Amount of benefit at the labor exchange

In each individual case, temporarily unemployed citizens may receive a different amount of compensation payments.

The amount of the benefit depends on:

- Average income at previous place of employment;

- The duration of the period between dismissal and registration;

- Duration of registration for unemployment.

When calculating benefits, the average earnings of the unemployed for the last quarter of official work are taken into account. Data on past wages must be provided to the labor exchange in a special certificate, which will indicate not only the amount of the salary, but also the dates of hiring and dismissal.

If you are dismissed due to a disciplinary offense, the amount of benefits will be reduced. The percentage by which payments will be reduced is set individually, taking into account the severity of the violation and the scale of the damage.

If the unemployed person has not previously been employed or the time interval between dismissal and registration exceeds a year, he will be assigned the minimum benefit rate, without taking into account past wages.

The longer a citizen maintains his unemployed status, the lower his payments. In the first three months, an unemployed person can receive up to 75% of their previous salary.

Expert opinion

Korolev Konstantin Georgievich

Practicing lawyer with 7 years of experience. Specialization: criminal law. More than 3 years of experience in document examination.

In the future, the amount will be reduced to 60% from the fourth to seventh months of being on the labor exchange. For ordinary citizens, the period for receiving benefits is 6 months.

Pre-retirees from the eighth month to a year can receive an amount not exceeding 40% of their previous salary.

If the temporarily unemployed period lasts more than a year, the citizen will receive the minimum rate of employment center benefits.

Important. As of 2021, the minimum unemployment benefit is 1,500 rubles.

Preferential conditions for being registered and increased benefits are provided for:

- Pregnant women fired due to the closure of the enterprise. They are provided with compensation payments of 100% of their previous salary until they go on maternity leave.

You can find out how much benefit you will receive before registering. To do this, you can use an online calculator:

To accurately calculate unemployment benefits, use the online calculator

Are taxes withheld from unemployment benefits?

I am an orphan. How much income tax is withheld from my unemployment benefits? I'm currently being charged 20%. Is this legal?

According to the general rule (clause 1 of Art.

210 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code of the Russian Federation)), when determining the tax base for personal income tax (hereinafter referred to as personal income tax), all income of the taxpayer received by him both in cash and in kind, or the right to dispose of which he has, is taken into account. it arose, as well as income in the form of material benefits, determined in accordance with Art. 212 of the Tax Code of the Russian Federation.

However, in Art. 217 of the Tax Code of the Russian Federation contains a list of income that is not taxed. These include, in particular, unemployment benefits.

- failure to appear without good reason for employment negotiations with the employer within three days from the date of referral by the employment service;

- refusal without good reason to appear at the employment service to receive a referral to work (training).

The above may cause your benefits to be reduced.

Unemployment benefits are paid subject to strict conditions, which are verified by the Employment Centre. The size of the benefit is small, and the Russian Government justifies its size by encouraging citizens to find a job faster, rather than live on state benefits. Is it really necessary to pay income tax on this small amount?

Is retained earnings subject to personal income tax during the period of employment?

I recommend that you go to court with a claim for recognition of the illegality as invalid in accordance with paragraph 6 of Part 2 of Art. 101 Federal Law on Enforcement Proceedings, the bailiff provides a property tax deduction for the purchase of housing indicating the “corresponding approximate cost.”

In relation to a technically complex product, if defects are discovered in it, the consumer has the right to refuse to fulfill the purchase and sale agreement and demand a refund of the amount paid for such a product or make a demand for its replacement with a product of the same brand (model, article) or with a different product. brand (model, article) with a corresponding recalculation of the purchase price within fifteen days from the date of transfer of such goods to the consumer. After this period, these requirements are subject to satisfaction in one of the following cases: discovery of a significant defect in the product, violation of the deadlines established by this Law for eliminating defects in the product, impossibility of using the product during each year of the warranty period for a total of more than thirty days due to repeated elimination of its various defects. ..

Are unemployment benefits subject to personal income tax?

Article 208 of the Tax Code of Russia specifies the income of individuals from sources in the country and abroad. According to the general meaning of paragraph 11 of the article, it is clear that benefits are also income of an individual. And Article 209 of the Tax Code of the Russian Federation states that the object of personal income tax is the income of citizens in the country and abroad.

Therefore, personal income tax must be paid on unemployment benefits. However, clause 1 of Article 217 of the Tax Code of the Russian Federation states that all types of state benefits are exempt from income taxation, except leave for temporary disability, and unemployment and maternity benefits are included in the exemption.

