From your employees' salaries, you withhold personal income tax or personal income tax - 13%, transfer it to the state, and give the remaining money to the employee. This is how it happens in life.

You hired an employee and agreed that you would give him 20 thousand rubles a month. The employment contract must indicate a salary of 22,990 rubles. This amount includes 13% personal income tax, which you will transfer to the state. Every month you pay 20 thousand rubles to the employee and 2,990 rubles to the tax office.

Who submits 6-NDFL in 2021

All organizations and individual entrepreneurs that are tax agents for personal income tax must submit quarterly calculations to their Federal Tax Service Inspectorate in form 6-NDFL. In 2021, calculations must be submitted on time, no later than the last day of the month following the corresponding reporting period (Clause 2 of Article 230 of the Tax Code of the Russian Federation).

You need to submit 6-NDFL calculations in 2021 to the Federal Tax Service at your place of registration (clause 2 of Article 230 of the Tax Code of the Russian Federation).

For organizations, this is, as a rule, the location, for individual entrepreneurs – the place of residence (clause 1 of Article 83 of the Tax Code of the Russian Federation). If the organization has separate divisions, then the 6-NDFL calculation in relation to income must be submitted to the tax authority at the place of their registration (clause 2 of Article 230 of the Tax Code of the Russian Federation):

- employees of such departments,

- individuals under civil contracts concluded with these separate divisions.

6-NDFL: where to submit?

Entrepreneurs and firms, being tax agents, submit 6-NDFL to the inspectorate at their place of residence (code 120 for individual entrepreneurs) or accounting (code 212 for organization). The “paper” calculation option is acceptable for agents who have paid income to a maximum of 25 individuals, while the rest report only electronically.

And where to submit 6-NDFL for a separate division to organizations that have such structures? They submit the calculation to the Federal Tax Service at the place of registration of each “separate unit” (code 220).

Such a 6-NDFL will reflect information about the tax on the income of employees of the division, as well as on the income of individuals with whom this division entered into civil contracts. Even if several divisions of an organization are registered with one tax office, you will have to submit 6-NDFL separately for each (letter of the Federal Tax Service of the Russian Federation dated August 1, 2016 No. BS-4-11/13984). In this calculation, the checkpoint of a separate subdivision is indicated (letter of the Federal Tax Service for Moscow dated December 29, 2017 No. 13-11/232704).

Apply the new form in 2018

From March 25, 2021, for reporting for 2021 and beyond, a new form of calculation, 6-NDFL, is in effect - as amended by Federal Tax Service order No. MMV-7-11/18 dated January 17, 2021. Until this date, you can submit the previous payment form. You can view the changes here:

https://publication.pravo.gov.ru/Document/View/0001201801250013

According to the amendments to the order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/450, which approved the form and procedure for filling out the 6-NDFL calculation, the title page of the 6-NDFL form was adjusted, the bar code “15201027” was replaced by the bar code “15202024” ”, the procedure for filling out and presenting the calculation, as well as the delivery format, have been changed.

Procedure for filling out 6-NDFL: submitting reports correctly

Let us note that the already mentioned Law No. 325-FZ made another change to the procedure for submitting 6-NDFL calculations. The number limit at which you can submit calculations on paper has been reduced. From 2020, the paper version is only acceptable for those with fewer than 10 employees.

Starting with reporting for the 1st quarter of 2021, global changes were made to the calculation of 6-NDFL: it was combined with 2-NDFL certificates.

You will see how to fill out the updated calculation on form 6-NDFL in the ready-made solution “ConsultantPlus”. You will find even more useful materials if you sign up for a free trial access to K+.

For 2021, the calculation should be submitted using the old form. It consists:

- from the title page - general information about the tax agent and contact details are indicated on it, a mark is placed on the method and date of submission;

- an information sheet that contains generalized cumulative indicators for personal income tax amounts; a breakdown of tax rates is also given, highlighting the amount of dividends;

- a payslip that reflects the dates of receipt of income, the date of withholding personal income tax and the deadline for payment to the budget, relating only to the reporting quarter.

