Tip 1: How to determine the TN VED code

If the country of the manufacturer from whom you are purchasing the goods has an international HS system, then the first six digits of the HS code for the goods you import must match.

In practice, you may encounter a situation where the seller does not declare the exported goods or customs inspectors simply do not agree with the specified code. 2 Try to independently understand the principles of product classification and determine the HS code. Carefully study the Commodity Nomenclature of Foreign Economic Activity: it has a tree-like structure, the top of which is “Sections”. Each section name characterizes the industry that produces the goods or products you are importing. This is followed by “Groups”, formed taking into account the raw materials from which the product is made, the degree of processing of the product, as well as the functionality of the product.

Then “Commodity Items” are presented, followed by “Commodity Subitems” and subsequent detailed classification.

Code - (HSVED)

Let's look at this code as an example: 8519813100 - car radio with CD The code contains the following information: The commodity group of the HS is contained in the first two characters (85ХХХХХХХХ - sound recording and sound reproducing equipment...); The following numbers indicate the product item (8519ХХХХХХ - Sound recording or sound reproducing equipment:); Then the numbers of the product subposition are located (851981ХХХХ - using magnetic, optical or semiconductor media:); Let's open the code completely and get the product subposition (8519813100 - sound-reproducing app, without a sound recording device: with a laser reading system: used in motor vehicles, using disks dia.

no more than 6.5 cm) Any code element has explanations that are an official supporting document. In practice, declarants are most often involved in determining and assigning a code.

Drawing up and form of UPD

The recommended UPD form is given in the letter of the Federal Tax Service of Russia dated October 21, 2013 No. ММВ-20-3/ [email protected]

Now let’s look at how to fill out the UPD form line by line in Table 2:

| Name of the line (columns) in the UPD | String value, columns |

| 1 | 2 |

| "Status" | Possible values: "1" and "2". They are selected depending on the purpose of using the document: “1” - UPD replaces the invoice and the transfer deed; “2” - UPD replaces only the transfer act (i.e. it is primary) |

| Lines (1)-(7) columns 1-11 | For UPD with status “1” they all must be filled out. If invoices in an organization are signed not by the director, but by another person authorized to do so by order (power of attorney), then this document or the position of the authorized person can be indicated on the invoice. It is allowed to clarify the indicators on lines (3) and (4) with information about the TIN, checkpoint of the consignor and the TIN, checkpoint of the consignee. For UPD with status “2”, you can fill in lines (1), (1a), (2), (6), (7), columns 1, 2 or 2a, 3 and 9 to reflect the fact of economic life and the amount of natural and monetary measurements. And also fill in the indicators that clarify the conditions for the fulfillment of a fact of economic life in lines (2a), (2b), (3), (4), (5), (6), (6a), (6b), columns (4) , (5), (6), etc. |

| Column A “Item No.” | The serial number of the entry in the table is indicated |

| Column B “Code of goods/works, services” | If a product is reflected in the UPN, then you need to indicate its article number. If works or services are reflected - then OKVED, or OKUN |

| Line [8] “Grounds for transfer (delivery)/receipt (acceptance)” | It is necessary to indicate information identifying the emerging relations of the parties: types of relations, details of contracts, agreements, instructions, etc. |

| Line [9] “Data about transportation and cargo” | It reflects the details of transport documents (bill of lading, waybill), instructions to forwarders, warehouse receipts and other clarifying information about transportation. For example, you can indicate the name of the organization that bears the transportation costs. The line also reflects information about the cargo: net/gross weight |

| Line [10] “Product (cargo) transferred/services, results of work, rights handed over” | A signature is affixed indicating the surname and initials: - the position of the person who made the shipment; - or a person authorized to act on a transaction for the transfer of work results (services, property rights) on behalf of an economic entity. If a person is simultaneously a person authorized to sign invoices and has signed the document on behalf of the manager (chief accountant), then this line indicates only information about his position and full name. without repeating the signature |

| Line [11] “Date of shipment, transfer (handover)” | It is necessary to indicate the date of the fact of economic life, that is, the actual date of shipment of goods, provision of services, transfer of results of work performed, transfer of property rights |

| Line [12] “Other information about shipment, transfer” | This line provides additional information. For example, data on passports, product certificates. If there are integral annexes to the UPD, indicate the number of these documents and their type |

