VAT declaration 2021 – form

From the first quarter of 2021, a new VAT declaration form will be used. The form was approved by order of the Federal Tax Service of the Russian Federation dated October 29, 2014 No. ММВ-7-3/558, as amended on December 20, 2016.

For VAT, reporting “on paper” has not been submitted since 2014 - you need to report to the Federal Tax Service electronically via TKS through a special operator. The paper form can only be used by non-paying tax agents and taxpayer agents exempt from calculating and paying VAT (clause 5 of Article 174 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of the Russian Federation dated January 30, 2015 No. OA-4-17/1350).

The VAT return is submitted no later than the 25th day after the end of the quarter. For the 4th quarter of 2021, you must report by January 25, 2018, regardless of the form of submission of the report.

How to submit a VAT return

You must submit your VAT return in 2021 electronically through a special operator. The number of employees does not matter.

Only two categories can submit declarations on paper:

- tax agents who do not act as VAT payers and do not conduct intermediary activities with issuing invoices on their own behalf;

- foreign tax agents and foreign organizations providing electronic services in the Russian Federation.

If you submit a declaration on paper, the Federal Tax Service will not accept it and will consider it unsubmitted with all the resulting fines, penalties and blocks.

Composition of the VAT return

The procedure for filling out the declaration was developed by the Federal Tax Service of the Russian Federation in Appendix No. 2 to the same order No. MMV-7-3/558, which approved the form.

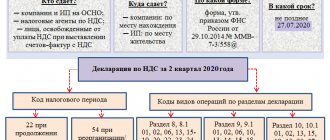

The VAT form consists of a title page and 12 sections, of which only section 1 is mandatory for everyone, and the rest are filled out only if the relevant data is available.

Thus, for taxpayers who carried out only non-VAT-taxable transactions in the reporting quarter, section 7 of the VAT declaration is required to be completed. “Special regime officers” who allocated VAT in invoices, and persons exempted from taxpayer obligations under Articles 145 and 145.1 of the Tax Code of the Russian Federation, but those who have issued VAT invoices submit Section 12 as part of the declaration. VAT agents fill out Section 3 if they have had no other tax transactions other than agency ones. Sections 8 and 9 are intended for taxpayers keeping books of purchases/sales, and sections 10 and 11 are intended for intermediaries filling out a declaration according to the invoice journal.

VAT return: examples of calculations

VAT is calculated based on the results of the quarter and paid in equal installments over the next 3 months. The payment deadline is in accordance with the provisions of Art. 174 of the Tax Code of the Russian Federation - until the 25th of the month. For example, if payment is due at the end of the 1st quarter. In 2021, 2,190 thousand rubles are due, which means that the company must pay 730 thousand each by the 25th of April, May and June. Please note that the payment deadline may be postponed due to weekends. This happened in June - you can pay VAT on the 26th of the month without penalties.

VAT return 2021: calculation of deductions

The formula for calculating the share of deductions in the declaration form for 2021 is as follows:

Cost of goods and services for activities with VAT/Cost of all goods

Please note that the VAT control ratio makes it easy to find the amount for non-taxable transactions and write it off as expenses in accordance with the law. Thus, the company will reduce income tax.

Rules and procedure for filling out the new declaration 2017

The VAT declaration 2021 form is filled out according to the instructions:

- Everyone fills out the cover page of the form without fail.

- Sections 2-12 are completed in the presence of the specified operations

- Tax agents must submit the form with Section 2

- Section 7 deals with non-taxable transactions

- Section 8 reflects past tax deductions

- The sales book data is transferred to the table in Section 9

- From the invoice journal, the numbers are placed in Sections 10 and 11

- Section 12 reflects transactions without tax

Form 2021 was approved by the beginning of the year and is used from the 1st quarter report.

Deadlines for submitting reports and VAT adjustments

For the 4th quarter of 2021, you still need to use the old form; a similar rule applies to corrections. The updated VAT return in 2021 for 2021 will be submitted on the form of the previous period. If the clarification for VAT 2021 concerns data for the period when the new form was already in effect, it is this that should be used when submitting corrective information.

From the report for 1 quarter. 2021 a new VAT form is in effect. Due dates do not change. Late payments will still incur penalties. By the way, the Federal Tax Service may fine you 20% of the unpaid amount in accordance with the provisions of Art. 122 of the Code. If you deliberately “avoided” paying tax, the Federal Tax Service may impose a sanction in the amount of 40% of the arrears. These are the rules for 2021.

