Why declare a transition to the simplified tax system?

The simplified tax system, as well as imputation and patent, are voluntary tax regimes and can be used by individual entrepreneurs and organizations at their own discretion, subject to the appropriate conditions.

When registering an entrepreneur or legal entity, it is automatically transferred to the OSNO if the notification for the transition to the simplified tax system is not provided to them within 30 days after registration.

OSNO is one of the most complex and economically unprofitable tax regimes for small businesses. In most cases, it is used when, due to the number of employees and cash turnover, a company or individual entrepreneur cannot apply the simplified tax system or UTII, or, in the case where the taxpayer cooperates mainly with counterparties interested in offsetting the “input” VAT.

If, when registering, an individual entrepreneur or organization forgot to submit a notification for the use of UTII or the simplified tax system, they will be able to switch to the special regime only next year.

The application of the simplified tax system is carried out only after notifying the tax authority about this and registering the specified person as a simplified tax payer. Without notification, you cannot switch to a simplified tax system, both during initial registration and when changing the taxation regime.

In what cases is a notice of transition to a simplified tax system submitted?

Business entities have the right to independently choose the taxation regime.

The transition to another system is made voluntarily once a year. If the company meets the requirements listed in Art. 346.12 of the Tax Code of the Russian Federation, and wants to switch to the special regime from next year, she can submit to the tax authorities a notification about the transition to the simplified tax system before December 31 of the current year. Newly created enterprises should decide on the choice of a simplified taxation system no later than 30 days from the date of registration.

Read about the transition to a simplified system, including the deadlines for submitting notifications, in this section.

Notification form according to form 26.2-1

At the moment, there is no unified notification form that is mandatory for use when switching to the simplified tax system. An organization or individual entrepreneur can use both Form 26.2-1 recommended by the Federal Tax Service of the Russian Federation and one developed personally. However, in order to avoid possible refusals at the level of local inspectorates, we recommend drawing up and submitting a notice of transition to the simplified tax system in form 26.2-1, recommended by the Federal Tax Service.

notifications about the transition to a simplified taxation system.

There is no special procedure for filling out this document; a list of the main codes that will be needed to enter information is given at the bottom of the notification.

Form for notification of transition to the simplified tax system in 2020-2021

The notification form for the simplified tax system for 2020-2021 was approved by order of the Federal Tax Service of Russia dated November 2, 2012 No. ММВ-7-3/ [email protected] This document is accepted by the tax inspectorate in the event of a voluntary change of regime from the next tax period until the last day of December of the current year inclusive, and if it is a non-working day, then until the first working day of the next year. When filling out the form, you must select the future object of taxation - “income” or “income minus expenses.”

For information on how to decide on an object, read the publication “Which object is more profitable - “income” or “income minus expenses?”

Follow the link below for notifications about the transition to the simplified tax system for free:

You can find a sample and line-by-line algorithm for filling out a notification in ConsultantPlus. A free trial of full access to the legal system is available.

Submission deadlines

The deadline for submitting a notification directly depends on the reasons for which an organization or individual entrepreneur is switching to the simplified tax system:

- When registering an LLC or individual entrepreneur for the first time, the notification must be submitted either simultaneously with the general package of documents for registration, or within 30 days after it.

As mentioned above, if a businessman forgets to submit an application to switch to a simplified tax regime within thirty days, he will automatically be transferred to the general taxation regime, which he will be able to change only next year.

- An existing organization or individual entrepreneur, when switching from another taxation system or when opening a new type of activity for which it is planned to apply the simplified tax system , must submit an application no later than December 31 of the year preceding the one from which the simplified tax system will be applied.

Sample filling in 2021

note

that in the paragraph – “Taxpayer Identification”, the number “1” will only appear if you are going to submit an application simultaneously with documents for registration; number “2” - if you submit a document within thirty days from the date of registration, or when transferring from the UTII system; number “3” – when switching from other taxation systems, except for UTII.

