Tax period code

In 3-NDFL, the tax period (code) is the period of time for which you are reporting. Each time period is indicated by a digital value, depending on the period for which the declaration is submitted and indicated on the title page.

| 21 | First quarter |

| 31 | Half year |

| 33 | Nine month |

| 34 | Year |

How to abbreviate “By whom the passport was issued” in a tax return

According to the instructions (clause 7.2.), personal data is recorded in accordance with how they are indicated in the identity document. There are two lines for the “issued by” field:

If the contents of the “by whom the passport was issued” field in 3-NDFL does not fit and does not fit completely into the cells, you can use two methods:

- Use abbreviations (the list of permitted ones is given in Order of the Ministry of Finance dated November 5, 2015 No. 171n), for example:

- Do not indicate passport data at all if the TIN number is registered. The rules allow taxpayers to do this - individuals. individuals, but not individual entrepreneurs.

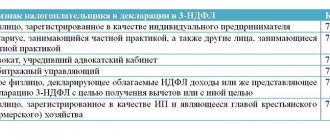

Taxpayer category code in the 3-NDFL declaration

On the title page of the form you will also find the payer category code for 3-NDFL. The categories are listed in Appendix No. 1 to the procedure for filling out reports. For ordinary citizens, the appropriate 3-NDFL taxpayer category code is “760,” and the 3-NDFL taxpayer category code “720” is allocated for individual entrepreneurs.

| 720 | An individual registered as an individual entrepreneur |

| 730 | Notary engaged in private practice and other persons engaged in private practice |

| 740 | Lawyer who established a law office |

| 750 | Arbitration manager |

| 760 | Another individual declaring income in accordance with Articles 227.1 and 228 of the Tax Code, as well as for the purpose of obtaining tax deductions in accordance with Articles 218-221 or for another purpose |

| 770 | Individual entrepreneur - head of a peasant (farm) enterprise |

Social tax deduction for training

The right to a tax refund in connection with expenses for educational services is specified in paragraph 3 of Art. 219 of the Tax Code of the Russian Federation.

The benefit is provided for training expenses;

- yours;

- children under the age of 18 (up to 24 with full-time education);

- brothers and sisters under the age of 18 (up to 24 with full-time education).

The maximum amount of expenses from which income tax can be refunded is limited by the amount of social deduction:

- 120,000 rub. - for your own education, as well as the education of your brothers and sisters;

- 50,000 rub. — for children’s education (for each).

The indicated social deduction amounts include not only training costs, but also treatment, medications, and payment of voluntary insurance contributions.

You can return 13 percent of the specified deduction amounts per year within the framework of expenses incurred for educational services:

- RUB 15,600 - for yourself, brothers and sisters;

- 6,500 rub. - for each child.

How to fill out 3-NDFL to receive a deduction for treatment and medicines for 2021 - sample filling.

How to get 13 percent back on study expenses?

Conditions for tax refund in connection with training:

- availability of a Russian license for educational activities by persons providing training services;

- payment for studies with the own funds of the person who claims a tax deduction;

- deduction of income tax from income used to pay for education;

- safety of documents confirming expenses - payment documents, agreement for training services.

If all conditions are met, then to receive a tax refund for 2021, you need to collect the necessary documents in 2021 (service agreement, payment documents for expenses, 2-NDFL certificate from the employer confirming receipt of taxable income in the reporting year), fill out a tax return 3 -Personal income tax and submit documentation to the Federal Tax Service can be done in any month during 2021.

If the deadline is missed, the right to deduction will be lost, and in subsequent years for 2021 it will no longer be possible to return personal income tax.

The declaration can be filled out manually, in the Declaration 2021 program, in the taxpayer’s personal account.

When entering data into the declaration form yourself, it is important to make sure that the current 3-NDFL form is being filled out. A new form is in effect for 2021.

