Is VAT included when returning a train ticket?

When accounting for expenses to reduce the taxable base for income tax, expenses should be:

- Executed in forms permitted by law.

- Economically justified - committed as part of an activity aimed at making a profit.

- Confirmed by documentary forms.

In document flow, it is allowed to use a non-documentary form - electronic tickets (ETTs). Documents are purchased by non-cash online payment. Having a document is not enough to confirm expenses and the fact of travel.

To certify the actual receipt of services on railway transport, you must have a route/receipt, boarding pass. The fact of payment is confirmed by an extract from the electronic system - a control coupon.

Refund amounts and commissions when returning train tickets applications for refunds for an unused train ticket To receive your own money spent on purchasing a ticket, you need to provide:

- If a boarding pass printed on the ticket form was previously issued, then it should also be attached to the package of documents along with the passport;

- Internal Russian passport (required to confirm identity);

- Also provide your passport number;

- Submit the document package to the ticket office that handles refunds for tickets.

- Electronic travel document or order number;

It is worth paying attention to the fact that you can only return an electronic ticket that was purchased for an international destination (for example, to Europe) at ticket offices that sell international tickets. The document is subject to verification by an accounting employee, approved by the manager and submitted to the cash desk for settlements.

In organizations, orders set reporting deadlines. The period for business trips is calculated from the date of arrival.

The inclusion of travel expenses in the composition of expenses of the Tax Code of the Russian Federation establishes the right to include expenses for business trips, including travel expenses, in the composition of expenses (clause 12, paragraph 1, Article 264 of the Tax Code of the Russian Federation). Amounts are accepted as part of other expenses.

One of the main tasks when writing off expenses is to confirm the need for a business trip, for which a job assignment is developed and approved.

4 p. 3 art. 170 Important Tax Code of the Russian Federation; P.

14 Rules for maintaining a sales book, approved. Government Decree No. 1137 dated December 26, 2011. You recognize the excess amount of the fee recognized as expenses in income.

The fee that the carrier withheld upon return

VAT on Russian Railways tickets

Many companies send their employees on business trips; upon return, the latter are required to report their expenses using strict reporting documents, including air and train tickets.

A reasonable question arises: is it possible to deduct VAT on tickets in 2021, for which in most cases no invoice is issued.

The Ministry of Finance of the Russian Federation answered this question as follows: in order to deduct VAT from railway and air tickets, the ticket form (paper or electronic) must have a line with the specified tax amount.

So, if the ticket says “including VAT”, but the amount itself is not deciphered, usually accountants write off the entire cost of the ticket as expenses, in full.

However, doing so is dangerous. It is necessary to determine VAT by calculation and exclude it from costs. If the ticket does not say anything about VAT, you can include the entire cost of the trip as expenses. Find out how to confirm your flight without a boarding pass. From January 1, 2021, the VAT rate on domestic rail transport has decreased to 0%.

The zero rate applies to the transportation of passengers and baggage both on commuter trains and long-distance trains (clause 9.2, clause 3, clause 1, article 164 of the Tax Code of the Russian Federation). However, additional services, including food, water, bed, and newspapers, are subject to a VAT rate of 18%. In a letter

“On the procedure for applying VAT rates in relation to the cost of services included in travel documents for the transportation of passengers and luggage by public railway transport in domestic traffic”

JSC Russian Railways has undertaken to reflect VAT on tickets by rate.

That is, the ticket must contain two lines with VAT amounts: separately VAT at a rate of 0% on passenger transportation and at a rate of 18% on additional fees and services.

If the ticket contains the total amount of VAT without details, the accountant may have difficulty accepting the tax for deduction, since VAT on the passenger’s meals cannot be taken into account.

What should I do?

- Russian Railways was obliged to include VAT details on tickets, but to this day this is not always observed.

- The Federal Tax Service allows you not to break down VAT in the purchase book, but to take it into account as a whole

- Most often, food is included in the cost of services, VAT on which can be deducted

- Make a request to Russian Railways with a request to decipher the tax, but this will cost the company money.

In most cases, VAT can be deducted from Russian Railways tickets in 2020 without additional detail. When a posted employee provides an air or railway (paper or electronic) or a receipt for the purchase of a ticket with the amount of VAT indicated on it, the company has the right to accept this VAT as a deduction if its activities are subject to VAT.

Acceptance of service fees for the purchase of train tickets

Source: https://gordeychik.ru/vkljuchaet-li-nds-sbor-pri-vozvrate-zhd-bileta-19029/

VAT refund for legal entities when purchasing an air ticket

, prepare invoices, record purchases and sales, prepare a tax return. And they have the right to use deductions in the amount of tax claimed by suppliers and appearing in a number of individual situations.

