Check

A business trip is required to resolve pressing issues for the employer’s company.

When sending an employee on a trip, the company reimburses him for expenses, including accommodation. Often the most convenient option for an employee is a hotel located close to the business trip. At the end of the client’s stay, the hotel issues reporting documents for business travelers to confirm the fact of their stay at the hotel on certain days. Letter of the Ministry of Finance of the Russian Federation dated February 25, 2015 No. 03-07-11/9440 indicates that if the hotel does not use cash register payment, the accommodating party is obliged to draw up a strict reporting form, which is developed independently. It is allowed to call the form by different names, such as a voucher or a hotel check.

Upon returning from a business trip, you must provide documents issued by the hotel to the accounting department, which confirm your accommodation there. A cash receipt is required for the advance report. The basic requirements for the form provided by the hotel enterprise are as follows:

- The strict reporting form must contain the following details: name of the document, six-digit number and series of the document, full name of the organization providing the services, address, TIN of the organization and seal.

- It is necessary that the strict reporting form be produced using a printing method or generated using automated systems. System requirements: mandatory protection from unauthorized access, identification and preservation of the number and series of the form for at least 5 years (Resolution of the Government of the Russian Federation of May 6, 2008 No. 359). Forms printed on a computer without the use of automated systems will not be accepted by the organization as confirmation.

Payment for accommodation on a business trip in a budgetary organization and in a commercial one is equally made on the basis of a hotel invoice or an invoice and a cash receipt.

IMPORTANT!

If a seconded employee provides his organization with a document on hotel accommodation that does not meet the specified requirements, and the organization takes expenses into account in tax reporting, the Federal Tax Service will have claims. In this case, the company defends the costs through the court. To do this, we recommend that you read the Resolution of the Federal Antimonopoly Service of the North-Western District dated November 1, 2010 in case No. A52-3413/2009.

If a hotel-type enterprise uses cash registers, the reporting includes a check and invoice or other documentation of the employee’s stay at the hotel.

Types of settlements with hotel clients. Strict reporting forms

For payments by bank transfer, traveler's and personal checks can also be used.

For reference, it should be noted that recently in Russia this type of payment has begun to be used, such as payment by plastic card, but for these purposes the hotel must be equipped with a special electronic terminal. It is no secret that not every enterprise can yet afford such expensive equipment, and therefore, for the most part, in our country, cash payments still come first.

Therefore, we must not forget about the requirements of the Federal Law of May 22, 2003, which came into force. No. 54-FZ “On the use of cash register equipment when making cash payments and (or) payments using payment cards.”

In accordance with paragraph 1 of Article 2 and Article 5 of this law, organizations when making cash payments are required to use cash register equipment (CCT) and issue cash register receipts printed by cash register equipment to buyers (clients) when making such payments at the time of payment. For the purposes of this Law, cash payments mean payments made using cash for goods purchased, work performed, and services rendered.

However, paragraph 2 of Article 2 of this law establishes that*

* Organizations and individual entrepreneurs, in accordance with the procedure determined by the Government of the Russian Federation, can carry out cash payments and (or) payments using payment cards without the use of cash register equipment in the case of providing services to the population, provided that they issue the appropriate strict reporting forms.

The procedure for approving the form of strict reporting forms equated to cash receipts, as well as the procedure for their recording, storage and destruction, is established by the Government of the Russian Federation.*

Since hotel activity is a process of providing a service, when working with individuals (citizens), it can use strict reporting forms approved by the Order of the Ministry of Finance of the Russian Federation dated December 13, 1993. No. 121.

Note!

Federal Law No. 54-FZ allows the use of strict reporting forms when organizations and individual entrepreneurs provide services to the population. For legal entities, the Law on CCP does not establish calculations using strict reporting forms. Therefore, if an organization enters into an agreement for the provision of services with a legal entity and payment is made in cash, the presence of a cash register is mandatory.

Considering the primary documents that hotels use when providing services, it is no coincidence that we drew the reader’s attention to the fact that some of them are strict reporting forms (SSR). The hotel accountant should properly organize the accounting and storage of such forms.