Document type code in the 3-NDFL declaration

On the title page of the declaration, in the section about the identity document, indicate its code value. The full list is contained in Appendix No. 2 to the procedure for filling out 3-NDFL and in the following table.

| 21 | Russian citizen passport |

| 03 | Birth certificate |

| 07 | Military ID |

| 08 | Temporary certificate issued in lieu of a military ID |

| 10 | Foreign citizen's passport |

| 11 | Certificate of consideration of an application for recognition of a person as a refugee on the territory of Russia on the merits |

| 12 | Residence permit in the Russian Federation |

| 13 | Refugee ID |

| 14 | Temporary identity card of a Russian citizen |

| 15 | Temporary residence permit in the Russian Federation |

| 18 | Certificate of temporary asylum on the territory of the Russian Federation |

| 23 | Birth certificate issued in another state |

| 24 | Identity card of a Russian military personnel, military ID of a reserve officer |

| 91 | Other documents |

Taxpayer status code

This code determines whether the person submitting the declaration is a tax resident of the Russian Federation or not.

A citizen of the Russian Federation and a tax resident of the Russian Federation are different concepts! A foreign citizen can obtain the status of a tax resident of the Russian Federation, and a citizen of the Russian Federation can become a tax non-resident.

To be a tax resident, you must be in Russia for at least 183 calendar days a year on the date of receipt of income . In this case, citizenship does not matter:

- for someone who crossed the border of the Russian Federation in the status of a non-resident, the right to be a tax resident arises after he spends 183 days or more in the territory of the Russian Federation during the year;

- The opposite rule is also true - if a citizen of the Russian Federation, who is initially a tax resident, stays outside the Russian Federation for more than 183 days during the year, he becomes a non-resident for the purposes of calculating and paying personal income tax in Russia.

Another important rule: resident status is determined not after the end of a calendar year, but on each date of receipt of income.

The declaration must indicate the status to which the declared income relates.

EXAMPLE

The citizen of the Russian Federation was on a long business trip from 07/01/2018 to 09/30/2019. I came to the Russian Federation on vacation from 06/01/2019 to 06/30/2019. On November 10, 2019, a citizen sold an apartment in the Russian Federation. Let’s say that he needs to pay tax on the sold apartment. A citizen forms 3-NDFL for 2021.

As of the date of sale of the apartment (11/10/2019), the citizen spent 292 days outside the territory of the Russian Federation for the year from 11/10/2018 to 11/09/2019 (excluding vacations, and days of entry and exit from Russia are considered days in the Russian Federation). This means that on the date of receipt of income from the sale of an apartment, the citizen is a tax non-resident. He is obliged to calculate and pay tax at a non-resident rate of 30%. And indicate status “2” (not a tax resident) in the 3-NDFL declaration.

Region code of the Russian Federation

In the “Address and telephone” section on the title page, you must indicate the code designation of the Russian region. Find the region (code) for 3-NDFL in Appendix No. 3 to the filling procedure, or in the following table:

