What benefits on insurance premiums are available to companies and individual entrepreneurs using the simplified tax system in 2021?

By a benefit on insurance premiums when paying taxes under the simplified tax system, it is legitimate to understand the opportunity to pay insurance premiums in a smaller amount (at reduced rates). At the same time, there is a very wide range of grounds on which these rates are applied, as well as criteria that determine the specific value of the reduced rates.

Let us consider them in more detail - in the context of the distribution of taxpayers entitled to benefits according to the categories listed in paragraph 1 of Art. 427 of the Tax Code of the Russian Federation, as well as the rates established in the same article of the code for various categories.

See also: “Is it possible to recalculate contributions if the income condition for preferential simplified taxation system activities is met mid-year?”

You can learn more about the specifics of the simplified taxation system in the article “Deadlines for payment of the simplified tax system for 2016–2017.”

Object of taxation of insurance premiums

Before we find out which payments are not subject to insurance premiums, we will determine what premiums should be charged on. According to paragraph 1 of Art. 420 of the Tax Code of the Russian Federation, insurance premiums are charged on payments for labor (salaries, bonuses, allowances and other payments in connection with labor relations) and GPC contracts for the provision of services and performance of work, also under author’s order contracts, publishing licenses and agreements on the alienation of exclusive rights to works of science, literature and art.

If there is no taxable object, there is no need to pay insurance premiums. For example, are dividends subject to insurance premiums? Since dividends are part of the company’s profit, distributed among its participants, not related to labor relations, there is no object subject to insurance contributions (letter of the Federal Insurance Service of the Russian Federation dated November 17, 2011 No. 14-03-11/08-13985).

Benefits for contributions under the simplified tax system: intellectual activity

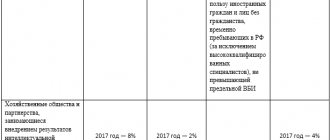

Business entities or partnerships using the simplified tax system that carry out activities in the field of intellectual development (including those related to the use of computer programs) have the opportunity to pay contributions:

- for compulsory pension insurance (MPI) - at a rate of 8% in 2017, then increasing (13% in 2018, 20% in 2019);

- for compulsory social insurance for temporary disability and maternity (OSS for VNIM) - at a rate of 2% in 2017, then, again, with an increase (2.9% - in 2018 and 2019);

- for OSS for temporary disability for foreigners - at a rate of 1.8%;

- for compulsory health insurance (CHI) - 4% in 2021, 5.1% in 2018 and 2019.

At the same time, firms must apply research results in practice (produce products based on developments), and also enter notifications about the formation of business entities and partnerships into the accounting register - quarterly in the manner prescribed by law.

Basic insurance premium rates

The basic rates of insurance premiums in 2021 are applied by all policyholders (organizations and individual entrepreneurs) who are not entitled to benefits and, accordingly, reduced rates. We will summarize the general tariffs for 2021, taking into account the new limits on the base of insurance premiums.

In 2021, the maximum base for calculating insurance premiums for compulsory pension insurance is 876,000 rubles. The maximum base for insurance premiums for temporary disability and in connection with maternity is 755,000 rubles. See “Limit value of the base for calculating insurance premiums for 2021: table.”

So, we summarize the new tariffs for most organizations and individual entrepreneurs in the table:

| Type of contributions | Tariff in 2021 |

| For compulsory pension insurance (within 876,000 rubles) | 22 % |

| For compulsory pension insurance (over 876,000 rubles) | 10 % |

| For compulsory social insurance in case of temporary disability and in connection with maternity (755,000 rubles). | 2,9% |

| For compulsory social insurance in case of temporary disability and in connection with maternity in relation to foreigners and stateless persons temporarily staying in the Russian Federation (except for highly qualified specialists) (within 755,000 rubles) | 1,8 % |

| For compulsory social insurance in case of temporary disability and in connection with maternity (over 755,000 rubles) | 0 % |

| For compulsory medical insurance (except for foreigners and stateless persons temporarily staying in the Russian Federation, as well as highly qualified specialists) | 5,1 % |

Benefits for social contributions: business in special economic zones

Firms (including those working under the simplified tax system) that have entered into agreements on technology-innovation activities with SEZ management bodies, as well as making payments to citizens working in these SEZs, have the right to pay contributions using the same rates differentiated by year that simplifiers use in field of intellectual developments.