Free tax consultation

Sample for individual entrepreneurs and LLCs submitting an application along with documents for registration

Sample for individual entrepreneurs and LLCs submitting an application within 30 days after registration or when switching from UTII

Sample for individual entrepreneurs and LLCs switching from other taxation systems (except UTII)

Why is it recommended to submit a notification simultaneously with the registration of an individual entrepreneur/LLC?

The recommendation to submit a notice of transition to the simplified system along with the main package of documents is associated with eliminating the risk of transfer to OSNO if an entrepreneur or LLC forgot to submit the specified document, which happens quite often. Postponing the submission of an application “for later” threatens an individual entrepreneur or company with the need to pay three main OSNO taxes, as well as submitting a full package of documents, including tax and accounting reporting.

To prevent a possible outcome, it is recommended to submit Notice 26.2-1 along with all documents submitted for registration.

How to switch to the simplified tax system immediately after registering a business

and fill it out. Here are some rules:

- Fill out the application on the computer in capital letters. Each cell contains one character.

- If you submit an application simultaneously with documents for registration of an individual entrepreneur or LLC, do not fill out the TIN and KPP.

- Tax authority - tax office according to the registration of the individual entrepreneur and the registration address of the LLC.

The application contains tips on how to fill it out. If you find it difficult to understand, look at the sample.

✉️ Print out the completed application in two copies and take it to the tax office. Give one copy to the inspection officer, and on the second he will put a mark indicating that he accepted the application.

Article: What if you didn’t have time to switch to the simplified tax system

Course for a young entrepreneur: 11 videos with Elba’s advice

Open an IP for free in 5 minutes

Elba will prepare documents for registration, and the application for the simplified tax system will be included. After opening a business, submit your reports for free for a whole year!

Prepare documents Submit reports for free The promotion is valid for individual entrepreneurs under 3 months

Sample filling

Let's briefly look at examples of filling out notifications in different situations.

Sample of filling out form 26.2-1 when submitting simultaneously with the general package of documents for registration.

For individual entrepreneurs upon initial registration

Filling procedure:

- In block 1, you must indicate the TIN of the individual.

If it is not there, then the line needs to be crossed out.

- In block 2 you need to reflect the code of the tax authority to which the application will be submitted and the taxpayer’s characteristics.

The code of the tax authority to which the application is submitted can be found using a special service on the website of the Federal Tax Service of the Russian Federation.

When submitting an application along with documents for registration, the taxpayer’s identification is indicated as “1”.

- In block 3, the full name of the individual entrepreneur submitting the specified document is indicated.

- In block 4 , code 2 is indicated, in the remaining cells dashes are placed.

- Block 5 reflects the code corresponding to the type of the selected object according to the simplified tax system: “ 1 ” - for the object “Revenue” 6% and “ 2 ” - for the object “Revenue minus expenses” 15%.

- Block 6 indicates the year the document was submitted.

- In block 7, the code “ 1 ” is entered if the notification is submitted by the future individual entrepreneur himself and “ 2 ” if his representative.

If the code “ 1 ” is entered, then the bottom 3 lines are crossed out and only the contact phone number, the date of filling out the application and the signature of the individual entrepreneur are indicated.

If the code “ 2 ” is entered, then in the bottom three lines you must indicate the full name of the individual entrepreneur’s representative, then the contact phone number and, at the very bottom, information about the document confirming the authority of the representative.

All other lines, as well as lines that are not completely filled in, are crossed out.

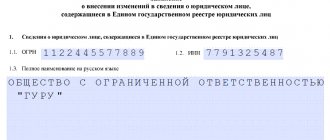

For LLC upon initial registration

Form of transition to simplified tax system: additional information

In the form for switching to the simplified tax system in 2020-2021, submitted to the Federal Tax Service by already operating firms, in addition to the selected taxable object, information on income for 9 months of the current year and the residual value of fixed assets as of October 1 are indicated. There is no requirement to report the average number of employees and other data affecting compliance with the criteria for applying the simplified tax system. But keep in mind that the tax office can check some of the criteria independently using the Unified State Register of Legal Entities, and some - during an on-site or desk audit. Therefore, you should not count on the possibility of using the simplified tax system if there is at least some discrepancy with the standards specified in paragraph 3 of Art. 346.12 Tax Code of the Russian Federation.

