The concept of strict reporting forms

Strict reporting forms are paper documents that some organizations issue instead of sales and cash receipts to confirm the acceptance of money from the public. There are many types of forms, and examples include train tickets, theater tickets, shoe repair receipts, etc.

At the moment, the use of strict reporting forms (abbreviated as BSO) is possible when providing any services, even those not listed in OKUN.

Organizations using such documents must keep strict records of them, since BSOs are a form of reporting to the tax authorities.

Off-balance sheet account 006

Off-balance sheet accounts are designed to account for various property that is in the company temporarily, in storage or on a rental basis, for example. A feature of accounting on these accounts is the absence of a double entry method, that is, there will be no correspondence in the Dt or Kt account. Analytical accounting is maintained in registers developed by the company independently and reflected in the accounting policies.

By the way, you can find out what’s new in the accounting policy for the next year here.

To account for strict reporting forms, the current chart of accounts provides for account 006. It is off-balance sheet, that is, its balance will not be affected in any way by the balance sheet currency, however, this account will not allow you to forget about some material assets in the company.

The debit of this account records the receipt of forms in the conditional valuation, and the credit indicates the expense. It is assumed that records are kept in the context of the name of each form and where they are stored. Thus, if your company has a separate division, then you will have 2 storage locations in this account. The company sets the conditional valuation (for example, 1 ruble) independently.

The requirements for maintaining off-balance sheet accounts are almost the same as for balance sheet accounts. You can find out about the inventory of such accounts in our article “Is it possible to carry out an inventory for an off-balance sheet account?”

You can read about off-balance sheet accounting in general here.

Let's look at accounting for strict reporting forms using an example.

Purpose of account 006

Account 006 “Strict reporting forms” is off-balance sheet, so its balance will not be directly related to the enterprise’s balance sheet.

Off-balance sheet accounts, including 006, are intended to control the movement and use of assets that do not actually belong to the enterprise, but are currently at its disposal.

To record such values, the simplest version of the accounting system is used.

Account 006, like other off-balance sheet accounts, does not correspond with others and is not reflected in the enterprise’s balance sheet.

You can also keep records to control the use of BSO. In this case, debit assumes the receipt of BSO, and credit takes into account their expenditure in a certain denomination.

Payment documents such as receipts, checks, lottery tickets, work record forms, diplomas, certificates and securities are credited to this account as BSO.

Movements for each type of BSO are recorded in a separate journal, according to which postings are then generated.

Moreover, in this case, it is not the cost of all forms that is important, but their number.

Example of BSO accounting on account 006

Most often, BSOs are purchased independently by the company and are issued to employees. Accounting for the costs of purchasing such forms is carried out in cost accounts at the cost of their acquisition according to the documents. The BSO themselves are accounted for in account 006.

Example

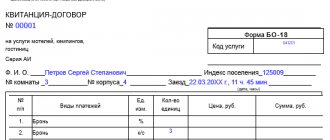

works with the population in cash. According to current regulations, when receiving funds, the company issues receipts, which are BSO. A batch of BSO purchased on April 3 was purchased for 25 kopecks. per piece excluding VAT, 2000 pieces - according to the invoice. Receipts were immediately issued to stores for customer service. The accountant will show the following entries in accounting:

- Dt 10 “Materials” Kt 60 “Settlements with suppliers” - forms (receipts for the provision of services) have been capitalized at the cost of the invoice - 500 rubles. (0.25 rub. × 2000 pcs.);

- Dt 20 “Main production” Kt 10 “Materials” - receipts issued for work are written off - 500 rubles.

Simultaneously with this posting, others appear to control the use of forms (in terms of storage locations):

- Dt 006 “Store No. 1” - some of the forms were transferred under the act: 250 rubles. — 1000 pieces;

- Dt 006 “Store No. 2” - some of the forms were transferred under the act: 250 rubles. — 1000 pieces;

- Kt 006 “Store No. 1” - 50 forms were written off from the storage location (according to the store report from April 3 to April 10): 12.5 rubles. (50 × 0.25 rub.);

- Kt 006 “Store No. 2” - written off from the storage location based on the report of 200 forms: 50 rubles. (200 × 0.25 rub.).

OFF BALANCE ACCOUNTS

79. Off-balance sheet account 001 “Leased fixed assets” is intended to summarize information on the availability and movement of fixed assets received for rent for free use. Fixed assets are accounted for in off-balance sheet account 001 “Leased fixed assets” at the cost specified in lease agreements for free use.

Analytical accounting for off-balance sheet account 001 “Leased fixed assets” is carried out for lessors, lenders and individual fixed assets.

(clause 79 as amended by the resolution of the Ministry of Finance dated December 20, 2012 N 77)

80. Off-balance sheet account 002 “Property accepted for safekeeping” is intended to summarize information about the availability and movement of property accepted for safekeeping.

Property accepted for safekeeping is accounted for in off-balance sheet account 002 “Property accepted for safekeeping” at the cost indicated in the primary accounting documents.

Analytical accounting for off-balance sheet account 002 “Property accepted for safekeeping” is carried out by organizations from which this property was received, types of property and places of their storage.

