List of violations

To fill out and submit 6-NDFL without error, we strongly recommend that you refer to the letter of the Russian Tax Service dated November 1, 2021 No. GD-4-11/22216. It contains a list of 26 violations that are common to tax agents. When an accountant finds an error in 6-NDFL, this is not an uncommon situation. But it can be avoided if you are aware of the experience of colleagues who also make mistakes when filling out 6-NDFL and submitting it.

At the end of 2021, the Federal Tax Service of Russia identified the following errors in form 6-NDFL:

| № | NKRF norm that has been violated | The essence of the violation | Reason for violation | How to fill out 6-personal income tax without errors, and also submit |

| 1 | Art. 226 Article 226.1 Art. 230 | The amount of accrued income on line 020 of section 1 is less than the sum of the lines “Total amount of income” of 2-NDFL certificates | Failure to comply with control ratios | The amount of accrued income (line 020) at the corresponding rate (line 010) must correspond to the sum of lines “Total amount of income” at the corresponding tax rate of 2-NDFL certificates with attribute 1, submitted for all payers by this tax agent, and lines 020 at the corresponding tax rate (page 010) of appendices No. 2 to the DNP, submitted for all payers by this tax agent (the ratio is applied to the calculation for the year) (letter of the Federal Tax Service dated March 10, 2016 No. BS-4-11/3852, clause 3.1). |

| 2 | Art. 226 Art. 226.1 Art. 230 | Line 025 of section 1 at the corresponding rate (line 010) does not correspond to the amount of income in the form of dividends (according to income code 1010) of 2-NDFL certificates with attribute “1” presented for all payers | Failure to comply with control ratios | The amount of accrued dividends (p. 025) must correspond to income in the form of dividends (according to income code 1010) of 2-NDFL certificates with attribute “1” submitted for all payers by this tax agent, and income in the form of dividends (according to income code 1010) of the applications No. 2 to the DNP submitted for all payers by this tax agent (the ratio is applied to the calculation for the year) (letter of the Federal Tax Service dated March 10, 2016 No. BS-4-11/3852, clause 3.2). |

| 3 | Art. 226 Art. 226.1 Art. 230 | The calculated tax on line 040 of section 1 is less than the sum of the lines “Calculated tax amount” of 2-NDFL certificates for the previous year | Failure to comply with control ratios | The amount of calculated tax (line 040) at the corresponding tax rate (line 010) must correspond to the sum of the lines “Tax amount calculated” at the corresponding tax rate of 2-NDFL certificates with attribute “1” submitted for all payers by this tax agent, and lines 030 at the corresponding tax rate (line 010) of appendices No. 2 to the DNP, submitted for all payers by this tax agent (the ratio is applied to the calculation for the year) (letter of the Federal Tax Service dated March 10, 2016 No. BS-4-11/3852, clause 3.3 ). |

| 4 | clause 3 art. 24 Article 225 Art. 226 | According to line 050 of section 1, the amount of fixed advance payments is greater than the calculated tax | Failure to comply with control ratios | The amount of fixed advance payments should not exceed the amount of calculated tax for the payer. (letter of the Federal Tax Service dated March 10, 2016 No. BS-4-11/3852, clause 1.4) |

| 5 | Art. 226 Art. 226.1 Art. 230 | Overestimation or understatement of the number of individuals (p. 060) who received income Similar errors in the 6-NDFL declaration regarding discrepancies with the number of 2-NDFL certificates. | Failure to comply with control ratios | The value of line 060 must correspond to the total number of 2-NDFL certificates with attribute “1” and appendices No. 2 to the DNP, submitted for all payers by this tax agent (the ratio is applied to the calculation for the year) (letter of the Federal Tax Service dated March 10, 2016 No. BS-4- 11/3852) |

| 6 | clause 2 art. 230 | Section 1 is filled in with a non-cumulative total | Failure to follow the procedure for filling out the calculation | Section 1 is filled out with an accrual total for the first quarter, six months, 9 months and a year (clause 3.1 of section III of the Procedure for filling out and submitting calculations in form 6-NDFL, approved by order of the Federal Tax Service dated October 14, 2015 No. ММВ-7-11/450 (hereinafter - Order). |

| 7 | clause 2 art. 230 art. 217 | Line 020 indicates income that is completely exempt from personal income tax. | Failure to comply with the clarifications of the Federal Tax Service of Russia | There is no need to show non-taxable income (letter of the Federal Tax Service dated 08/01/2016 No. BS-4-11/13984, question No. 4) |

| 8 | Art. 223 | There are frequent errors in 6-NDFL on line 070 of section 1. This is when a tax is shown that will be withheld only in the next reporting period (for example, wages for March paid in April) | Failure to comply with the clarifications of the Federal Tax Service of Russia | Line 070 of Section 1 indicates the total amount of tax withheld on an accrual basis from the beginning of the tax period. Since tax withholding from wages accrued for May, but paid in April, must be made by the tax agent in April directly upon payment, line 070 for the first quarter of 2017 is not filled in (letter of the Federal Tax Service dated 01.08.2016 No. BS-4-11/ 13984, question No. 6). |