| 01 | Republic of Adygea |

| 02 | Republic of Bashkortostan |

| 03 | The Republic of Buryatia |

| 04 | Altai Republic |

| 05 | The Republic of Dagestan |

| 06 | The Republic of Ingushetia |

| 07 | Kabardino-Balkarian Republic |

| 08 | Republic of Kalmykia |

| 09 | Karachay-Cherkess Republic |

| 10 | Republic of Karelia |

| 11 | Komi Republic |

| 12 | Mari El Republic |

| 13 | The Republic of Mordovia |

| 14 | The Republic of Sakha (Yakutia) |

| 15 | Republic of North Ossetia-Alania |

| 16 | Republic of Tatarstan (Tatarstan) |

| 17 | Tyva Republic |

| 18 | Udmurt republic |

| 19 | The Republic of Khakassia |

| 20 | Chechen Republic |

| 21 | Chuvash Republic - Chuvashia |

| 22 | Altai region |

| 23 | Krasnodar region |

| 24 | Krasnoyarsk region |

| 25 | Primorsky Krai |

| 26 | Stavropol region |

| 27 | Khabarovsk region |

| 28 | Amur region |

| 29 | Arhangelsk region |

| 30 | Astrakhan region |

| 31 | Belgorod region |

| 32 | Bryansk region |

| 33 | Vladimir region |

| 34 | Volgograd region |

| 35 | Vologda Region |

| 36 | Voronezh region |

| 37 | Ivanovo region |

| 38 | Irkutsk region |

| 39 | Kaliningrad region |

| 40 | Kaluga region |

| 41 | Kamchatka Krai |

| 42 | Kemerovo region |

| 43 | Kirov region |

| 44 | Kostroma region |

| 45 | Kurgan region |

| 46 | Kursk region |

| 47 | Leningrad region |

| 48 | Lipetsk region |

| 49 | Magadan Region |

| 50 | Moscow region |

| 51 | Murmansk region |

| 52 | Nizhny Novgorod Region |

| 53 | Novgorod region |

| 54 | Novosibirsk region |

| 55 | Omsk region |

| 56 | Orenburg region |

| 57 | Oryol Region |

| 58 | Penza region |

| 59 | Perm region |

| 60 | Pskov region |

| 61 | Rostov region |

| 62 | Ryazan Oblast |

| 63 | Samara Region |

| 64 | Saratov region |

| 65 | Sakhalin region |

| 66 | Sverdlovsk region |

| 67 | Smolensk region |

| 68 | Tambov Region |

| 69 | Tver region |

| 70 | Tomsk region |

| 71 | Tula region |

| 72 | Tyumen region |

| 73 | Ulyanovsk region |

| 74 | Chelyabinsk region |

| 75 | Transbaikal region |

| 76 | Yaroslavl region |

| 77 | Moscow |

| 78 | Saint Petersburg |

| 79 | Jewish Autonomous Region |

| 83 | Nenets Autonomous Okrug |

| 86 | Khanty-Mansiysk Autonomous Okrug - Ugra |

| 87 | Chukotka Autonomous Okrug |

| 89 | Yamalo-Nenets Autonomous Okrug |

| 91 | Republic of Crimea |

| 92 | Sevastopol |

| 99 | Other areas, including the city and Baikonur Cosmodrome |

Income type code in 3-NDFL

The type of income code (020) in the 3-NDFL declaration is filled out on Sheet A “Income from sources in the Russian Federation”. The list of designations is given in Appendix No. 4 to the procedure for completing the declaration.

For example, when selling a car, the income code in 3-NDFL is “02”. For other cases, see the table:

| 01 | Income from the sale of real estate and shares in it, determined based on the price of the object specified in the agreement on the alienation of property |

| 02 | Income from the sale of other property (including a car) |

| 03 | Income from transactions with securities |

| 04 | Income from renting out an apartment (other property) |

| 05 | Cash and in-kind income received as a gift |

| 06 | Income received on the basis of an employment (civil) contract, the tax from which is withheld by the tax agent |

| 07 | Income received on the basis of an employment (civil) contract, the tax from which is not withheld by the tax agent (even partially) |

| 08 | Income from equity participation in the activities of organizations in the form of dividends |

| 09 | Income from the sale of real estate and shares in property, determined based on the cadastral value of this property, multiplied by a reduction factor of 0.7 |

| 10 | Other income |

3-NDFL: instructions

The declaration form consists of the following sheets:

- Title page (it indicates the taxpayer’s information);

- Section 1 (intended to reflect the final amounts of tax that are subject to payment/addition to the budget);

- Section 2 (it calculates the tax base and the amount of income tax accrued at different tax rates);

- Appendix 1 (it indicates income received from sources in the Russian Federation);

- Appendix 2 (intended to reflect information on income received from sources located outside the Russian Federation);

- Appendix 3 (indicate income received from business activities, private practice, also fill out to obtain professional tax deductions in accordance with Article 221, paragraphs 2 and 3 of the Tax Code of the Russian Federation);

- Appendix 4 (indicate the amounts of income that are not subject to taxation in accordance with Article 217, paragraphs 28, 33, 39 of the Code);

- Appendix 5 (intended for calculating standard, investment, social tax deductions);

- Appendix 6 (it calculates the amount of property deductions in accordance with Article 220 of the Tax Code of the Russian Federation: sale of property, shares in it, property rights, etc.);

- Appendix 7 (intended for calculating property tax deductions: for the construction of new housing, for the purchase of property, and so on in accordance with Article 220 of the Tax Code of the Russian Federation);

- Appendix 8 (it calculates the tax base for transactions carried out with securities and derivative financial instruments).

The rules for filling out a tax return are approved by Order of the Federal Tax Service of the Russian Federation No. ММВ-7-11 / [email protected] dated 10/03/2018. Penalties are provided for their violation.

