What is an advance payment under the simplified tax system?

We have told you about the simplified special regime (USN or simplified tax regime) more than once. We have also already written about filling out declarations on the simplified tax system “Income” and about how to fill out a declaration on the simplified tax system “Income minus expenses”.

We also wrote separate articles about KUDIR for individual entrepreneurs on the simplified tax system “Income” and about KUDIR for individual entrepreneurs on the simplified tax system “Income minus expenses”.

Let us note several important points regarding simplification for today’s topic:

- According to the simplified tax system, the tax period is considered to be a year. The declaration must be drawn up and submitted based on the results of the year;

- The simplified reporting periods are quarter, six months and 9 months. At the end of these periods, you do not need to prepare and submit a declaration, but you do need to calculate the advance tax payment and pay it.

The advance payment represents the amount of tax calculated and subject to transfer to the budget based on the results of the reporting period.

That is, based on the results of the 1st quarter, we first calculate what tax we currently have and pay it. Then we make a calculation based on the results of 6 months, subtract from it the amount already paid based on the results of the 1st quarter, and pay the rest to the budget. The same calculations are made based on the results of 9 months. Then we calculate the tax at the end of the year and make the final calculation, which should be reflected in the declaration you submit.

The situation may change during the year, so as a result, when drawing up an annual declaration, you may end up with both an amount that needs to be paid additionally to the budget, and an amount to be deducted from the budget - this is when you transferred more advances during the year than you ended up with tax came out.

Tax accounting of advances received under a simplified taxation system

Clause 1, paragraph 1, which refers to income in the form of property, property rights, work or services received from other persons in advance of payment for goods. However, this rule is applicable only to taxpayers who determine income and expenses using the accrual method.

Thus, advances received by the seller-taxpayer of the simplified tax system, using the cash method of income recognition, should not reduce the tax base for the single tax, but are included in income when calculating it.

Let's look at an example. A trading organization using the simplified tax system received an advance in July from a buyer in the amount of 600 thousand rubles. In November, goods worth 490 thousand rubles were delivered to the buyer. The organization returns 110 thousand rubles to the buyer. In this case, in July the organization had to recognize an advance in income in the amount of 600 thousand rubles. Since the organization returned to the buyer part of the overpaid advance in November, it must adjust the income, which is made on the date of the transfer of funds to the buyer’s account. At the same time, adjustments are made in the book of income and expenses: in columns 4 “Income - total” and 5 “Including income taken into account when calculating the tax base”, reverse entries are made: “- 150,000 rubles.” In the Single Tax Declaration, in Section 2, in the “Income” column, line 010 “Amount of income received” indicates the amount of income minus the advance payment returned to the buyer.

Advances returned to the buyer (accounting with the buyer)

The above-mentioned Article 251 of the Tax Code does not contain income in the form of an advance payment returned to the buyer as not taken into account when calculating the single tax. That is, the taxpayer-buyer must take into account the advance payment returned to him by the buyer in his income.

However, there is some controversy on this issue. The Ministry of Finance in its letters expresses a slightly different point of view: if the amounts of advances and prepayments paid to sellers were not taken into account as expenses when determining the tax base for the single tax, then the returned amounts of advances and prepayments should not be taken into account as part of the taxpayer’s income; if advances and prepayments were taken into account as expenses, then the returned amounts should be taken into account in the income of the taxpayer under the simplified tax system.

At the same time, in other letters, the Ministry of Finance contradicts itself: having transferred the advance to the seller, the taxpayer has not yet received the goods, that is, has not incurred expenses associated with generating income. And the taxpayer of the simplified tax system accepts expenses for accounting only if they meet the criteria established in paragraph 2 of Article 252 of the Tax Code. The criteria are not met, and therefore advances paid to the seller cannot be taken into account in expenses, but are included in expenses only in the reporting period of the acquisition. But what kind of refund of the advance can we talk about if the goods are purchased - the obligation is terminated by fulfillment.

When an advance is received, it is assumed that he must subsequently fulfill some obligation, in our case, to sell the goods. As a result, he will receive income, which will form the object of taxation with a single tax. If the seller returns the advance to the buyer, then no object of taxation arises, since neither sale (income from sale) nor non-operating income arises. Consequently, there are no obligations associated with the calculation and payment of the single tax on these transactions.

According to Article 78 of the Tax Code, the amount of overpaid tax from the advance, returned to the taxpayer, in this case is subject to offset against upcoming tax payments or to be returned to the taxpayer.

(ADVANCE PAYMENTS) ISSUED (PAYED) TO SUPPLIERS?