| Line [13] “Responsible for the correct execution of the transaction, operation” | Here you need to write down the position of the person responsible for the correct execution of the transaction (operation) on the part of the seller, his signature indicating his last name and initials. If this person is at the same time the person who made the shipment or is authorized to act on the transaction on behalf of the economic entity (line [10]), then (if there is a signature in line [10]) only his position and full name can be indicated in this line . without repeating the signature. If this person is simultaneously the person authorized to sign invoices and signed the document on behalf of the manager (chief accountant), then only his position and full name are also indicated in this line. without repeating the signature. If several persons are simultaneously responsible for the correct execution of the transaction, then an additional line ([13a]) must be entered into the document to indicate the position, full name. and signatures of the second responsible person. |

| Line [14] “Name of the economic entity - the document preparer (including the commission agent (agent)" | The name and other details identifying the economic entity that drew up the document on the part of the seller may be indicated. This line indicates: - information about the economic entity maintaining the seller’s accounting records on the basis of the agreement; - or information about the commission agent (agent), if he transfers to the principal (principal) goods, results of work, services purchased from the seller on his own behalf (in this case, line [8] indicates the details of the agreement between the principal (principals) and the intermediary). The line may not be filled in if there is a seal containing the full name of the economic entity that compiled the document. |

| Line [15] “Goods (cargo) received/services, results of work, rights accepted” | The position of the person who received the cargo and (or) authorized to accept services, results of work, rights under the transaction of transfer of results of work (services, property rights) on behalf of the buyer is indicated; as well as his signature indicating his last name and initials |

| Line [16] “Date of receipt (acceptance)” | It indicates the actual date of receipt of the goods (cargo), acceptance of the results of the work performed, receipt of property rights by the buyer or another person authorized by the buyer. Please keep in mind that the date of receipt cannot be earlier than the date of preparation of the UTD (line 1) and the date of transfer recorded by the seller in line [11] |

| Line [17] “Other information about receipt, acceptance” | This line reflects information about the presence or absence of claims; as well as data on documents drawn up by the buyer (customer) upon receipt of goods (work, services, property rights), which are integral annexes to the UPD. For example: no complaint. If there are complaints, indicate information about additional documents drawn up upon receipt/acceptance of goods |

| Line [18] “Responsible for the correct execution of the transaction, operation” | The position of the person responsible for the correct execution of the transaction, operations on the part of the buyer, his signature indicating the surname and initials are indicated. If the person responsible for processing the transaction is at the same time a person authorized to act on the transaction on behalf of the economic entity (line [15]), then only information about the position and full name should be filled in this line. without repeating the signature. If several persons are simultaneously responsible for the correct execution of the transaction, then an additional line must be entered into the document ([18a]) to indicate the position, full name. and signatures of the second responsible person |

| Line [19] “Name of the economic entity - the document preparer” | The line may indicate the name and other details identifying the economic entity that drew up the document on the part of the buyer (participant in the transaction, operation). For example, information about the person maintaining the accounting records of an economic entity on the basis of an agreement. The line may not be filled in if there is a seal containing the full name of the economic entity taking part in the preparation of a specific bilateral document. |

| "M.P." | The stamps (or INN/KPP) of the economic entities that compiled the document are affixed. However, the absence of stamps (if all the required details are present) will not be grounds for refusal to accept a document for tax registration |

Selection of HS codes

It was the HS that formed the basis for most commodity classifiers that were created in the countries of the European Union and the CIS. Classification of goods according to the Commodity Nomenclature of Foreign Economic Activity consists of assigning each product a special code consisting of ten or fourteen characters.

The code is subsequently used when carrying out or performing all sorts of activities, including declaring goods and collecting duties. The purpose of such coding is to ensure the same identification of goods crossing Russian borders. This is goal number one. Goal number two: as a result, simplification of automated processing of customs declarations and declarations, which are provided by customs when carrying out foreign trade activities.

Strictly speaking, everything is created for systematization, and the customs service simply needs a single classifier.

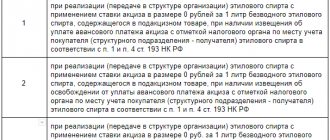

In accordance with paragraph 5 of Article 169 of the Code as amended by the Law, the invoice issued for the sale of goods (work, services), transfer of property rights must indicate the code of the type of goods in accordance with the unified Commodity Nomenclature for Foreign Economic Activity of the Eurasian Economic Union (hereinafter - TN VED).