| 9 | subp. 1 clause 1 art. 223 | Income in the form of temporary disability benefits is reflected in the period for which the benefit was accrued | Failure to comply with the clarifications of the Federal Tax Service of Russia | The date of actual receipt of temporary disability benefits is the day the income is paid, including transfers to the payer’s bank accounts or, on his behalf, to the accounts of third parties. Such income is reflected in the period in which it was paid (letter of the Federal Tax Service dated August 1, 2016 No. BS-4-11/13984, question No. 11). |

| 10 | clause 5 art. 226 and paragraph 14 of Art. 226.1 | Line 080 of Section 1 indicates the tax on wages that will be paid in the next reporting period (submission period). These are typical errors in 6-NDFL for 2021 - that is, when the deadline for fulfilling the obligation to withhold and transfer personal income tax has not arrived. | Failure to comply with the clarifications of the Federal Tax Service of Russia | Line 080 reflects the total amount of tax not withheld by the tax agent from income received by individuals in kind and in the form of material benefits in the absence of payment of other income in cash. If the amount of tax withheld in the next reporting period (submission period) is reflected on line 080, an updated calculation for the corresponding period must be submitted (letter of the Federal Tax Service dated August 1, 2016 No. BS-4-11/13984, question No. 5). |

| 11 | clause 5 art. 226 | Incorrect completion of line 080 of section 1 in the form of the difference between calculated and withheld tax | Failure to comply with the clarifications of the Federal Tax Service of Russia. Violation of the procedure for filling out the calculation. | Line 080 of Section 1 reflects the total amount of tax not withheld from received natural income and from material benefits, in the absence of payment of other income in cash (letter of the Federal Tax Service dated 01.08.2016 No. BS-4-11/13984, issue No. 5) . |

| 12 | Art. 126 clause 2 art. 230 | Filling out section 2 with a cumulative total | Error when filling out reports. Failure to comply with the clarifications of the Federal Tax Service of Russia. | Section 2 reflects those transactions that took place over the last 3 months of this period (letters from the Federal Tax Service dated 02/25/2016 No. BS-4-11/3058 and dated 02/21/2017 No. BS-4-11/14329, issue No. 3) . |

| 13 | clause 6 art. 226 | Lines 100, 110, 120 of section 2 indicate periods outside the reporting period | Error when filling out reports. Failure to comply with the clarifications of the Federal Tax Service of Russia. | Section 2 reflects those transactions that took place over the last 3 months of this period. If a tax agent performs an operation in one reporting period and completes it in another, it is reflected in the completion period. In this case, the operation is considered completed in the reporting period in which the deadline for tax transfer occurs in accordance with clause 6 of Art. 226 and paragraph 9 of Art. 226.1 of the Tax Code of the Russian Federation (letters of the Federal Tax Service dated 02/25/2016 No. BS-4-11/3058 and dated 02/21/2017 No. BS-4-11/14329, issue No. 3). |

| 14 | clause 6 art. 226 | When the timing of personal income tax transfer is incorrectly reflected (for example, the date of actual tax transfer is indicated) - this is an error in line 120 of 6-NDFL | Failure to comply with the clarifications of the Federal Tax Service of Russia. | It is necessary to take into account the provisions of paragraph 6 of Article 226 and paragraph 9 of Article 226.1 of the Tax Code of the Russian Federation (letter of the Federal Tax Service dated February 25, 2016 No. BS-4-11/3058) |

| 15 | clause 2 art. 223 | When the date of money transfer is indicated on line 100 when paying wages, this is an error in the date in 6-NDFL | Error when filling out reports. Failure to comply with the clarifications of the Federal Tax Service of Russia. | The date of actual receipt of wages is the last day of the month for which income was accrued for the performance of labor duties in accordance with the employment agreement (contract) (letter of the Federal Tax Service dated February 25, 2016 No. BS-4-11/3058) |

| 16 | clause 2 art. 223 | On line 100 of section 2, when paying a bonus based on the results of work for the year, the last day of the month is indicated on which the bonus order is dated | Error when filling out reports. Failure to comply with the clarifications of the Federal Tax Service of Russia. | The date of actual receipt of the bonus based on the results of work for the year is the day of payment of income, including its transfer of income to the payer’s accounts or, on his behalf, to the accounts of third parties (subclause 1, clause 1, article 223 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of Russia dated 06.10 .2017 No. ГД-4-11/20217). |

| 17 | Art. 231 | According to line 140 of section 2, the withheld tax is indicated taking into account the amount of personal income tax returned by the tax agent | Failure to comply with the procedure for filling out the calculation | In line 140 indicate the generalized amount of tax withheld on the date indicated in line 110. That is, exactly the one that was withheld (clauses 4.1, 4.2 of the Procedure). |