The procedure for using strict reporting forms of approved forms and the types of activities for which the use of such forms is permitted will have to be approved by the Government of the Russian Federation.

Until the new strict reporting forms are put into effect, the current ones approved by the Russian Ministry of Finance can be used.

Forms must be produced only by typographical method with the obligatory indication of the output typographical data.

Strict reporting forms are developed and approved by the Ministry of Finance of the Russian Federation. General requirements for BSO and the procedure for their registration are given in the Letter of the Ministry of Finance of the Russian Federation dated August 23, 2001. No. 16-00-24/70 “On strict reporting documents when making monetary settlements with the population.”

The strict reporting form must, along with indicators characterizing the specifics of the transactions being processed, contain the following mandatory details:

- approval stamp, name of the document form;

- six-digit number;

- series;

- form code according to the All-Russian Classifier of Management Documentation (OKUD);

- date of settlement;

- name and code of the organization according to the All-Russian Classifier of Enterprises and Organizations (OKPO);

- TIN code;

- type of work (services) provided;

- units of measurement of services provided (in kind and in monetary terms);

- the name of the position of the person responsible for carrying out the business transaction and the correctness of its execution with a personal signature.

Each form is numbered in a typographical manner, and if it was accidentally damaged when making a cash payment, it should be saved and crossed out.

A form with all required details filled in, signed by an official, acquires legal force and is the primary accounting document. Strict reporting forms are equivalent to a cash register receipt.

In accordance with the “Regulations on documents and document flow in accounting”, approved by the USSR Ministry of Finance on July 29, 1983. No. 105, forms of primary documents classified as strict reporting forms must be numbered in the order established by ministries and departments by numerator or typographic method.

Strict reporting forms, like other primary accounting documents, in accordance with Federal Law of November 21, 1996 No. 129-FZ “On Accounting” must contain the following mandatory details:

- Title of the document;

- date of document preparation;

- name of the organization on behalf of which the document was drawn up;

- content of a business transaction;

- measuring business transactions in physical and monetary terms;

- the names of the positions of the persons responsible for the execution of the business transaction and the correctness of its execution;

- personal signatures of these persons;

The check or insert (backing document) issued to buyers (clients) must contain the following details:

- Title of the document;

- date of document preparation;

- name of the organization on behalf of which the document was drawn up;

- content of a business transaction;

- measuring business transactions in physical and monetary terms;

- the names of the positions of the persons responsible for the execution of the business transaction and the correctness of its execution;

- personal signatures of these persons.

In addition, in addition to indicators characterizing the specifics of the transactions being processed, the following must be indicated in the form of strict reporting forms:

- approval stamp of the form;

- code of the form according to the All-Russian Classifier of Management Documentation (OKUD);

- name and code of the organization according to the All-Russian Classifier of Enterprises and Organizations (OKPO);

- TIN of the organization.

An integral requisite is the presence on each copy of the form of its serial number. When affixing a number, some of the characters can be alphabetic (series), and some can be digital.

Strict reporting forms for carrying out monetary settlements with the population without the use of cash registers are produced in printing houses according to orders (available samples approved by the Ministry of Finance of Russia) of ministries and departments, as well as the organizations themselves.

Note!

Computer (independent production using existing computer equipment) production of strict reporting forms is unacceptable.

On February 11, 2002, the Federal Law of August 8, 2001 No. 128-FZ “On licensing of certain types of activities” came into force, introducing significant changes to the “old” version of the law on licensing. Previously, it was legislatively approved that a license was required to carry out printing activities. This meant that the production of strict reporting forms by printing, which are printed products, was subject to mandatory licensing. The new Federal Law has significantly reduced the list of activities for which licenses are required.

According to Article 17 of Law No. 128-FZ, a license is required to carry out activities for the production of counterfeit-proof printed products, including forms of securities, as well as trade in these products.

This means that strict reporting forms with security elements must be produced by printing enterprises that have the appropriate license issued by the federal executive body (in this case, the Ministry of Finance of Russia). Consequently, from February 11, 2002, printing activities for the production of strict reporting forms (not protected against counterfeiting) and activities for trading in these forms are not subject to licensing.