The current version consists of 21 sections and 97 groups. Only group No. 77, which is only reserved, is not used for its intended purpose. The information provided for in this subclause is indicated in relation to goods exported outside the territory of the Russian Federation to the territory of a member state of the EAEU.

At the same time, according to paragraph three of paragraph 10 of Article 165 of the Code as amended by the Law, for raw materials, upon export of which value added tax amounts are deducted

Product codes

All-Russian product classifiers are Russian national standards included in the “Unified System of Classification and Coding of Technical, Economic and Social Information” and developed and implemented by departmental orders in order to obtain information about products in all sectors of the national economy and the country’s economy.

Need instant expert advice? Just call the toll-free number Or in the feedback form: Or write to us in instant messengers and get an instant response from an expert:

TORG-12 product code in column 3

7) signatures of the persons provided for in paragraph 6 of this part, indicating their surnames and initials or other details necessary to identify these persons.

These norms are included in the text of Article 169 of the Code in connection with the establishment of a new procedure for deductions of value added tax (as registered on the basis of invoices) when selling non-commodity goods for export. Only the listed details are mandatory; inclusion of all other details in the document form is the right, not the obligation of the organization. As for the use of HS codes when filling out TORG-12, ATP Consultant + does not contain any explanations on this matter. The presented samples (in the attachment) are filled out using “OK 005-93. All-Russian Classifier of Products”, approved by Decree of the State Standard of Russia dated December 30, 1993 N 301. However, from 2019 “OK 034-2014 (CPES 2008) will be in force.

All-Russian classifier of products by type of economic activity" (approved by Order of Rosstandart dated January 31, 2014 N 14-st), which can be used now.

- (9 MB)

- (91 kB)

- (107 kB)

- (14 kB)

- (5 MB)

What it is?

The Commodity Nomenclature of Foreign Economic Activity is an official classifier that contains the information required for declaring goods. The customs code includes ten digits containing characteristics of the product class, its variety, subgroup, etc. The HS codes we now know were developed in parallel with the creation of the EurAsEC Customs Union. Since then, they have been actively used by customs officers and participants in foreign trade activities in customs operations. The HS Classifier is essentially a domestic variation of the Harmonized System, which is widely used in Europe. Thanks to HS codes, customs authorities compile trade statistics. Based on the code, the customs duty for the goods is determined, and a set of permits required for its successful transportation across the border is generated.

Filling out the Product Code column in Torg-12

In accordance with clause 13 of the Regulations on accounting and financial reporting in the Russian Federation, approved by Order of the Ministry of Finance of Russia dated July 29, 1998 N 34n, primary accounting documents are accepted for accounting if they are drawn up in the form contained in the albums of unified (standard) forms of primary accounting documentation. The unified form of consignment note N TORG-12, approved by Resolution of the State Statistics Committee of Russia dated December 25, 1998 N 132 “On approval of Unified forms of primary accounting documentation for recording trade operations,” is used to register the sale (issue) of inventory assets to a third-party organization. The consignment note is drawn up in two copies, one of which is transferred to the buyer and is the basis for the posting of these values. In accordance with Resolution of the State Statistics Committee of Russia dated March 24, 1999 N 20, deleting individual details from unified forms is not allowed. At the same time, it is allowed to include additional necessary details, change the form, expand or narrow the columns and lines, and include additional lines and loose-leaf sheets. The changes made must be documented in the organizational and administrative document of the organization. In accordance with Art. 9 of the Federal Law of November 21, 1996 N 129-FZ “On Accounting” (hereinafter referred to as Federal Law N 129-FZ), all business transactions must be documented with primary accounting documents on the basis of which accounting is maintained. Primary accounting documents are accepted for accounting if they are drawn up in the form contained in the albums of unified forms of primary accounting documentation, and documents whose form is not provided for in these albums must contain the following mandatory details:

