Definition

A conditional indicator that determines the assessment of the state of the enterprise's fixed assets and carries an analytical value is called the depreciation coefficient of fixed assets, otherwise - the depreciation coefficient .

Any fixed asset is subject to wear and tear over time, whether it is in use or simply kept idle. At the same time, its residual value decreases. The process of reducing value and transferring it to manufactured products - depreciation - occurs at different rates, which depend not only on the depreciation group to which a specific fixed asset is assigned, but also on the reporting period. For more information about this, see the material depreciation and amortization of fixed assets.

Results

The depreciation rate of fixed assets is used in conjunction with similar indicators to analyze the state of the company's fixed assets. This indicator is conditional and fundamentally depends on the depreciation write-off method chosen by the company. If it is too high, then, according to analysts, there is a high probability of a workflow failure and the OS needs to be upgraded.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Conventional wear coefficient

The value of this indicator is used for analytical accounting, and does not reflect the actual state of a particular fund. An asset that is not actually completely worn out may have a zero residual value. The reason for the conditionality is the dependence of the wear coefficient on the chosen method for determining depreciation charges. Thus, it shows not how much fixed assets are worn out, but to what extent they are depreciated.

IMPORTANT! If you need to evaluate the depreciation rate more objectively than simply taking into account depreciation, it must be compared with the corresponding data for the industry or correlated with similar data for this group of fixed assets from partners or competitors.

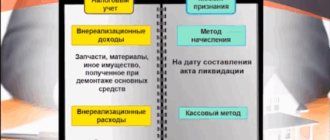

The depreciation rate of fixed assets can be calculated in relation to:

- physical depreciation of fixed assets;

- obsolescence of tools, equipment, etc.;

- the ratio of the residual value of funds and their market price.

Standard wear rate indicator

Legislative acts do not provide a standard value for the wear coefficient. Each enterprise determines the standard indicator individually, its value is fixed in the provisions of the accounting policy. Practice shows that most organizations consider the value of 50% to be the limiting rate of depreciation of fixed assets. What does it mean?

Let's say an enterprise accountant has calculated the wear rate of equipment in a production workshop, the result of the calculation is a value greater than or equal to 50%. In this case, the result indicates a high degree of wear and tear on fixed assets in this group and the need for their prompt replacement. If, according to the calculation results, an indicator below the level of 50% is obtained, this indicates that, in general, the degree of equipment wear corresponds to the established norm.

In this case, it is advisable to carry out a detailed analysis of the condition of the property. For example, you can conduct a technical inspection of each piece of equipment or analyze the condition of property by groups of fixed assets. This will make it possible to obtain more specific information about the state of fixed assets in the context of their structure.

Formula for calculating the depreciation rate of fixed assets

The depreciation rate of fixed assets is actually the ratio of the summed depreciation deductions to the original cost of a given fixed asset. It is calculated as a percentage, for which the calculated value must be multiplied by 100%.

The formula for calculating the depreciation rate is as follows:

Kizn. = ∑damper. / STperv. x 100%

- Kizn. – wear coefficient (depreciation coefficient);

- ∑shock – the amount of depreciation charges for the calculated period;

- STfirst – the initial cost of the fixed asset.

Data for determining the amount of depreciation, as well as the cost of the fixed asset, the depreciation rate of which needs to be determined, are taken from the organization’s financial statements.

ATTENTION! If modernization or improvement of a fixed asset was carried out, as a result of which its value was increased, then the final indicator, that is, the indicator increased as a result of the measures taken, will be used in calculating the depreciation rate.

Calculation example

Derevo-Stil JSC has 12 woodworking machines on its balance sheet. Their initial cost, reflected on the balance sheet in January 2021, is RUB 900,000. for each machine, that is, only 12 x 900,000 = 10,800,000 rubles. At the end of March, 3 machines were modernized, higher quality components were supplied, as a result of which the cost of each of the modernized machines increased by 25,000 rubles. Thus, the cost of 3 out of 12 machines was (900,000 + 25,000) x 3 = 2,775,000 rubles, and the remaining 9 machines are reflected on the balance sheet at a cost of 9 x 900,000 = 8,100,000 rubles.

The amount of depreciation charges for this group of equipment of Derevo-Stil JSC as of 04/01/2017 was equal to 4,005,620 rubles. Let's calculate the wear rate of equipment, just as an accountant would do.

