For whom is the transition to Unified Agricultural Tax available?

Tax law provides for the application of a special regime for commercial structures that meet the following parameters:

- legal entities or individual entrepreneurs engaged in the reproduction and sale of products classified as agricultural;

- the share of sales of agricultural products in gross revenue is at least 70% (for all types of products).

Based on their functionality and the organizational and legal form of a business entity, payers of the Unified Agricultural Tax include:

- LLCs and individual entrepreneurs with OKVED codes of agricultural producers;

- agricultural consumer cooperatives (processing, marketing, livestock, horticultural);

- artels engaged in fishing and processing of fish and other aquatic biological resources.

Important: to be classified as an agricultural producer, the complex presence of three factors is necessary - the products must be produced, processed and sold by an applicant for the use of unified agricultural tax. The absence of one component provides grounds for refusing the taxpayer to switch to the agricultural tax.

Fishing farms in Russian single-industry towns and settlements, where this type of activity is a city-forming activity, must meet additional criteria to use the preferential regime:

- the number of employees of fishing enterprises (including family members living with them) must be at least half of the total number of residents of the city/village;

- the number of employees involved in fishing activities is limited - no more than 300 people per year;

- fishing must be carried out using own or leased (chartered) fishing vessels.

Please note: for fishing enterprises (IEs), the requirement to use the Unified Agricultural Tax remains with the volume of sales of agricultural products (fish catch) amounting to 70% of gross income.

Who can become a payer of the Unified Agricultural Tax

As I already said, both a legal entity and an individual entrepreneur can switch to the Unified Agricultural Tax. But for this you need to meet certain criteria. Which one exactly?

Only an agricultural producer can be a taxpayer under this special regime. Who is it?

According to the Tax Code of the Russian Federation, agricultural producers are recognized:

- legal entities and individual entrepreneurs engaged in the production of agricultural products, their processing (this means both primary and subsequent (that is, industrial) processing) and the sale of these products. It is important here that income from this activity is equal to at least 70% of the taxpayer’s total income.

- agricultural consumer cooperatives (gardening, market gardening, livestock farming, as well as those processing agricultural products, selling them or working in the field of agricultural supply). At the same time, the criterion for the share of income of 70% also remains here!

- fisheries, fishery organizations and individual entrepreneurs, if: the average number of employees for the tax period is no more than 300 people;

- if the share of “core” income (sales of catch and market products) is at least the same 70% of total income;

- if they are engaged in fishing on vessels that are owned by them or used under a charter agreement.

What is considered agricultural products? This concept includes:

- crop products (not only agriculture, but also forestry);

- livestock products (including growing / growing fish and other biological water resources);

- catch of aquatic biological resources, fish and other products from them.

Summarize. To apply the Unified Agricultural Tax, you must meet the following criteria:

- Engage in production/processing/sale of agricultural products.

- The share of income from this activity must be equal to at least 70% of all income.

- For fisheries, there are additional restrictions in the form of the number of employees (up to 300 people) and the availability of their own and rented vessels.

Unified agricultural tax does not have the right to apply:

- Those who produce excisable goods;

- Those who work in the gambling business;

- State and budgetary institutions.

Prohibition on the use of the single agricultural tax

In some cases, tax legislation does not allow the application of preferential treatment even if the above conditions are met. Agricultural producers who, in addition to their main activities, perform the following work are not allowed to use the Unified Agricultural Tax:

- produce goods subject to excise duties (tobacco products, alcohol);

- are engaged in gambling business.

In addition, it is prohibited to switch to paying unified agricultural taxes to agricultural organizations that are part of the budget structure.

What to do after registering a peasant (farm) enterprise

After registering a peasant farm, if you forgot to submit a notification for the special regime, you can submit it within 30 days.

Notifications from the funds (FSS, Pension Fund) should come on their own, but if they don’t send them, you will need to receive them.

Renting or purchasing a plot of land for the needs of a peasant farm can be carried out both before and after registration.

Also find out about government support, benefits, tax holidays in your region for farms.

Peasant farms have a number of significant differences from other business entities, not only because of their special structure and other legal requirements, but also due to the possibility of using a special form of taxation. The Unified Agricultural Tax is easier to submit reports and make regular payments on profits received.

As you know, the transition to the Unified Agricultural Tax does not occur automatically - to do this, when creating a peasant farm itself, you need to submit a special application to the tax authority and receive confirmation from this body.

Procedure for transition to Unified Agricultural Tax

If an organization or individual entrepreneur meets all the criteria corresponding to the status of an agricultural producer, then the taxpayer has the right to declare to the fiscal authorities his intention to use a preferential special regime.