| 18 | clause 2 art. 230 | Duplication in section 2 of operations started in one reporting period and completed in another | Failure to comply with the clarifications of the Federal Tax Service of Russia | Section 2 reflects those transactions that took place over the last 3 months of this period. If a tax agent carries out an operation in one reporting period and completes it in another, it is reflected in the completion period (letters of the Federal Tax Service dated 02.25.2016 No. BS-4-11/3058 and dated 02.21.2017 No. BS-4-11/, question . No. 3). |

| 19 | subp. 2 clause 6 art. 226 | Interpayments (salaries, vacation pay, sick leave, etc.) are not included in a separate group. | Failure to comply with the clarifications of the Federal Tax Service of Russia. Violation of the procedure for filling out the calculation. | The block of lines 100 – 140 of Section 2 is filled out for each tax transfer deadline separately, if for different types of income with the same date of their actual receipt, there are different tax transfer deadlines (clause 4.2 of the FN order dated October 14, 2015 No. ММВ-7-11/ 450). |

| 20 | clause 2 art. 230 | When changing the location of an organization (separate division), the report is submitted to the Federal Tax Service at the previous place of registration | Failure to comply with the clarifications of the Federal Tax Service of Russia | After registration with the Federal Tax Service at the new location of the organization (separate unit), the following is submitted here:

In this case, the checkpoint is indicated as assigned to the new location (letter of the Federal Tax Service dated December 27, 2016 No. BS-4-11/25114). |

| 21 | clause 2 art. 230 | Submission of a report on paper if the number of employees is 25 or more people | Failure to comply with the provisions of the Tax Code of the Russian Federation | If the number of people who received income in the tax period is 25 or more, submit it electronically using the TKS |

| 22 | clause 2 art. 230 | Submission of reports for separate units on paper with an average number of 25 people (with a number of separate units of up to 25 individuals). | Failure to comply with the provisions of the Tax Code of the Russian Federation | If the number of people who received income in the tax period is 25 or more, submit it electronically using the TKS |

| 23 | clause 2 art. 230 | Organizations with several divisions and operating within one municipality submit one report | Failure to follow the procedure for filling out the calculation | The report is filled out separately for each separate division registered. Even if it is one municipal territory. In the line “Checkpoint” indicate the checkpoint at the place of registration of the organization at the location of its separate location (clause 2.2 of Section II of the Procedure). |

| 24 | clause 2 art. 230 | Inaccurate data regarding calculated personal income tax amounts (over/underestimated) | Error when filling out reports | Submit the updated calculation (question No. 7 from the letter of the Federal Tax Service dated July 21, 2017 No. BS-4-11/14329) |

| 25 | clause 7 art. 226 | When filling out OKTMO, there is an error in 6-NDFL (the same applies to the checkpoint). Discrepancies between OKTMO codes in calculations and personal income tax payments, leading to unreasonable overpayments and arrears. | Failure to follow the procedure for filling out the calculation | If an error is detected regarding the indication of the checkpoint or OKTMO, 2 calculations are submitted: 1. Clarified to the previously presented one, indicating the corresponding checkpoints or OKTMO and zero indicators for all sections. 2. Primary indicating the correct checkpoint or OKTMO. (letter of the Federal Tax Service dated August 12, 2016 No. GD-4-11/14772) |

| 26 | clause 2 art. 230 | Violation of the deadline for submitting 6-NDFL | Failure to comply with the norms of the Tax Code of the Russian Federation | Payments for the first quarter, half a year, 9 months are submitted no later than the last day of the month following the corresponding period. And for the year - no later than April 1 of the following year |

If there is an error in 6-NDFL: what to do

Of course, there are mistakes in 6-NDFL, for which you will be fined immediately. First of all, this is information that does not correspond to reality. Moreover, this is not necessarily an error in section 1 of 6-NDFL.

There is also a fine for violating the deadline for submitting 6-NDFL and for submitting it in the wrong form (on paper/electronically).

For more information about this, see “Fines for 6-NDFL in 2021.”

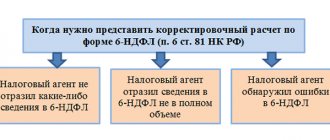

Provide an updated calculation if an error is found in 6-NDFL. When the tax authorities were the first to do this, explanations to the tax office will help. Errors in 6-NDFL must be explained and hushed up before the inspectors.

Advice

There is a universal way to check 6-NDFL for errors. So, if an error is made in 6-NDFL, check with the order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/450. He approved the control ratios of the indicators of this report.

Read also

15.05.2018

Explanations to 6-NDFL

It is worth noting that the document presented by the government agency sets out as clearly as possible the inaccuracies made and the correct option for their further correction.

What exactly is written:

- Link to the article of Tax legislation under which a violation occurred when filling out the established form 6-NDFL;

- Detailed information about the inaccuracy;

- For what reasons there was an error in filling;

- The last point is a detailed description of the correct format for submitting reports in Form 6-NDFL.

What kind of reporting should entrepreneurs submit to the Pension Fund? Find out here.

It is worth noting that the most common mistake that occurs when submitting reports is the incorrect use of the provided explanations of the civil service.