To apply the formula, we need to know two indicators:

- the initial cost of the asset (in our case, we need to take into account the modernization), for which we sum up the book value of conventional and improved machines: 2,775,000 + 8,100,000 = 10,875,000;

- the indicator of accrued depreciation charges (according to accounting documents) - for JSC Derevo-Stil as of 04/01/2017 it is equal to 4,005,620 rubles.

We calculate the wear rate using the above formula: 4,005,620 / 10,875,000 x 100% = 37%.

Thus, the depreciation rate of these machines owned by Derevo-Stil JSC as of April 1, 2021 is 37%.

Wear factor: formulas and calculation examples

Both the manager and the owner seek to control the property they manage or own. One of the aspects of control is concern for the safety of objects owned or managed, and for this purpose in financial management, an indicator is used - the wear rate.

The concept of "wear and tear"

Wear is a negative change in properties and qualities:

- if we are talking about equipment, then these are changes that worsen the performance of the equipment - an increase in energy consumption and consumption of other resources (lubricating oils, consumables, etc.), the rate of defects when working with such equipment, corrosion, grinding of parts, an increase in the frequency of repairs and cost of maintenance, increased risk of injury;

- If we are talking about buildings, then we are also talking about the deterioration of the consumer properties of the premises - cracks and changes in the geometry of the foundation, damage and defects of the facade and roof, failure of ceilings and staircases, an increase in the number of unscheduled replacement or repair activities inside the building. For the consumer, these are drafts and leaks, sloped floors, mold in corners, uncomfortable temperature conditions and damage to furniture, equipment and other property.

It is also possible that it is not a physical deterioration in consumer properties, but their inconsistency with the current level of technological needs, for example, when it comes to computer technology - the power of a computer purchased two years ago may not be enough for a new graphics editor, or the image quality of a working kinescope monitor does not correspond to similar TFT monitors and no longer satisfies the designer.

Formula for calculating wear rate

The simplest estimate of the degree of physical wear can be made based on the standard service life of the product:

Kizn = Tfact / Tpi * 100%,

where Kizn is the wear coefficient,

Tfact – period of actual use of the product,

TSpi – useful life.

A machine whose useful life is stated to be 5 years is planned for sale. 2 years have passed since installation.

Then the wear rate of the machine is 2 / 5 * 100% = 40%.

The meaning of this indicator is that the machine has worked 40% of the period for which, according to the standard, it can operate as much as possible without loss of productivity.

Physical wear and tear can be assessed with high accuracy visually, using instrumental measurements and the involvement of experts, but moral wear and tear cannot be measured quantitatively. Involving experts and instrumental measurements is an expensive procedure that is not used as a method of regular monitoring; such research is done when selling or appraising property for other purposes, for example, as collateral.

Depreciation rate in financial management

In finance, the depreciation rate is calculated differently than for physical depreciation, although the result may be the same.

The formula used in accounting and financial management is based on depreciation - amounts regularly charged by accounting to expenses that reduce the value of fixed assets (see also how to revaluate fixed assets). According to economic logic and accounting principles, the organization is a going concern.

To ensure this, it is necessary to periodically replace equipment, and in order to have funds for this, management must form a fund for replacing equipment. The source of the formation of the fund for replacing equipment is depreciation charges.

Depreciation can also be considered as a transfer of the cost of fixed assets to products, but these two statements do not contradict each other - the second describes the principle of payment of depreciation payments.

How to calculate the depreciation rate of fixed assets

The formula for calculating the depreciation rate of fixed assets is as follows:

Kizn = ∑amort. /OS * 100%,

where ∑amort. – the amount of depreciation or accumulated depreciation,

OS – book value of fixed assets.

This is what the depreciation coefficient formula looks like for the purposes and objectives of accounting and financial management. Accrued depreciation plays a decisive role in the formula, and since the accountant calculates depreciation not based on the actual degree of depreciation, estimated in money, but on the basis of the accounting policy adopted by the enterprise, the essence of the indicator changes - it is not so much a criterion for assessing the depreciation of fixed assets, but an indicator of the share of accrued depreciation in the cost of fixed assets.

Let’s assume that a company has 10 machines purchased and put on the balance sheet for 10,000 thousand rubles each. per piece, the machines were operated for three years, the useful life is 5 years, depreciation is calculated using the straight-line method.

The amount of depreciation accrued over three years will be - (10,000/5*3)*10=60,000 thousand rubles.

