VAT declaration 2021 – form

From the first quarter of 2021, a new VAT declaration form will be used. The form was approved by order of the Federal Tax Service of the Russian Federation dated October 29, 2014 No. ММВ-7-3/558, as amended on December 20, 2016.

For VAT, reporting “on paper” has not been submitted since 2014 - you need to report to the Federal Tax Service electronically via TKS through a special operator. The paper form can only be used by non-paying tax agents and taxpayer agents exempt from calculating and paying VAT (clause 5 of Article 174 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of the Russian Federation dated January 30, 2015 No. OA-4-17/1350).

The VAT return is submitted no later than the 25th day after the end of the quarter. For the 4th quarter of 2021, you must report by January 25, 2018, regardless of the form of submission of the report.

Desk verification of the declaration

The VAT return sample is received by the tax inspector and its verification begins. The duration of the “camera chamber” is 3 months. Inspectors, using the capabilities of EDI, immediately see purchase and sale transactions in the context of counterparties, identify inconsistencies, for example, if the buyer did not pay the seller in full or the seller did not submit a VAT return, while you set the tax amount to be refunded, etc. For any inconsistencies, tax officials request clarification.

PLEASE NOTE: tax inspectors are now armed with the ASK VAT2 program, which perfectly analyzes the data in the declaration; a new version of VAT3 will soon be released, which will allow reconciliation of bank payments.

Now inspectors make a request to the bank to find out about payments. Receiving statements on hundreds of sheets is extremely inconvenient. The new version of the ASK solution will allow you to have all data on electronic media. Inspectors will save time and find discrepancies faster.

Tax officers receive the declaration and immediately see all transactions without payment. This does not interfere with the deduction. Still, inspectors take note of such operations. If you are not paying your supplier on an ongoing basis but are making deductions, this is suspicious.

Similar articles

- VAT return for the 4th quarter of 2017

- Filling out section 2 of the VAT return correctly

- VAT declaration

- How to fill out sections of a VAT return without errors?

- Filling out the VAT return for the 3rd quarter

Composition of the VAT return

The procedure for filling out the declaration was developed by the Federal Tax Service of the Russian Federation in Appendix No. 2 to the same order No. MMV-7-3/558, which approved the form.

The VAT form consists of a title page and 12 sections, of which only section 1 is mandatory for everyone, and the rest are filled out only if the relevant data is available.

Thus, for taxpayers who carried out only non-VAT-taxable transactions in the reporting quarter, section 7 of the VAT declaration is required to be completed. “Special regime officers” who allocated VAT in invoices, and persons exempted from taxpayer obligations under Articles 145 and 145.1 of the Tax Code of the Russian Federation, but those who have issued VAT invoices submit Section 12 as part of the declaration. VAT agents fill out Section 3 if they have had no other tax transactions other than agency ones. Sections 8 and 9 are intended for taxpayers keeping books of purchases/sales, and sections 10 and 11 are intended for intermediaries filling out a declaration according to the invoice journal.

How to draw up a VAT return - basic rules

Let's start with the fact that correctly filling out any documents, including tax documents, implies understanding the structure of the document. The declaration consists of several sections, each of which has its own characteristics and is designed to display specific information.

There are restrictions on the timing of submitting a document to the tax office - it must be submitted no later than the 20th day of the month following the completed reporting period - quarter. The transfer can be made personally by the taxpayer or his representative. It is also possible to send the declaration by mail or transmit it electronically.

VAT declaration 2017: filling out the required sections

The VAT declaration is filled out based on the following documents:

- Purchase books and sales books,

- Invoices from VAT evaders,

- Invoice journal (intermediaries),

- Accounting registers and tax registers.

The title page of the declaration is quite standard. It contains information about the organization/individual entrepreneur:

- TIN and checkpoint,

- Adjustment number – “0” for the primary declaration, “1”, “2”, etc. for subsequent clarifications,

- Tax period code, according to Appendix No. 3 to the Filling Out Procedure, and year,

- Code of the Federal Tax Service where reports are submitted,

- Name/full name VAT payer, as indicated in the company’s charter, or in the individual’s passport,

- OKVED code, as in the extract from the Unified State Register of Legal Entities/Unified State Register of Individual Entrepreneurs,

- Number of pages of the declaration and attached documents,

- Contact details, signature of the manager/individual entrepreneur.

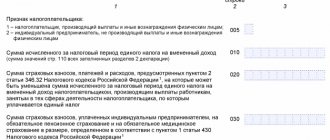

Section 1 of the VAT return, which is mandatory for everyone, reflects the amount of tax to be paid or reimbursed from the budget. The data is entered into it after calculating the results in other necessary sections of the declaration, and includes:

- Territory code according to OKTMO - it can be found in the territory classifier, or on the websites of Rosstat and the Federal Tax Service;

- KBK, relevant for this period,

- Lines 030-040 reflect the total amount of tax payable, and line 050 - the amount to be reimbursed,

- Lines 060-080 are filled in if the code “227” is indicated in the “At location” line of the title page.

