Procedure for issuing financial assistance

In its internal documents, the company prescribes the conditions and documents necessary to receive financial support. But even if the company’s regulations do not contain a specific life situation, the company can still provide assistance and support.

does not establish a clearly defined procedure for issuing financial assistance . Each employer independently approves this procedure.

Based on practice, we can say that in order to receive financial assistance, an application is initially written to the head of the company. Because only he makes a decision on the need to provide financial support to an employee. The exception is the situation when the general director himself needs financial assistance. In this case, the decision is made by the owners of the company or members of the board of directors.

In what cases is financial support required by law?

It is not the employer's responsibility, it is only his right. Such payments are one-time in nature. The basis for issuing money is the corresponding order.

The list of situations when an employee can receive support is indicated in the local documents of the enterprise and in the employment contract. Typically, the manager issues a Regulation on Financial Assistance, which lists the situations when the employee will be provided with financial support. The document also prescribes the procedure for allocating assistance, etc.

Most often, financial support is provided to an employee in connection with:

- with treatment;

- with the death of a close relative;

- with the death of the employee himself;

- with damage caused by an emergency;

- with marriage;

- with the birth of a child.

How to draw up an order for financial assistance

In this article we will analyze the situation when an employee needs financial assistance.

Any decision of the manager is formalized in an administrative document - an order or directive. Payment of financial assistance is also carried out on the basis of an approved order.

Of course, in small companies with a small turnover, you can get by with the director’s approval of the employee’s application. However, in most cases it is better to formalize the decision with an order for the payment of financial assistance.

The form of the order is not established . Therefore, you can use your own, which is used to formalize management decisions.

Next, we will consider a sample order for the payment of financial assistance to an employee.

Order for payment of financial assistance - sources of legal regulation

Among the legally significant documents that must be relied upon when issuing an order for the payment of financial assistance are the following:

- Labor Code (hereinafter referred to as the Labor Code);

- departmental regulations in relation to various categories of workers (municipal employees, cultural workers, teaching staff, etc.);

- collective agreement concluded between the enterprise and its workforce (if any);

- instructions for office work in the organization;

- procedure or provision for providing financial assistance to employees.

In particular, labor legislation (Article 8 of the Labor Code) establishes the right and obligation of the employer (except for cases when it is an individual, that is, a person who does not have the status of an individual entrepreneur) to issue local legal acts on labor issues. In Art. 135 of the Labor Code establishes the rules for the formation of wages, the procedure for fixing additional guarantees for the employee and paying bonuses. At the same time, the collective agreement Art. 40 of the Labor Code is defined as an act regulating social and labor relations, which allows for the possibility of establishing material assistance to employees precisely as social assistance, and not as an incentive payment in the form of a salary supplement.

ConsultantPlus experts tell us whether it is possible to take financial assistance to an employee into account in income tax expenses. Get trial access to the system and move on to the Ready-made solution.

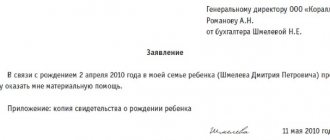

An example of an order for the provision of financial assistance

Due to the fact that there is no , it is drawn up in any form. You need to use the form that the company uses as an element of personnel document flow.

As with any order, the document for the provision of financial assistance must indicate the basis or reason . For example:

“in connection with marriage/due to difficult financial situation/in connection with the birth of a child/”, etc.

Do not forget to indicate the basic details in the order:

- name of the employer indicating the organizational and legal form;

- place, number, date of registration of the order;

- link to a local or regulatory document;

- basis for providing assistance;

- position and full name employee assigned to support;

- amount and terms of payment;

- attachment – supporting documents.

The reason for indicating in the order is taken from the employee’s statement.

So that there are no questions left, we have prepared an order for the payment of financial assistance, a sample of which you can download and fill out when issuing financial assistance to your employees.

Contents and sample order for the issuance of financial assistance

Based on the sources of legal regulation relating to the issuance of an order for financial assistance and its payment in general, as well as the established practice of social and labor legal relations, this legal act of the organization must contain:

- name of the organization or individual entrepreneur issuing the order;

- details of the document (place of signing, date of publication, identification number in accordance with the nomenclature of cases and rules of office work);

- grounds for issuing the order - a list of documents in accordance with which the decision to allocate assistance was made (including those regulating the implementation of this payment);

- circumstances in connection with which social assistance is provided to an employee (birth of a child, registration of marriage, death of a family member, illness, etc.);

- position held by the employee, exact place of work (branch, structural unit), full name;

- the exact amount of assistance provided, indicated in Russian rubles;

- instructions for accounting (accrual, payment procedure and terms, etc.);

- list of annexes to the order;

- other information in accordance with internal rules and specific circumstances (assignment of control over execution, procedure for entry into force, etc.).