The same applies to companies that have entered into agreements to conduct tourism and recreational activities in the SEZ and make payments to citizens working in these SEZs. The taxation system does not matter - it may be a simplification.

Contribution benefits: business in the field of information technology

Legal entities (including those on the simplified tax system) working in the field of information technology (outside the SEZ) can pay contributions (in 2017–2023):

- for OPS - at a rate of 8%;

- OSS for VNiM - at a rate of 2%;

- OSS under contracts with foreign workers - at a rate of 1.8%;

- Compulsory medical insurance - at a rate of 4%.

Moreover, if a company is classified as newly created, then it must be:

- accredited as an IT firm;

- a business that receives at least 90% of its quarterly revenue from IT activities (for example, from the sale of software);

- an employer with an average number of employees in the quarter of at least 7 employees.

If the company is not newly created, then it must meet the same criteria, but in terms of income and average headcount in relation to 9 months of the year preceding the one in which the transition to reduced contributions is made.

STS in 2021. Insurance premiums with reduced rates

When working under the simplified tax system for some types of activities in 2021, you can pay contributions at a reduced rate - 20%. The list of discount codes is given in the table below. The codes are shown from the new OKVED 2 , which has been in effect since 2021. You can see a table of comparisons of old and new in our publication - Correspondence of codes OK-029 200 1 (rev. 1) to OKVED OK 029-2014 (NACE rev. 2)

Who can pay the reduced rate?

Reduced rates of insurance premiums ( 20% instead of 30% ) can be applied to organizations and entrepreneurs under the simplified tax system , whose main type of activity is specified in Article 427 of the Tax Code of the Russian Federation (as amended by the new law on contributions to the Federal Tax Service ). Entrepreneurs can also apply a preferential tariff to payments to employees. the Pension Fund of the Russian Federation in 2021 at a rate of 20%. contributions to the Social Insurance Fund of Russia , as well as to the Federal Compulsory Medical Insurance Fund . This is established by paragraph 3.4 of Article 58 of Law No. 212-FZ . Contributions are paid until the salary in the year reaches the limit of 876,000 rubles, established by Government decree. Amounts exceeding 876,000 are not subject to contributions (including to the Pension Fund of Russia )

If you are going to pay contributions at preferential rates, you must fulfill the conditions (clauses 2 and 6 of Article 427 of the Tax Code of the Russian Federation):

- the code used in your business is presented in the table below;

- activities covered by benefits bring you at least 70% of all income;

- annual income does not exceed 79 million rubles

No. | Type of main activity | OKVED 2017 |

| 1 | Food production | Entire Section 10 “Food Production” |

| 2 | Production of mineral waters and other non-alcoholic drinks | Code 11.07 from section 11 “Beverage production” |

| 3 | Textile and clothing production | Complete sections 13 “Production of textiles” and 14 “Production of clothing” |

| 4 | Production of leather, leather goods and footwear production | Entire Section 15 “Production of leather and leather products” |

| 5 | Wood processing and production of wood products | Entire section 16 “Wood processing and production of wood products” |

| 6 | Chemical production | Complete sections 20 “Production of chemical substances and chemical products” and 21 “Production of medicines and materials used for medical purposes” |

| 7 | Production of rubber and plastic products | Entire Section 22 “Manufacture of rubber and plastic products” |

| 8 | Manufacture of other non-metallic mineral products | Entire Section 23 “Production of other non-metallic mineral products” |

| 9 | Production of finished metal products | Entire section 25 “Production of finished metal products” |

| 10 | Manufacturing of machinery and equipment | Entire section 28 “Production of machinery and equipment” |

| 11 | Production of electrical equipment, electronic and optical equipment | Complete sections 26 “Production of computers, electronic and optical products” and 27 “Production of electrical equipment”, as well as code 28.23 “Production of office equipment and machinery” |

| 12 | Production of vehicles and equipment | Complete sections 29 “Production of motor vehicles, trailers and semi-trailers” and 30 “Production of other vehicles and equipment” |

| 13 | Furniture manufacture | Entire section 31 “Furniture production” |

| 14 | Production of sporting goods | Code 32.30 from section 32 “Production of other finished products” |

| 15 | Production of games and toys | Code 32.40 from section 32 “Production of other finished products” |