Object name code in 3-NDFL

The object name code (010) in 3-NDFL is filled out in Sheet D1 “Calculation of property tax deductions for expenses on new construction or acquisition of real estate.” Indicate the numerical designation of the purchased property.

| 1 | House |

| 2 | Apartment |

| 3 | Room |

| 4 | Share in a residential building, apartment, room, land plot |

| 5 | Land plot for individual housing construction |

| 6 | Plot of land with purchased residential building |

| 7 | Residential building with land |

Instructions for filling out the 3-NDFL declaration: Applications

Annex 1

is intended to calculate the amounts of income received from all sources in the Russian Federation. For each tax rate and amount of income, fill in the following lines:

- 010 - tax rate at which income is taxed;

- 020 - code of type of income;

- 030 — TIN of the source of payments (employer);

- 040 - checkpoint of the source of payments;

- 050 — OKTMO of the source of payments (employer);

- 060 - name of the employer who pays income to the individual;

- 070 - the amount of income received from the source of payments;

- 080 - the amount of personal income tax withheld (if the source of payments is a tax agent).

The tax rate depends on the status of the taxpayer and the type of income received by him.

Filling out the Calculation to Appendix 1

:

- line 010 - cadastral number of the alienated property;

- 020 - cadastral value of the property as of January 1 of the year in which state registration of the transfer of ownership was carried out;

- 030 - the amount of income received from the sale of the property specified in the contract (price);

- 040 - cadastral value indicated in line 020, multiplied by the coefficient established by Art. 217.1 clause 5 of the Tax Code of the Russian Federation;

- 050 - the amount of income received from the sale of real estate.

The indicator from the last line is transferred to line 070 of Appendix 1.

In Appendix 2

indicate the amount of income from all sources located outside the Russian Federation. The following lines should be filled in:

- 010 - code of the country from which the income was received;

- 020 — name of the source of income payments;

- 030 — income currency code;

- 031 - code of type of income;

- 032 - digital unique number of a controlled foreign company, which is the source of income payments;

- 040 - date of receipt of income;

- 050 - foreign currency exchange rate against the ruble, which is established by the Bank of Russia on the date of receipt of income;

- 060 - the amount of income received from a foreign company;

- 070 - the amount of income received in foreign currency in terms of rubles;

- 071 - the amount of income in cash/in kind received as a result of the liquidation of a foreign company or its reorganization;

- 072 - the amount of income in the form of dividends received from a controlled foreign company, exempt from taxation;

- 073 - code of the applied procedure for determining profit/loss of a controlled foreign company, chosen by the taxpayer in accordance with Art. 309.1 clause 14 of the Tax Code of the Russian Federation;

- 080 — tax payment date;

- 090 - foreign currency exchange rate against the ruble, established by the Bank of Russia on the date of payment of the tax;

- 100 - the amount of tax paid in a foreign country in foreign currency;

- 110 - the amount of tax paid in a foreign country, converted into rubles;

- 115 - the amount of tax calculated on income;

- 120 - the estimated amount of tax calculated in the Russian Federation at the appropriate rate;

- 130 - the estimated amount of tax that is subject to offset/reduction in the Russian Federation.

The amount indicated in the last line is determined separately for taxes paid in each foreign country.

Appendix 3

intended for filling out by individual entrepreneurs, heads of farms, arbitration managers, lawyers and notaries who conduct private practice, and other categories of citizens specified in the Tax Code of the Russian Federation.

The application is filled out as follows:

| Line number | What to indicate |

| 010 | Activity code |

| 020 | Code of the main type of business activity according to the All-Russian Classifier of Types of Economic Activities (OKVED) |

| 030 | The amount of income received for each type of activity |

| 040 | The amount of expenses actually incurred, which are taken into account as part of the professional tax deduction |

| 041 | Amount of material costs |

| 042 | Amount of depreciation charges |

| 043 | Amount of expenses for payments/remunerations in favor of individuals |

| 044 | The amount of other expenses that are associated with generating income |

| 050 | The total amount of income, which is calculated as the sum of line 030 indicators for each type of activity |

| 060 | Professional deduction amount |

| 070 | Amount of advance payments actually paid |

| 080 | This line is filled in by the heads of farms. It indicates the year of registration of the farm |

| 090 | The amount of the adjusted tax base (if such an adjustment is made) |

| 100 | Amount of adjusted tax (if adjustment was made) |

| 110 | Source of income code |

| 120 | The total amount of actually incurred and documented expenses for all GPC agreements |

| 130 | The amount of actually incurred and documented expenses for all sources of income payments received in the form of royalties, the creation of prototypes and other similar activities (according to the Tax Code of the Russian Federation) |

| 140 | The amount of expenses for royalties, execution or use of works of science, art, literature within the limits of the standard |

| 150 | Total amount of expenses. Determined by summing the indicators of lines 120-140 |