a) name of the document; b) date of preparation of the document; c) the name of the organization on whose behalf the document was drawn up; d) content of the business transaction; e) measures of business transactions in physical and monetary terms; f) names of positions of persons responsible for carrying out a business transaction and the correctness of its execution; g) personal signatures of these persons. Thus, the posting of goods can be confirmed by the taxpayer with a consignment note or other documents that meet clauses 1 and 2 of Art. 9 of Federal Law N 129-FZ. According to the arbitration courts, the absence of certain details in the invoices does not prevent the recognition of such an invoice as evidence of the registration of purchased goods for the purpose of making VAT deductions by the taxpayer, if the disputed invoices allow one to reliably establish the fact of a business transaction, and the missing details, taking into account their significance, do not influence the confirmation of this fact. In the Resolution of the Federal Antimonopoly Service of the East Siberian District dated February 10, 2006 N A19-14981/05-33-Ф02-6833/05-С1, the court considered it documented that the taxpayer accepted the purchased goods for accounting, despite the absence of individual details in the invoices submitted by the taxpayer, such as the payer's OKPO code, the number and date of the waybill, the decoding of the consignee's signature, indicating that the absence of the listed details does not indicate the absence of the fact of a business transaction. The Resolution of the Federal Antimonopoly Service of the East Siberian District dated February 14, 2006 N A19-16647/05-43-Ф02-211/06-С1 noted that the absence of a stamp on the receipt of received timber in the waybills does not prevent the registration of purchased goods, since the goods themselves invoices allow you to reliably establish the fact of delivery of goods, their price and quantity. These violations in the execution of documents indicate a violation of accounting rules, but cannot be an unconditional basis for refusal to apply tax deductions. In the Resolution of the Federal Antimonopoly Service of the North-Western District dated 01.03.2006 in case No. A13-5001/2005-05, the court came to the conclusion that the absence of mandatory details in the invoices in the columns: “Vacation made - position, signature, transcript of signature”; “By power of attorney - number, date, by whom and issued to”; “Received the cargo - title, signature, transcript of the signature” is a minor violation of registration and does not refute the fact of transfer and receipt of the goods, since the columns “Release of goods was authorized” and “The cargo was received by the consignee” are properly filled out. In the Resolution of the Federal Antimonopoly Service of the East Siberian District dated January 19, 2006 N A74-2150/05-Ф02-6972/05-С1, the court came to the conclusion that the receipt of goods can be confirmed by the invoice in the absence of the details provided for in the unified form, if In this regard, it complies with the general requirements for the preparation and execution of primary documents established by Art. 9 of Federal Law N 129-FZ. Thus, the absence in the delivery note of certain details provided for by the unified form does not refute the fact that the taxpayer has accepted for registration of goods purchased from suppliers, and cannot be an independent basis for declaring the application of the corresponding VAT deductions unjustified if violations in registration are of a minor nature and when In this case, the invoice meets the general requirements for the preparation and execution of primary documents provided for in Art. 9 of Federal Law N 129-FZ. Yu.M. Lermontov Ministry of Finance of Russia

Product code of work and services in UPD

Thus, the UTD can be considered as an invoice with additional details, and accordingly, taxpayers should not be afraid to claim deductions based on it. The UPD form, along with the procedure and recommendations for filling it out, was developed by the Federal Tax Service of Russia and proposed for use in a letter on its application.

The first part of this document is almost identical to the invoice form, with the only difference that the UPD contains the “Status” attribute, two new columns “Item No.” and “Product/work, service code”, as well as a field in which you need to write down how many sheets it is compiled on. The “Status” detail is selected by the taxpayer from two options: 1 – invoice and transfer document (act); 2 – transfer document (act).

It is not mandatory, it is only designed to make the work of accountants easier and reduce the costs of organizations.

Since the invoice form changed from 07/01/2017, and then from 10/01/2017, the UPD form also needs to be adjusted, including adding:

- columns 1a to reflect the code of the type of goods exported to the EAEU countries.

- lines 8 to indicate the government contract identifier. This line is filled in by those who work under government contracts, others put a dash here.

You can adjust the “invoice” part of the UPD yourself.

Attention! The form is advisory in nature.

Failure to use this form for registration of facts of economic life cannot be a basis for refusal to take into account these facts of economic life for tax purposes (Letter of the Federal Tax Service of Russia dated October 21, 2013 N ММВ-20-3/ [email protected] )

Attention! Federal Tax Service of Russia that taxpayers can use the document form, independently supplementing it with indicators, including those necessary to fulfill the requirements established by Article 169 of the Tax Code of the Russian Federation and the Rules for filling out an invoice used in calculations for value added tax (Federal Tax Service of Russia dated September 14, 2017 N ED-4-15/18322)

Recommended by Letter of the Federal Tax Service of Russia dated October 21, 2013 N ММВ-20-3/ [email protected]

ATTENTION! Information about the product code will be indicated only if in the accounting parameters settings (section Main - subsection Settings) on the "Inventory" tab in the part "When printing documents next to the "Name" column, the following is displayed:" a check mark is set for the "Column" values “Article” or “Code” column.

