Organizations and individual entrepreneurs, acting as tax agents, are required to withhold and pay personal income tax on income paid to each of their employees.

Whether your employees work under an employment contract or individuals under a GPC (civil law) agreement does not matter, personal income tax is withheld from payments to both.

In some cases, income is exempt from personal income tax, for example, gifts and material assistance up to 4,000 rubles, payments to individual entrepreneurs, compensation payments, maternity benefits, etc. (Article 217 of the Tax Code of the Russian Federation).

Calculation and payment of personal income tax

ATTENTION: from January 1, 2021, tax agents are required to transfer calculated and withheld personal income tax no later than the day following the day the income is paid to the taxpayer. Now this is a single rule for all forms of income payments (clause 6 of Article 226 of the Tax Code of the Russian Federation).

And personal income tax withheld from sick leave (including benefits for caring for a sick child) and vacation benefits must be transferred to the budget no later than the last day of the month in which they were paid.

IMPORTANT: There is no need to pay personal income tax on the advance payment.

Calculated using the formula:

Personal income tax = (employee’s monthly income – tax deductions) * 13%

- Tax deductions are an amount that reduces the income on which personal income tax is charged.

- The tax rate on payments to foreign employees is 30%.

- For organizations, dividends paid are also subject to personal income tax at a rate of 13% (since 2015).

Where to pay income tax:

Personal income tax is paid to the tax office with which the employer is registered. On the website of the Federal Tax Service of Russia there is an online service “Determining the details of the Federal Tax Service”, which will help you find out the necessary details.

KBK (code corresponding to a specific type of payment), which is indicated in the payment order, for personal income tax payment in 2021 - 182 1 0100 110.

At what rate should personal income tax be calculated?

In the vast majority of cases, the employer deals with a rate of 13% of the Tax Code of the Russian Federation, Article 224. Tax rates.

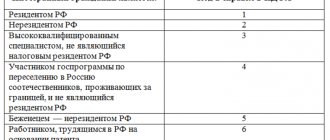

30% should be collected from non-residents, that is, from those who spent 183 days or more abroad during the year. But there is an exception here too. It applies to foreigners working under a patent, highly qualified specialists who arrived to work under a contract, those who moved to Russia under the resettlement program for compatriots, crew members of Russian ships, refugees and persons granted temporary asylum, as well as residents of the countries of the Eurasian Economic Union: Armenia , Belarus, Kazakhstan and Kyrgyzstan. A rate of 13% is also applied to the income of such people.

Tax paid early

According to the law, personal income tax must be withheld upon actual payment of income to employees (clause 4 of article 226 of the Tax Code of the Russian Federation). And then transfer it to the budget.

And if you decide to pay personal income tax FROM YOUR OWN FUNDS ahead of time before paying your salary, then this is already a violation (clause 9 of Article 226 of the Tax Code of the Russian Federation), and the transferred amount will not be considered tax paid. That is, such payments cannot be offset “against future accrued personal income tax.”

And then you will have to pay personal income tax again, only according to the rules - when issuing your salary. If this is not done, a fine will be charged - 20% of the untransferred amount (Article 123 of the Tax Code of the Russian Federation), as well as penalties.

That first, early paid amount is positioned as erroneously transferred. It can be returned by writing an application to the Federal Tax Service.

Features of taxation

According to personal income tax for individual entrepreneurs on UTII in 2021:

- if a businessman conducts an activity that does not fall under the single tax, but indicated it in the Unified State Register of Individual Entrepreneurs, then he is not exempt from drawing up the corresponding declaration;

- if the work is carried out only on the main activity, then the individual entrepreneur is not considered a taxpayer in terms of profit and is not required to submit declarations;

- if there are employees on staff, then he must withhold income tax of 13% from employees and submit reporting forms in accordance with the regulations established by the Tax Code of the Russian Federation.