| 16 | Research and development | Entire Section 72 Research and Development |

| 17 | Education | Entire Section 85 “Education” |

| 18 | Health and social service provision | Full sections 86 , 87 and 88 “Activities in the field of health and social services” |

| 19 | Activities of sports facilities | Code 93.11 from section 93 “Activities in the field of sports, recreation and entertainment” |

| 20 | Other sports activities | Other activities in section 93 “Activities in the field of sports, recreation and entertainment” |

| 21 | Processing of secondary raw materials | Code 38.3 from section 38 “Collection, processing and disposal of waste, processing of secondary raw materials” |

| 22 | Construction | Complete sections 41 , 42 and 43 “Construction” |

| 23 | Vehicle maintenance and repair | Code 45.2 from section 45 “Wholesale and retail trade in motor vehicles and motorcycles and their repair” |

| 24 | Disposal of sewage, waste and similar activities | Complete sections 37 “Collection and treatment of wastewater” and 38 “Collection, treatment and disposal of waste; processing of secondary raw materials" |

| 25 | Transport and communications | Complete sections 49 “Activities of land and pipeline transport”, 50 “Activities of water transport”, 51 “Activities of air and space transport”, 61 “Activities in the field of telecommunications” |

| 26 | Providing personal services | The entire section 96 “Activities for the provision of other household services” |

| 27 | Production of cellulose, wood pulp, paper, cardboard and products made from them | Entire Section 17 “Manufacture of Paper and Paper Products” |

| 28 | Production of musical instruments | Code 32.2 from section 32 “Production of other finished products” |

| 29 | Production of various products not included in other groups | Code 32.9 from section 32 “Production of other finished products” |

| 30 | Repair of household products and personal items | The entire section 95 “Repair of computers, personal consumption and household items” |

| 31 | Property Management | Code 68.32 from section 68 “Transactions with real estate” |

| 32 | Activities related to the production, distribution and exhibition of films | Codes 59.11 , 59.12 , 59.13 and 59.14 from section 59 “Production of films, videos and television programs, publication of sound recordings and notes” |

| 33 | Activities of libraries, archives, club-type institutions (except for the activities of clubs) | Code 91.01 from section 91 “Activities of libraries, archives, museums and other cultural objects” and code 90.04.3 , except for clubs from section 90 “Creative activities, activities in the field of art and entertainment” |

| 34 | Activities of museums and protection of historical sites and buildings | Codes 91.02 and 91.03 from section 91 “Activities of libraries, archives, museums and other cultural objects” |

| 35 | Activities of botanical gardens, zoos and nature reserves | Codes 91.04.1 and 91.04.2 from section 91 “Activities of libraries, archives, museums and other cultural objects” |

| 36 | Activities related to the use of computer technology and information technology | Complete sections 62 “Computer software development, consulting services in this area and other related services” and 63 “Activities in the field of information technology” |

| 37 | Retail trade of pharmaceutical and medical goods, orthopedic products | Codes 47.73 and 47.74 from section 47 “Retail trade, except trade in motor vehicles and motorcycles” |

| 38 | Production of bent steel profiles | Code 24.33 from section 24 “Metallurgical production” |

| 39 | Steel wire production | Code 24.34 from section 24 “Metallurgical production” |

With you

We reduce taxes using a “simplified” approach through voluntary health insurance

Tax holidays for entrepreneurs in 2021

Contribution benefits: shipping

Taxpayers making payments and other remuneration to the crews of ships registered in the Russian International Register have the right not to charge contributions on these payments and remuneration (from 2021 to 2027):

- on OPS;

- OSS for VNiM;

- Compulsory medical insurance.

The above-mentioned contributions for the performance of labor duties of ship crew members are not accrued to the corresponding payments and remunerations.

At the same time, vessels should not be used for the purpose of storing and transporting oil or petroleum products within the seaports of the Russian Federation.

The procedure for registering a taxpayer in the register of ships is established by Order of the Ministry of Transport of the Russian Federation dated December 9, 2010 No. 277 and involves inclusion in the register of passenger, cargo ships, as well as ships used to provide related services.

Who can count on benefits when calculating insurance premiums?

Who can count on benefits when calculating insurance premiums? Reduced insurance premium rates apply to several categories of payers.

For some categories of payers, reduced tariffs apply, which are permitted to be applied in accordance with Article 427 of the Tax Code of the Russian Federation.