In this case, the amount of VAT payable to the budget is determined as the amount of tax indicated in the issued invoice. Consequently, if an organization using the simplified tax system for some reason issues an invoice to the buyer with the value “Without VAT” indicated in column 7 “Tax rate” and, accordingly, with the absence of the tax amount in column 8 “Tax amount required” buyer”, then such an organization will not have the obligation to calculate and pay the amount of tax to the budget. At the same time, due to the presence of a posted document in the accounting system “Invoice issued”, the program will automatically generate an UPD with the status “1”.

Filling out the consignment note Torg-12

Thus, the posting of goods can be confirmed by the taxpayer with a consignment note or other documents that meet clauses 1 and 2 of Art. 9 of Federal Law N 129-FZ. According to the arbitration courts, the absence of certain details in the invoices does not prevent the recognition of such an invoice as evidence of the registration of purchased goods for the purpose of making VAT deductions by the taxpayer, if the disputed invoices allow one to reliably establish the fact of a business transaction, and the missing details, taking into account their significance, do not influence the confirmation of this fact. Product code in TN When filling out the invoice, you must enter the product code in the main part of the document. Typically, the seller company assigns this code independently and indicates it in the price list. But sometimes organizations work on the basis of the All-Russian Product Classification (OK).

Attention When filling out a delivery note in 1C, along with other data, you must indicate the product code. To do this, you need to perform the following steps: Open the “Nomenclature” directory. When adding a new product, press the “add new product” button and fill in “Product Name”, “Product Code”, columns “Price”, “Unit of Measure.” etc. When editing products by line, enter the Product Code.” Subsequently, when filling out the delivery note, the program automatically enters the name and code of the product. How to change an invoice in 1C In the 1C configurator, you can change the invoice by opening a form with a table.

According to accounting legislation, the column “Product Code” is not required to be filled out. Rationale for the conclusion: According to Part 4 of Art. 9 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting” (hereinafter referred to as Law N 402-FZ), the forms of primary accounting documents are determined by the head of the economic entity on the proposal of the official entrusted with accounting. Based on this, at present At the same time, organizations are not required to use unified forms of primary documents in accounting, with the exception of those established by authorized bodies in accordance with and on the basis of federal laws (see information from the Ministry of Finance of Russia dated December 4, 2012 N PZ-10/2012). However, the provisions of Law N 402-FZ does not contain a ban on the use of unified forms of primary accounting documents, so an organization can continue to use them if it makes such a decision.

Registration of a delivery note

In terms of design, the document must exactly correspond to the approved form - otherwise it will be invalid.

You can see what the invoice should look like by downloading the TORG-12 invoice form. Important advice for entrepreneurs: do not waste your time, even on simple routine tasks that can be delegated. Transfer them to the freelancers “Ispolnyu.ru”. Guarantee of quality work on time or refund.

Prices even for website development start from 500 rubles.

First of all, information about the sender and recipient of the product, information about the seller and buyer is indicated. All this information must be entered into the invoice based on the details contained in the constituent documents of the counterparty companies. Details include:

- full or abbreviated name of the company;

- organization address. It is best to indicate a legal address. This allows you to avoid problems with obtaining a VAT deduction in the future;

- contact phone number;

- Bank details. How to fill out column 3 in the consignment note according to form No. TORG-12 You should indicate the number of current and correspondent accounts, the name of the bank and BIC.

On the right side of the form there is a table in which you need to indicate OKPO and OKDP of the sender of the goods. These classification codes are assigned by authorized organizations and differ in each specific case. Below are the columns “Consignment note”. They are filled out in cases where the TORG-12 form is executed instead of the commodity section of the TTN.

An agreement or work order is the actual basis for a transaction to be completed. The number and date of the contract are the main information. They should be entered in the appropriate line of the TORG-12 form.

