Numbering on invoices over several years leads to the fact that the numbers on the papers become larger and larger. This is not very convenient when keeping records, since you have to operate with large numbers. For this reason, some enterprises, usually large ones, start numbering from one every month, year or quarter. However, according to Letter of the Ministry of Finance of Russia dated October 16, 2012 N 03-07-11/427, the organization’s policy in this area has some nuances. The same document did not explain exactly how to carry out the numbering. For this reason, this operation still raises a lot of questions.

The legislative framework

Standard details of invoices for shipment, advances and adjustments are set out in paragraphs 5, 5.1 and 5.2 of the Tax Code of the Russian Federation. The serial number is also considered a property. However, there is no numbering order in the law. The features of this operation are spelled out in the Resolution of the Russian Federation dated December 26, 2011, number 1137. In particular, a reference to this normative act is contained in paragraph 8 of Article 169 of the Tax Code of the Russian Federation.

The numbering order has not been edited for many years. Some of the latest innovations were introduced in 2014: the resolution specified a separating symbol that is used when drawing up documentation. This law applies to the following structures:

- Separate divisions.

- Trust managers.

- Persons participating in the partnership.

In particular, you need to use the “/” sign for separation.

Numbering order of invoices

Home — Consultations

Does an organization have the right to establish a special order for numbering invoices? Wouldn't this be grounds for refusing a VAT deduction?

Commentary to the Letter of the Ministry of Finance of Russia dated January 12, 2021 N 03-07-09/411

An invoice is a document that serves as the basis for the buyer to accept “input” VAT for deduction (Article 169 of the Tax Code). The mandatory details of this document are established by paragraphs 5, 5.1 and 6 of Article 169 of the Tax Code (hereinafter referred to as the Code). In particular, according to subparagraph 1 of paragraph 5 of Article 169 of the Code, the invoice issued for the sale of goods (work, services), transfer of property rights must necessarily indicate the serial number and date of the invoice.

In turn, the Rules for filling out invoices were approved by Government Decree No. 1137 of December 26, 2011 (hereinafter referred to as the Rules). The rules establish that the serial number is indicated in line 1 of the invoice (subparagraph “a”, paragraph 1 of the Rules). Moreover, there are two cases when the serial number through the “/” sign (dividing line) is supplemented with a digital index:

- when selling goods through a separate division of the organization;

- if the invoice is issued by a member of the partnership or a trustee.

Neither the Code nor the Rules establish any more requirements for the formation of the “serial number” indicator of an invoice. At the legislative level, there is also no prohibition on the taxpayer being able in other cases to use a dividing line and any indexes (numeric or alphabetic) in numbering.

Plus, paragraph 2 of Article 169 of the Code establishes a rule - errors in invoices that do not prevent tax authorities from identifying the seller, buyer of goods (work, services), property rights, the name of goods (work, services), property rights, their the cost, as well as the tax rate and the amount of tax presented to the buyer, are not grounds for refusing to accept tax amounts for deduction. Obviously, the mistake made in the invoice number refers precisely to shortcomings that do not in any way prevent tax authorities from identifying the parties and the amount of the transaction, as well as the tax rate and, in fact, the amount of tax. The Ministry of Finance, in a letter dated January 12, 2021 N 03-07-09/411, also confirmed that the right to apply VAT deductions is not made dependent on the procedure for generating serial numbers of invoices issued by the seller when selling goods (works, services) .

Thus, the seller (supplier) has every right to independently determine the procedure for recording invoices and assigning serial numbers to them. The appropriate procedure simply needs to be stated in the organization’s accounting policies. For example, it is quite acceptable to “code” the month of issue when numbering invoices. That is, invoices issued in January are numbered 01-01, 02-01, 03-01, etc., in February - 01-02, 02-02, 03-02, etc. There should be no claims from the tax authorities against such invoices in the absence of other shortcomings.

At the same time, you need to be careful when entering letter suffixes in invoice numbers. We are talking about a situation where it is unclear in which layout the letter is “hammered in”. For example, the letter “X” looks the same both in English and in Russian, but... Let’s assume that the supplier indicates it in the English keyboard layout, and the buyer reflects it in the purchase book and in the VAT return - in Russian. It is obvious that when conducting a desk audit of VAT returns, tax authorities will not “find” the specified invoice when automatically comparing data from the supplier’s sales book and the buyer’s purchase book. And this will become the basis for demanding explanations from taxpayers.