For some types of costs, a special procedure for recognition as expenses is provided. In such cases, the question of when to take into account the advance payment for single tax purposes does not arise. Such costs include (clause 2 of Article 346.17 of the Tax Code of the Russian Federation):

— material costs, including costs for the purchase of raw materials and supplies (clause 1, clause 2, article 346.17 of the Tax Code of the Russian Federation);

— labor costs (clause 1, clause 2, article 346.17 of the Tax Code of the Russian Federation);

— expenses for paying the cost of goods purchased for further sale (clause 2, clause 2, article 346.17 of the Tax Code of the Russian Federation);

— expenses for paying taxes and fees (clause 3, clause 2, article 346.17 of the Tax Code of the Russian Federation);

— expenses for the acquisition (construction, production) of fixed assets, their completion, additional equipment, reconstruction, modernization and technical re-equipment (clause 4, clause 2, article 346.17 of the Tax Code of the Russian Federation);

— expenses for the acquisition (creation by the taxpayer himself) of intangible assets (clause 4, clause 2, article 346.17 of the Tax Code of the Russian Federation).

Note

Read more about the procedure for recognizing these types of expenses in the section in Section. 4.2.3 “In what order do the simplified tax system recognize expenses for paying taxes, acquiring fixed assets, paying labor, selling purchased goods, etc.”

In relation to other costs listed in paragraph 1 of Art. 346.16 of the Tax Code of the Russian Federation, the general procedure for recognizing expenses as established by paragraph. 1 item 2 art. 346.17 Tax Code of the Russian Federation. This could be, for example, expenses for accounting services, advertising, etc.

The question arises: if the relevant agreement provides for prepayment (advance payment), can it be taken into account in expenses at the time of payment?

The Tax Code of the Russian Federation does not contain a clear answer.

In practice, taxpayers usually reflect prepayment amounts paid to suppliers as expenses not at the time of payment, but on the date of termination of the counterparty’s counter-obligation (when a document is signed confirming the completion of work, provision of services, etc.). And if the delivery and acceptance of work (services) occurs in stages, the specified amounts are included in expenses as such work (services) are accepted.

For example, the Alpha organization rented non-residential premises from the Beta organization.

Advance payments according to the simplified tax system “Income”: calculation and formula

So, what data do we need to calculate the advance:

- The amount of income for the period on an accrual basis;

- Applicable tax rate;

- The amount of insurance premiums paid during the period;

- Amounts of advances already transferred earlier in the current year.

Then the formula for calculating the advance looks like this:

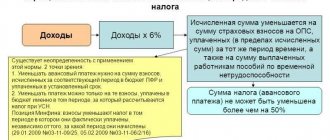

Advance payment = Income for the period * Rate – Insurance premiums – Advance payments of previous periods

We’ll show you how to calculate using an example: let’s say you’re an individual entrepreneur without employees, and at the end of the 1st quarter you received 100 thousand rubles. income. Your simplified tax rate is standard 6%. In the 1st quarter, you transferred part of your contributions to the funds, for example, 5 thousand rubles.

Advance (after 1st quarter) = 100 thousand rubles. * 6% - 5 thousand rubles. = 1 thousand rub.

Then in the 2nd quarter you received another 150 thousand rubles. income and paid the next 5 thousand rubles for themselves. contributions.

Advance (after 6 months) = (100 + 150 thousand rubles) * 6% - (5 + 5 thousand rubles) – 1 thousand rubles. = 4 thousand rub.

Further calculations are done in a similar way.

Important! On the simplified tax system (with income base):

- LLCs can deduct contributions for their employees from tax, but the tax can only be reduced by 50% of the calculated amount.

- Individual entrepreneurs who do not have employees have the right to deduct all contributions for themselves .

- Individual entrepreneurs can deduct from the tax both contributions for themselves and contributions for employees, but they are allowed to reduce the calculated tax amount by no more than 50% of the calculated tax amount.

Refund of advance received

Let’s assume that the organization, having decided not to argue with the tax authorities, included the received advance payment as part of its income, and then for some reason returns the advance payment to the buyer. How to reflect the returned amount in this case?

With “simplification”, the list of expenses that are taken into account when calculating the single tax is closed (clause 1 of Article 346.16 of the Tax Code of the Russian Federation), and it does not provide for such type of expense as a returned advance. And for those organizations that have chosen income as an object of taxation, expenses are not taken into account at all when calculating the single tax.