The title page with section 1 is submitted to the Federal Tax Service and in the case where there are no indicators to be reflected in sections 2-12 of the declaration, such VAT reporting will be “zero”.

Return to supplier in VAT return

There are certain situations in which a customer returns an item because it is defective or not as described. In this case, it is necessary to reflect this operation in the declaration for VAT refund.

To do this, the return must be made in writing. An expense report is drawn up and the reason for the return is indicated. An act declaring the product to be of poor quality must be drawn up. Then the amount is returned to the buyer, and the returned goods must be indicated on off-balance account 002. Then you need to restore and pay the tax for this product. In 090, indicate the tax amount.

If the declaration is filled out correctly and on time, the taxpayer will never have problems with the tax service.

How to check the declaration

Before sending the completed declaration to the Federal Tax Service, you need to check that it is filled out correctly. This can be done using the “Control ratios of declaration indicators”, published in the letter of the Federal Tax Service of the Russian Federation dated 04/06/2017 No. SD-4-3/6467. The ratios are checked not only within the VAT return, but are compared with indicators of other reporting forms and financial statements.

If any control ratio for VAT is violated, the declaration will not pass a desk audit, the tax authorities will consider this an error and send a request for appropriate explanations within 5 days. Taxpayers are required to submit explanations, as well as the declaration, in electronic form according to the TKS (clause 3 of Article 88 of the Tax Code of the Russian Federation). Electronic formats for such explanations were approved by order of the Federal Tax Service of the Russian Federation dated December 16, 2016 No. ММВ-7-15/682.

What is a zero VAT return and is it possible not to submit it?

Formation of a zero VAT return is possible when a business entity on the OSN did not have transactions that were the object of tax assessment and transactions for which VAT could be deducted.

That is, there are no numerical indicators for calculation. The declaration is submitted on the form from the order of the Federal Tax Service of Russia dated October 29, 2014 No. ММВ-7-3/ [email protected] (as amended by the order dated November 20, 2019 No. ММВ-7-3/ [email protected] ). In zero they draw up:

- title page with data on the business entity;

- section 1 with OKTMO, KBK and the result of tax calculation.

Lack of data for calculating tax is not a reason for failure to submit a declaration. Fine 1,000 rubles. will follow even for failure to submit a zero report.

If the tax authorities do not receive the VAT return within 10 days after the end of the reporting campaign, they will block the current account.

All general regime workers who do not apply exemption under Art. 145 of the Tax Code of the Russian Federation, submit a report for the 2nd quarter of 2021 no later than July 27 of the current year (since the 25th falls on a weekend). Otherwise, you face a fine and blocking of your current account.

Sample of filling out a VAT return

Astra LLC uses OSNO and is engaged in wholesale trade of products. Let's say that in the 4th quarter of 2021 Astra had only three operations:

- Goods were sold to one buyer in the amount of 1 million rubles. excluding VAT. Goods sold are subject to VAT at a rate of 18%.

- Goods were purchased for the amount of 1416 thousand rubles. including VAT 18% (RUB 216 thousand). This tax, according to the documents, can be deducted.

- An advance payment was received from the buyer for future deliveries in the amount of 531 thousand rubles. including VAT 18% (RUB 81 thousand).

In this case, you need to fill out the following sections of the declaration:

- title page,

- Section 1 – the amount of VAT to be transferred to the budget;

- Section 3 – tax calculation for the reporting quarter;

- section 8 – indicators from the purchase book on the received invoice in order to deduct the submitted VAT from the total tax amount;

- section 9 - data from the sales book on issued invoices. In our case, this section needs to be filled out twice, because... There were two sales transactions, and we will fill in the total lines 230-280 only once.

VAT return: what needs to be taken into account when filling out

Key points you need to know when filling out:

- The declaration must be submitted at the end of each reporting period;

- Such a document must be filled out taking into account the available documents;

- The declaration includes data from the books of purchases and sales;

- Reliable information is provided to the tax office.

Another important condition is the weight of the document when sending. If it is large, the recipient must be warned about this in advance so that his technical capabilities allow him to work with such a document.

In order to fill out the document correctly, you need to know what it looks like. VAT return form cover page:

Who submits the VAT return and when?

According to paragraph 5 of Art. 174 of the Tax Code of the Russian Federation, the VAT declaration must be submitted by:

- legal entities and individual entrepreneurs applying the general taxation regime (except for VAT payers exempt from duties in accordance with Article 145, 145.1 of the Tax Code of the Russian Federation);

- legal entities and individual entrepreneurs who apply special tax regimes, as well as those who are exempt from the obligations of VAT payers if they issue invoices with the allocated tax amount.