There is a so-called carryover personal income tax - when salaries or other types of income are accrued to employees in one period, and payment is made in the next. In this case, the tax amount is recorded only in Section 1 of 6-NDFL for the reporting period, and in Section 2 it is displayed in the next period, when the tax was actually withheld.

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

You will find the calculation form and a sample of how to fill it out using the links at the beginning of our article.

In the absence of accruals and payments in favor of employees, there is no obligation to pay personal income tax, so you do not need to submit a blank form. However, it is better to play it safe, especially since the Federal Tax Service will accept a zero 6-personal income tax. Also in this case, you can send a letter to the tax authorities about the lack of activity.

If at least one payment was made during the year, the 6-NDFL calculation is formed for the quarter in which it was made and for all subsequent ones. Also in this case, we submit 6-personal income tax for the year, since the report displays the amounts on an accrual basis.

Reporting periods in 2021

Paragraph 2 of Article 230 of the Tax Code of the Russian Federation provides that for the purpose of submitting the calculation of 6-NDFL in 2021, the reporting periods are:

- 1 quarter;

- half year;

- 9 months;

- year.

Accordingly, based on the results of these reporting periods, calculations must be submitted to the Federal Tax Service using Form 6-NDFL. Moreover, if the last day for filing 6-NDFL falls on a weekend or a non-working holiday, then the calculation is submitted on the next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of Russia dated December 21, 2015 No. BS-4-11/ 22387). Accordingly, some deadlines for submitting 6-NDFL in 2021 may be postponed.

How are line 120 and the period for which 6-NDFL is formed related?

The report, prepared according to form 6-NDFL, consists of 2 sections, generated according to different rules:

- 1st reflects on an accrual basis (with a breakdown by rates) accruals of income and deductions made for the period from the beginning of the year, as well as the value of tax (calculated, withheld, not withheld, returned);

- The 2nd is devoted to information for the last quarter of the reporting period, which allows you to obtain information about specific amounts of tax that must be paid to the budget no later than a specific date falling in this quarter.

Line 120 in the 2nd section of form 6-NDFL is intended to indicate these specific tax payment dates. The significance of this line is quite large, since it is it that determines in which quarter this report will reflect data on paid income and personal income tax withheld from it. And the fact of reflection in section 2, in turn, will affect the amount of the tax withheld (or not withheld), shown in section 1 on an accrual basis.

The payment deadline for 6-personal income tax is determined according to rules that differ depending on what type of income is paid. These rules are established by two articles of the Tax Code of the Russian Federation:

- clause 6 art. 226, relating to the vast majority of income, but with regard to timing, dividing them into 2 types;

- clause 9 art. 226.1, applicable to income of only one type (from securities), but having several options for establishing the date of personal income tax payment.

You can see an example of filling out 6-NDFL in the Ready-made solution from ConsultantPlus. Get free demo access to K+ and go to the Ready Solution to find out all the details of this procedure.

Deadlines for submitting 6-NDFL in 2021: table

In 2021, taxpayers (organizations and individual entrepreneurs) need to submit calculations to the Federal Tax Service using Form 6-NDFL within the time limits indicated in the table below:

| Reporting period | Due in 2021 |

| 2017 | April 2, 2021 |

| 1st quarter 2021 | May 3, 2021 |

| 2nd quarter 2021 | July 31, 2021 |

| 3rd quarter 2021 | October 31, 2021 |

| 2018 | April 1, 2021 |

Next, we will explain the deadlines for submitting 6-NDFL for each reporting period in more detail.

6-NDFL for 2021

In 2021, you need to submit the annual calculation of 6-NDFL for 2021. According to the requirements of paragraph 2 of Article 230 of the Tax Code of the Russian Federation, the annual 6-NDFL must be submitted no later than April 1. However, April 1, 2021 is Sunday and tax offices are closed on these days. Therefore, the annual calculation of 6-NDFL for 2021 can be submitted no later than April 2, 2018.