March 2021

Invoice, VAT deduction

Consultations on the topic:

Storing electronic invoices

How many adjustment invoices should be prepared when goods are re-graded?

Who should keep a purchase ledger, a sales ledger, an invoice ledger?

Single adjustment invoice

USN: the counterparty asks the organization to issue a simplified invoice with VAT

Numbering rules

The main rule of numbering is assigning numbers in chronological order: numbers are indicated as they are assigned. Renewal of numbering is permitted. This is inevitable if a company has been in business for a long time. It is imperative to reflect renewal periods in the company's accounting policies. The period may be as follows:

- Month.

- Quarter.

- Year.

However, a government decree limits the resumption of numbering: it cannot be started from the beginning every day. This will be considered a violation.

The frequency of updates depends on the document flow of a particular enterprise. The more papers are filled out, the more often the numbers are renewed.

How to number invoices?

The numbering of invoices in 2021 - 2021 is carried out, first of all, on the basis of the rules enshrined in paragraph 1 of Appendix No. 1 to Government Resolution No. 1137 dated December 26, 2011. Moreover, in this document the numbering order is regulated differently, depending from the person who issues the invoice.

ATTENTION! As of January 1, 2019, a new invoice form is in effect. See here for details.

So, its compilers can be:

- An ordinary supplier of goods or services (as an individual entrepreneur, head office or sole office of a legal entity).

In this case, you must adhere to the following rule: the number of each account indicated in line 1 of the document is reflected in chronological order within the account turnover period determined by the document compiler. For example, month, quarter or year.

Linking an account to a specific period is usually done using a slash. For example:

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

- No. 1/2021 - the number of the very first account drawn up in 2021 (the next one will be No. 2/2021);

- No. 1/10/2020 is the number of the very first invoice drawn up in October 2021.

- A separate division of a legal entity.

In this case, the structure of the number should include the index established for the division and recorded in the accounting policy of the legal entity (clause 1 of the appendix to resolution 1137).

- A participant in a simple partnership or a trusted manager.

In this case, the account number includes the index defined in the agreement with the partner or manager. This index is also recorded in the accounting policy.

Types of invoice numbers

The numbers can consist of both numbers and letters. Letter designations must be present when document flow is in the following structures:

- Separate units. After the number you need to indicate the index in numbers. Values are separated by slash (/). The index is determined by the company and prescribed under a specific contract.

- People in a partnership or trustee managers. The index separated by a slash must be specified in this case as well.

Compliance with rules is important not only for the implementation of regulations. Correct numbering ensures orderly document flow and prevents confusion.

What types of invoices are there?

According to invoices there are the following types:

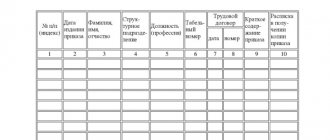

| Invoice type | When is it issued? | Normative act |

| Invoice | when selling goods (works, services), transferring property rights | |

| Adjustment invoice | when the cost of shipped goods (work performed, services rendered), transferred property rights changes downward, including in the event of a decrease in price (tariff) and (or) a decrease in the quantity (volume) of shipped goods (work performed, services rendered) transferred property rights, | |

| Invoice for prepayment (advance payment) | upon receipt of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights |

Features of putting down letter values

Some enterprises number advance and adjustment documents using different letters and numbers. For example, advance invoices are assigned the letter A, and adjustment invoices are assigned the letter B. This measure allows you to quickly find the necessary documents. However, it is not recommended to use the method in question, since there are no permissions for this in the law.

There is a risk that the buyer, upon discovering the letter designation, will require correction of the papers. A person’s motivation is to prevent problems from arising during a tax audit.

ATTENTION! There is a compromise method. You can assign both an official and an auxiliary number to an invoice. This measure will not be considered a violation. You can indicate the auxiliary number not only in the accounting program, but also in the document itself. However, the additional value does not need to be mentioned in the Number column. It is indicated after all the details in the “For reference” column. Permission to use additional numbers is given in letters from the Ministry of Finance.

Numbering Features

The main rule in filling out the numbering remains to be in chronological order. In other words, the data is displayed in accordance with the appearance of the documentation. Resumption of numbering is allowed. T

This phenomenon becomes common if the enterprise has been operating for a long time. When renewing, this period must be indicated in the enterprise’s reporting.

How to number invoices according to law? Watch the video:

These periods may be quarterly, monthly or annual. It is worth noting that the legislation has introduced restrictions on the renewal of numbering. Doing this more than once a month is not allowed and will be considered a violation.