SINCE STRICT REPORTING FORMS FOR HOTELS DO NOT HAVE PROTECTION, CONSEQUENTLY, A LICENSE IS NOT REQUIRED FOR THEIR PRODUCTION AND SALE.

So, strict reporting forms must be published in printing. When producing BSO, the series is assigned to them by the organization independently when submitting an order for the production of forms to the printing house. The number of a specific form within the corresponding series is assigned by the printing house.

Recently, taxpayers have been concerned about the question of whether strict reporting forms need to be registered with local tax authorities?

The answer is simple, there is no need to do this, since the current Russian legislation does not provide for such an obligation. Therefore, the corresponding demands of local tax inspectorates are unfounded and illegal.

In addition, those who work with BSO are probably concerned about how to properly store, record and destroy these documents. Today, there are no such rules, so we can only recommend that taxpayers use the “Regulations on Documents and Document Flow in Accounting” (approved by the USSR Ministry of Finance on July 29, 1983 N 105 in agreement with the USSR Central Statistical Office) to the extent that does not contradict current Russian legislation.

Accounting and tax accounting of strict reporting forms.

The costs of acquiring BSO are classified as expenses associated with the provision of services.

In accounting, these expenses are reflected in accordance with the Accounting Regulations “Expenses of the Organization” PBU 10/99, approved by Order of the Ministry of Finance of Russia dated May 6, 1999 N 33n, as expenses of the organization for ordinary activities.

To summarize information about the availability and movement of BSO that are in storage and issued for reporting, the Chart of Accounts provides off-balance sheet account 006 “Strict reporting forms.”

The acquisition of BSO (including by accountable persons) is reflected in the debit of account 006 in a conditional valuation (for example, 1 ruble), write-off - in the credit of account 006 on the basis of relevant documents on their use, etc. Analytical accounting is maintained for each type of BSO and their storage locations.

When acquiring BSO, the following entries are made in accounting:

Debit 26 “General business expenses” Credit 60 (71, 76) - purchased by BSO at actual cost;

Debit 006 “Strict reporting forms” - capitalized by BSO for storage;

Debit 19 “Value added tax on purchased material assets” Credit 60 “Settlements with suppliers and contractors” - VAT on purchased BSO is taken into account;

Debit 60 “Settlements with suppliers and contractors” Credit 51 “Current account” - the debt to the supplier for the purchased BSO is repaid;

Debit 68 “Calculations for taxes and fees” subaccount “VAT” Credit 19 “Value added tax on acquired material assets” - VAT is reimbursed to the budget;

Credit 006 “Strict reporting forms” - used SSBs are written off.

The organization's expenses for the acquisition of BSO reduce the tax base for the organization's profit tax in accordance with paragraph 24, paragraph 1, article 264 of the Tax Code of the Russian Federation. Moreover, the amounts spent on the acquisition of BSO must be expensed immediately, and not as they are used in the course of business activities.

As for individual entrepreneurs, in accordance with clause 1 of Article 221 of the Tax Code of the Russian Federation, they have the right to a professional tax deduction in the amount of expenses incurred for the purchase of BSO.

Responsibility for non-use of BSO.

In Article 14.5. The Code of Administrative Offenses of the Russian Federation provides for administrative responsibility for the provision of services by organizations, as well as citizens registered as individual entrepreneurs, without the use of cash registers in cases established by law.

The punishment for this offense is an administrative fine in the amount of:

- for citizens - from 15 to 20 minimum wages;

- for officials - from 30 to 40 minimum wages;

- for legal entities - from 300 to 400 minimum wages.

If there is no account

In the absence of supporting documents, payment for hotel accommodation on a business trip is made on the basis of a request to a hotel-type enterprise to confirm the fact of the employee’s residence during the specified period of time and obtain a certificate.

In Moscow, a request is allowed to confirm an employee’s expenses, which is confirmed by Letter of the Federal Tax Service for Moscow and the Moscow Region dated August 26, 2014 No. 16-15/084374. The certificate must contain details of the services provided and confirmation of payment. The company must have other documentation confirming the employee's business trip, in particular, a business trip order, travel documents, etc.