There is no legally established form for this document, which can cause difficulties in the absence of practice in its publication. On our website you can order a free order for financial assistance, which will help you avoid common mistakes.

How else can you apply for financial assistance?

If the company provides for the payment of financial assistance when an employee goes on vacation, there may not be an order to assign financial support. An internal act may provide that the basis for payment of financial assistance for vacation is an order to provide annual leave for a period of at least 14 calendar days.

You can also specify the frequency of payments. That is, for example, an employee can receive payment for vacation only once a calendar year. If an employee does not take his required vacation this year, he loses the right to additional payment. Thus, they also encourage their workaholics to rest as they should.

An employer may decide to provide financial assistance to all employees regardless of their financial status. This is not prohibited . It is now very important to provide assistance for the purchase of drugs for the prevention and treatment of ARVI, and personal protective equipment.

All companies are required to provide their employees with PPE in the workplace. However, during the raging coronavirus pandemic, it is necessary to protect yourself outside of work. This can be organized by issuing material assistance in cash or in kind (masks, gloves, disinfectants).

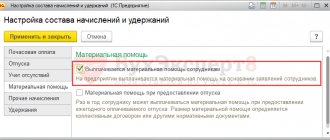

Material aid

The order is drawn up based on the employee’s application for financial assistance. There can be many situations in which financial assistance is needed, for example:

- pregnancy, childbirth of an employee or employee’s spouse;

- marriage;

- illness, injury;

- recovery after severe treatment, the need for special expensive food, sanatorium treatment;

- force majeure, natural or other disasters.

By the way! One-time financial assistance can also be provided to former employees of the company for the same reasons.

Copies of the following documents can confirm the grounds for payment:

- containing expenses for treatment, purchase of medicines, including doctor’s prescriptions (Article 217 of the Labor Code of the Russian Federation, clauses 10-1, 28-5);

- death certificates;

- certificates, certificates, similar documents confirming force majeure circumstances, disasters;

- marriage certificates;

- child's birth certificate, medical certificate of pregnancy.

If financial assistance is provided in connection with going on vacation, a separate application is not drawn up.

When issuing an order to provide one-time financial assistance, it should be remembered that the rule “any material assistance over 4,000 rubles is subject to personal income tax” does not work for some types of such payments (Article 217 of the Labor Code of the Russian Federation), in particular, if we are talking about natural disasters, emergencies, medical problems. At the same time, payment of the total amount specified in the order in several parts does not violate its “one-time” nature, but several amounts issued under several orders with reference to the same reason do.

In practice, the fiscal authorities recognize the first such payment as a one-time payment, but subsequent ones no longer. They need to pay income tax.

You cannot issue an order for one-time financial assistance to pay for good work, bonuses, especially regular ones. During an inspection, inspectors will recognize such payments as a reward for work and will require payment of income tax and contributions to funds.

For your information! According to Art. 40 of the Labor Code of the Russian Federation, social payments, including financial assistance, may be reflected in the collective agreement.

The provision of material assistance is prescribed in departmental and interdepartmental NA (if any) of certain categories of employees: teachers, cultural workers, etc. There is also the publication of individual LNA of the company, reflecting the procedure for providing one-time financial assistance.

Order for financial assistance: sample in free form

For an order to provide financial assistance, the sample is not established at the legislative level, so it can be issued in free form. The following mandatory details must be entered into it:

- Full name of the organization.

- Name of the administrative document.

- Date and document number.

- Preamble, which sets out the legal basis for providing financial assistance.

- The text of the order, which states who receives financial assistance and indicates its amount.

- Date and signature of the manager.

The original order for the issuance of financial assistance refers to orders for personnel; it is registered in the appropriate book and stored for 75 years if issued before 2003, and 50 years if issued later. A copy of it is provided to the accounting department in order to credit the employee with the required amount. Paid financial assistance does not reduce the tax base for calculating income tax (clause 23, article 270 of the Tax Code of the Russian Federation).

Documents and grounds for drawing up an order for the provision and issuance of assistance

The list of grounds and procedure for allocating assistance should be determined by the regulations in force in the organization. In this case, the interested employee will need to submit an application requesting the necessary assistance, as well as documents confirming the facts that formed its basis.