Please note: the transition to the Unified Agricultural Tax is not mandatory and is carried out by taxpayers on a voluntary basis.

When to declare the use of Unified Agricultural Tax

The unified agricultural tax is calculated based on the results of the tax period – the calendar year. For this reason, you can declare the transition to the Unified Agricultural Tax when using other taxation methods before the start of the new reporting period .

The deadlines for filing an application with the tax authority are:

- for existing LLCs/IPs – December 31;

- for new business entities – within 30 days from the date of registration.

Remember: violation of the deadlines for notification of the transition to the Unified Agricultural Tax is grounds for non-recognition of the taxpayer as a subject of the special regime and the accrual of all taxes according to the previous taxation scheme.

Specifics of applied taxation and reporting systems for peasant farms

The activities of a farm and its taxation are regulated in Russia by the Tax Code, as well as Federal Law No. 74 “On Peasant Farming” dated June 11, 2003, as amended in 2021. When submitting documents for registration of a farm, the head of the peasant farm can immediately declare the taxation regime (see →). The peasant farm (as an entrepreneur) has the right to work according to one of the systems to choose from:

- OSNO;

- Unified Agricultural Sciences.

In this case, from the moment of registration the selected taxation regime will come into force. By default, peasant farms switch to OSNO. If a month has passed after registration, if the peasant farm does not declare a transition to the unified agricultural tax or simplified tax system, the farm will be able to switch to one of these regimes only from next year. He will need to submit the application to the tax authorities by December 31.

It should be taken into account that, according to the law, peasant farms calculate, in addition to taxes, insurance contributions (to the Pension Fund of the Russian Federation, Social Insurance Fund, Federal Compulsory Medical Insurance Fund) regardless of the special regime applied. Since the participants of peasant farms are not only members of the farm, but also hired workers, the head of the farm (IP) transfers fixed insurance payments for himself and the members of the farm and at the same time pays for compulsory insurance for all employees. The procedure for payment of contributions for heads of farms is determined by Federal Law 212 of July 24, 2009, Article 14

If hired workers work in a peasant farm, under any special regime it is necessary to submit the following reports.

| Reporting forms | Due dates | Who to submit reports to? |

| 2-NDFL (on employee income); 6-NDFL (information about deductions made by the tax agent for all employees); KND 1110018 (information on the average number of employees) | Annually until 01.04; quarterly (in the current year: until May 4, August 1, October 31, annually - together with form 2-NDFL until 04/01/2017); annually: for farms created during the year - until the 20th day of the month following the one in which they were created, newly registered payers do not submit this information in the year of opening | Tax Service |

| Personalized accounting and form RSV-1; SEV-M (data on insured workers) | Quarterly (submitted on paper if there are up to 25 employees, in 2021: until May 16, August 15, November 15, for a year - until 02/15/2017); monthly (until the 10th) | Pension Fund |

| Information confirming the main activity; | Annually (until April 15); quarterly: on paper if the number of employees is up to 25, submitted before the 20th day of the month following the reporting period, in other cases, the electronic version is submitted until the 25th after the reporting period | FSS |

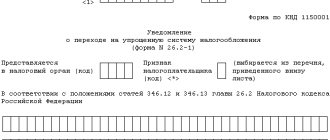

How to draw up a notice of application of the Unified Agricultural Tax

FILES

An application-notification on the use of the unified agricultural tax is drawn up by the taxpayer using Form No. 26.1-1 independently.

A separate block is provided for the tax authority’s marks, in which the inspector indicates the date of receipt of the document and the registration number.

At the head of the notification, the applicant indicates the required information:

- name of the subject;

- INN and KPP of the taxpayer notifying about the transition to the Unified Agricultural Tax;

- number (code) of the tax office at the location/registration of the applicant;

- taxpayer sign.

Drawing up a notification does not cause problems for the applicant, but attention should be paid to the following nuances:

- the applicant's attribute is selected depending on the time of submission of the notification;

- if the notification is submitted to the regulatory authority along with the main package of documents for registration, then the number “1” should be indicated;

- when submitting an application within a month (30 days) after registration - number “2”;

- when switching from another tax regime – number “3”.

Newly created individual entrepreneurs and organizations indicating “1” or “2” as the applicant’s attribute sign the notification, certify it with a seal and submit it to the tax office.

For payers who previously applied a different taxation scheme and plan to switch to the Unified Agricultural Tax from January 1 of the next calendar year, it is necessary to provide information on the share of gross revenue related to the sale of agricultural products. The same field indicates the period for which the calculated share is at least 70%.