The initial cost (book value) of fixed assets is 10 * 10,000 = 100,000 thousand rubles.

Wear rate – 60,000/100,000*100%=60%.

If, as a result of revaluation, modernization or other reasons, the value of the book value changes, then the new value of the indicator will also be used in the calculation and this must be taken into account during the analysis.

In our previous example, let's assume that two of the ten machines were modernized, as a result of which their book value increased by 2,000 thousand.

Depending on the date of modernization, the amount of accrued depreciation will change; if the improvements were made in the same period as they were placed on the balance sheet, then depreciation on the improved machines will be calculated from the increased book value.

If the modernization was carried out later, then depreciation will first be calculated at the original cost, and after improvements have been made and registered, at the increased cost. For simplicity, let’s assume that the amount of depreciation at the end of the third year for all machines was 62 thousand rubles.

Let's calculate the book value - 8*10,000+2*(10,000+2,000)=104,000 thousand rubles. Then the wear rate will be 62,000/104,000=59.6%.

Use in practice

There is no standard value for this indicator, but in your own accounting policy you can specify a limit value for the depreciation rate of fixed assets.

Despite the rather conditional relationship between the depreciation coefficient and the real depreciation of fixed assets, this indicator can be used, but to do this it is necessary to calculate it for different groups of assets separately, and in the company’s accounting policy to include and describe in detail the value of the depreciation coefficient at which it is necessary to begin to generate cash equipment replacement fund.

In Russia, the attitude towards depreciation and amortization is rather formal; it is believed that these are categories of non-monetary expenses that must be used for legal tax optimization (see also dangerous and safe VAT optimization schemes), and the accrued amounts should be used arbitrarily. However, in the West, depreciation is far from a formal attitude.

Interpretation

Certain norms for the depreciation coefficient are not prescribed in any legislative documents. As noted above, the meaning of this indicator is purely analytical. However, the standard value must be determined for each specific organization and recorded in internal documentation defining accounting policies. This means that the limit value of wear must be determined, at which the degree of “used” is considered high enough to begin to take any measures: make a decision on repairs or an immediate future replacement.

Additional indicator - suitability coefficient

To clarify the degree of wear and tear, along with the depreciation coefficient, the serviceability coefficient of fixed assets is calculated. It does not show the degree of depreciation, but part of the residual value of the asset in relation to the original (according to accounting documents). To calculate it, you need to divide the residual value (that is, the amount minus accrued depreciation) by the original cost of the asset (if improvements were made, then taking into account the increased cost). For a percentage value, multiply the result by 100%.

Kgodn. = STost. / STperv. * 100%

The lower the depreciation rate, the better the condition of the funds. With the serviceability coefficient, the situation is the opposite - the lower it is, the shorter the effective service life of the fixed asset will be.

The determination of the normative validity of the suitability coefficient is completely similar to the wear coefficient, the only difference is in the sign: for the wear coefficient the norm is set “not higher than” a certain percentage, and for suitability – “not lower”.

Indicators of the condition of fixed assets: example 1

The company acquired a fixed asset with a service life of 5 years.

The initial cost was 700,000 rubles. Calculate the indicators of the state of fixed assets at the beginning of the 4th year of operation if depreciation is calculated using the straight-line method. Annual = 700,000 / 5 = 140,000 rubles

Aza 3 years = 140,000 * 3 = 420,000 rubles

Kg = (700000 - 420000) / 700000 = 0.4

Ki = 1 - 0.4 = 0.6

Thus, this equipment is already worn out by 60 percent, and not worn out - by 40%.

If the depreciation method is linear, then these indicators can also be calculated through the depreciation rate.

For = (1 / 5 years) * 100% = 20%

Since the equipment has worked for 3 years, this means that wear and tear was 20% * 3 years = 60%. Therefore, the validity is 40%.

How to calculate the percentage of depreciation of fixed assets

The assets of a business entity have the property of wear and tear. To determine its degree, the depreciation coefficient of fixed assets of a business entity is used. The parameter is calculated based on information from accounting reports based on a given date. How to calculate the percentage of depreciation of fixed assets, what the resulting figure means, and how to apply this information in practice in analyzing the operation of the enterprise operating system.

general information

The amount of depreciation of company assets, which include buildings, equipment, machinery, tools and other items used in production activities, is identified by their depreciation rate.