For information on the amount of income that gives the right to the simplified tax system, see the material “Income limit when applying the simplified tax system .

How to receive a letter about the application of the simplified tax system

In order to receive an information letter on the application of the simplified taxation system, you must write an application to the tax authority at the place of registration of the organization or individual entrepreneur. The application is written in free form. The letter must be addressed to the head of the tax authority to which you are submitting this application. His position, last name, first name, patronymic will need to be clarified with the tax office itself or on its official website. Next, you need to indicate who this letter is from; the name of the organization, its INN, OGRN, address, telephone number are indicated here. If there is a number for the outgoing letter, then it must be indicated, as well as the date of the letter. If the application is submitted by an individual entrepreneur, then he indicates his last name, first name, patronymic in full, his INN and OGRN. Next, write the word “Application” and below the text of the letter. The text of the letter may be as follows: “Please provide an information letter about our organization’s current application of a simplified taxation system for provision to interested parties.” Next, indicate the position of the employee, his last name, initials, signature and seal of the organization. For an individual entrepreneur, the text may be as follows: “Please provide an information letter stating that I, as an individual entrepreneur, currently apply a simplified taxation system. The letter must be submitted to the bank (or at the place of request).” Next, indicate his last name, initials, signature and, if there is a seal.

After this, the application must be taken to the tax authority and registered. Within 30 days after registration of this letter, the tax authority is obliged to respond. The response will be issued in form 26.2-7 (Order of the Federal Tax Service No. MMV-7-3 / [email protected] dated November 2, 2012).

What is a notice of application of the simplified tax system

Important! Notification of the application of the simplified taxation system, abbreviated as simplified tax system, is currently not issued by tax authorities by organizations or individual entrepreneurs . However, when taxpayers contact the tax authorities, they can receive confirmation that they are on a simplified taxation system. Currently, such a notification looks like an information letter. This letter will indicate the date of filing an application to begin applying the simplified taxation system by an organization or individual entrepreneur.

What conditions must be met to switch to the simplified tax system from 2021

At the end of the year, it's time to decide whether to switch to simplified or not. Make a decision and select the object of taxation (“income” or “income minus expenses”). Also check whether the conditions for the transition to the simplified tax system from 2021 are met, namely:

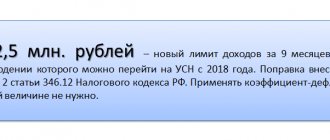

| 1 | Income for 2021 – no more than 150 million rubles. (Letter of the Ministry of Finance dated August 25, 2017 N 03-11-06/2/54808). To switch from the OSN to the simplified tax system from 2021, income for 9 months of 2021 must be no more than 112.5 million rubles. |

| 2 | The accounting residual value of fixed assets is a maximum of 150 million rubles. |

| 3 | The average number of employees is no more than 100 people. |

| 4 | The maximum share of other organizations in the authorized capital is 25%. |

| 5 | The organization has no branches. |

If everything is ok, then you can submit a notification to the Federal Tax Service about the transition to a simplified taxation system from the beginning of next year.

You can switch from the OSN to the simplified tax system only from the beginning of the new year 2021. To do this, no later than December 31, submit a notification to the Federal Tax Service (clause 1 of Article 346.13 of the Tax Code of the Russian Federation).

What will the tax office answer?

The Federal Tax Service will confirm the transition to simplified taxation in a response document within 30 days. The confirmation is drawn up according to the unified form 26.2-7 (approved by order of the Federal Tax Service No. ММВ-7-3/ dated 02.11.2012). In the response letter, the Federal Tax Service confirms the transition of an organization or individual entrepreneur to a simplified taxation system, indicating the date of receipt of the application for the transition and the date of filing the tax return of the simplified tax system.

If the customer has requested confirmation of the application of the simplified taxation system in the notice, the supplier has the right to provide a copy of this letter as part of the application as a document of compliance.