Based on a certificate received upon request, payment for a hotel on a business trip is not always accepted by the tax authorities. Clause 1 Art. 252 of the Tax Code of the Russian Federation allows for indirect confirmation of expenses to be taken into account, so the company has the opportunity to appeal the decision of the tax authorities.

Decree of the Government of the Russian Federation 1085 dated October 09, 2015 approved new Rules for the provision of hotel services. This Decree indicates the obligation to issue a strict reporting form or check.

Also, there are no documents on hotel accommodation if the company rents residential premises to accommodate employees during a business trip. Then payment for the premises is made by the employer himself, so payment of expenses and reporting documents for living in an apartment on a daily basis are not provided.

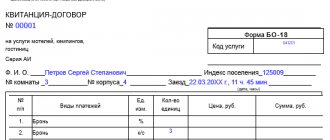

for free. Form No. 3-G. Check

Hotel account form NN 3-G, 3-GM (form) - is a strict reporting form. To be filled in when making payment for a reservation, accommodation, as well as for additional paid hotel services. The invoice is issued in three copies: the first is issued to the client (resident), the second is submitted to the accounting department, the third is stored until the guest leaves in the checkout area of the hotel in a special file cabinet. With the mechanized method of conducting payments, the invoice is filled out in 2 copies. It records payment for the entire period of stay. Both copies are stored in the control file until the guest leaves.

Form 3-d is indeed approved and is a BSO, but previously there was a list of organizations that had the right to work without a cash register. This list included hotels. Now they are not there. And today, almost all hotels issue the client both a cash register receipt and an invoice in form 3-g. In this situation, account 3-g is simply a transcript of the cash register receipt, with a detailed description of the services provided. Those. he lost his BSO function.

On the other hand, formally, he is a BSO - it seems that no one has canceled this. Therefore, if the employee brought only invoice 3-d, then it seems that it can be attributed to expenses. Another thing is that the hotel did not have the right to issue only the 3rd and not issue a KKM check.

By the way, the court believes that any document that contains the necessary details will do to confirm expenses. That is, the paper needs to indicate the name of the hotel, the cost of living, a signature and date (clause 2 of article 9 of the law of November 21, 1996 No. 129-FZ; clause 8 of the Rules for the provision of hotel services in the Russian Federation, approved Government Decree of April 25, 1997 No. 490). However, such a document does not necessarily have to be a strict reporting form.

Is it possible to include breakfast on the bill?

If breakfast costs are indicated as a separate item on the invoice, it is not recommended to include them in reporting documents for hotel stays. Subclause 12, clause 1, art. 264 of the Tax Code of the Russian Federation indicates that accommodation costs include additional services, with the exception of service in bars and restaurants, in the room, and use of recreational and health facilities.

Letter of the Ministry of Finance dated October 14, 2009 No. 03-04-06-01/263 explains that if the cost of food is allocated as a separate item, the employee receives income in kind. According to the Ministry of Finance, compensation for food does not apply to reimbursement of living expenses, therefore it is subject to personal income tax and insurance payments.

If breakfast is not listed as a separate item on your hotel bill, including it as an expense is fraught with tax risks. This situation has conflicting judicial precedents, so the tax authorities charge personal income tax on the specified amount. Then insurance premiums are not charged, as indicated by Letters of the Ministry of Health and Social Development of the Russian Federation dated 05.08.2010 No. 2519-19, FSS of the Russian Federation dated 17.11.2011 No. 14-03-11/08-13985.

Spending limits

The company has the right to set a limit on expenses for its posted employee. Note that payment for accommodation on a business trip for a budget organization differs from payment in commercial companies only in that the source of funding is indicated in the travel order. It is not always possible to meet the specified amount, so a situation arises when an employee exceeds the limit of the allocated amount. In this case, if the employee exceeds the limit and provides an invoice from the hotel for the full cost of expenses, personal income tax is not withheld from him (paragraph 10, clause 3, article 217 of the Tax Code of the Russian Federation).