All objects used in the enterprise are accounted for on the balance sheet. As they become obsolete, their value is lost, after which a write-off procedure is initiated. It is implemented by transferring the cost of the object to the products produced or services provided. When determining the amount of deductions to the depreciation fund, one of the methods regulated by regulations is used. At the same time, the residual value decreases with each reporting period; accrued depreciation is accumulated in a designated account.

The coefficient, which identifies the level of depreciation of the enterprise’s assets, makes it possible to determine how urgently it is necessary to carry out measures aimed at repair work or the complete replacement of individual objects.

With its help, you can determine the level of risks of stopping the production process, which is important for worn-out equipment. It is also necessary to determine the need for equipment modernization. Any management decision is made only after settlement transactions have been carried out, the results of which have been assessed and analyzed.

How to calculate the percentage of depreciation of fixed assets, formula

To determine how worn out the fixed asset is, calculations are made. The basic calculation values are:

- the price of the asset at which it was acquired, interpreted as its original cost;

- the time period, calculated in years, during which the use of the object is planned, which is identified by the useful life and is often regulated by regulations that take into account the time of operation without deterioration of characteristics;

- the cost of an asset transferred to cost through depreciation.

To determine the percentage of depreciation of assets, you should find the quotient of depreciation and initial cost. The resulting value should be adjusted to 100.

Example

The equipment was purchased for a million rubles. Its service life, during which no deterioration in performance is expected, is 10 years. The management regulated the linear method of calculating depreciation with a monthly frequency.

If the equipment has been in use for 5.5 years from the date of purchase, then depreciation will be 1000000X55/100=550000 rubles, and the percentage of wear and tear (55000/1000000)X100%=55%.

When calculating the degree of wear and tear of equipment, information is taken from the accounting records of the business entity. Accounting is required to provide data on the original cost of the object and what percentage of depreciation was accrued as of the date the parameter was determined. When carrying out calculations, not only physical wear and tear is taken into account, but also moral wear and tear. The residual value is also compared to the market value.

If the enterprise has revalued assets, then in the calculations it is necessary to take into account the replacement value and the full value when revaluing or depreciating the value.

The minimum value of the wear factor cannot be less than 50 percent. If the indicator is higher than this value, then we can judge that the wear and tear of fixed assets at the enterprise is high, which indicates the need to take measures to replace assets. During the analysis, one should take into account the specifics of the business entity’s activities, the values of the coefficients in the industry average and the possibility of an accelerated method of writing off assets.

How to determine the amount of depreciation of a fixed asset

Fixed assets are objects involved in the manufacture of finished products or in the process of enterprise management. The period of their useful use is longer than twelve months. Wear and tear is a fragmentary transfer of their value to the cost of products produced by the organization. In other words, this process is called depreciation. After studying this article, you will gain knowledge on how to calculate the amount of depreciation of fixed assets.

Types of wear

At the present stage, there are two types of wear:

- Functional wear and tear, the essence of which is that the main equipment has become obsolete, the reason for which is the achievements of science and technology. Therefore, the functionally worn-out main tool is the typewriter, because its operation is no longer relevant due to the invention of computer equipment;

- Physical wear and tear occurs when the main asset has worn out in material terms during use. An example of this is a woodworking machine, when its components are worn out and rusty.

Features of the depreciation calculation process

So that by the time the fixed asset wears out completely, the organization can buy or create a new one in its place, a special depreciation fund is created. Which is replenished every month with depreciation charges.

There are a number of principles when calculating depreciation that must be observed:

- It doesn’t matter whether the company made a profit or a loss, it still needs to accrue depreciation;

- Depreciation deductions must be made every month, and the first deduction must be made a month after the object is accepted for accounting;

- The company must stop making depreciation deductions one month after the final wear and tear or disposal of the fixed asset.

Methods for calculating depreciation

There are various methods for calculating depreciation of fixed assets. The organization itself must choose the appropriate method for each of the existing objects. Below is a detailed description of each of them.

- Linear - in order to calculate accumulated wear by this method, the following parameters should be highlighted:

- The primary cost of a fixed asset item (consists of the amount of expenses for the purchase of a fixed asset or the total cost of its creation);

- The useful life of a fixed asset (determined based on the classification list approved by the Decree of the Government of the Russian Federation);

- Depreciation rate (calculated by dividing one by the useful life and multiplying by one hundred percent).