According to Article 346.17 of the Tax Code of the Russian Federation, expenses during “simplified taxation” are recognized as expenses if they:

- paid;

- are recognized as expenses in accordance with the rules of Article 252 of the Tax Code of the Russian Federation (according to clause 2 of Article 346.16 of the Tax Code of the Russian Federation).

In accordance with the operation of Article 252 of the Tax Code of the Russian Federation, expenses are recognized as justified and documented expenses incurred by the taxpayer. In this case, any expenses are recognized as expenses, provided that they are incurred to carry out activities aimed at generating income.

From the above provisions of tax legislation it follows that the return of the advance does not meet all the criteria for recognizing expenses. Therefore, we can conclude that it is impossible to reduce income by the amount of the returned advance.

Note that there might not have been a problem with the return of the advance in the “simplified” system (recognition of expenses). If the financial departments determined once and for all that the funds received for the upcoming sale (advance) are not taken into account in the organization’s income, then their return would not need to be reflected in the expenses taken into account when calculating the single tax.

But officials of financial departments tried to solve this problem in their own way, one might say, “one-sidedly”: they allowed the return of the advance to be taken into account in expenses, while proposing to “not touch” expenses, but to adjust income (Letter of the Ministry of Finance of Russia dated April 28, 2003 N 04- 02-05/3/39).

In the said Letter, the Ministry of Finance explains that if the return of an advance is associated with a change in the terms of the contract (its termination), then income should be reduced by the amount of the returned advance in the tax return and this operation should be reflected in the Book of Income and Expenses in the corresponding reporting (tax) period, in which changes occurred in the contract.

A similar opinion is expressed by the Department of Tax Administration for Moscow (Letter dated May 24, 2004 N 21-09/34822). Tax service specialists believe that changes resulting from an additional agreement to the contract (in accordance with Article 453 of the Civil Code of the Russian Federation) should be reflected in tax accounting as an adjustment to the tax base of the current reporting (tax) period in accordance with Article 81 of the Tax Code of the Russian Federation.

In the tax return for a single tax (approved by Order of the Ministry of Taxes of Russia dated November 21, 2003 N BG-3-22/647) by the amount of the advance to be returned in connection with changes in the terms of the agreement, it is necessary to reduce the income of the reporting (tax) period in which the parties have made such changes. In this case, according to the tax authorities, it is not necessary to recalculate the tax base for the single tax and prepare updated declarations for previous reporting (tax) periods.

In practice, there are situations when the return of the advance is not related to changes in the terms of the contract. For example : the client transferred 1 million rubles “for the sale” of services, and the services were provided in the amount of 900 thousand rubles. In this case, the “simplifier” is forced to admit an overpayment of 100 thousand rubles. received in advance. After a certain period of time, the client (without changing the terms of the contract) asks to return the overpaid amount of 100 thousand rubles, since he does not intend to use it in the near future.

In such a situation, the organization must adjust income for tax purposes (i.e., recalculate tax liabilities) in the same manner as described above.

When returning an advance in a “simplified” form, the organization also has a question: how should this operation be reflected in the Income and Expense Accounting Book?

It should be noted that the procedure for maintaining the Book of Income and Expenses (Order of the Ministry of Taxes and Taxes of Russia dated October 28, 2002 N BG-3-22/606) does not provide for the possibility of making reversal entries in column 4 “Income”.

At the same time, the Russian Ministry of Finance believes that in order to correct errors it is necessary to cross out the incorrect value of the indicator reflected in the Book of Accounting for Income and Expenses and enter the correct value. Correction of errors must be confirmed by the signature of the head of the organization (individual entrepreneur) indicating the date of correction.

Advance payments according to the simplified tax system “Income minus expenses”: calculation and formula

So, what is needed to calculate the advance payment according to the simplified tax system “Income minus expenses”:

- The amount of income for the period on an accrual basis;

- The amount of expenses for the period on an accrual basis;

- Applicable tax rate;

- Amounts of advances already transferred earlier in the current year.

Then the expression for calculating the advance is the following expression:

Advance payment = (Income for the period – Expenses for the period) * Rate – Advance payments of previous periods

Now let’s look at an example: you are an individual entrepreneur without employees, at the end of the 1st quarter you received income of 100 thousand rubles, expenses for this period amounted to 60 thousand rubles. Your simplified tax rate is standard 15%.

Advance (after 1st quarter) = (100 thousand rubles – 60 thousand rubles) * 15% = 6 thousand rubles.

Then in the 2nd quarter you received another 150 thousand rubles. income and incurred expenses of 70 thousand rubles.

Advance (after 6 months) = ((100 + 150 thousand rubles) – (60 + 70 thousand rubles)) * 15% - 6 thousand rubles. = 12 thousand rubles.