Appendix 4

is intended to reflect amounts of income that are not subject to taxation in accordance with Art. 217 Tax Code of the Russian Federation. The following lines should be filled in:

- 010 - the amount of one-time financial assistance that a taxpayer received in the reporting tax period from employers upon the birth/adoption of a child, and which is not subject to taxation;

- 020 - 080 - amounts for specific types of income;

- 090 - the total amount of assistance in kind/cash, as well as the cost of gifts received by WWII veterans, WWII home front workers, WWII disabled people, widows of military personnel who died during the war with Finland, Japan, WWII, widows of deceased WWII disabled people and former Nazi prisoners concentration camps, ghettos and prisons, former prisoners of war during the Second World War, as well as former minor prisoners of concentration camps, ghettos and other places of forced detention, which were created by the Nazis and their allies during the Second World War, and not subject to taxation on the basis of paragraph 33 of Art. 217 of the Tax Code of the Russian Federation (exception: assistance and the cost of gifts from the budgetary system of the Russian Federation and funds from foreign states), in an amount that does not exceed 10,000 rubles;

- 100 - the total amount of contributions paid by all employers of the taxpayer in accordance with Federal Law No. 56-FZ of April 30, 2008;

- 110 - the amount of other income that is not subject to taxation in accordance with Art. 217 Tax Code of the Russian Federation;

- 120 - the total amount of income that is not subject to taxation, determined by summing lines 010-110.

The value of line 120 is transferred to line 020 of Section 2.

Appendix 5

must be completed by tax residents. It contains the following information:

| Line number | What to indicate |

| 010 | The amount of the standard tax deduction according to Art. 218 clause 1 sub. 1 Tax Code of the Russian Federation |

| 020 | The amount of the standard tax deduction according to Art. 218 clause 1 sub. 2 Tax Code of the Russian Federation |

| 030 | The amount of the standard deduction for a child for a parent/spouse of a parent/adoptive parent/guardian/trustee/spouse of an adoptive parent |

| 040 | The amount of the standard deduction for a child provided to the only parent/adoptive parent/adoptive parent/guardian/trustee, as well as one of the parents (adoptive parents) if one of them refuses to receive the deduction |

| 050 | The amount of a standard tax deduction provided to a parent, spouse of a parent, adoptive parent, guardian, trustee, adoptive parent, spouse of an adoptive parent for a disabled child under the age of 18, for a full-time student, graduate student, resident, intern, student, cadet under the age of 24 who is a disabled person of group I or II |

| 060 | The amount of a standard tax deduction provided to a single parent (adoptive parent), adoptive parent, guardian, trustee, as well as one of the parents (adoptive parents) if the other parent (adoptive parent) refuses to receive a tax deduction for a disabled child under 18 years of age, as well as for a full-time student, graduate student, resident, intern, student, cadet under the age of 24 who is a disabled person of group I or II |

| 070 | The total amount of standard tax deductions that were provided during the reporting tax period |

| 080 | The total amount of standard tax deductions that are declared in the declaration |

| 090 | The amount of social tax deduction according to Art. 219 clause 1 sub. 1 Tax Code of the Russian Federation |

| 100 | The amount of social tax deduction provided in accordance with Art. 219 clause 1 sub. 2 Tax Code of the Russian Federation |

| 110 | The amount of social tax deduction provided in accordance with Art. 219 clause 1 sub. 3 Tax Code of the Russian Federation |

| 120 | Total amount of social tax deductions (sum of values of lines 090-110) |

| 130 | The amount of social tax deduction provided in accordance with Art. 219 clause 1 sub. 2 Tax Code of the Russian Federation for training your own or close relatives |

| 140 | The amount of social tax deduction provided in accordance with Art. 219 clause 1 sub. 3 of the Tax Code of the Russian Federation for payment for medical services or treatment |