Mandatory nomenclature

Each invoice must be provided with a number and date of preparation. The tabular part of the form contains a list of items that will be transferred to the buyer of the goods. In addition, it will contain information about the product itself: units of measurement, packaging form, quantity of the product or its weight, unit price, VAT and total cost.

The following information about the product must be entered:

- serial number;

- product name;

- unit of measurement;

- quantity or net weight;

- unit price;

- total amount excluding VAT;

- VAT (not indicated if the simplified tax system is used);

- total amount including VAT.

The remaining columns are optional. Information is entered into them only when necessary.

After the table is completed, the number of positions is written down in words (not in numbers) to avoid errors. The mass of goods or the number of units of production is also written in words. If goods are subject to certification, then the number of attached certification documents is indicated.

If even the slightest mistake was made when filling out the document, then the invoice should be completely redone. Typos and corrections are not allowed. Details and all information about organizations must be filled out in accordance with legal requirements.

Signatures of counterparties

Filling out the consignment note ends with the parties putting their signatures. Most often, the seller is also the sender of the goods in the transaction, but sometimes the actual senders can also be third parties - transport and courier services.

Signatures must be placed in the following order:

- signature of the seller (“chief accountant”);

- the responsible person of the seller (“the release of cargo has been authorized”);

- The responsible person of the sender is the one who actually carried out the shipment of the goods (“released the goods”).

Signatures are certified by a seal impression.

If on the buyer’s side the goods are accepted not by the responsible person, but by a trusted person, then he must receive a power of attorney, and this information is also reflected in the invoice.

Only in this case will the signature of the authorized person accepting the goods be valid. At the end of the document there is a date of conclusion - when the goods were issued and received.

Comments

What is the code in the bill of lading trade-12, column 3

Bill of lading (CH) is a document required for registration when selling products. The form for filling out the invoice is approved by Resolution of the State Statistics Committee of the Russian Federation dated December 25, 1998 No. 132. Rules for filling out the goods invoice TN is filled out in two copies, one of which, together with the goods, is transferred to a third party, the other remains in the accounting department of the selling enterprise.

Info The presence of a delivery note allows you to write off products from the warehouse, as well as register them with the buyer. The TN invoice can be issued in paper or electronic form. The main importance of the documents is the registration of the fact of purchase/sale of goods with the subsequent synthesis of information to determine the income tax for payment to the budget. Mandatory details that are indicated in the technical specification are: - date and number, - details of counterparty organizations, - name, quantity, cost of goods, - full name. and signatures of officials. If a special accounting program is used for accounting, the product code is assigned automatically when entering the product into the program directory (in the absence of special coding). The letter of Rosstat dated 02/03/2005 N IU-09-22/257 states that in the unified forms there are unfilled details are not allowed. However, this clarification refers to the period when the use of unified forms of primary accounting documents was mandatory (clause 2 of Article 9 of the Federal Law of November 21, 1996 N 129-FZ “On Accounting”). Currently, unified forms are used at the request of the organization. According to part 2 of Art. Law N 402-FZ mandatory details of the primary accounting document are: 1) name of the document; 2) date of preparation of the document; 3) name of the economic entity that compiled the document; 4) content of the fact of economic life; 5) the value of the natural and (or) monetary measurement of the fact economic life indicating the units of measurement;6) the name of the position of the person (persons) who completed the transaction, operation and the person(s) responsible for its execution, or the name of the position of the person(s) responsible for the execution of the accomplished event;7 ) signatures of the persons provided for in the previous paragraph, indicating their last names and initials or other details necessary to identify these persons. Thus, the product code is not a mandatory detail of the primary accounting document, therefore, in our opinion, it may not be filled out.

Filling out the column

Universal transfer document.

Filling out the “Product Code” column, responsibility. Question: is it necessary to fill out the column “Code of goods/works, services” of the Universal Transfer Document. What could this mean for the Buyer and Supplier?

Answer:

Fill out that part of the UPD that completely duplicates the invoice according to the rules established for issuing invoices. That is, be sure to fill out column 1a “Product Type Code” when selling goods for export to the countries of the Customs Union (clause 15 of Article 169 of the Tax Code of the Russian Federation).

If this column is left empty, there is a possibility that inspectors will point out that the invoice (part of the UPD) was not filled out in the prescribed form (mandatory details are missing), they will refuse to confirm the zero VAT rate applied for exports, and this refusal will need to be appealed.