In 2021, reduced insurance premium rates (in the Pension Fund - 8%, in the Social Insurance Fund - 2%, in the Federal Compulsory Medical Insurance Fund - 4%) are applied by the following taxpayers:

- business companies and business partnerships whose activities involve the practical application (implementation) of the results of intellectual activity;

- organizations and individual entrepreneurs that have entered into agreements with the management bodies of special economic zones on the implementation of technology and innovation activities;

- organizations and individual entrepreneurs that have entered into agreements on the implementation of tourist and recreational activities and make payments to individuals working in tourist and recreational special economic zones, united by a decision of the Government of the Russian Federation into a cluster;

- organizations operating in the field of information technology.

Form and submit insurance premiums online through Kontur.Accounting.

Try for free

During 2016–2018, reduced insurance premium rates are applied (in the Pension Fund of the Russian Federation - 20%, in the Social Insurance Fund - 0%, in the Federal Compulsory Medical Insurance Fund - 0%) the following taxpayers:

- pharmacy organizations;

- organizations and individual entrepreneurs using the simplified taxation system (STS) for certain types of economic activities (the amount of income is determined in accordance with Article 346.15 of the Tax Code of the Russian Federation);

- charitable organizations registered in the manner established by the legislation of the Russian Federation and applying the simplified tax system;

- Individual entrepreneurs applying the patent taxation system (with the exception of individual entrepreneurs carrying out the types of business activities specified in paragraphs 19, 45 - 47, paragraph 2 of Article 346.43 of the Tax Code of the Russian Federation);

- NPOs on the simplified tax system working in the field of social services, scientific development, healthcare, culture and art, education and mass sports (except professional). Basic - paragraphs. 7 clause 1 art. 427 Tax Code of the Russian Federation.

Organizations that have received the status of a participant in the Skolkovo project must pay 14% to the Pension Fund, 0% to the Social Insurance Fund, and 0% to the Federal Compulsory Medical Insurance Fund.

Also, during 2016–2027, reduced rates of insurance premiums are applied (in the Pension Fund of the Russian Federation - 0%, in the Social Insurance Fund - 0%, in the Federal Compulsory Medical Insurance Fund - 0%) for payers making payments to crew members of ships registered in the Russian International Register of Ships for the performance of the member’s labor duties crew of the vessel, in terms of the specified payments and rewards.

You can always check the information or familiarize yourself with new legal acts in the database of regulatory documents of the Kontur.Accounting web service. Users of the service literally have it at their fingertips. There is a search bar in any section, and you can access the latest version of a document at any time. In this case, the data on the page you are working on will not be lost.

However, in the service itself, all forms and templates are updated automatically to take into account changes in legislation. All payments and contributions will be calculated correctly, and reporting will be generated without errors, which eliminates penalties and fines.

Contribution benefits: production and services on the simplified tax system and individual entrepreneurs on a patent

In 2017–2018, companies using the simplified tax system have the right to pay contributions to the Pension Fund at a rate of 20% and not to pay contributions to the Social Insurance Fund for sick leave and maternity leave and to the Federal Compulsory Medical Insurance Fund, which:

1. Are engaged in production (in accordance with the list reflected in subparagraph 5, paragraph 1, article 427 of the Tax Code of the Russian Federation).

2. Carry out activities in the field of science, innovation, healthcare, social services, and sports.

3. They are engaged in processing recyclable materials,

4. They are engaged in construction.

5. Services provided:

- for vehicle maintenance and repair;

- for the removal of wastewater and waste;

- transport;

- in the field of communications;

- personal;

- repair of household products;

- in real estate management.

6. They are engaged in film production.

7. Organize the work of libraries, archives, museums, protect historical places and buildings.

8. Organize the work of botanical gardens, zoos, and nature reserves.

9. Are engaged in activities in the IT field (but do not belong to companies classified in subparagraphs 2 and 3 of paragraph 1 of Article 427 of the Tax Code of the Russian Federation).

10. Are engaged in retail trade in medicines and orthopedic products.

The main condition for applying a reduced tariff is that one of the above types of activities is the main one. Moreover, these taxpayers must have an annual income of no more than 79,000,000 rubles. and extract at least 70% of its value within the framework of a preferential type of activity.

An individual entrepreneur on a patent has the right to pay contributions at the same preferential rates that are established for listed companies on the simplified tax system, subject to the implementation of types of activities not specified in subparagraph. 19, 45–48 paragraph 2 art. 346.43 Tax Code of the Russian Federation.