| 150 | The amount of social tax deduction provided in accordance with Art. 219 clause 1 sub. 3 of the Tax Code of the Russian Federation for the amount of insurance premiums paid by the taxpayer during the tax period under voluntary personal insurance contracts, spouse, parents, children (including adopted children and wards under the age of 18) |

| 160 | The amount of social tax deduction provided in accordance with subparagraph. 4 and 5 paragraph 1 art. 219 of the Code, in the amount of pension and insurance contributions paid by the taxpayer under contracts of non-state pension provision, voluntary pension insurance and voluntary life insurance, additional insurance contributions for funded pension |

| 170 | The amount of social tax deduction provided in accordance with subparagraph. 6 clause 1 art. 219 of the Code, in the amount paid in the tax period by the taxpayer for an independent assessment of his qualifications for compliance with qualification requirements in organizations carrying out such activities in accordance with the legislation of the Russian Federation |

| 180 | The total amount of social tax deductions for which the limitation established by Art. 219 clause 2 of the Tax Code of the Russian Federation (no more than 120 thousand rubles) |

| 181 | The total amount of social tax deductions that were provided during the tax period by tax agents |

| 190 | The total amount of social tax deductions declared in the declaration |

| 200 | Calculation of the total amount of standard and social tax deductions that are declared in the declaration (sum of lines 080 and 190 in Appendix 5) |

| 210 | The amount of investment tax deduction in the amount of funds that were contributed by the taxpayer during the tax period |

| 220 | The amount of investment tax deduction provided in accordance with Art. 219.1 clause 1 sub. 2 of the Tax Code of the Russian Federation in the previous tax period |

Filling out the Calculation for Appendix 5

:

- line 010 - TIN of a non-state pension fund or insurance company;

- 020 - checkpoint of a non-state pension fund or insurance company;

- 021 - code of the type of agreement on the basis of which pension or insurance contributions were paid (code 1 - for a non-state pension agreement, code 2 - for a voluntary pension insurance agreement, code 3 - for a voluntary life insurance agreement);

- 030 — details of the contract of a non-state pension fund or insurance company;

- 040 and 050 - details of the non-state pension provision/voluntary pension insurance/voluntary life insurance agreement (date of conclusion of the agreement and its number);

- 060 - the total amount of pension/insurance contributions paid by the taxpayer under non-state pension provision/voluntary pension insurance/voluntary life insurance contracts.

In line 070, the amount of social tax deductions is calculated in the amount of additional insurance contributions actually paid in the tax period for a funded pension in accordance with the Federal Law of the Russian Federation No. 56-FZ of April 30, 2008. In line 080, the total amount of pension contributions that were paid under the non-state pension agreement is reflected. insurance/voluntary pension insurance/voluntary life insurance, as well as additional insurance. contributions to funded pension. It is calculated by summing the indicators of lines 060 and 070.

In Appendix 6

fill in the following lines:

- 010 - the amount of property deduction for income received from the sale of houses/apartments/rooms, including privatized housing;

- 020 - the amount of costs for the purchase of housing, dachas, garden plots, houses, apartments, rooms, which can be documented;

- 030 - the amount of property deduction for income from the sale of a share or shares in apartments, houses, residential premises, rooms, including privatized residential premises;

- 040 - the amount of actual expenses for the purchase of a share/shares in residential buildings, apartments, including privatized residential premises, which can be documented;

- 050 - the amount of property deduction for income from the sale of other real estate;

- 060 - the amount of actual and documented costs that are associated with the purchase of real estate;

- 070 - the amount of property deduction for income received from the sale of other property;

- 080 - the amount of actual and documented expenses that are associated with the purchase of other property.

In line 090, the calculation of property deductions provided for in Art. 220 Tax Code of the Russian Federation. In lines 100 - 110 - calculation of property deductions in accordance with Art. 220 clause 2 sub. 2.1 and 2.2.

Lines 120 - 150 indicate the income received by the taxpayer from the sale of a share or part thereof in the established capital of the community, upon leaving the company, transferring funds to a community member, or liquidation of the community.

Lines 120, 130, 140 and 150 are intended to reflect the amounts of expenses actually incurred and documented. Line 160 - to indicate the total amounts of property deductions and expenses. Determined by summing the indicators in lines 010 - 150.

In Appendix 7

indicate property deductions for expenses associated with new construction of houses or purchase of real estate.