What numbers can be used

Most often, alphabetic or digital variations of numbering are used.

If letters are used, they must follow established rules:

- They are separated by a special separate unit. After the written alphabetic symbol, the sign “/” is placed and then the index is written in numbers. The index number is determined by the enterprise itself.

- The indicated index must also be indicated if we are talking about a partnership or when working as trust managers.

Is it possible to cancel an invoice? More details at the link.

Why is it so important to comply with the rules for filling out documentation established by law? The point is not only in regulations, but also in the fact that by ensuring the correct approach to paperwork, the enterprise does not allow confusion to arise.

Letter numbering

The use of a letter system when filling out documentation is not uncommon. For example, advance invoices may be designated by the symbol “A”, while adjustment invoices may be designated by the letter “B”.

Such a system allows you to find and retrieve the necessary information in a short time. However, there is one thing. This form of filling is not reflected in the legislation in any way.

Law on invoice numbering. Photo nalog-nalog.ru

Thus, problems may arise with the client when providing such documentation. The buyer may ask to correct these designations and will be right in this regard. In addition, problems may arise during a tax audit.

Use of symbols in documentation: dot, dash

Everything is quite clear with the use of letters and numbers, but some enterprises add additional characters such as “dot” or “dash” to their numbering. Is it permissible to put these marks on an invoice?

To answer this question, you should refer to the main regulations governing numbering. It is worth noting that neither the 2011 Resolution nor the Tax Legislation contains a direct ban on these signs.

Thus, the conclusion suggests itself that these characters in numbering are acceptable; the main rule remains compliance with chronological order.

Is it allowed to put separate numbers on different invoices?

Is it permissible to put numbers separately on advance or adjustment invoices? The need for a unified chronology is established by the Decree of the Russian Federation of December 26, 2011, number 1137. Until this year, such a norm did not exist, and therefore accountants often put different numbering on invoices for shipments and prepayments. This procedure was considered the simplest, but is now prohibited. Otherwise, violations may be revealed during verification.

Separate numbering is also clearly prohibited by Letter of the Ministry of Finance of Russia dated October 16, 2012 N 03-07-11/427. If you want to highlight advance invoices, you can use a letter value. The letters must correspond to a single chronology, for example, these could be the values “A”, “AB”.

There are also separate standards for filling out adjustment tax forms. They must be listed in chronological order.

Penalty for incorrect numbering

Errors often occur when assigning invoice numbers. The most common ones are:

- Skipping numbers.

- Ignoring the need for chronology.

- Assigning the same number to the same document.

The last mistake is quite rare, since most accountants use special programs. The software prevents bifurcation.

Violation of the numbering order is the most difficult case. To correct the violation you will have to spend a lot of time and effort. An error in the chronology of one number leads to the fact that other numbers “creep”. It turns out that the invoices already sent to the buyer contain incorrect numbers.

Do the numbering need to be corrected? This measure makes sense if an error was made in the last number of the document, which has not yet been transferred to the buyer. If the error concerns a late number, it is not necessary to correct it. The seller does not bear any penalties for this violation.

ATTENTION! Article 120 of the Tax Code of the Russian Federation states that the absence of invoices for completed transactions entails a fine. These penalties do not apply to incorrect numbers. However, correct numbering is important in any case. This is taken into account during inspections.

Common Mistakes

It is easy to understand that no work is complete without errors, typos or typos. The same applies to numbering. One way or another, errors in filling out occur.

The most common ones are:

- Missing one or more serial numbers on documents;

- Deliberate disregard for chronological order in numbering;

- When the same license plate is listed on several different documents.

What mistakes are made when numbering invoices? Answer in video:

It is worth noting that the last of these errors does not occur so often, since accounting employees are quite meticulous in maintaining these reports or use specialized software systems.

If there is a violation of the ordinal chronology, then the situation is much more complicated. Even just one missing sheet will require restoring the entire system. Such errors should be corrected, especially if the documentation has not yet been transferred to the buyer.

How does incorrect numbering affect the buyer?

In most cases, incorrect numbering does not have any impact on the buyer. Errors don't bother you:

- identification of the parties to the contract;

- name of GWS, their cost;

- rate and total VAT.

That is, the buyer will not be denied a deduction, as stated in paragraph 2 of Article 169 of the Tax Code of the Russian Federation. If the controller makes his claims, they can be challenged, as evidenced by judicial practice. Based on court decisions, we can conclude that even the complete absence of numbering cannot be a basis for deducting VAT.