Is sick leave subject to insurance contributions?

Hospital benefits are not subject to insurance contributions (Clause 1, Article 422 of the Tax Code of the Russian Federation). This applies to both the amount of benefits paid by the employer (the first 3 days) and the amount reimbursed from the Social Insurance Fund.

However, in some cases, sick leave is subject to insurance premiums:

- when the employer makes an additional payment from his own funds up to 100% of average earnings;

- when the amount of sick leave paid to an employee is not accepted by the Social Insurance Fund (letter of the Ministry of Labor of the Russian Federation dated February 26, 2016 No. 17-3/B-76).

Contribution benefits: charitable organizations and NPOs

Charitable organizations using the simplified tax system can pay compulsory health insurance contributions at a rate of 20% in 2017–2018, but not pay compulsory medical insurance and compulsory medical insurance contributions. The main thing is that the company’s activities correspond to the goals stated in the constituent documents. The authorized federal body monitors compliance with this criterion.

Non-profit organizations (NPOs) on the simplified tax system that operate in the field of:

- social services;

- Sciences;

- education;

- healthcare;

- mass sports;

- culture and art.

These NPOs can pay compulsory health insurance contributions at a rate of 20% in 2017–2018, and not pay compulsory health insurance and compulsory health insurance contributions, provided they receive at least 70% of total income from:

- targeted financing of NPOs;

- grants;

- carrying out economic activities of those types that are reflected in paragraph. 17–21, 34–36 sub. 5 p. 1 art. 427 Tax Code of the Russian Federation.

You can learn more about the features of the work of non-profit organizations in the context of accounting in the article “Features and tasks of accounting in non-profit organizations.”

What amounts are not subject to insurance premiums?

Firstly, these are payments to individuals, which the Tax Code does not at all recognize as an object of taxation:

- under GPC agreements (except for those listed above) on the transfer of ownership and other real rights, or the transfer of property for use (clause 4 of Article 420 of the Tax Code of the Russian Federation);

- Payments to foreign individuals working in foreign divisions of Russian companies are not subject to insurance premiums (clause 5 of Article 420 of the Tax Code of the Russian Federation);

- reimbursement of expenses to volunteers who have entered into GPC agreements, in accordance with the law on charity (Article 7.1 of Law No. 135-FZ of August 11, 1995). Volunteer expenses for food exceeding the daily allowance are subject to insurance contributions (clause 6 of Article 420 of the Tax Code of the Russian Federation);

- payments not subject to insurance premiums to foreigners and stateless persons who have entered into employment and GPC agreements with the organizers of the 2018 World Football Championship and the 2017 FIFA Confederations Cup, as well as compensation for some expenses incurred by volunteers of these events (clause 7 of Art. 420 Tax Code of the Russian Federation).

Secondly, Art. 422 of the Tax Code of the Russian Federation provides an exhaustive list of payments not subject to insurance contributions, consisting of 15 points. In particular, employers should not charge insurance premiums for the following payments:

- state benefits, including those paid for compulsory social insurance and unemployment;

- standardized compensation, incl. when dismissing employees (except for compensation for unused vacation), for compensation for harm to health, for expenses of individuals under GPC agreements, reimbursement to the employee of costs for professional training and advanced training, etc.,

- one-time financial assistance to persons affected by natural disasters, terrorist attacks in the Russian Federation, in connection with the death of a relative or the birth (adoption) of a child;

- other financial assistance for employees up to 4,000 rubles. in year;

- The following payments to residents of the Far North are not subject to insurance premiums: payment for travel to the place of vacation, transportation of luggage up to 30 kg, or their payment to the point of crossing the state border of the Russian Federation when going abroad on vacation;

- payments for employees under annual medical care contracts, non-state pension agreements, etc.;

- amount not subject to insurance premiums, up to 12,000 rubles. per year per employee for an additional funded pension;

- other payments listed in paragraph 1 of Art. 422 of the Tax Code of the Russian Federation.

Thirdly, some payments are not subject to certain insurance premiums (clause 3 of Article 422 of the Tax Code of the Russian Federation):

- payments for student work for full-time students, as well as the maintenance of judges, prosecutors and investigators are exempt from “pension” contributions;

- Contributions in case of maternity and temporary disability are not subject to any GPC agreements, unless they contain a special clause that contributions will be accrued.

