Which form should I use when filling out the UTII declaration for the 1st quarter of 2021? Has a new form been approved or is the old one being used? We will answer your questions and provide links to download the UTII form in the new format. Please note that the procedure for filling out the new declaration form has also been updated. If you have any questions, contact the experts on the forum on the topic “Filling out a new UTII declaration form in 2021.”

When to report

The UTII declaration must be submitted to the Federal Tax Service no later than the 20th day of the month following the expired quarter. This is provided for in paragraph 3 of Article 346.32 of the Tax Code of the Russian Federation.

If the deadline for submitting the declaration falls on a weekend, it is postponed to the next Monday (Clause 7, Article 6.1 of the Tax Code of the Russian Federation). In April 2018, such transfers will not be necessary. After all, the deadline for submitting the UTII declaration for the 1st quarter of 2021 is April 20, 2021 (Friday).

If you fail to submit your UTII declaration for the 1st quarter of 2021 or submit the document late, the company or individual entrepreneur may be fined. The amount of the fine is 5% of the amount of tax that is payable on the basis of the declaration. In this case, the total amount of the fine cannot be more than 30% of the tax amount and less than 1000 rubles. (Article 119 of the Tax Code of the Russian Federation).

Tax return for UTII in 2021. What should you pay attention to?

Send this article to my email

UTII (Unified Tax on Imputed Income) is a voluntary and maximally simple taxation regime: one tax replaces a number of other taxes (VAT, personal income tax, profit, property); there is no need to hire an accountant, the calculation formula is extremely simple.

Let's set up your 1C. We have been working since 2000. We are among the TOP 10 partners of 1C. Read more →

Organizations and individual entrepreneurs applying the UTII taxation system must submit quarterly (no later than the 20th day of the month following the reporting quarter) to the Federal Tax Service (Federal Tax Service) at the actual place of business activity (or at its location in the case where the exact the place cannot be determined) tax return and pay tax in accordance with it. The form of the UTII tax return and the procedure for filling it out are determined by the Federal Tax Service of Russia.

For UTII payers in 2021, significant changes have been made regarding their activities:

Deflator coefficient K1 has been changed;

The validity of UTII has been extended;

A tax deduction is provided for entrepreneurs using online cash registers;

The tax return form for UTII has been updated.

NEW K1 VALUE

Let us recall the formula for calculating UTII.

• BD - basic profitability depending on the type of activity. It means a value established by law that determines the amount of profit from the activities of an entrepreneur obtained using a unit of physical indicator;

• FP - physical indicator (sales area, number of employees, etc.);

• K1 – deflator coefficient, established by law separately for each year;

• K2 is a variable coefficient, has a value of 1 or less, is established legally by local authorities and depends on the type of activity.

The deflator coefficient K1 is a correction coefficient; it is used to bring imputed income, i.e., closer to the level of consumer prices for goods (work, services) of the previous year. needed to take into account inflation rates. For 2021, the size of K1 was equal to 1.798; in 2018, this value increased by 3.4% and is 1.868. Thus, the amount paid by UTII payers in 2018 increases.

THE POSSIBILITY OF USING UTII has been extended

It was decided to postpone the abolition of UTII. The period of application of UTII has been increased by another 3 years. Previously, the deadline was 12/31/17, but now it has been moved to 12/31/20.

TAX DEDUCTION FOR ONLINE CASH FOR INDIVIDUAL ENTREPRENEURS

In connection with the need to install an online cash register for individual entrepreneurs in 2018, for those who are on UTII (except for those who work in the field of retail and catering and individual entrepreneurs without employees), a law was adopted that allows reducing the amount of tax on the total costs associated with the purchase and implementation of an online cash register at the enterprise. Such expenses include the cost of a cash register, a fiscal drive, software, the cost of upgrading related equipment and other additional expenses. expenses. The amount of compensation offered is no more than 18,000 rubles. for each CCP.

UPDATED TAX DECLARATION FORM FOR UTII

The tax return for UTII in 2021 has been changed, a new form has been approved. It has not undergone significant changes, it still has the title page and three sections, the changes affected the barcodes, the KBK lines were removed, the OKUN codes were removed, lines appeared to include contributions for oneself, some wording and the formula were updated. These amendments have also been made to electronic declarations.

EVERYONE MUST DO THEIR JOB! TRUST THE 1C SETUP TO A PROFESSIONAL. MORE →

Discuss the article on the 1C forum?

New declaration form

For the first quarter of 2021, organizations and individual entrepreneurs on UTII must submit a declaration according to the “imputation” of the new form. The electronic declaration form required for submitting the UTII declaration electronically has also changed. There is also a new procedure for filling out the declaration.

The amendments are due to the fact that from January 1, 2021, entrepreneurs have the right to reduce UTII by the cost of online cash registers. The maximum amount of such a deduction is 18,000 rubles. for each cash register (Federal Law of November 27, 2021 No. 349-FZ). Accordingly, special lines are provided to reflect this deduction.