When selling goods in Russia, indicating the product code according to the Commodity Nomenclature of Foreign Economic Activity is not required. Therefore, failure to fill out column 1a in the invoice (Invoice) issued for sales in Russia does not entail tax risks.

Rationale

How to use the universal transfer (adjustment) document (UDD and UCD)

Filling out universal documents

How to fill out the UPD

UPD

If the organization decides to replace both the invoice and the primary document with the UPD form, then it needs to be assigned status 1. In this case, all the details must be filled in in the UPD. After all, the UPD contains mandatory details for all primary documents (Article 9 of the Law of December 6, 2011 No. 402-FZ) and for the invoice (Clause 5 of Article 169 of the Tax Code of the Russian Federation).

If you use the UPD form only as a primary document, that is, you mark status 2 in it, it is not necessary to fill out all the details. You can leave blank lines that are required only for the invoice.

Fill out that part of the UPD that completely duplicates the invoice according to the rules established for issuing invoices. That is, in accordance with the requirements of paragraphs 5 and 6 of Article 169 of the Tax Code of the Russian Federation and Appendix 1 to Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

Fill out the details of the UPD, which duplicate the details of the consignment note and the commodity section of the consignment note, according to the rules established for the preparation of these documents.

It should be noted that the UPD form, unlike the invoice, has the requisite “MP.” However, it is not mandatory. Therefore, if there is no stamp on the document, the buyer (customer) will still be able to accept the UTD as the basis for deducting VAT and confirming income tax expenses.

At the same time, having affixed the seal, the seller (executor) will be able not to fill out line 14 “Name of the economic entity - the document preparer (including the commission agent/agent)”, and the buyer (customer) – line 19 “Name of the economic entity - the originator document."

This is provided that the print contains information about the full name of the organization that compiled the document.

Detailed recommendations for filling out individual UPD details are given in Appendices 3 and 4 to the letter of the Federal Tax Service of Russia dated October 21, 2013 No. ММВ-20-3/96.

How to issue an invoice for a buyer

What invoice details must be filled in?

Here is a complete list of details that must be filled in in the invoice for goods shipped, services provided, work performed or property rights transferred:

1. serial number and date of compilation;

2.

name, address and identification numbers of the seller and buyer or contractor and customer;

3. name and address of the shipper and consignee - only for shipped goods;

4. number of the payment order or other payment and settlement document - if payment took place before shipment;

5. the name of the goods shipped or a description of the work performed, services provided and property rights transferred, their units of measurement, when they can be determined;

6. the quantity of goods shipped or the volume of work performed and services provided in the specified units of measurement, when they can be determined;

7. name of currency;

8. identifier of the government contract, contract (agreement) (if any) – for deliveries under government orders;

9. price per unit of measurement, if it is possible to indicate it, under the contract excluding tax. In case of application of state regulated prices - taking into account the amount of tax;

10. cost of goods shipped, work performed, services provided, transferred property rights without tax;

11. amount of excise tax on excisable goods;

12. tax rate;

13. the amount of tax based on current tax rates;

14. the cost of the total quantity of goods supplied (shipped) according to the invoice (work performed, services rendered), transferred property rights, taking into account the amount of tax;

15. country of origin of the goods - only for imported goods;

16. registration number of the customs declaration - only for imported goods;

17. code of the type of goods according to the Commodity Nomenclature of Foreign Economic Activity of the EAEU - when exporting goods to the countries of the Eurasian Economic Union.

This follows from the provisions of paragraphs 5 and 6 of Article 169 of the Tax Code of the Russian Federation.

Name and code of goods, works, services

In which column of the invoice should the name and code of the type of goods or description of works, services and transferred property rights be indicated?

In column 1, indicate the name of the product or a description of the work performed, services provided, and property rights. This procedure is provided for invoices that are issued upon shipment or upon receipt of an advance payment. This is stated in subparagraph “a” of paragraph 2 of section II of Appendix 1 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

When exporting goods to the countries of the Eurasian Economic Union, in column 1 (a) of the invoice, indicate the code of the type of goods according to the EAEU HS. This is stated in subparagraph “a(1)” of paragraph 2 of section II of Appendix 1 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

How to pay VAT when exporting to countries participating in the Customs Union

VAT rate

What is the VAT rate for exports to the countries of the Customs Union

When exporting goods to countries participating in the Customs Union, charge VAT at a rate of 0 percent.