Therefore, in order to calculate the amount of depreciation per month using the above method, it is necessary to perform a mathematical operation: multiply the initial cost of the asset by the depreciation rate and divide by twelve months.

- The next technique is reducing balance. In order to apply this technique, certain parameters are also required:

- Residual value (equal to the primary cost of the object minus accumulated depreciation);

- Useful life;

- Depreciation rate;

- Accelerating coefficient (assigned by the company; according to the rules, it cannot be equal to a number greater than three).

To calculate the amount of depreciation charges per year using the above method, you should do the following: multiply the residual value by the accelerating factor and the depreciation rate and then divide the result by one hundred. To calculate the monthly depreciation amount, divide the result by twelve.

- There is also a technique called “by the sum of the numbers of years of useful work.” To determine the amount of depreciation, this method uses certain data:

- Primary cost;

- Useful life;

- The sum of the numbers of years of useful work (calculated by summing the numbers of years of work). Let's give an example: if the period of operation of a fixed asset is three years, then the sum of the numbers of years of useful work is taken to be equal to six (one plus two plus three equals six).

To calculate depreciation charges using the above method, the following action is performed: dividing the number of years until final wear and tear by the sum of the numbers of years of useful work and multiplying the result by the primary cost of the asset.

- The last technique is proportional to the volume of manufactured products. The following parameters are used to calculate depreciation:

- Primary cost of the object;

- Actual volume of manufactured products in the current period;

- The total planned number of products produced.

Depreciation should be calculated using this method as follows: the primary cost of an item of fixed assets should be multiplied by the ratio of the volume of products produced in the period to their total planned volume.

Enterprises are allowed to decide on the appropriate method on their own. To avoid mistakes, it is necessary to correctly apply the useful life. To do this, you should carefully study the classification list.

Source: https://buh-spravka.ru/buhgalterskij-uchet/amortizaciya-iznos-os/kak-rasschitat-iznos-osnovnyh-sredstv.html

Depreciation rate of fixed assets - calculation formula

Related publications

When determining the degree of depreciation of an enterprise's assets, the depreciation coefficient of fixed assets (FA) is used. The indicator is calculated for a given date according to financial statements. Let's look at how to calculate the depreciation rate of fixed assets. We will also learn how to apply the information received in practice to analyze the performance of the company's assets.

What is the depreciation rate of fixed assets

The depreciation rate of fixed assets shows the extent to which objects - equipment, buildings, tools, structures, etc. - are depreciated. All fixed assets used by the enterprise in the accounting process are written off by assigning the original purchase price to the cost of manufactured products (services). When determining the amount of depreciation charges, one of the methods available under the legislation of the Russian Federation is used. In this case, the amount of the residual value of the depreciable object decreases, and on the account. 02 accumulates the amount of accrued depreciation.

Coef. depreciation of fixed assets helps determine the urgency of repair or complete replacement of the operating system, the presence of risks of stopping production processes due to high wear and tear of equipment, the level of reflection of the operating system in the balance sheet of the enterprise, the need to modernize assets, etc. Management decisions are made using CIOS after calculating the indicator.

How to calculate the depreciation rate of fixed assets

The calculation of the coefficient in % is carried out according to the physical wear and tear of the operating system, obsolescence of assets, as well as the ratio of the residual price data and the current market price in order to establish the correspondence of the cost. For calculations, you will need information from the organization’s accounting records, first of all, data on the accrued amount of depreciation and the initial cost of the objects.

If an enterprise revaluates assets in accordance with the norms of PBU 6/01, when determining the CIOS, one should take into account the amounts of the replacement cost and the total value obtained during the revaluation (depreciation) of objects. Since there are several ways to calculate depreciation for a company’s fixed assets, the results of the formulas for calculating the coefficient will vary depending on the depreciation calculation method, that is, indicator A.

Depreciation rate of fixed assets - calculation formula

In general, the depreciation rate of fixed assets is calculated as the ratio of the depreciation amount to the original price of the asset:

KIOS = A / PS x 100%, where:

A is the amount of depreciation charges accumulated as of the date of calculation (balance on account 02);

PS – the value of the initial purchase price of fixed assets (balance on account 01).

In addition to the CIOS, there is the wear and tear coefficient of fixed assets (KGOS). This indicator characterizes the technical condition of the object and is calculated as the ratio of the residual price to the original price.

KGOS = OS / PS.