The reason for such bureaucratic delay is not the lack of trust in the employee, but the requirements of Art. 217, 422 of the Tax Code of the Russian Federation, which determine the list of situations when tax (insurance contributions) is not levied on such payments. For example, at the birth of a child in accordance with clause 8 of Art. 217 of the Tax Code of the Russian Federation, the administration of an organization can pay an employee up to 50,000 rubles without charging personal income tax.

As for the order itself, we list the documents, the presence of which will greatly simplify the process of preparing it. This:

- general situation in the organization;

- employee statement;

- a document confirming the reason for the employee’s request for help;

- a manager's decision (resolution) on a specific issue.

We emphasize that these are desirable, but not mandatory documents, the presentation of which is required in accordance with the Labor Code of the Russian Federation or regulations. However, if on their basis an exemption from personal income tax or contributions to the Social Insurance Fund is planned, proper compliance with the procedure is in the interests of both the employee and the organization’s administration.

The decision on the use of net profit is made by shareholders

The founders of the organization (participants and shareholders) can use part of the net profit to pay financial assistance. Such a decision of the founders must be documented.

Please note : Financial assistance is a payment made by an organization in favor of individuals. Including employees, their relatives and strangers. Payment of financial assistance may be associated with a difficult life situation, the birth of a child, or the death of a family member. Also, financial assistance can be issued for vacation, professional holiday, etc.

If the organization has one founder, then the allocation of part of the profit for the payment of financial assistance is formalized by the decision of the sole founder (Clause 3, Article 47 of the Federal Law of December 26, 1995 No. 208-FZ, Article 39 of the Federal Law of February 8, 1998 No. 14-FZ).

If there are several founders, then you need to draw up minutes of the general meeting of participants (shareholders) (Article 63 of the Federal Law of December 26, 1995 No. 208-FZ, paragraph 6 of Article 37 of the Federal Law of February 8, 1998 No. 14-FZ).

When funds are allocated, the head of the organization can decide to pay financial assistance, guided by the circumstances (clause 2 of article 69 of the Federal Law of December 26, 1995 No. 208-FZ, subclause 4 of clause 3 of article 40 of the Federal Law of 02/08/1998 No. 14-FZ) (for more details, see “Providing financial assistance to an employee”).

Bonus and financial assistance for the New Year

On the eve of the holidays, many employers encourage their employees. Published in the magazine “Accounting News” No. 45 dated December 4, 2012

Author: Irina Sidorova, financial consultant

Let's consider how to correctly reflect the issuance of bonuses and financial assistance for the New Year in accounting and tax accounting.

New Year's bonus

The bonus system at enterprises is established by collective agreements, agreements, and local regulations (Article 135 of the Labor Code of the Russian Federation). The mandatory development and approval of regulations on bonuses is not stipulated by the norms of the Labor Code of the Russian Federation. However, controllers often, in order to justify the costs of paying bonuses, require the company to have a provision on bonuses (see Letters of the Ministry of Finance of the Russian Federation dated 02/05/08 No. 03-03-06/1/81 and dated 11/27/07 No. 03-03-06/1 /827).

Income tax. The procedure for accounting for bonuses when calculating income tax is established in Art. 255, as well as in clauses 21 and 22 of Art. 270 of the Tax Code of the Russian Federation.

The bonus reduces the tax base for income tax if it is provided for in an employment or collective agreement and is paid for the production results of the employee’s activities (clause 2 of Article 255 of the Tax Code of the Russian Federation). In other words, if the bonus is an incentive payment, its amount is taken into account as expenses for the purpose of calculating income tax.

Some types of bonuses are not included in labor costs. These are awards that:

• not provided for by the employment contract (clause 21, article 270 of the Tax Code of the Russian Federation);

• paid from special-purpose funds (for example, from retained earnings from previous years) or targeted revenues (clause 22 of Article 270 of the Tax Code of the Russian Federation);

• do not reward the employee for production results, but are of a social nature.

A bonus dedicated to the New Year holiday should not be included in expenses that reduce the tax base for income tax. This point of view is shared by controllers, for example, in the Letter of the Ministry of Finance of the Russian Federation dated October 17, 2006 No. 03-05-02-04/157. It is more expedient to designate such a payment in an employment or collective agreement as a bonus “at the end of the year for high production results.” Such a premium will reduce taxable income.

Personal income tax. Norms clause 1 art. 210 of the Tax Code of the Russian Federation requires that all income of the taxpayer received by him, both in cash and in kind, or the right to dispose of which he has acquired, be subject to personal income tax. Only income specified in Art. is not subject to personal income tax. 217 Tax Code of the Russian Federation. Consequently, any bonuses paid to employees are subject to personal income tax. The organization is obliged to calculate the amount of tax, withhold it from the employee’s income and transfer it to the budget system of the Russian Federation (Article 226 of the Tax Code of the Russian Federation).