A Russian organization can sell goods through its branches, which are located on the territory of member states of the Customs Union. In this case, she is also entitled to a zero VAT rate.

At the same time, the exporting organization must confirm its right to a zero tax rate.

This is stated in paragraph 3 of Appendix 18 to the Treaty on the Eurasian Economic Union. Similar clarifications are contained in letters of the Ministry of Finance of Russia dated March 20, 2015 No. 03-07-13/1/15445 and dated March 17, 2015 No. 03-07-13/1/14229.

This procedure applies regardless of whether the import of exported goods into the territory of a country that is a member of the Customs Union is subject to VAT or not.

How to justify a zero rate

How to justify a zero VAT rate when exporting to the countries of the Customs Union

To justify the application of a zero VAT rate when exporting goods to countries participating in the Customs Union, a Russian organization must:

1. collect a package of documents confirming the fact of export to the countries participating in the Customs Union;

2.

fill out a VAT return;

3. submit a package of supporting documents and a declaration to the tax office.

What documents to collect

The package of documents confirming the fact of export to the countries participating in the Customs Union includes:

1. agreement on the basis of which the Russian seller exported goods (purchase and sale agreement, leasing, trade credit, agreements for the manufacture of goods or for the processing of customer-supplied raw materials);

2.

application from the buyer (exception - export in a free customs zone or customs warehouse) with a note from the tax inspectorate of the importing country about the import of exported goods and payment of indirect taxes, or that the import of such goods is not subject to VAT (letter from the Ministry of Finance of Russia dated April 16, 2014 No. 03-07-RZ/17338). The application can be submitted either in paper form (in four copies) or electronically with an enhanced qualified electronic signature. If the application is received from the buyer electronically, then it must also contain a message about the marking by the tax office of the importing country. In this case, a paper application is not required (letter of the Federal Tax Service of Russia dated July 1, 2015 No. ZN-4-17/11507). If information about applications is received by the tax office within the framework of certain international interdepartmental agreements, information about them must be included in the list of applications;

3. copy of the customs declaration (when exporting under the free customs zone or customs warehouse regime). In this case, the buyer’s application for the import of goods is not submitted;

4.transport and (or) shipping documents confirming the movement of goods from the territory of Russia to the territory of another country - a member of the Customs Union (if the preparation of such documents is provided for by national legislation);

5. other documents confirming the validity of applying the zero VAT rate (for example, intermediary agreements, if a Russian organization exports goods through an intermediary (clause 2 of Article 165 of the Tax Code of the Russian Federation)).

This follows from the provisions of paragraph 4 of Annex 18 to the Treaty on the Eurasian Economic Union.

How inspectors will check the fact of export

Having received a package of documents from the exporter along with a tax return, inspectors conduct a desk audit. Based on the results of such a check, they make one of the following decisions:

1. confirm the fact of export and reimburse (offset) the amount of input VAT on goods (work, services) used to sell goods for export;

2.

do not confirm the fact of export, that is, refuse a zero rate and charge a tax on sales at a rate of 18 or 10 percent.

When the inspection refuses VAT refund when exporting to the countries of the Customs Union

Inspectors may not confirm the fact of export if the information submitted by the organization does not match those available to the inspectorate.

We are talking about information about the movement of goods and the payment of indirect taxes, which is received by the Russian tax office from the inspectorate of another country to which the goods were exported.

When there are discrepancies, inspectors will charge VAT at the usual rates - 10 or 18 percent. This procedure is provided for in paragraph 8 of Appendix 18 to the Treaty on the Eurasian Economic Union.

Alexander Sorokin answers,

Deputy Head of the Operational Control Department of the Federal Tax Service of Russia

“Cash payment systems should be used only in cases where the seller provides the buyer, including its employees, with a deferment or installment plan for payment for its goods, work, and services.

It is these cases, according to the Federal Tax Service, that relate to the provision and repayment of a loan to pay for goods, work, and services.

If an organization issues a cash loan, receives a repayment of such a loan, or itself receives and repays a loan, do not use the cash register. When exactly you need to punch a check, look at the recommendations.”

From the recommendation: Is it necessary to use cash register when issuing, receiving and repaying a loan?

Ask your question to the experts of the Glavbukh System

Returning goods in 2021: new rules

Source: https://www.glavbukh.ru/hl/222219