Also in the new UTII declaration form, a new section 4 has appeared, “Calculation of the amount of expenses for the acquisition of cash register equipment, which reduces the amount of the single tax on imputed income for the tax period.”

Let us remind you that the costs of purchasing a cash register online include:

- purchasing a device;

- fiscal accumulator;

- software;

- payment for related work and services (for example, setting up a cash register, etc.).

For UTII you do not need to contact the Federal Tax Service for a deduction via the online cash register. It is enough to declare it in the declaration. Due to this possibility, her form has been adjusted. For more information, see “Amendments to UTII from 2021.”

Tax return UTII

Home / Tax returns

Zero declaration on UTII

The opinion of the Ministry of Finance on this matter is clear: Chapter 26.3 of the Tax Code of the Russian Federation does not provide for the submission of “zero” declarations on UTII (letter of the Ministry of Finance dated July 3, 2012 No. 03-11-06/3/43).

The absence of economic activity under the imputed regime is the basis for deregistration under UTII in the manner prescribed by current legislation.

If the taxpayer was not deregistered under UTII, then stopping business activities, even if there is no physical indicator, is the basis for paying imputed tax and filing full (not zero) reporting.

In this case, the tax is calculated based on the size of the individual. indicator reflected in the reporting for the previous period in which activities were still ongoing (letter of the Ministry of Finance dated October 24, 2014 No. 03-11-09/53916).

Failure to fulfill tax payment obligations will entail the collection of arrears on UTII, as well as the accrual of fines and penalties.

However, there are clarifications from the Federal Tax Service, published on the official website of the tax service on September 19, 2016 (https://www.nalog.ru/rn32/news/activities_fts/6167481/), based on the decision of the Supreme Arbitration Court of the Russian Federation, according to which the submission of a zero declaration is possible .

This situation arises if the use or ownership of property, without which it is impossible to carry out the imputed activity, is terminated. The precedent under consideration is the termination of the lease agreement for retail space by the lessor.

But, if the taxpayer nevertheless decides to submit a zero return, with a high degree of probability he will have to defend his position in court.

Therefore, if a business entity does not want to incur additional expenses for paying taxes and submitting unnecessary reports in cases where activities for some reason were suspended or terminated completely, the most reliable way to avoid claims from regulatory authorities is to submit an application for deregistration under UTII.

Penalty for late submission of declaration

If the taxpayer does not submit the declaration on time, then the sanctions will range from 5% to 30% of the amount of unpaid tax reflected in the report for each full or partial month of delay, but not less than 1,000 rubles.

Moreover, if the imputed tax itself is paid on time, then failure to submit a declaration within the prescribed period will result in a fine of 1,000 rubles.

Responsibility for the delay in the UTII report imposed on the head of the legal entity of the Code of Administrative Offenses of the Russian Federation can range from 300 to 500 rubles.

Moreover, if the deadline for submitting the declaration is exceeded by more than 10 working days, the regulatory authorities may suspend operations on the current account of the business entity.

Programs and services for report preparation

A UTII declaration can be prepared using the following software and online services:

| Software name | Website |

| “Taxpayer Legal Entity” (free program from the Federal Tax Service) | https://www.nalog.ru/rn77/program/5961229/ |

| "Taxpayer PRO" | https://online.nalogypro.ru |

| "Bukhsoft" | https://online.buhsoft.ru |

| "1C" | 1c.ru |

| "Kontur.Accounting" | https://www.b-kontur.ru/lp/envd |

| "Sky" | nebopro.ru |

| "My business" | https://www.moedelo.org/landingpage/reporting-ednvd/ |

Did you like the article? Share on social media networks:

- Related Posts

- Sample declaration of the simplified tax system “income minus expenses”

- Explanatory note to the tax return for UTII

- Sample of filling out the UTII declaration for individual entrepreneurs

- Sample of filling out the simplified taxation system “income” declaration

- Tax return for simplified tax system in 2021

- Sample of filling out the Unified Agricultural Tax declaration for an LLC

- Sample of filling out the Unified Agricultural Tax declaration for individual entrepreneurs

- Zero declaration of the simplified tax system in 2021

Discussion: 3 comments

- andrey:

04/20/2018 at 13:43Has the new UTII declaration been approved yet?

Answer

Alexei:

04/23/2018 at 03:34

Hello. Not yet, they took it using the old form (Letter of the Ministry of Finance dated February 20, 2018 No. SD-4-3/ [email protected] ).

Answer

01/10/2019 at 19:21

Hello, can you tell me in the new declaration form, in section 4, if you didn’t buy a cash register, do you need to put dashes everywhere or can you not fill it out at all?