6-NDFL for the 1st quarter of 2021

The deadline for submitting 6-NDFL for the 1st quarter of 2021 is no later than the last day of the month following the reporting period. That is, no later than April 30. But due to weekends and holidays in 2021 (April 30-May 2 are holidays), the deadline for submitting reports is postponed. The postponement of reporting is provided for in paragraph 7 of Art. 6.1 Tax Code of the Russian Federation. The deadline for submitting 6-NDFL for the 1st quarter of 2021 is 05/03/2017. Payments for the 1st quarter of 2021 must be submitted on the first working day after the holidays, that is, May 3.

6-NDFL for the 2nd quarter of 2021

For April-June 2021, you must submit 6-NDFL to the Federal Tax Service no later than the 30th day of the month following the 2nd quarter. The deadline for submitting 6-NDFL for the 2nd quarter (half year) of 2021 is 07/31/2018. There are no holidays in July, and there are no transfers from weekends either, so the deadline is not postponed or extended.

6-NDFL for 9 months of 2021

Report for 9 months - the last calculation of 6-NDFL in 2021. The deadline for submitting 6 personal income taxes for the 3rd quarter (9 months) of 2021 is 10/31/2018. There will be no rescheduling due to weekends or holidays. Therefore, it is better to prepare and submit the calculation in advance. The reporting campaign for 9 months will begin on October 1, 2021. For a delay in settlement of more than 10 working days - until November 9, the inspectorate has the right to block current accounts (clause 3.2 of Article 76 of the Tax Code of the Russian Federation).

In 2021, you do not need to submit a “zero” calculation of 6-NDFL if you did not accrue or pay income on which you need to pay tax (Letter of the Federal Tax Service of Russia dated 01.08.2016 N BS-4-11/13984) We recommend notifying the Federal Tax Service about this that you do not plan to submit a 6-NDFL calculation, and explain the reason. Otherwise, the tax authority may suspend your transactions on accounts (transfers of electronic funds), as well as fine you for failure to submit a payment (clause 3.2 of Article 76, clause 1.2 of Article 126 of the Tax Code of the Russian Federation). If you nevertheless decide to submit a “zero” calculation of 6-NDFL, then the tax authority will accept it (Letter of the Federal Tax Service of Russia dated May 4, 2016 N BS-4-11/7928).

If you violate the deadlines for submitting 6-NDFL in 2021, then penalties may be applied to the organization or individual entrepreneur or the account may be blocked. Read more about this “Fines for late submission of 6-NDFL”.

Read also

25.11.2016

Sanctions for late submission of a report

Tax agents who fail to submit the form on time are fined and their bank account is subsequently frozen. According to clause 1.2 of Art. 126 of the Tax Code, a legal entity or individual entrepreneur pays 1000 rubles. for each calendar month. The delay time is counted from the moment after the deadline for submitting 6-NDFL - the deadline for submitting reports for 2018 must also be observed by the company’s employees. They are subject to a fine of 300-500 rubles.

For the calendar year 2021, reporting papers are submitted 4 times. We recommend downloading the unified form of the new form below to avoid misunderstandings on the part of the tax authorities.

Similar articles

- 6-NDFL for the 4th quarter: due date

- Deadline for submitting 2-NDFL (with sign 2) for 2021

- Accounting calendar for 2021 - reporting

- Submitting 2-NDFL on paper

- Declaration 6-NDFL in 2018

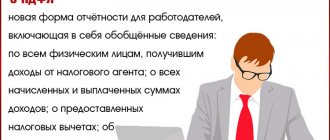

What does Form 6-NDFL show?

6 Personal income tax is a relatively new report, mandatory for all employers, applied from the 1st quarter of 2021.

It includes information about:

- employee remuneration (income);

- accrued, withheld and transferred personal income tax;

- terms of assignment, withholding and transfer of tax.

The document form and the algorithm for its execution were approved by order of the Federal Tax Service on October 14, 2015 No. ММВ-7-11/ [email protected] To calculate for 9 months, you should take the form as amended. Order of the Federal Tax Service dated January 17, 2018 No. ММВ-7-11/ [email protected]

You can download the current 6-NDFL form here .