You can find out more about the amount of the fine in 243-FZ dated 07/03/16. If you forgot to submit the form on time, you can submit the primary one with a zero amount, and then send a corrective VAT return for the full amount. This technique will protect you from a fine, although you will have to give explanations to the tax inspectors about your “forgetfulness.”

Particular adjustments to the new declaration form

VAT reporting must now be submitted taking into account the following provisions:

- You can find a free form on the official website

- Updated KND form code 1151001

- The main changes affected Section 3

- Lines 041-042 reflect sales upon expiration

- Line 110 discloses the tax amounts according to the customs declaration

- Norms Art. 173 of the Tax Code of the Russian Federation in part of clause 6 applies to the data on page 115

The new form has the same number of sections as the old form. There are exactly 12 of them, but sections 2-12 need to be filled out only if the taxpayer had relevant transactions in the reporting period, and these are the quarters of 2021. But in practice this rule works like this:

Taxpayers usually fill out forms electronically, therefore, they do not need to decide which sheets will be included in the final report. They enter only the data they have as required by the legislator. As a result, they generate a report where some of the sheets will contain zeros. You don’t need to “throw out” anything from the form yourself, and this won’t work in the electronic declaration. Just submit the form in full.

| Download VAT Declaration 2017 |

VAT declaration 2017: filling out the required sections

The VAT declaration is filled out based on the following documents:

- Purchase books and sales books,

- Invoices from VAT evaders,

- Invoice journal (intermediaries),

- Accounting registers and tax registers.

The title page of the declaration is quite standard. It contains information about the organization/individual entrepreneur:

- TIN and checkpoint,

- Adjustment number – “0” for the primary declaration, “1”, “2”, etc. for subsequent clarifications,

- Tax period code, according to Appendix No. 3 to the Filling Out Procedure, and year,

- Code of the Federal Tax Service where reports are submitted,

- Name/full name VAT payer, as indicated in the company’s charter, or in the individual’s passport,

- OKVED code, as in the extract from the Unified State Register of Legal Entities/Unified State Register of Individual Entrepreneurs,

- Number of pages of the declaration and attached documents,

- Contact details, signature of the manager/individual entrepreneur.

Section 1 of the VAT return, which is mandatory for everyone, reflects the amount of tax to be paid or reimbursed from the budget. The data is entered into it after calculating the results in other necessary sections of the declaration, and includes:

- Territory code according to OKTMO - it can be found in the territory classifier, or on the websites of Rosstat and the Federal Tax Service;

- KBK, relevant for this period,

- Lines 030-040 reflect the total amount of tax payable, and line 050 - the amount to be reimbursed,

- Lines 060-080 are filled in if the code “227” is indicated in the “At location” line of the title page.

The title page with section 1 is submitted to the Federal Tax Service and in the case where there are no indicators to be reflected in sections 2-12 of the declaration, such VAT reporting will be “zero”.

VAT declaration 2021 sample filling

There is already a list of innovations in the new document and visual professional instructions on the 2021 declaration form, which must be strictly followed in order for the tax inspector to recognize the fact that the document has been submitted. Otherwise you will have to pay a fine. The Tax Service decided to change the 16 barcodes that identified the sections of each sheet. The formats for submitting declarations and tax registers, such as the company's purchase book and sales book, will also be adjusted.

How to check the VAT payer?

The purpose of legislative innovations is to bring the value added tax declaration into compliance with current legal norms. Previously, there were a number of inconsistencies that prevented the correct interpretation of the information. To avoid discrepancies, changes were made to the form and requirements for filling it out. In order for taxpayers to know exactly what the legislator expects from them, instructions were developed and comments from tax department specialists were given. For this purpose, amendments were even prepared to the order of the Federal Tax Service MMV-7-3 / [email protected] , which was issued on October 29, 2014.

How to check the declaration

Before sending the completed declaration to the Federal Tax Service, you need to check that it is filled out correctly. This can be done using the “Control ratios of declaration indicators”, published in the letter of the Federal Tax Service of the Russian Federation dated 04/06/2017 No. SD-4-3/6467. The ratios are checked not only within the VAT return, but are compared with indicators of other reporting forms and financial statements.

If any control ratio for VAT is violated, the declaration will not pass a desk audit, the tax authorities will consider this an error and send a request for appropriate explanations within 5 days. Taxpayers are required to submit explanations, as well as the declaration, in electronic form according to the TKS (clause 3 of Article 88 of the Tax Code of the Russian Federation). Electronic formats for such explanations were approved by order of the Federal Tax Service of the Russian Federation dated December 16, 2016 No. ММВ-7-15/682.