Notification of the application of the unified agricultural tax can be submitted directly to the fiscal authority (by the head of the organization, entrepreneur or authorized representative), sent by mail or via telecommunication channels.

Keep in mind: if application No. 26.1-1 is submitted by an authorized person, then a power of attorney certified by a notary office is required.

General rules and features of taxation of peasant farm activities

Unified agricultural tax = fixed interest rate * (amount of profit - amount of expenses).

Tax payments are paid at the end of the half-year and for the year. In addition, simplified accounting is used in accounting using the “cash” method. The head of the peasant farm maintains an accounting book of expenses and profits, which is not certified by the tax authorities. Rented annually:

- declaration to the Unified Agricultural Tax at the place of registration by March 31 of the following reporting year;

- Form RSV-2 (for the Pension Fund of Russia) must be submitted by March 1.

The Unified Agricultural Tax has enough advantages. A single special regime allows, for example, to write off fixed assets when they are put into operation and to include advance payments in profit. But at the same time, the head of the household will not be able to take advantage of the deferment on payments and will be required to pay land tax. Read in more detail about the use of unified agricultural tax in the article: → application of unified agricultural tax for peasant farms, payment procedure, calculation formula.

To switch to a single special regime, you must submit a corresponding application within the established time frame. Applicants can only be those from farms that are engaged in the production, sale, and processing of exclusively agricultural products with a share of this type of income of at least 70% of the total profit. Moreover, the production and sale of agricultural products in this case act as a mandatory requirement. For example, if a farm is engaged only in processing products without production, then it may be denied the transition to the Unified Agricultural Tax.

A peasant farm consisting of 3 people is engaged in the cultivation, processing and sale of vegetables and fruits. The profit of the farm is 800 thousand rubles, costs are 600 thousand rubles. Based on these data, the tax base is first calculated (based on the difference between profits and expenses): 800,000—600,000 = 200,000 rubles.

After this, the unified agricultural tax for payment to the budget is calculated. The current rate of 6% is used for calculations. The result is the following: 200,000 * 6% = 12 thousand rubles. This is the amount of single tax that will need to be paid.

| Main components of counting | Estimated data and costing |

| Data for calculation | Tax rate for Unified Agricultural Tax (6%); expenses (600 thousand rubles), profit (800 thousand rubles) |

| Tax base | Calculated using the formula: amount of profit – amount of expenses; 800000—600000=200 thousand rubles. |

| Unified agricultural tax payable | Calculation using the formula: tax base * fixed rate (6%); 200000 * 6%=12 thousand rubles. |

In order to use the unified agricultural tax, you must draw up an application in the established form and submit it to the tax office within the time limits specified by law.

The head of the peasant farm pays a single fee at the approved rate - 6.0%.

Since January 1, 2021, an innovation has appeared in the legislation, according to which individual entrepreneurs and organizations become VAT payers, in accordance with the current general procedure (clause 12 of article 9 of the Federal Law of November 27, 2017 No. 335-FZ).

The same law provides for a number of conditions that allow individual entrepreneurs and organizations working on the Unified Agricultural Tax to obtain the right to VAT exemption.

Conditions for obtaining the right not to be a value added tax payer:

If two actions were completed within one calendar year:

– transition to a special unified agricultural tax regime;

– exemption from obligations to pay VAT.

If in 2021 the peasant farm received less than 100.0 million rubles in income from its activities at the Unified Agricultural Tax

Important! For subsequent years, a limiting amount is also prescribed, which is reduced by 10 million rubles

in each subsequent annual period, so in 2021. it will amount to 70 million rubles in 2021. – 80 million rubles, for 2021 – 90 million rubles).

One-click call

The Unified Agricultural Tax has enough advantages. A single special regime allows, for example, to write off fixed assets when they are put into operation and to include advance payments in profit. But at the same time, the head of the household will not be able to take advantage of the deferment on payments and will be required to pay land tax. Read in more detail about the use of unified agricultural tax in the article: → application of unified agricultural tax for peasant farms, payment procedure, calculation formula.

Start of work on Unified Agricultural Tax

Individual entrepreneurs and firms operating under a general or simplified taxation system switch to the Unified Agricultural Tax starting on January 1 of the year following the year in which the notification was submitted. Those who received the status of an individual entrepreneur or a legal entity and immediately declared their intention to apply the Unified Agricultural Tax, use this regime from the beginning of production activities.

When the right to use the unified agricultural tax is lost

Loss of the status of an agricultural producer and, accordingly, the right to apply a preferential agricultural special regime is possible in the following cases:

- reducing the mandatory 70% barrier to the share of sold agricultural products in gross income;

- violation of requirements for agricultural producers entitled to apply a special regime;

- termination of activities that give the right to apply the Unified Agricultural Tax;

- transition to another form of taxation.