According to OSNO, entrepreneurs must be guided by the norms of Chapter 23 of the Tax Code of the Russian Federation and pay in advance payments up to:

- July 15;

- October 15;

- January 15, 2021 (for the 4th quarter of 2021).

The tax office makes the calculation (including deductions) and sends a notification about the timing and amount of the advance payment. After which the IP must complete them. If such notification is not received, the entrepreneur is not obliged to calculate the amount of tax himself. To avoid late fees, it is better to call the Federal Tax Service and ask for a duplicate document.

When you are an entrepreneur or have just started filling out documents for an individual entrepreneur, it is very important to visit the tax office at your place of registration and place of residence in order to write down exactly who you need to report to, where to transfer taxes, and what documents to submit. Because the law allows for some local changes, there may be slight differences in requirements by region.

Memo on transactions with personal income tax

| Calculation of personal income tax | Tax amounts are calculated by tax agents on the date of actual receipt of income, determined in accordance with Article 223 of this Code, on an accrual basis from the beginning of the tax period (clause 3 of Article 226 of the Tax Code of the Russian Federation). |

| Date of actual receipt of income | Clause 2 of Art. 223 of the Code establishes that when receiving income in the form of wages, the date of actual receipt by the taxpayer of such income is the last day of the month for which he was accrued income for work duties performed in accordance with the employment agreement (contract). |

| Personal income tax withholding date | Tax agents, according to clause 4 of Art. 226 of the Code are required to withhold the accrued amount of tax directly from the taxpayer’s income upon actual payment. As for the payment of income in kind and in the form of material benefits, personal income tax must be withheld from any income that was paid to a given individual in cash (but not more than 50% of this amount). |

| Date of personal income tax transfer | From January 1, 2021, tax agents are required to transfer calculated and withheld personal income tax no later than the day following the day of payment of income to the taxpayer (clause 6 of Article 226 of the Tax Code of the Russian Federation).

|

How personal income tax is paid for employees

All these deductions can be obtained in person by contacting the tax office at the end of the year, or from the employer based on a notification from the tax office. As for the child deduction, the employee simply needs to write a statement to the employer stating that he wants to receive such a deduction. And the employer is obliged to provide it. Individual entrepreneurs who want to hire an employee are interested in the question of who pays personal income tax: individual entrepreneurs for employees or directly the citizens themselves to the Federal Tax Service? Every officially working citizen of the Russian Federation knows that he is obliged to pay the state personal income tax on wages. At the same time, no one goes to submit returns to the tax service. The responsibility to calculate and pay income tax rests with employers. This was done to reduce the workload at the Federal Tax Service when working with citizen taxpayers.

Please note => What is considered living space in a private house

Tax agent reporting

1) Calculation of 6-NDFL.

On January 1, 2021, Law No. 113-FZ of 05/02/2015 came into force, according to which every employer must submit personal income tax reports quarterly. That is, you need to report no later than the last day of the month following the reporting quarter.

• View a sample of filling out 6-NDFL.

• Read more: Quarterly personal income tax reporting 2021.

2) Certificate 2-NDFL.

It is compiled (based on data in tax registers) for each of its employees and submitted to the tax office once a year no later than April 1, and if it is impossible to withhold personal income tax - before March 1.

ATTENTION: by order of the Federal Tax Service of Russia No. ММВ-7-11/ [email protected] dated October 30, 2015, a new form 2-NDFL was approved. It is valid from December 8, 2015.

How to submit a 2-NDFL certificate:

- On paper - if the number of employees who received income is less than 25 people (from 2021). You can bring it to the tax office in person or send it by registered mail. With this method of reporting, tax officials must draw up in 2 copies a “Protocol for accepting information on the income of individuals for ____ year on paper,” which serves as proof of the fact that 2-NDFL certificates were submitted and that they were accepted from you. The second copy remains with you, do not lose it.

