reflecting the accrual of interest on loans and borrowings before the facility is put into operation | ||||

| 08.4 | 66 | The cost of interest on short-term loans is taken into account | ||

| 08.4 | 67 | The cost of interest on long-term loans is taken into account | ||

| Interest on loans and borrowings (used for the purchase of fixed assets) accrued after the object is put into operation | ||||

| 91.2 | 66 | The cost of interest on short-term loans is taken into account | ||

| 91.2 | 67 | The cost of interest on long-term loans is taken into account | ||

Answers to common questions

Question No. 1 : When purchasing from an individual, can it be accepted for accounting on the basis of a purchase and sale agreement and a transfer and acceptance certificate?

Answer : An individual seller does not have the obligation to provide forms OS-1 (OS-1a), therefore, to accept property for accounting, it is sufficient to accept transfer and acceptance certificates in any form, but with the obligatory indication of details, in accordance with 402-FZ for primary documentation.

Question No. 2 : Is it necessary to put into operation what is planned to be rented out (leasing)?

Answer : In order to start using it as a rental property (to generate income), it must be put into operation on account 03: D03 K08.

The fixed asset transaction object has been accepted for accounting. Receipt of fixed assets to the enterprise

Fixed assets are assets that are directly used to produce products, provide services and perform other functions of the enterprise and have a service life of at least one year. In addition to those in operation, part of the fixed assets may be kept in stock or leased. Read about OS rental. Depreciation of fixed assets subject to wear and tear, for example, machine tools or vehicles, is taken into account in the cost of manufactured products (services provided).

We discussed the concept and classification of fixed assets in , here we will dwell in more detail on the features of accounting for their receipt by the enterprise, consider the entries made when accepting fixed assets for accounting in the case of construction, purchase, gratuitous receipt, as well as when receiving an object in the form of a contribution to the authorized capital.

Accounting for receipt of fixed assets

OSes put into operation are accounted for using account 01. The basis for commissioning is an order from the head of the enterprise. The accounting department draws up transfer and acceptance reports and records fixed assets on inventory cards (type OS-6).

Most often, the arrival occurs as a result of:

- completion of construction

- acquisitions for a fee (OS purchase)

- receiving free of charge

- receipts in the form of a contribution to the authorized capital.

In accordance with this, the accounting for the receipt of such funds is somewhat different. Let's consider each case separately.

How is the initial cost of fixed assets formed for each method of receipt:

Accounting for construction projects accepted for operation

The formation of the initial cost of a commissioned facility during construction is determined by the cost of its construction. These costs are reflected on the balance sheet. The construction of facilities can be carried out by the enterprise or with the involvement of contractors.

In the case of construction with the help of a third-party developer, the account “Settlements with suppliers and contractors” (account 60) is used.

Accounting entries during the construction of an OS facility by third parties:

- D08 – K60 – the full cost of the work has been determined

- D19 – K60 – VAT allocated

- D01 – K08 – construction project accepted for operation

- D68 – K19 – allocated VAT is sent for reimbursement from the budget

- D60 – K51 – funds transferred to the contractor.

If construction is carried out on its own, then to record the costs of it, the accounts “Materials” (10), “Settlements with personnel for wages” (70), “Auxiliary production” (23), “Depreciation” (02) and others are used. In this case, the postings are made:

- D08 – K10 (02,23,70,69, etc.) – construction costs are taken into account

- D01 – K08 – the facility has been put into operation.

Accounting for fixed assets upon purchase

Purchase is the most common type of receipt. To account for such funds, the accounts “Settlements with suppliers and contractors” (account 60) or “Settlements with various debtors and creditors” (account 76) are used. Depending on the type of funds purchased, corresponding subaccounts are opened to the “Investments in non-current assets” (08) account.

The initial cost of acquired assets is the sum of all costs associated with their purchase and commissioning. Such expenses, in addition to the amount paid to the seller, may include: customs duties, non-refundable taxes, state duties, fees for intermediaries and consultants, as well as funds spent on installation and commissioning of equipment.

Accounting entries for the purchase of fixed assets:

- D08 – K60 (76) – the cost of the object is taken into account according to the supplier’s documents

- D19 – K60 (76) – VAT is allocated from the cost of the object

- D08 – K70 (69, 76, 10, etc.) – costs for delivery, assembly, adjustment are taken into account

- D01 – K08 – object accepted for operation

- D68 – K19 – VAT is sent for reimbursement from the budget

- D60 (76) – K51 – funds transferred to the supplier.

Accounting for fixed assets when received free of charge

The initial cost of fixed assets of an enterprise that were accepted free of charge, for example, in the form of a gift, is considered to be the market value of such objects. If it is impossible to determine it, the assessment is based on the cost of similar material assets. According to the Tax Code of the Russian Federation, funds received free of charge are considered non-operating income of the enterprise.

Postings when receiving fixed assets free of charge:

For accounting purposes, the subaccount “Gratuitous receipts” (98-2) is used. The following entries are reflected in the accounting records:

- D08 – K98-2 – OS accepted for accounting

- D01 – K08 – objects put into operation.

- D98-2 – K91 – depreciation charges are written off.

Receipt as a contribution to the authorized capital

Fixed assets received as a contribution to are accounted for at the cost agreed upon by the founders of the organization (joint stock company). If necessary, resort to the services of an independent appraiser.

Reflected using the account “Authorized capital” (80), the subaccount “Calculations for contributions to the authorized capital” (75-1).

The wiring is as follows:

- D75-1 – K80 – the debt of the founders has been formed

- D08 – K75-1 – funds received as a contribution to the authorized capital of the organization

- D01 – K08 – the object has been accepted for operation.