Answer

Leave a comment Cancel reply

How to fill out the new section 4

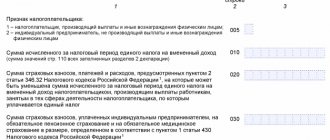

Here's how to fill out the new section 4 as part of the new UTII declaration form in 2021:

- on line 010 – name of the cash register equipment model;

- on line 020 – serial number of cash register equipment;

- on line 030 – registration number of cash register equipment assigned by the tax authority;

- on line 040 – the date of registration of cash register equipment with the tax authority;

- on line 050 - the amount of expenses incurred for the purchase of cash register equipment cannot exceed 18,000 rubles;

- If there are insufficient lines with codes 010, 020, 030, 040, 050, the required number of sheets in Section 4 of the Declaration must be filled out.

Read also

19.07.2016

Letter dated July 25, 2018 No. SD-4-3/ [email protected]

Federal Tax Service on the issue of the procedure for applying the provisions of paragraph 2.2 of Article 346.32 of the Tax Code of the Russian Federation (hereinafter referred to as the Code), put into effect by Federal Law dated November 27, 2017 No. 349-FZ “On Amendments to Part Two of the Tax Code of the Russian Federation” (hereinafter referred to as — Federal Law No. 349-FZ), providing for the opportunity for individual entrepreneurs (hereinafter referred to as individual entrepreneurs) paying a single tax on imputed income for certain types of activities (hereinafter referred to as a single tax, UTII), to reduce the amount of a single tax by the amount of expenses for the acquisition of a cash register equipment (hereinafter referred to as CCT), reports the following.

In accordance with clause 2.2. Article 346.32 of the Code An individual entrepreneur has the right to reduce the amount of the single tax, calculated taking into account paragraph 2.1 of Article 346.32 of the Code, by the amount of expenses for the acquisition of a cash register included in the register of cash registers, for use in making payments in the course of business activities subject to a single tax, in the amount of no more than 18 000 rubles for each copy of a cash register, subject to registration of the specified cash register with the tax authorities from February 1, 2021 to July 1, 2021, unless otherwise provided in paragraph two of this paragraph.

According to paragraph two of clause 2.2. Article 346.32 of the Code Individual entrepreneurs carrying out business activities provided for in subparagraphs 6 - 9 of paragraph 2 of Article 346.26 of the Code, and having employees with whom employment contracts were concluded on the date of registration of the cash register in respect of which the tax amount is reduced, have the right to reduce the amount of the single tax by the amount of expenses , specified in paragraph one of this paragraph, subject to registration of the corresponding cash register equipment from February 1, 2021 to July 1, 2021.

In order to implement the specified provisions of the Code, by order of the Federal Tax Service dated June 26, 2018 No. ММВ-7-3/ [email protected] “On approval of the tax return form for the single tax on imputed income for certain types of activities, the procedure for filling it out, as well as the presentation format tax return for a single tax on imputed income for certain types of activities in electronic form" (hereinafter referred to as the Order), a new form of a tax return for a single tax on imputed income for certain types of activities was approved (for registration with the Ministry of Justice of Russia).

In accordance with paragraph 3 of Article 346.32 of the Code, tax returns based on the results of the tax period are submitted by taxpayers to the tax authorities no later than the 20th day of the first month of the next tax period.

In order to exercise the right of taxpayers to reduce the amount of the single tax by the amount of expenses for the acquisition of cash registers and before the entry into force of the Order, the Federal Tax Service of Russia recommends using the tax return form attached to this letter, starting with the submission of tax reports for the tax period - the 3rd quarter of 2018.

Taxpayers must submit amended tax returns in the form in which the original returns were submitted.

In connection with the use in one tax period of two forms of tax declarations, having one KNI with different composition of indicators, the Federal Tax Service of Russia for the constituent entities of the Russian Federation is instructed to pay special attention to lower tax authorities on the registration of declarations received on paper, since in this case, when registration, you must correctly select one of two templates (old and new form).

To register the recommended form of declaration submitted on paper, you must:

— take into account that for this KND for the 3rd quarter of 2021 there are two forms;

— take into account the barcode of the title page;

— take into account the correspondence of the template to the title page.

The Federal Tax Service of Russia for the constituent entities of the Russian Federation is instructed to bring this letter to lower tax authorities, as well as to taxpayers.

Application for 34 l.

Acting State Advisor of the Russian Federation, 3rd class D.S. Satin

Application zip (235 kb)

Download

Section 4 of the declaration

Lines 010-050 of Section 4 must be completed for each copy of the cash register purchased for UTII activities and registered with the tax authorities within the established time frame.

Let's continue with our original example. According to its terms, IP Kuleshova N.A. On July 17, 2018, I registered a cash register with the tax authorities. The cost of purchasing a cash register and connecting it amounted to 12,480 rubles. In section 4, to receive a cash register deduction, the entrepreneur filled out one block of lines 010-050:

The amount of expenses for purchasing a cash register reduces the UTII tax and is reflected in section 2 of the declaration.