Note! The minimum standard value of CIOS is on average 50%. If the indicator exceeds this level, the wear and tear of the enterprise's assets is high and replacement of assets is necessary. When analyzing, you should take into account the specifics of the organization’s activities, industry average values of the coefficient and the use of an accelerated method for writing off objects.

Standard value of the serviceability coefficient of fixed assets

Important! The values of the service life coefficient of fixed assets should be studied in dynamics over several reporting periods.

The higher the value of this indicator, the better the technical condition of fixed assets (now is the time to repair or change the property).

You should be concerned about the technical condition of a fixed asset if the value of the coefficient is less than 0.5 (when calculating the KGOS for the entire enterprise as a whole), since the standard value for this financial indicator is considered to be 0.5 or higher.

OS wear rate - calculation example

To clearly understand how the depreciation rate of fixed assets changes (the formula is given above), depending on the method of calculating depreciation, we will give a practical example of calculating the indicator.

Let's assume that the LLC has 5 processing machines on its balance sheet. The equipment was purchased in December 2021, the initial cost of each was RUB 250,000, total RUB 1,250,000. The machines were put into operation on 01/01/17. The service life is set at 7 years. Planned production volume for 7 years = 280,000 units. Let's consider how the calculation of CIOS for the first year of operation will change depending on the depreciation calculation method. The calculation was made for all machines:

- Linear method - depreciation for the year = 178,571.43 rubles. (1,250,000 / 7 years). At the same time, KIOS as of December 31, 2017 = 178,571.43 / 1,250,000 x 100% = 14.28% - the degree of wear is within normal limits.

- Reducing balance method – depreciation for the year = RUB 1,250,000. x (100% / 7 years) = 178,625 rubles; KIOS = 178,625 / 1,250,000 x 100% = 14.29%.

- Write-off method according to SPI - depreciation for the year = 1,250,000 rubles. x 7 years / 28 years = 312,500 rubles; KIOS = 312,500 / 1,250,000 x 100% = 25%.

- In proportion to production volume - depreciation for the year = 1,250,000 rubles. x 45,000 units (volume of products actually produced in 2017) / 280,000 units. = RUB 200,892.86; KIOS = 200,892.86 / 1,250,000 x 100% = 16%.

Note! The coefficient of physical depreciation of fixed assets is determined taking into account the real obsolescence of objects, that is, the amount of not only accrued depreciation, but also actual.

Depreciation and serviceability rates of fixed assets in 2019

Fixed assets tend to wear out, gradually losing their operational properties. Eventually, complete wear and tear occurs, after which the object is written off and is no longer used. To assess the condition of objects, it is necessary to carry out regular calculations of such indicators as the wear rate and the serviceability rate of fixed assets. The first shows the degree of wear and tear of the object, clearly demonstrating how depreciated the OS is. The second provides additional information about the state of the funds. These coefficients can be calculated using special formulas. Calculation formulas are given below, and the calculation of wear and serviceability coefficients is discussed using an example.

For what purpose is the serviceability ratio of fixed assets calculated?

A significant factor when studying the condition of a fixed asset is its service life, since the degree of wear and tear of the property, which affects the suitability of the given object for the production process, depends on the period of time of use of the fixed asset.

Internal analysts and external financial experts, when analyzing the activities of companies, are also involved in studying the value of the asset's usefulness coefficient - it helps to understand what proportion of the initial cost of the asset is the residual value of the property for the reporting period. Thanks to the CG, it is possible to find out what is the proportion of worn-out fixed assets in relation to the total fleet of the enterprise.

Having an idea of the state of fixed assets, the company's management has the opportunity to plan further steps towards improving and updating equipment. In addition, the management staff can make an informed decision on replacing physically and morally obsolete fixed assets.

Important! The serviceability ratio of fixed assets is a one-time indicator, i.e. it allows you to assess the physical condition of fixed assets only directly on the date of calculation.

How to calculate the depreciation rate of fixed assets - calculation formula

Calculation formula:

OS wear coefficient = A / PS * 100%,

- A is depreciation accumulated at the time of calculation. The indicator is taken from the credit of account 02;

- PS is the initial cost of the OS. If revaluation, modernization, reconstruction were carried out, which changed the initial cost indicator, then you need to take the cost taking into account these changes. That is, this is the indicator that is reflected in the debit of account 01.