Contribution benefits: Skolkovo residents

Residents of an innovative center have the right, within 10 years after receiving resident status of a given center (from the 1st day of the month following the one in which the corresponding status was received), to pay contributions to compulsory health insurance in the amount of 14%, and not to pay to compulsory social insurance and compulsory medical insurance, provided :

- receiving a profit of no more than 300,000,000 rubles, which is calculated on an accrual basis from the beginning of the year;

- receiving revenue of no more than 1,000,000,000 rubles. at the end of the year.

From the 1st day of the month following the one in which the company exceeded the specified indicators, the use of the benefit in question on insurance premiums is not carried out.

Information on the revenue and profit of a Skolkovo resident is provided to the Federal Tax Service by the management company of the corresponding business entity.

Contribution benefits: residents of special economic territories and ports

The following have the right to pay contributions to compulsory health insurance at a rate of 6%, compulsory social insurance at a rate of 1.5% and compulsory medical insurance at a rate of 0.1%:

- legal entities and individual entrepreneurs operating in Sevastopol and Crimea as participants in free economic zones;

- organizations and individual entrepreneurs with the status of resident of the priority development territory;

- organizations and individual entrepreneurs with resident status of the free port in Vladivostok.

These business entities have the right to apply benefits on social contributions for 10 years after they acquire one of the designated statuses (from the 1st day of the month following the one in which the status was received).

In this case, firms must have time to obtain a preferential status within 3 years after the entry into force of the legal acts establishing the corresponding statuses.

Conditions for applying preferential rates for insurance premiums

Some economic entities can count on relaxations when calculating the amount of payments to extra-budgetary funds. We will provide below detailed information on how to correctly apply reduced rates, and who has the right to reduce payments using the required benefits on insurance premiums.

Reduced tariffs can be used by organizations whose activities are aimed at introducing the results of intellectual work, the rights to which are in the exclusive ownership (including joint ownership) of the founders or participants of these organizations, as well as their partners (budgetary and autonomous scientific institutions).

The tariff rate for such organizations is reduced:

- contributions to the Pension Fund: 8% for 2021, 13% for 2021, 20% for 2019;

- contributions to the Social Insurance Fund: 2% for 2021, 2.9% for 2018-2019, for foreigners, as well as stateless persons and temporary residents - 1.8%;

- contributions to the Compulsory Medical Insurance Fund: 4% for 2021, 5.1% for 2018-2019.

To do this, the following conditions must be met:

- The research institute carries out development and design activities;

- activities are carried out on the simplified tax system;

- information about the creation of the company is entered into the accounting register.

Benefits are provided to companies and individual entrepreneurs engaged in technical innovation or tourism and recreational activities in special economic zones. Tariff rates are similar.

The rate has been reduced for resident organizations engaged in the development of information systems and computer software, as well as providing services for modification and adaptation of computer programs and systems.

Tariff rate until 2023 inclusive:

- contributions to the Pension Fund and Social Insurance Fund - 8%;

- contributions to the Compulsory Medical Insurance Fund - 4%.

To qualify for a benefit on insurance premiums, the following conditions must be met:

- a document on state accreditation has been received;

- income from core activities is 90% for the reporting period;

- Average headcount (SSH) is more than seven people.

Organizations and individual entrepreneurs that have received the status of:

- participant in the free economic zone in accordance with Federal Law No. 377 of November 29, 2014;

- resident of zones of rapid socio-economic development in accordance with Federal Law No. 473 of December 29, 2014;

- resident of the port of Vladivostok.

The following rates apply to them:

- Pension Fund - 6%;

- Social Insurance Fund – 1.5%;

- Compulsory medical insurance – 0.1%.

Benefits are valid for 10 years from the date of receipt of the above status.

Results

Payers of the simplified tax system, and in many cases - payers of any tax system, have the right to take advantage of the opportunity to pay contributions to compulsory health insurance, compulsory health insurance for VNIM and compulsory medical insurance at reduced rates or not to pay them at all. The magnitude of these rates, as well as the possible duration of application, may depend on the type of activity of the business entity, its organizational and legal form, and the region of operation.

You can learn more about the use of the simplified tax system by various business entities in the articles:

- “What are the insurance premiums for the simplified tax system in 2017?”;

- “Procedure for maintaining accounting under the simplified tax system (2015–2016)”.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.