What to fill out

The entire VAT reporting form is given in the first appendix to the order of the tax service dated October 29, 2014 No. ММВ-7-3/558. However, there is no need to submit a zero VAT return for the 3rd quarter of 2021 with all sheets. It is enough to pass two components:

- title page;

- first section.

This is required by the rules for filling out such reports. From a practical point of view, this is easy to explain: tax officials at the inspectorates do not need unnecessary electronic trash in the form of corresponding redundant files (sheets of a zero VAT return with dashes).

Sample of filling out a VAT return

Astra LLC uses OSNO and is engaged in wholesale trade of products. Let's say that in the 4th quarter of 2021 Astra had only three operations:

- Goods were sold to one buyer in the amount of 1 million rubles. excluding VAT. Goods sold are subject to VAT at a rate of 18%.

- Goods were purchased for the amount of 1416 thousand rubles. including VAT 18% (RUB 216 thousand). This tax, according to the documents, can be deducted.

- An advance payment was received from the buyer for future deliveries in the amount of 531 thousand rubles. including VAT 18% (RUB 81 thousand).

In this case, you need to fill out the following sections of the declaration:

- title page,

- Section 1 – the amount of VAT to be transferred to the budget;

- Section 3 – tax calculation for the reporting quarter;

- section 8 – indicators from the purchase book on the received invoice in order to deduct the submitted VAT from the total tax amount;

- section 9 - data from the sales book on issued invoices. In our case, this section needs to be filled out twice, because... There were two sales transactions, and we will fill in the total lines 230-280 only once.

Instructions for filling out a VAT return

Before filling out the declaration, double-check that the information in the purchase book and sales book is correct. Here are short instructions for filling out for a company on OSNO, which works without intermediaries.

- Be sure to complete the title page and first section.

- Indicate the organization data, INN and KPP, OKTMO code.

- In line 030, the amount of VAT payable to the budget is indicated by suppliers who apply special regimes or are exempt from VAT, but issue invoices with a dedicated tax.

- In lines 040 and 050, indicate the total values from 3-6 sections, if they were filled out. Line 040 will reflect VAT payable, and line 050 will reflect VAT payable.

- Fill in lines 060-080 only if code 227 is indicated on the title page “at the location (accounting)”.

- Lines 085-095 are completed by taxpayers who are a party to an investment protection and promotion agreement.

- Complete Section 3 to calculate tax on regular transactions. This does not include transactions at a 0% rate and non-taxable VAT.

On the first page of the section you need to reflect the cost of goods shipped, construction and installation works and advances received. For each category, indicate the VAT charged on them. The total amount of calculated tax, taking into account the restored VAT, is reflected on line 118.

On the second page, provide information about deductions for purchased goods, works, services, as well as advances issued and received. On line 190, enter the total amount of deductions.

On line 200, reflect the difference between the calculated VAT and deductions. If the deductions exceeded the tax, leave this line empty, and indicate the VAT to be refunded on line 210.

Appendix No. 1 to the third section is filled out by companies planning to restore value added tax on real estate, which must correspond to tax-exempt transactions. Appendix No. 2 to the third section is filled out by foreign companies.

3. Fill out sections 8 and 9, indicating data from the purchase book and sales book, that is, data on invoices received and issued. Include only those invoices for which the right to deduction arose during the reporting quarter.

Before filling out sections 8 and 9, it is advisable to check with your counterparties the number and details of invoices that you will include in the declaration. If there were no invoice registrations during the quarter, these sections may not be included in the declaration.

Updated declaration

Before calculating VAT, how to fill out the declaration for the 3rd quarter and how to submit it to the tax service, you should carefully check all the indicated amounts. If the taxpayer submitted a document and only then discovered an error, he is obliged to submit an updated declaration to the fiscal service.

If the updated version of the document is submitted to the authorities later than the deadline for submitting the report, then the taxpayer will need to reimburse the arrears and penalties. In this case, he can avoid punishment in the form of a fine. If the submitted VAT return for the 3rd quarter of 2017, which can be downloaded from our website, displays inaccurate data that does not affect the amount of tax, then the taxpayer has the right not to submit updated data, as evidenced by Article 81 of the Tax Code of the Russian Federation.

When submitting a declaration to the fiscal service for the second time with updated data, the correction number “001”, “002”, “003”, etc. is indicated on the title page of the document. depending on how often the clarification is submitted.

Similar articles

- VAT return for the 4th quarter of 2017

- Income tax for the 3rd quarter of 2016

- VAT return for the 4th quarter of 2017

- Zero VAT return

- Filling out the VAT return for the 3rd quarter