Based on the formula, it can be seen that the higher the wear rate, the more worn out the equipment; the higher the depreciation charges, the more worn out the fixed asset.

The coefficient can be calculated to determine the wear and tear of the physical and moral condition of objects.

Why is it needed : the indicator allows you to assess the condition of fixed assets, plan further actions to improve and update equipment, and decide on the advisability of replacing fixed assets with new ones. That is, the value of the wear rate makes it possible to rationally analyze the assets of the enterprise in order to develop a further development strategy.

Example of wear factor calculation

The company has 10 cars on its balance sheet, each object is recorded in the debit of account 01 at its original cost, the total value of which is 4,600,000 (460,000 each). An improvement was made to one car; the body was replaced with a more convenient and functional one; this change led to an increase in the initial cost of the car to 630,000 (by 170,000). As a result, the total cost of fixed assets was equal to 4,770,000.

The accumulated depreciation on the credit of account 02 as of the date of calculation of the coefficient is 1,630,000.

Calculation:

It is required to calculate the depreciation rate of cars. To do this, we calculate using the formula:

CI = 1630000/4770000 *100% = 34%

Conclusions:

What conclusion can an accountant make after making such a calculation?

The degree of depreciation of the company's vehicle fleet is 34%, that is, roughly speaking, fixed assets are depreciated by a third. How much such an indicator suits the company is up to it to decide. There are no normative values established by law. No recommendations are given regarding at what wear rate the equipment should be replaced. Each enterprise determines its own standard depending on the type of equipment, fixed assets, and its financial capabilities.

Sometimes it is better not to wait for the OS to completely wear out, when its performance properties are completely lost. Sometimes, it is much more profitable to upgrade equipment to obtain maximum operating efficiency, and write off the old facility as an expense. The feasibility of these actions is assessed during economic calculations.

The company needs to develop acceptable standards for the depreciation rate and consolidate the results in its accounting policies.

In practice, the limit after which measures to renew the fixed assets fleet usually follows is a depreciation rate of 50%. It is believed that if the coefficient is over 50%, the equipment is very worn out and does not provide the proper economic effect from its use.

The value of 34% obtained in the example shows that the cars are not worn out enough to require replacement. In general, the indicator is within the normal range.

Please note that this calculation does not provide an accurate representation of the condition of individual objects. It is possible in some situations to conduct a more detailed analysis of each individual fixed asset to determine the degree of its deterioration. Only a comprehensive analysis will allow you to make a rational decision.

Formula for calculating the OS suitability coefficient

Formula for calculation:

Fit factor = OS / PS * 100%,

- OS - residual value, defined as the difference between the initial and accumulated depreciation charges;

- PS is the initial indicator of the cost at which objects are listed on the balance sheet.

Depreciation of fixed assets

Depreciation of fixed assets is a gradual transfer of the value of fixed assets to the cost of finished products, work performed or services provided in the form of monthly depreciation charges. Depreciation is a cost expression of the degree of wear and tear. The monthly calculation of depreciation and the inclusion of its amounts in the cost of products, works and services is the process of recoupment of fixed assets. The company includes a few kopecks of depreciation into the entire ruble of revenue and earnings. This is the financial return of fixed assets, that is, when a fixed asset is capable of bringing economic benefit to its owner. The amount of depreciation is also reflected in the sales price of finished products, work performed or services rendered, which is ultimately paid by the final buyer. Depreciation of fixed assets can be calculated in linear and non-linear ways. In accounting, it is allowed to use any methods of calculating depreciation at the organization’s discretion; in tax accounting, only linear methods can be used. The depreciation methods used at the enterprise are established by accounting policies for accounting and tax accounting purposes. The degree of depreciation shows how often the enterprise renews its fixed assets. Depreciation must be less than 50% of the total cost of fixed assets. If wear is more than 70%, then the organization needs to update or modernize production facilities; otherwise, a high degree of wear can negatively affect the production cycle and product quality, causing interruptions and downtime in the production process. And this, in turn, will affect the amount of revenue and sales proceeds of the enterprise.

The condition of fixed assets reflects their technical suitability for subsequent operation. Worn-out fixed assets often require urgent or major repairs, improvements can cause interruptions, downtime in the production process and product defects. Therefore, it is important for enterprises to monitor their condition with the support of calculating special indicators.

The main indicators that are used when assessing the condition of fixed assets are the wear rate and the serviceability rate.