- In electronic form on a flash drive or via the Internet (number of employees more than 25 people). In this case, one file should not contain more than 3,000 documents. If there are more of them, then you need to generate several files. When sending 2-NDFL certificates via the Internet, the tax office must notify you of their receipt within 24 hours. After this, within 10 days the Federal Tax Service will send you a “Protocol for receiving information on the income of individuals.”

Also, together with the 2-NDFL certificate, regardless of the method of submission, a document is attached in 2 copies - Register of information on the income of individuals.

• Download the 2-NDFL certificate form.

• See Instructions for filling out 2-NDFL.

3) Tax accounting register.

Designed for personal data recording for each employee, including individuals under a GPC agreement. Based on this accounting, a 2-NDFL certificate is compiled annually.

Tax registers record income paid to individuals for the year, the amount of tax deductions provided, as well as the amount of personal income tax withheld and paid.

There is no single sample tax register for personal income tax. You must create the form yourself. For this purpose, you can use accounting programs or draw up a personal income tax-1 certificate based on the currently inactive personal income tax certificate.

But the Tax Code defines the mandatory details that must be in personal income tax registers:

- Information allowing identification of the taxpayer (TIN, full name, details of the identity document, citizenship, address of residence in the Russian Federation)

- Type of income paid (code)

- Type and amount of tax deductions provided

- Amounts of income and dates of their payment

- Taxpayer status (resident / non-resident of the Russian Federation)

- Date of tax withholding and payment, as well as details of the payment document

Where to pay and report personal income tax

A tax agent using centralized registration can contact the Russian Ministry of Finance or the Federal Tax Service of Russia for clarification of tax legislation. This must be done in writing, outlining the problem in detail, and, if necessary, attach documents related to the question being asked to the request. In the letter, it is advisable to provide arguments confirming the possibility for the tax agent in this case to report on personal income tax in the old manner - that is, according to the general rule for all separate divisions at the place of registration of the selected one. Submitting a 2-NDFL certificate and a 6-NDFL calculation at the location of each separate division forces the organization to register with the tax office at each such location and violates its right to choose one place of registration under clause 4 of Art. 83 of the Tax Code of the Russian Federation. II . Submission of personal income tax reporting Submitting personal income tax reporting (certificate in form 2-NDFL, calculation in form 6-NDFL) must be submitted to the tax office at the place of registration of the tax agent. It was established that:

- organizations that have separate divisions report, including at the place of their registration (taking into account a number of features);

- the largest taxpayers can submit reports to the inspectorate at the place of their registration or at the place of registration of the corresponding separate divisions (separately for each);

- individual entrepreneurs who are registered at the place of conduct of activity in connection with the use of UTII and (or) PSN - at the place of conduct of such activity.

Please note => Write-off of a mortgage in Sberbank upon the birth of a child

In relation to the income of a citizen working under a civil contract, reporting forms (certificate in form 2-NDFL and calculation of 6-NDFL) must be submitted at the place of registration of the separate unit with which this agreement was concluded. Confirmation: clause 2 of Art. 230 of the Tax Code of the Russian Federation. Presentation order:

- certificates in form 2-NDFL (depending on the method of its submission) approved by Order of the Federal Tax Service of Russia No. ММВ-7-3/576 dated September 16, 2011;

- calculation of 6-NDFL was approved by Order of the Federal Tax Service of Russia No. ММВ-7-11/450 dated October 14, 2015.

This procedure for submitting reporting forms also applies to amounts of income from which tax is not withheld, and amounts of tax not withheld by the tax agent (clause 5 of Article 226, clause 2 of Article 230 of the Tax Code of the Russian Federation). Tax agent - an organization with separate divisions or the largest taxpayer At the place of registration of separate divisions, you must report (Clause 2 of Article 230 of the Tax Code of the Russian Federation):

- in relation to employees of these separate divisions;

- in relation to citizens working under civil contracts concluded by such separate units.

