When can you change the object of taxation?

The change of object is carried out from the beginning of the tax period (calendar year).

It is prohibited to change the object during the year (clause 2 of Article 346.14 of the Tax Code of the Russian Federation). Read in the material “A new company cannot change an object under the simplified tax system in the middle of the year” that even a mistake made when choosing a taxable object will not allow you to change it outside of normal hours.

Example

Gedeon LLC has been applying the simplified tax system since 01/01/2020. The company's management thought about changing the object of taxation in March 2021. However, it is impossible to change the object of the simplified tax system during the year (clause 2 of article 346.14 of the Tax Code of the Russian Federation). It can only be changed from January 1 of the next year, that is, from 01/01/2021.

At the same time, according to the clarifications of the Ministry of Finance from letter No. 03-11-11/58878 dated October 14, 2015, the taxpayer has the right, before the end of the official deadline for submitting a notice of a change of object, to change his decision and re-submit the notification if he made a mistake with the object in the first one. The same should be done if the taxpayer made a mistake when filling out the “Object of taxation” column when submitting a notice of transition to the simplified tax system. He has the right to correct the error and change the object if he manages to submit a new notification before December 31 of the current year (letter of the Ministry of Finance dated January 16, 2015 No. 03-11-06/2/813).

Notification of the transition to the simplified tax system from 2021 for LLCs and individual entrepreneurs

Many companies and entrepreneurs want to switch to a simplified taxation system. This can be done after registration and during the operation of the company, individual entrepreneur. To switch to the simplified tax system, you need to submit an application for the switch on a special form. However, you need to fill it out correctly. For a sample application that the tax authorities will accept, see below.

For limits on the transition to the simplified tax system and conditions, see the article on the Simplified website. Limits on the simplified tax system for 2021: table for application and transition.

Below in the article there are also sample applications for individual entrepreneurs. We also devoted a separate article on the procedure for filling out a transfer application for a newly created individual entrepreneur on our website.

You can fill out the form online using the BukhSoft program. After which the program will check the application for errors and you can print it on a printer or save it as an Excel file.

Fill out notification online

Below, see detailed samples for all cases of transition to the simplified tax system: in the middle of the year and at the beginning.

It is uniform for use by entrepreneurs and companies. Any tax authority will register it if they want to change the tax regime.

Notification period for the Federal Tax Service when switching to a simplified system for newly registered companies and individual entrepreneurs

Newly registered companies and individual entrepreneurs can submit a notification of transition to the simplified tax system within 30 calendar days from the date of registration.

Example: An entry was made in the Unified State Register of Legal Entities about the creation of Buttercup LLC on June 15, 2020. This means that the notification of the application of the simplified taxation system must be submitted to the tax authority before July 15, 2020.

For new individual entrepreneurs, the notice period is the same - 30 days.

Notification period for the Federal Tax Service upon transition to the simplified tax system for companies and individual entrepreneurs working on the simplified tax system

For companies that want to switch to a simplified system, but are currently working on a different general system, the procedure is slightly different. Firstly, only from the beginning of next year you can work with the simplified tax system. That is, you can switch from the OSN to the simplified tax system from January 1, 2021.

Secondly, notification of the transition to the simplified tax system must be submitted to the tax authority before December 31, 2021. Accordingly, in order to switch to the simplified tax system from 2021, the application must be sent before December 31, 2019.

Thirdly, several criteria must be met.

Criteria for companies and individual entrepreneurs wishing to switch to a simplified system:

- Revenue for 9 months of 2021 amounted to less than 112.5 million rubles;

- The number of personnel is less than 100 people;

- The residual value of the fixed assets is less than 150 million rubles (this requirement applies only to companies);

- No branches, representative offices are allowed

- Other companies do not have a share of more than 25%.

Filling out the notice of transition to the simplified tax system from 2021

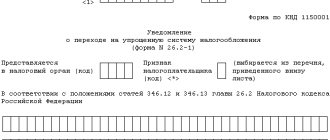

The form that must be submitted is called 26.2-1. When filling out, you must select the object of taxation (“income”, “income minus expenses”), the residual value of fixed assets, and revenue for 9 months.

Sample of filling out a notice of transition to the simplified tax system for an entrepreneur

You can familiarize yourself with an example of filling out an application for transition to the simplified tax system for an individual entrepreneur who wants to work with the object “income minus expenses” from 2021. At the moment, the entrepreneur is on the general taxation system.

Sample of filling out a notice of transition to the simplified tax system for newly created LLCs and individual entrepreneurs

Only registered companies and entrepreneurs do not fill out information on income and fixed assets. In the application they need to indicate only the selected object of taxation.

There are subtleties in filling out the “Taxpayer Identification” field. The value “1” is indicated by companies and entrepreneurs who submitted the application at the time of filing the registration application.

The value “2” is indicated if the notification is submitted later.

Deadlines for submitting information about changes in the object of taxation

Submission of information about a change in the object of taxation according to the simplified tax system is carried out before December 31 of the current year by notifying the tax authorities in form 26.2-6, approved by order of the Federal Tax Service of Russia dated November 2, 2012 No. ММВ-7-3 / [email protected]

Such notification to the head of the company or individual entrepreneur should be brought to the tax office in person, sent through a representative by proxy, or sent by mail in a valuable letter with a list of the attachments.