There is no income tax on unemployment benefits.

But if you have any other income, for example, you sold a car, garage, rented out an apartment or transport, then you need to report this income to the Federal Tax Service by filing a 3-NDFL declaration, and then pay the tax itself, if the amount thereof is deduced from the calculation.

Results

- Unemployment benefits are an individual’s income and subject to personal income tax.

- However, according to Article 217 of the Tax Code of the Russian Federation, unemployment benefits are exempt from income tax.

- You can find out about the size and history of benefit payment at the employment center that assigned you the benefit.

I tried very hard when writing this article, please appreciate my efforts, it is very important to me, thank you!

Unemployment benefits and personal income tax are connected only by the need to confirm your income in the form of a 2-NDFL certificate from your last place of work to establish the status of unemployed and receive subsidies at the time of lack of employment. 2-NDFL is issued at the previous place of work in accordance with paragraph 3 of Article 230 of the Tax Code of the Russian Federation.

Also, according to the tax code, or more precisely according to paragraph 1 of Article 217, personal income tax is not included in the calculation of unemployment benefits. This allows you to accurately say whether the personal income tax benefit is subject to tax or not - it is not, since this point is enshrined in the law.

basic information

Personal income tax is assessed only on a number of incomes from places of employment. All other payments, including unemployment benefits, do not have such deductions.

Unemployment benefits can only be received by certain categories of citizens who meet all the requirements and have fulfilled all the conditions.

Also, benefits are not provided to the following categories:

- having an age of less than 16 years, that is, at the age of 16 you can already join the stock exchange if there is no permanent or temporary income;

- all full-time students;

- pensioners;

- IP;

- disabled people with non-working groups (most often they do not include group 3, which allows full work, but with a number of restrictions);

- to all persons who apply at the place of temporary registration, since registration and obtaining status is regulated only at the place of permanent registration and residence;

- convicted and sent by the court to correctional or community service;

- any person who provided false information when contacting.

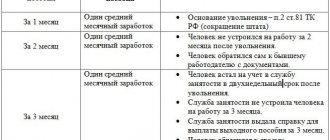

This benefit is a one-time cash payment to a dismissed employee. Benefit accrual is possible in the following situations:

Is retained earnings subject to personal income tax during employment?

Determine the number of working days based on your company’s work schedule. For example, if an employee is laid off on 02/15/2021, the second month will begin on 03/16/2021 and end on 04/15/2021. If the employee is employed before the end of the second or third month, count only the days before starting a new job.

An employee’s average daily earnings are due for each working day of the second month of employment (from 03/02/2021 to 04/01/2021), that is, for 20 days. The average earnings for this month are 27,149.40 rubles. (RUB 1,357.47 x 20 days).

We recommend that you read: Deductions under a writ of execution in kudir

Amount of payments in different situations

The amount of the benefit may vary, its size depends on the circumstances of termination of the employment contract and the employee’s average salary for the last year before dismissal:

- in case of liquidation of an enterprise or reduction of its staff, the benefit is equal to a monthly salary . If a citizen was unable to find a job within 2 months, then he is entitled to another payment - in the amount of 2 monthly salaries. When terminating a contract with a seasonal worker, he is entitled to benefits in the amount of 2 weeks' earnings. Severance pay is provided if an employment contract was concluded between a citizen and an organization. If the contract was concluded with an individual entrepreneur, then the employee is entitled only to those payments that are specified in the employment contract. In their absence, severance pay upon dismissal due to liquidation of the organization is not paid;

- upon termination of an employment contract due to the employee’s inability to perform his job duties for health reasons , the employer is obliged to pay severance pay in the amount of the employee’s earnings for 2 weeks;

- upon dismissal due to conscription for compulsory military service , due to the impossibility of moving to another locality for work reasons, the citizen is paid an allowance in the amount of 2 weeks’ salary.

Are severance pay and earnings during the period of employment subject to personal income tax and insurance contributions?

Upon dismissal, the employee is paid severance pay

in the amount of

average monthly earnings

, and also retains

the average monthly earnings

for the period of employment, but not more than two months from the date of dismissal (including severance pay).

Quote (Oksana Efimovna): Upon dismissal, the employee is paid severance pay

in the amount of

average monthly earnings

, and also retains

the average monthly earnings

for the period of employment, but not more than two months from the date of dismissal (including severance pay).

Personal income tax on severance pay

Severance pay is income received by a citizen. Therefore, according to the law, severance pay is subject to personal income tax (personal income tax). The state considers this type of benefit as a compensation payment and therefore provides preferential taxation.