Moreover, when applying this procedure, it does not matter whether the separate division has a separate balance sheet and bank account. Confirmation: letter of the Federal Tax Service of Russia No. BS-4-11/23300 dated December 30, 2015. If an employee combines the performance of his job duties in an organization with part-time work in a separate unit, then the reporting forms must be submitted separately:

- to the inspectorate at the place of registration of the head office of the organization - for income received for work in the head office of the organization;

- to the inspectorate at the place of registration of the separate unit - for income received for part-time work in the separate unit.

Confirmation: para. 3 p. 2 art. 230 of the Tax Code of the Russian Federation. If an organization belongs to the category of largest taxpayers, then it has the right to independently choose which tax office to submit reporting forms to:

- at the place of its registration as the largest taxpayer;

- or at the place of registration of a separate subdivision.

Confirmation: para. 4-5 p. 2 tbsp. 230 of the Tax Code of the Russian Federation. Providing a tax agent classified as a major taxpayer with such a right to choose does not provide for the possibility of simultaneously submitting reporting forms to tax inspectorates at two places of registration. This procedure does not depend on whether payments are made by an organization or a separate division. Confirmation: letter of the Federal Tax Service of Russia No. BS-4-11/1395 dated February 1, 2021. Features of reporting exist when using a centralized registration organization

.

If a tax agent has several separate divisions that are located in the same municipality (in the same city - for the federal cities of Moscow, St. Petersburg and Sevastopol), but on the territory of different tax inspectorates, then you can register at the location of one of the separate divisions, which the organization determines independently (centralized registration).

Confirmation: clause 4 of Art. 83 of the Tax Code of the Russian Federation. With regard to the presentation of personal income tax reporting with such centralized registration, no single point of view has been developed. Formally, based on the norms of paragraph 2 of Art. 230 of the Tax Code of the Russian Federation, a certificate in form 2-NDFL and calculation in form 6-NDFL must be submitted at the place of registration (and not location) of each separate division. Thus, if an organization has several separate divisions that are located in the same municipality (in the same city - for the federal cities of Moscow, St. Petersburg and Sevastopol), but in territories under the jurisdiction of different tax inspectorates, then reporting forms regarding employee income these units, as well as citizens working under civil contracts, can be represented at the place of registration of one separate unit, chosen by it independently. Similar explanations were given by regulatory agencies before, taking into account the features provided for organizations with separate divisions on the territory of different municipal districts in Moscow. Such organizations, due to the need to pay personal income tax at the location of each separate division, had to fulfill the obligation to submit reports in a similar manner. Please note => It is necessary to justify the refusal of the income approach when assessing real estate

Fines in 2021

1) For each 2-NDFL certificate not submitted on time - a fine of 200 rubles.

1) Violation of the deadlines for filing 6-NDFL - a fine of 1,000 rubles. for each full or partial month. delays.

2) After 10 days of delay in reporting on the calculation of 6-NDFL, the tax inspectorate has the right to suspend transactions on bank accounts and electronic money transfers.

3) For providing false information - a fine of 500 rubles (1 document). But if you independently discover and correct errors in the document in a timely manner before the tax office does, then this fine will not affect you.

What are the requirements for an individual entrepreneur?

It should be noted that this must be legal. Timely registration and payment of the required fees eliminates the possibility of fines and penalties.

Patent tax system for individual entrepreneurs - what is it and how does it work

There are no special requirements for entrepreneurs using the simplified tax system, OSNO and unified agricultural tax. Their main responsibility is to timely contribute the necessary funds to the budget of their locality.

UTII payers are required to contact the Federal Tax Service department. UTII in this department will accept transfers of material assets. In the case where such individual entrepreneurs are registered with the simplified tax system at their place of residence, tax payment data are made at the regional branch of the Federal Tax Service. In this city, the company undertakes a zero declaration.

Conditions for doing business exist for PSN payers. Applications required:

- about registration;

- to obtain a patent.

Important! A patent is valid only in the territory in which it is issued.