It is important to remember that in order for the fact of VAT refund to be detected, you need to go through the entire process, which is established by law.

When reimbursing the amount, the taxpayer is obliged to adhere to the latest version of the Tax Code of the Russian Federation. She, in turn, prescribes that it is necessary to use tax withholding in the process of filling out the relevant documents.

Taking this into account, the tax deduction is calculated as part of the cost, which will provide for a reduction in the tax required for payment. In order to be able to use the right to tax compensation, the taxpayer must calculate the amount of payment as correctly as possible.

Features of VAT refund for legal entities

In 2021, the tax rate is 18%, but it may be increased in the future.

VAT applies to almost all types of goods and services, however, there are exceptions.

A reduced rate of 10% is charged on children's products, medicines, and food products. Products for export - export are not subject to this tax.

Despite the fact that entrepreneurs pay the tax, the money is collected from buyers.

The receipt must indicate the amount of VAT in a separate column. As an example of VAT calculation, the following scheme can be given: An enterprise orders material for the manufacture of its goods from another company.

When paying for materials, VAT is applied.

Then, the goods are transferred and a price is set, taking into account the funds spent on production.

VAT on tickets in 2021

A reasonable question arises: is it possible to deduct VAT on tickets in 2021, for which in most cases no invoice is issued.

The Ministry of Finance of the Russian Federation answered this question as follows: in order to deduct VAT from railway and air tickets, the ticket form (paper or electronic) must have a line with the specified tax amount.

So, if the ticket says “including VAT”, but the amount itself is not deciphered, usually accountants write off the entire cost of the ticket as expenses, in full. However, doing so is dangerous. It is necessary to determine VAT by calculation and exclude it from costs.

If the ticket does not say anything about VAT, you can include the entire cost of the trip as expenses.

The letter from the Ministry of Finance notes: In addition, the Ministry of Finance spoke about income tax.

The department explained that in the case under consideration, the full cost of tickets is taken into account when determining the tax base. Experts emphasized: Let us recall that the procedure for VAT refund is regulated by the Tax Code of the Russian Federation.

Detailed information on issues related to paying taxes can be found on our website in the section. It provides information about the tax base, rates, benefits and tax deductions, etc.

Upcoming tax payment dates, submissions

VAT deduction based on air tickets

Taking into account the above provisions, as well as the fact that individuals are not payers of VAT and do not accept it for deduction, the Federal Tax Service of Russia indicated that when providing passenger transportation services on the basis of an air ticket paid by individuals by bank transfer, in which the amount of VAT is highlighted in a separate line , the airline may not issue invoices. Regarding the application of deductions based on air tickets.

Paragraph 1 of Article 172 of the Code establishes that deductions of tax amounts are made on the basis of invoices issued by sellers when selling goods (work, services), or on the basis of other documents in the cases provided for in subparagraphs 3, 6–8 of Article 171 of the Code. According to paragraph 7 of Article 171 of the Code, amounts of value added tax paid on business trip expenses accepted for deduction when calculating corporate income tax are subject to deductions.

How to deduct VAT on electronic train and plane tickets

Thus, VAT paid on the purchase of tickets for business travelers can be deducted on the basis of the BSO with an allocated tax amount. If an employee makes a business trip using an electronic plane ticket, then such a BSO is the route/receipt of the electronic passenger ticket (clause 2 of the order of the Ministry of Transport of Russia).

If he goes on a business trip by train using an electronic railway ticket, then the strict reporting form is the control coupon of the electronic travel document (ticket) (clause 2 of the order of the Ministry of Transport of Russia).

Thus, printouts of the following documents are recognized as the basis for deducting VAT: - itinerary receipt of an electronic plane ticket with the allocated tax amount; — control coupon for an electronic train ticket with the allocated tax amount. Similar clarifications are contained in letters from the Ministry of Finance and .3 546 Discuss on the forum3 5463 546 Discuss on

Rebus Company

2 of Order No. 134.

And when checking in for a flight, the passenger also receives a boarding pass, which confirms the very fact of transportation. It indicates the initials and surname of the passenger, flight number, departure date, boarding deadline for the flight, boarding gate number and seat number on board the aircraft (clause 84 of Order of the Ministry of Transport of Russia dated June 28, 2007 No. 82).

Due to the fact that both documents - the control coupon and the itinerary receipt - are recognized by the BSO, each of them must contain mandatory information. Which one is shown in the diagram.

“On the establishment of forms of electronic travel documents (tickets) for railway transport”

.

“On establishing the form of an electronic passenger ticket and baggage receipt in civil aviation”

.

In order to correctly reflect the cost of electronic tickets in tax accounting, an accountant needs to know some of the nuances associated with these travel documents.