The personal income tax rate is currently 13% for residents of the Russian Federation and 35% for citizens of other countries working in Russia.

- Fine for late filing of personal income tax declaration 3

- Property tax formula: holding period coefficient

- Accounting policies for tax purposes: how to apply, sample order for 2021

- Fine for non-payment of taxes by individual entrepreneurs

- Accounting for calculations of taxes and fees in the balance sheet

- Find out tax debt using TIN: how to find and pay for individuals

- Simplified taxation system: transition for individual entrepreneurs, types of activities, forms, necessary documents

Insurance premiums and personal income tax on average earnings for the period of employment

The use of account 76 “Settlements with other debtors and creditors” for settlements with former employees is due to the fact that account 70 takes into account only settlements with personnel working in the organization at the time of payment accrual (Instructions for the chart of accounts).

An example of how severance pay is reflected in accounting for an employee dismissed during the liquidation of an organization P.A. Bespalov works as a storekeeper at Alpha LLC. On January 13, he was fired due to the liquidation of the organization. When an employee is dismissed due to liquidation, the organization pays him severance pay in the amount of average monthly earnings. Bespalov's average daily earnings is 484 rubles/day. The severance pay was calculated for the first month after dismissal - from January 14 to February 13. In this period, according to Bespalov’s work schedule (five-day work week), there are 23 working days. The severance pay amounted to 11,132 rubles. (484 RUR/day × 23 days). Bespalov received it on the day of his dismissal, January 13. The Alpha accountant made the following entries in accounting: Debit 25 Credit 70 - 11,132 rubles. – severance pay accrued; Debit 70 Credit 50 – 11,132 rub. - severance pay was issued.

Unemployment benefit

Briefly about who can be recognized as unemployed:

- able-bodied citizens from 18 to 55 years (women), up to 60 years (men);

- persons who do not have an official place of employment at the time of contacting the employment service;

- citizens registered at the employment center.

These requirements must be present together.

Calculation of unemployment benefits is carried out by specialists from the employment center. The size of the payment depends on the average salary and the availability of employment during the year before contacting the employment service. You can read more about this on the pages of our Internet portal.

Unemployment benefits are not interpreted by law as income, therefore they are not subject to taxation (clause 1, article 217 of the Tax Code of the Russian Federation).

Saved earnings during employment are subject to personal income tax

At the same time, the Labor Code of the Russian Federation does not provide for the payment of severance pay and average earnings for the period of employment upon dismissal of managers (their deputies, chief accountants) on these grounds. For more information about this, see When you need to pay severance pay, average earnings for the period of employment and compensation upon dismissal.

— if the tax is not withheld, but payments will still be made in 2021, then upon subsequent payment, the tax agent has the right to withhold the amounts of personal income tax not withheld in a timely manner, but not more than 50% of payments (clause 4 of Article 226 of the Tax Code of the Russian Federation). - if the tax is not withheld and payments will not be made in 2021, then by virtue of clause 5 of Art. 226 of the Tax Code of the Russian Federation, it is necessary to send a message to the tax authority about the impossibility of withholding tax and the amount of tax not withheld in the form approved. By order of the Federal Tax Service of the Russian Federation dated November 17, 2021 N ММВ-7-3/, no later than one month from the end of the tax period.

Documents for applying for unemployment benefits

Next, we list what documents are needed for unemployment benefits (clause 7 of the Procedure for registering the unemployed):

- passport;

- work book (if available);

- salary certificate from last place of work. It is worth noting that such a document is needed if a citizen has been officially employed for 1 year before applying to the employment service. This certificate is necessary for calculating unemployment benefits, therefore there are special requirements for its execution:

- the document must be drawn up on the organization’s letterhead indicating its details, in particular – TIN and legal address,

- the document must bear an imprint of a corner stamp,

- It is mandatory to indicate the number of weeks worked during the last year of work;

- certificate of assignment of TIN;

- pension insurance certificate;

- all documents indicating the education received . It is worth considering that in addition to the document on basic education, you can submit certificates, diplomas, certificates of all additional acquired skills and knowledge. If such a document was received outside the Russian Federation, then a notarized translation into Russian must be attached.

Expert opinion

Korolev Konstantin Georgievich

Practicing lawyer with 7 years of experience. Specialization: criminal law. More than 3 years of experience in document examination.

Citizens who have not worked during the year before contacting the employment center or have not worked at all must present only a passport and a certificate of education. All other documents - only if they are available.