(as amended by the resolution of the Ministry of Finance dated December 20, 2012 N 77)

81. Off-balance sheet account 003 “Materials accepted for processing” is intended to summarize information about the availability and movement of customer materials accepted for processing, not paid for by the manufacturer. Accounting for the costs of processing materials is carried out on production cost accounts (with the exception of the cost of customer materials accepted for processing). Customer materials accepted for processing are recorded on off-balance sheet account 003 “Materials accepted for processing” at the cost specified in the contracts.

Analytical accounting for off-balance sheet account 003 “Materials accepted for processing” is carried out by customers, types, grades of materials and their locations.

82. Off-balance sheet account 004 “Goods accepted for commission” is intended to summarize information about the availability and movement of goods accepted for commission in accordance with the commission agreement, and is used by commission agents.

Goods accepted on commission are accounted for in off-balance sheet account 004 “Goods accepted on commission” at the cost indicated in the primary accounting documents.

Analytical accounting for off-balance sheet account 004 “Goods accepted on commission” is carried out by type of goods and consignors.

83. Off-balance sheet account 005 “Equipment accepted for installation” is intended to summarize information about the availability and movement of equipment received by the contractor from the customer for installation.

Analytical accounting for off-balance sheet account 005 “Equipment accepted for installation” is carried out for individual equipment items.

84. Off-balance sheet account 006 “Document forms with a certain degree of protection” is intended to summarize information on the availability and movement of document forms with a certain degree of protection stored and issued for reporting.

(as amended by the resolution of the Ministry of Finance dated December 2, 2013 N 71)

Forms of documents with a certain degree of protection are accounted for in off-balance sheet account 006 “Forms of documents with a certain degree of protection” at nominal value or in conditional valuation.

(as amended by the resolution of the Ministry of Finance dated December 2, 2013 N 71)

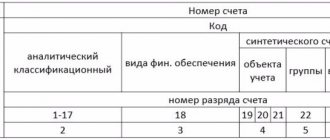

Analytical accounting for off-balance sheet account 006 “Document forms with a certain degree of protection” is carried out according to the types of document forms with a certain degree of protection and the places of their storage.

(as amended by the resolution of the Ministry of Finance dated December 2, 2013 N 71)

85. Off-balance sheet account 007 “Written off uncollectible receivables” is intended to summarize information about uncollectible receivables written off from settlement accounts. The specified debt is accounted for in off-balance sheet account 007 “Written off uncollectible accounts receivable” for five years from the date of its write-off from the settlement accounts.

The receipt of amounts to repay previously written off accounts receivable is reflected in the credit of off-balance sheet account 007 “Written off uncollectible accounts receivable”.

Analytical accounting for off-balance sheet account 007 “Write-off uncollectible accounts receivable” is maintained for each debtor whose debt is written off from the settlement accounts, and for each debt written off.

86. Off-balance sheet account 008 “Securities for obligations received” is intended to summarize information on the availability and movement of guarantees received to secure the fulfillment of obligations, as well as security received for goods transferred to other parties. The amounts of collateral recorded in off-balance sheet account 008 “Collateral for obligations received” are written off from this account as the obligations are repaid.

Analytical accounting for off-balance sheet account 008 “Collateral for obligations received” is maintained for each collateral received.

87. Off-balance sheet account 009 “Securities for obligations issued” is intended to summarize information on the availability and movement of guarantees issued to ensure the fulfillment of obligations. The amounts of collateral recorded in off-balance sheet account 009 “Collateral for obligations issued” are written off from this account as the obligations are repaid.

Analytical accounting for off-balance sheet account 009 “Collateral for obligations issued” is carried out for each issued collateral.

88. Off-balance sheet account 011 “Fixed assets leased” is intended to summarize information on the availability and movement of fixed assets leased, if, in accordance with the law, they are taken into account on the balance sheet of the lessee.

(as amended by the resolution of the Ministry of Finance dated December 20, 2012 N 77)

Fixed assets leased are accounted for in off-balance sheet account 011 “Fixed assets leased” at the cost specified in the lease agreements.

Analytical accounting for off-balance sheet account 011 “Fixed assets leased out” is carried out for tenants and individual fixed assets.

(as amended by the resolution of the Ministry of Finance dated December 20, 2012 N 77)

89. Off-balance sheet account 014 “Loss of value of fixed assets” is intended to summarize information about the loss of value of fixed assets for which depreciation is not charged in accordance with the law. The loss of value of the specified fixed assets is reflected in off-balance sheet account 014 “Loss of value of fixed assets” in the manner prescribed by law. When these fixed assets are disposed of, the accumulated amount of loss of value on them is reflected in the credit of off-balance sheet account 014 “Loss of value of fixed assets”.

Analytical accounting for off-balance sheet account 014 “Loss of value of fixed assets” is carried out for fixed assets.

90. Off-balance sheet account 016 “Real estate in joint household ownership” is intended to summarize information on the availability and movement of real estate in joint household ownership in the owners’ association.

(as amended by the resolution of the Ministry of Finance dated December 20, 2012 N 77)