On the application of VAT deductions for the purchase and return of air tickets

As stated above, deductions of tax amounts presented by the seller to the buyer are applied to purchased goods (works, services), property rights used for transactions subject to VAT.

Considering that when returning an air ticket and paying a fine to the airline for returning the ticket, there is no fact that the organization purchased transportation services, therefore, the purchasing organization does not have the right to deduct VAT amounts.

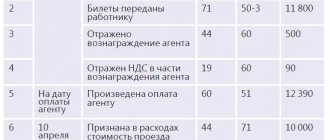

How to reflect the return of an air ticket by a legal entity in the accounting records of a travel agency? Let's show with an example... EXAMPLE An organization transferred 15,000 rubles in advance to a travel agency. to purchase an air ticket for a regular flight.

The amount of the agency fee of a travel agency for selling a ticket is 5 percent of its cost, or 750 rubles. (including VAT - 114.41 rubles).

The travel agency transfers the cost of the air ticket to the airline minus the reward. Five days before the flight, the purchasing organization canceled the trip.

According to the terms of the agreement with the airline, for a returned ticket five days before the flight, the travel agency pays a fine of 20 percent of the ticket price (excluding remuneration).

Additionally, we note that the penalty for returning a ticket for a regular flight is set by the carrier itself.

Its size depends on how long before the flight the passenger canceled the ticket, the fare at which the ticket was sold, and other factors.

4.10. Deduction of VAT amounts based on electronic tickets

7 tbsp.

171 of the Tax Code of the Russian Federation: “tax amounts paid on business trip expenses (travel expenses to the place of a business trip and back... accepted for deduction when calculating corporate income tax) are subject to deductions.”

It should be noted that the procedure for applying the VAT tax deduction will vary depending on the method by which air transportation is purchased - by purchasing a ticket by an employee of an enterprise as an individual in cash or through a non-cash payment on behalf of a legal entity.

If an employee purchases an air ticket in cash.

According to paragraph 7 of Art.

168 of the Tax Code of the Russian Federation: “when selling goods (work, services) for cash... directly to the public... the requirements for preparing payment documents and issuing invoices are considered fulfilled if the seller issues the buyer a cash receipt or other document in the established form." The Tax Code itself does not specify what other documents can replace an invoice for travel expenses.

At the same time, according to paragraph.

Business tickets purchased through an agent: let’s see what happens with VAT and profit

Your organization can deduct input VAT from the ticket price based on the ticket itself, if the tax amount is highlighted on a separate line in it.

An invoice is not required for this, , ; , . If you purchased an electronic ticket with allocated VAT, then a printout of this ticket and boarding pass is sufficient. Selenko Irina, Moscow When purchasing tickets through an agency, the company received an invoice for the amount of the service fee for issuing tickets.

Do I need to wait until the end of the business trip to deduct VAT on the agency fee and write off the cost of the fee itself as an expense? : No, you don’t need to wait until the end of the business trip. After all, the service fee is a remuneration to the intermediary for his services, and they have already been provided.

This fee can be immediately written off as other expenses; .

There is no need to wait until the end of the trip and approval of the advance report (as is required for recognition of travel expenses in “profitable” accounting).

Purchasing tickets from an agent may exclude the deduction of VAT paid for them.

Accordingly, the payment was made taking into account the tax, as evidenced by the payment orders. In the invoices issued by the company to the customer, the amount of VAT is also highlighted. But VAT is not indicated on the tickets themselves.

The company considered that it could deduct tax on purchased tickets on the basis of invoices (bills and payment documents), even if it was not indicated directly in the transportation documents.

Source: https://GarantR.ru/vozvrat-nds-dlja-juridicheskih-lic-pri-pokupke-aviabileta-50016/

Purchase of an electronic ticket by an employee for cash on passenger transport

The forms of electronic travel documents (tickets) for railway transport are approved by Order of the Ministry of Transport of Russia dated August 21, 2012 N 322 (hereinafter referred to as Order N 322).

According to clause 2 of the Order, the control coupon of an electronic travel document (ticket) (extract from the automated control system for passenger transportation on railway transport) is a document of strict accountability and is used for organizations and individual entrepreneurs to carry out cash payments and (or) payments using payment cards without use of cash register equipment.

Therefore, the rationale for applying a deduction for an electronic ticket on passenger transport is similar to the situation associated with the purchase of an electronic ticket.

Taking into account the above, we can conclude that if in an electronic passenger ticket printed on paper, the amount of VAT is highlighted as a separate line, then the tax deduction is legal.

In this case, the control coupon (extract from the automated system) with the VAT amount highlighted in a separate line is registered in the purchase book and is the basis for accepting this VAT amount for deduction.