The VAT return is submitted no later than the 25th day of the month following the reporting quarter. The deadline for submitting calculations for the 2nd quarter of 2021 is no later than July 25. This day falls on a day off (Saturday), and therefore the deadline is transferred to the first working day following it, i.e. on July 27th.

How to submit a VAT return

The VAT return for the 2nd quarter is submitted to the tax office at the location of the legal entity or place of residence of the individual entrepreneur.

According to paragraph 5 of Art. 174 of the Tax Code of the Russian Federation, the declaration must be submitted only in electronic form via TKS through an authorized special operator or through the Federal Tax Service website. If a taxpayer submits a VAT return on paper, for example, by mail, it will be considered that the calculation has not been submitted, for which the business entity will be held accountable.

Preparing a declaration for the 2nd quarter (general requirements)

The majority of companies and individual entrepreneurs report VAT using the KND form 1151001. Using our tips in the pictures, you can quickly navigate the basic rules for filing it and facilitate the process of generating a VAT return for the 2nd quarter of 2021:

A significant difference between a VAT return and other tax returns is the absence for most companies and individual entrepreneurs of alternative ways of submitting it to the INFS. VAT reporting can only reach the controllers electronically via TKS. Only the persons specified in paragraphs have the right to report on paper. 5-6 section 2 of Appendix No. 2 of the Procedure, approved. by order of the Federal Tax Service of Russia dated October 29, 2014 No. ММВ-7-3/ [email protected]

All the nuances of filing a VAT return were explained by ConsultantPlus experts:

Get trial access to K+ for free and go to the Ready-made solution.

Find out how you can send VAT explanations to inspectors from this publication.

Responsibility for failure to submit a VAT return

If the taxpayer does not submit a VAT return to the Federal Tax Service on time, he will be assigned administrative liability. According to paragraph 1 of Art. 119 of the Tax Code of the Russian Federation, the fine will be 5% of the tax amount according to the declaration for each full or partial month of delay. The fine cannot be more than 30% of the tax amount and less than 1,000 rubles.

In addition, the tax inspectorate may block transactions on the taxpayer’s current account on the basis of paragraphs. 1 clause 3, clause 11 art. 76 Tax Code of the Russian Federation. This penalty applies if a legal entity or individual entrepreneur delays submitting a declaration for a period of more than 10 working days.

An example of filling out a VAT return for the 1st quarter of 2016.

Alpha LLC is a VAT payer. 1st quarter operations:

| Operation | Cost including VAT, rub. | VAT, rub. |

| Shipment of goods to Beta LLC, issued c/f No. 1 dated 01/15/16, goods not paid for | 295 000 | 45 000 |

| Materials were received from the supplier Delta LLC, c/f No. 11 dated 01/20/16 was received, the materials were accepted for accounting on 01/20/16. | 118000 | 18000 |

| Receipt of an advance from Gamma LLC, payment date No. 1 dated 03/20/16, issued with payment date No. 2 dated 03/20/16. | 590 000 | 90 000 |

Results

To generate a VAT return, you need to decide on the required reporting form and correctly formulate the tax base. To do this, you should take into account the explanations of officials and apply changes in tax legislation in a timely manner.

Sources: Order of the Federal Tax Service of Russia dated October 29, 2014 No. ММВ-7-3/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Filing a declaration. Deadlines. Fines

At the end of the quarter, that is, 4 times a year, you need to fill out a VAT return and submit it to the tax office.

The deadline for submission is the 25th day of the 1st month following the reporting quarter.

If a company does not submit VAT reports on time, does not submit them at all, or submits them in paper form, then the tax office will impose a minimum fine of 1,000 rubles; if, in addition, the tax is not transferred on time, then the fine will increase to 5% of the debt for each month of delay. This amount is limited to 30% of the debt.

If activities subject to VAT were not carried out in the past quarter, and there were no deductions, then a zero declaration is submitted; its failure to submit also serves as the basis for penalties in the minimum amount of 1000 rubles.

The declaration must be submitted to the Federal Tax Service at the end of the quarter:

- Payers of the added tax.

- Tax agents.

- Companies that are not payers, but generate VAT invoices.

VAT return forms for the 2nd quarter

Before we start filling out the VAT return for the 2nd quarter of 2020, let’s figure out what form is required to report. Tax legislation provides several forms for VAT reporting:

VAT payers and tax agents use the KND form 1151001 for VAT reporting for the 2nd quarter of 2020. The version with updates dated November 20, 2019 is currently in effect.

Importers of goods from the territory of the EAEU use the declaration of indirect taxes in the form KND 1151088 for VAT reporting. They do not need to summarize the tax information in this form of the VAT report for the 2nd quarter of 2021 as a whole - it is enough to submit a declaration of the specified form only for those months. in which imported goods are registered.

The declaration form according to KND 1151115 is used exclusively by foreign companies that provide services to individuals in electronic form. They must report on the specified VAT return form for the 2nd quarter of 2021.