Since the tax period for agricultural tax is a calendar year, all decisions regarding the loss of the right to use the Unified Agricultural Tax are made after December 31. If you refuse to further apply the special regime (regardless of the circumstances), the business entity is obliged to notify the fiscal service about this as follows:

- in case of violation of the criteria of the Unified Agricultural Tax payer - by submitting an application for loss of the right to a special tax in form No. 26.1-2;

- if you wish to use a general or simplified taxation system - according to form No. 26.1-3;

- when interrupting activities related to agriculture - according to form No. 26.1-7.

Information on the given forms must be submitted to the tax authority for a limited period - from January 1 to January 15 of the new calendar year.

Accounting and tax accounting of the Unified Agricultural Tax

Taxation of peasant farms under the Unified Agricultural Tax is often not associated with great difficulties. Peasant farms operating as a legal entity must organize the legal maintenance of accounting and tax records.

Peasant farms operating as individual entrepreneurs must keep a book of income received and expenses incurred.

The expenses of companies using special regimes (with the exception of those working on UTII) are strictly limited by tax law, due to the fact that they allow organizations to reduce the tax base when calculating this budget payment. As a result, each type of expense of an organization or entrepreneur on the Unified Agricultural Tax must be included in the list of expenses specified in Art. 346 of the Tax Code of the Russian Federation and be documented and economically justified.

Similar articles

- Tax base of the Unified Agricultural Tax

- Transition to Unified Agricultural Tax

- Accrued Unified Agricultural Tax transaction

- What are the advantages of the Unified Agricultural Tax?

- The reporting period according to the Unified Agricultural Tax is recognized

Recalculation of taxes upon loss of the right to a special regime

After the end of the reporting year, a taxpayer who has violated the requirements for agricultural producers is obliged to recalculate tax payments.

Instead of the unified agricultural tax paid during the year, an organization or individual entrepreneur will have to calculate and pay the main types of taxes to the budget:

- property tax (if there are fixed assets);

- VAT;

- income tax (NDFL);

- income tax.

All additional tax returns must be filed by January 31, and all budget obligations must be paid during this period.

Simultaneously with the formation and submission of declarations to the Federal Tax Service under the general taxation system, the former agricultural producer is obliged to draw up an updated calculation for the Unified Agricultural Tax (advance payments) for the 1st half of the year. The amounts paid will be considered an overpayment of agricultural tax.

You can return to the use of the Unified Agricultural Tax after one year has passed after the loss of the right to use it (or voluntary refusal).

Application for Unified Agricultural Tax when creating a peasant farm

Unified Agricultural Tax (USAT), Special tax regime for You need to pay it as when registering an individual entrepreneur - in the amount of rubles for personal To create and send an application electronically, you need. Official Internet portal of public services, city.

The general taxation system provides for the following taxes and duties to be paid by an individual entrepreneur: As can be seen from the above, most taxes and fees are associated with doing business in certain areas. Therefore, many peasant farms pay only some of the listed types of taxes: personal income tax and value added tax.

What to pay If the participants of the farm have decided to register an organization, then it becomes possible to use one of the following systems: General Taxpayer When you are on the OSSN, you must pay property, land and transport taxes, if necessary, value added tax, personal income tax as a tax agent. The mentioned benefit can be found in paragraph. Explanations are also available for personal income tax payments. For five years from the moment of registration of the farm, its members, including the head, are released from these obligations.

This benefit will remain in the event that during this time he switches to the taxation regime in the form of paying the unified agricultural tax, and then returns to the general regime of Lagutin L.

Unified agricultural tax can be used by organizations and individual entrepreneurs that are recognized as agricultural producers in accordance with Chapter. We talked in more detail about what the unified agricultural tax is and how it is calculated in a separate consultation. What is meant by peasant farm? Peasant farms are an association of citizens related by kinship or affinity, have property in common ownership and jointly carry out production and other economic activities - production, processing, storage, transportation and sale of agricultural products, based on their personal participation. Peasant farms can even consist of one person p. If a peasant farm is created by citizens, they enter into an appropriate agreement among themselves p. The peasant farm operates without forming a legal entity.

Unified agricultural tax Last updated: Only organizations and individual entrepreneurs that are agricultural producers can be transferred to pay the unified agricultural tax Unified Agricultural Tax. Agricultural producers Agricultural producers are organizations that meet the criteria given in the article

VIDEO ON THE TOPIC: Simplified taxation, imputation and patent, how to choose a tax system