Further calculations are done in a similar way.

Important! In this formula, contributions to insurance funds for yourself and for employees are not taken into account, since they are already included in expenses - there is no need to count them separately, they have already taken part in reducing the tax base.

Is an advance considered income?

The procedure for determining income by organizations using the simplified tax system is provided for in Article 346.15 of the Tax Code of the Russian Federation. According to this article, when determining the object of taxation, organizations take into account income from the sale of goods (work, services), the sale of property and property rights, determined in accordance with Article 249 of the Tax Code of the Russian Federation, and non-operating income, determined in accordance with Article 250 of the Tax Code of the Russian Federation. When determining the object of taxation, the income listed in Article 251 of the Tax Code of the Russian Federation is not taken into account. Let's look at this in more detail.

In accordance with paragraph 1 of paragraph 1 of Article 251 of the Tax Code of the Russian Federation, advances are not taken into account among taxable income by organizations that recognize income on an accrual basis.

But does it follow from this formulation that for those who calculate taxable profit using the cash method or have switched to the “simplified” method, the advance is income?

We believe that such a conclusion cannot be drawn, since the fact that paragraph 1 of clause 1 of Article 251 of the Tax Code of the Russian Federation does not indicate taxpayers who recognize income on a cash basis does not mean that an advance by such taxpayers should automatically be recognized as income.

In this case, it is obvious that the conclusion made by the officials in the above letters clearly contradicts the definitions of income given in Article 249 of the Tax Code of the Russian Federation and the provisions of Article 273 of the Tax Code of the Russian Federation. Paragraph 2 of Article 249 of the Tax Code of the Russian Federation stipulates that receipts associated with payments for goods sold (work, services) or property rights are recognized depending on the chosen method. According to Article 346.17 of the Tax Code of the Russian Federation, income under “simplified taxation” is recognized on the cash basis, which is determined in accordance with Article 273 of the Tax Code of the Russian Federation.

Firstly, Article 249 of the Tax Code of the Russian Federation states that income is revenue from goods sold (work, services) or property rights. But the organization receives the advance even before the sale, so it is impossible to recognize the advance as income on the basis of this article.

Secondly, within the meaning of clause 2 of Article 273 of the Tax Code of the Russian Federation, income is recognized on the day when the debt to the organization is repaid by its debtor. Note that debt as such arises only if the goods were first shipped and then payment was received. But by transferring an advance payment (advance payment), the partner does not repay his debt for the goods shipped (work performed, services rendered), therefore the transferred amounts cannot be considered taxable income.

Thirdly, the advance also does not fit the definition of non-operating income, which is named in Article 250 of the Tax Code of the Russian Federation.

In our opinion, an advance is not income also on the grounds that income is recognized as an economic benefit in monetary or in-kind form that can be assessed (Article 41 of the Tax Code of the Russian Federation). And in this case it is obvious that the organization does not receive any economic benefit.

Therefore, the requirements and explanations of the Ministry of Taxes and the Ministry of Finance of Russia regarding the inclusion of the prepayment received by the “simplified” people in the tax base for the single tax, to put it mildly, contradict common sense.

But nevertheless, officials of ministries and departments continue to firmly stand their ground.

Moreover, the Ministry of Finance of Russia believes that the prepayment returned to the organization should increase the tax base for the single tax on the day these funds are received in the bank account or cash register of the organization, since this type of income is not named in Article 251 of the Tax Code of the Russian Federation (Letter dated 12.05.2004 N 04-02-05/2/21).

It should be noted that, despite the obvious contradictions between the tax legislation and the position of the main financial departments of the country, few people decide to argue with the tax authorities, perhaps also for the reason that the single tax on prepayment will still have to be paid, but only a little later, after implementation implementation.

That is, in this case, a dispute with the tax authorities may arise regarding the moment of payment of the single tax, and not the amount of tax.

We note the fact that arbitration practice on the issue of advances has not been formed to date.

Deadlines for making advance payments under the simplified tax system in 2021

Advance payments under the simplified tax system must be transferred to the budget by the 25th day of the month following the completed period - that is, by April 25 / July / October.

You must pay them within a year! This is provided for by tax law, and if you violate it, you will be subject to late payment penalties.

To always pay advance payments under the simplified tax system and other taxes on time, use a special service that will simplify accounting.

Even if you already understand that the tax on your annual operating results will be lower than the amount of advances, you still need to pay them during the year. It’s just that at the end of the year you have an overpayment of taxes - you can offset it against payments from the next year or return it.