In addition, notification can be submitted electronically via telecommunication channels. The electronic data submission format was approved by order of the Federal Tax Service of Russia dated November 16, 2012 No. ММВ-7-6/ [email protected]

You can find a line-by-line algorithm for filling out a notification and a completed sample in ConsultantPlus. A free trial of full access to the legal system is available.

In the picture below, see the optimal procedure for changing the object of taxation.

To make the right decision, read the article “Which object is more profitable under the simplified tax system – “income” or “income minus expenses”?”

You will find tips on accounting for income and expenses after changing the object of taxation in ConsultantPlus. Sign up for a trial access to K+ for free and go to the Ready-made solution.

How to change the object of taxation of the simplified tax system

What to do if the idea arises of changing the object of taxation according to the simplified tax system? Depending on the reasons for such a change, the order of transition from one object to another also depends.

Already operating company (IP)

If a change in the object of taxation is dictated by the economic reasons of an existing business entity, the following nuances must be kept in mind:

For the form and sample of filling out notification 26.2-6 for this situation, see and download from the links below:

Newly created organization or individual entrepreneur

Let's assume a different situation. A new business entity has just registered and submitted a notice of transition to the simplified tax system from the moment of state registration. As we have already indicated, this can be done within 30 days from the date of registration.

The question arises: if the submitted notification incorrectly indicates the object of taxation (a technical error was made or the taxpayer immediately realized that he had made the wrong choice), when can it be changed? Is it only from the next calendar year?

In 2021, a letter from the Federal Tax Service of Russia dated September 11, 2020 No. SD-4-3/14754 was issued, explaining this point.

So, if a notification with an incorrect object of taxation of the simplified tax system is submitted before the expiration of 30 days from the date of registration of the business entity, then it is permissible to submit another notification about the transition to the simplified tax system with the already correct object of taxation. We pay attention here to the following nuances:

Do I need to obtain permission to change the object of taxation?

Changing the object of taxation is voluntary, just like the transition to the simplified tax system. Therefore, the tax authority does not have the right to refuse to change the object if all requirements for the execution and deadlines for submitting the notification are met.

Legal entities in some cases may need permission from the general meeting of participants or shareholders or the board of directors if the charter places the approval of local regulations within their competence. In this case, the sole executive body (director, general director, manager, etc.) does not have the right to make changes to the accounting policy of the enterprise, namely: a change in the object of taxation under the simplified tax system must be registered in it even before submitting a notification to the tax office.

IMPORTANT! The Ministry of Finance in letter dated 04/15/2016 No. 03-11-11/22058 explained that the taxpayer does not have the right to take into account the damage incurred with the “income” object to reduce the tax base after changing the object to “income minus expenses”.

Document role

Many people own several real estate properties - an apartment, a room, a country house, a cottage, a garage, etc. For each of them, they are obliged to pay annual property tax for individuals, even when the object is not in full, but in shared ownership. Thus, the amount required to pay the tax levy for all premises, buildings and structures may be quite large.

To solve this problem, legislators came up with a benefit: they allowed taxpayers to choose one of the properties that would be exempt from taxation. True, this relaxation is not available to all citizens, but to representatives of only certain groups.

A potential beneficiary can notify the tax service of his choice by filling out the appropriate notification.

Changing the object of taxation during reorganization

What happens to the object of taxation during reorganization depends on the form in which this reorganization is carried out. In Art. 57 of the Civil Code of the Russian Federation stands out:

- merger;

- accession;

- separation;

- selection;

- transformation.

In Art. 58 of the Civil Code of the Russian Federation, each of the above concepts is disclosed from the point of view of the transfer of rights and obligations. In the diagram below, see what type of reorganization will entail the need to re-apply for simplification, and in which cases nothing will change.

If, after reorganization, an enterprise has the right to remain on the simplified tax system, then the object of taxation remains the same.

If it is necessary to change the object of taxation, then this can be done as a general rule from January 1 of the next year by submitting to the tax office before December 31 of the current year a notice of change of object (clause 2 of Article 346.14 of the Tax Code of the Russian Federation).

Example

Kammelia LLC and Impulse LLC were reorganized on January 20, 2020 through a merger into Cammelia-Impulse LLC. Simultaneously with the registration of a new legal entity, the company submitted an application to the tax office to apply the simplified tax system to the object of income.

JSC "Cammelia-Impulse" On March 2, 2020, a decision was made to change the object of taxation. This procedure can be carried out only from 01/01/2021 by submitting an application before 12/31/2020.

Rules for changing a simplified tax system object

If you want to start applying the simplified tax system, abandon this system, or change the object of taxation, then please note: the timing of the implementation of each of these procedures is affected by the tax period established for the simplified tax system, which is equal to a year (clause 1 of article 346.19 of the Tax Code of the Russian Federation). This means that it is impossible to change the simplified tax system object during a given period of time.

That is why the Tax Code of the Russian Federation states that the opportunity to apply the simplified tax system for an already functioning taxpayer occurs only at the beginning of the next year (Clause 1 of Article 346.13), and there is also a direct ban on the transition before the end of the year:

- to a different tax system with simplified taxation (clause 3 of article 346.13);

- on another object of taxation with a simplified tax (clause 2 of Article 346.14).

However, the simplified tax system object can change annually. For the change to take effect, it is enough to notify the tax authority about it before the end of the year preceding the onset of the next tax period (clause 2 of Article 346.14 of the Tax Code of the Russian Federation).

If the notification is submitted on time, then from the coming year the procedure for determining the base for calculating the simplified tax will change. In this case, the value of the new object “income” can no longer be reduced by any current or previously incurred expenses.