Insurance premiums. All payments and other remuneration accrued by payers of insurance premiums in favor of individuals within the framework of labor relations are subject to mandatory insurance contributions (Clause 1, Article 7 of the Federal Law of July 24, 2009 No. 212-FZ).

Insurance premiums for industrial accidents and occupational diseases are calculated on payments and other remunerations paid to the employee within the framework of labor relations (clause 3 of the Rules for the accrual, accounting and expenditure of funds for the implementation of compulsory social insurance against industrial accidents and occupational diseases, approved. Decree of the Government of the Russian Federation dated March 2, 2000 No. 184).

Financial assistance for the holiday

The employer may or may not provide financial assistance, since financial assistance is not legally required. Such a payment is intended to support the employee financially in connection with a certain event that has occurred. Financial assistance may be timed to coincide with the holidays. The conditions, cases and procedure for providing financial assistance to employees are fixed in an employment or collective agreement. Payment of financial assistance is made on the basis of an order. Moreover, if the labor or collective agreement specifies the conditions for the payment of financial assistance, then the order contains a reference to such conditions.

Income tax. Expenses in the form of amounts of financial assistance provided to employees are not taken into account in expenses for the purposes of taxation of profits of organizations (clause 23 of Article 270 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated 02.22.11 No. 03-03-06/4/12).

Personal income tax. Financial assistance in an amount not exceeding 4,000 rubles. for the tax period, is not subject to personal income tax (clause 28 of article 217 of the Tax Code of the Russian Federation).

Insurance premiums. The object of taxation of insurance premiums for organizations are payments and other remunerations accrued by them in favor of individuals under employment contracts (Part 1, Article 7 of the Federal Law of July 24, 2009 No. 212-FZ). Amounts not subject to insurance premiums are listed in Art. 9 Federal Law dated July 24, 2009 No. 212-FZ. The list of payments not subject to insurance contributions also contains amounts of financial assistance provided by employers to their employees, not exceeding 4,000 rubles. per employee per billing period (clause 11, article 9).

That is, insurance premiums will have to be charged only for that part of the financial assistance that exceeds 4,000 rubles. in year.

Contributions for accidents at work and occupational diseases should be calculated only from the amount of financial assistance provided by the employer to the employee, exceeding 4,000 rubles. for the billing period (subclause 10, clause 1, article 20.2 of the Federal Law of July 24, 1998 No. 125-FZ).

Accounting for bonuses and financial assistance

If a bonus or financial assistance is considered by the organization as part of remuneration (for example, the payment of financial assistance is provided for in the Regulations on remuneration), then such amounts are calculated on the credit of account 70 “Settlements with personnel for remuneration”.

If bonuses and financial assistance are not considered as part of wages, then they are accrued on the credit of account 73 “Settlements with personnel for other operations.”

If the enterprise has a decision of the general meeting of founders (participants) to allocate part of the retained earnings to pay bonuses and (or) financial assistance, then when the bonus (material assistance) is calculated, account 84 “Retained earnings (uncovered loss)” is debited. If the organization does not have a decision of the founders (participants) to spend retained earnings on the payment of material assistance, then its amount is included in other expenses and is recorded as a debit to account 91 “Other income and expenses.”

Typical accounting entries for the calculation and payment of bonuses.

Dt84 (91) - Kt70 (73) - a bonus was awarded to an employee of the organization;

Dt70 (73)- Kt68 – personal income tax withheld;

Dt84 (91) - Kt69 – insurance premiums are charged;

Dt70 (73) - Kt50 - premium paid from the cash register.

Standard accounting records for the calculation and payment of financial assistance.

Dt84 (91) - Kt70 (73) – financial assistance accrued to an employee of the organization;

Dt70 (73) - Kt68 subaccount “Calculations for personal income tax” - income tax is withheld from the amount of financial assistance exceeding 4,000 rubles per year;

Dt84-Kt69 – insurance premiums and contributions from NS and PP are accrued from the amount of financial assistance exceeding 4,000 rubles;

Dt70 (73) - Kt50-1 - financial assistance was paid from the organization’s cash desk.

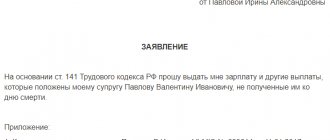

Finance All tags

Select the fragment with the error text and press Ctrl+Enter

We discuss the news here. Join us!