The following lines should be filled in:

| Line number | What to indicate |

| 010 | Object name code |

| 020 | Taxpayer attribute code |

| 030 | Object number code (cadastral, conditional, inventory) |

| 031 | Cadastral/conditional/inventory number of the object |

| 032 | Object location address (fill in if none of the object numbers are known) |

| 040 | Date of the act of transfer of the apartment, room, share in them |

| 050 | Date of registration of ownership rights to an apartment, room, residential building |

| 060 | Date of registration of ownership rights to the land plot |

| 070 | Share in ownership |

| 080 | The amount of actual expenses incurred for new construction or purchase of an object |

| 090 | The amount of interest actually paid on targeted loans that was spent on new construction or the purchase of real estate |

| 100 | The amount of property deduction for expenses for new construction or acquisition of real estate, taken into account for previous tax periods |

| 110 | The amount of property deduction for the cost of paying interest on targeted loans, which was spent on new construction or acquisition of real estate, as well as on loans under the refinancing program, taken into account when determining the tax base for previous periods |

| 120 | The amount of property deduction for the construction or purchase of real estate, provided in the reporting tax period by the tax agent on the basis of a notification |

| 130 | The amount of property deduction for the cost of paying interest on targeted loans/credits received for new construction or purchase of real estate, provided in the reporting tax period by the tax agent according to the notification |

| 140 | The tax base |

| 150 | The total amount of expenses for new construction or purchase of real estate (does not exceed the amount indicated in line 140) |

| 160 | The total amount of expenses for paying interest on targeted loans and borrowings received for new construction or purchase of real estate |

| 170 | The balance of the property deduction for expenses on new construction or the purchase of real estate, which transfers to the next tax period |

| 180 | The balance of the property deduction for the cost of paying interest on targeted loans or borrowings that were received for the construction or purchase of real estate, carried over to the next tax period |

In Appendix 8

reflect information on expenses and deductions for transactions with securities, derivative financial instruments, including transactions that are accounted for on an IIS (individual investment account). It contains the following data:

- 010 — transaction type code;

- 020 - the total amount of income received from the totality of completed transactions;

- 030 - the total amount of expenses associated with the acquisition/storage/sale and redemption of securities or derivative financial instruments, as well as for repo transactions, the object of which are securities, for securities lending transactions and transactions carried out within the framework of an investment partnership;

- 040 - the total amount of expenses that is taken to reduce income for the totality of transactions performed;

- 050 - a sign of accounting for losses on income, which are indicated in line 020;

- 051 — code of the type of operation for which the loss is accepted;

- 052 - the total amount of loss, which is taken as a reduction in income for the totality of transactions performed;

- 060 - the total amount of investment tax deduction, which is provided for in Art. 219.1 clause 1 sub. 1 of the Tax Code of the Russian Federation, accepted for deduction based on the totality of transactions performed;

- 070 - the total amount of investment deduction, which is provided for in Art. 219.1 clause 1 sub. 3 of the Tax Code of the Russian Federation, accepted for deduction based on the totality of transactions performed.

It is worth considering that the sum of the indicators indicated in lines 040, 052, 060 and 070 should not exceed the indicator in line 020.

Taxpayer identification in 3-NDFL

In Sheet D1, you must also select the taxpayer attribute (030).

| 01 | The owner of the property in respect of which a property deduction for personal income tax is claimed |

| 02 | Property owner's spouse |

| 03 | Parent of a minor child - owner of the property |

| 13 | A payer claiming a property deduction for expenses related to the purchase of housing in the common shared ownership of himself and his minor child (children) |

| 23 | A payer claiming a property deduction for personal income tax for expenses related to the purchase of housing in the common shared ownership of the spouse and his minor child (children) |

Budget classification code 3-NDFL

In field “020” of Section 1 “Information on the amounts of tax subject to payment (surcharge) to the budget/refund from the budget”, mark the budget classification code (BCC) of tax revenues, which is used to group items of the state budget. Find out the appropriate BCC for your case on the website of the Federal Tax Service.

In addition, you can use a service that will help you determine not only the BCC, but also the numbers of your inspection of the Federal Tax Service and the All-Russian Classifier of Municipal Territories (OKTMO).

OKTMO code - what is it in 3-NDFL?

Using OKTMO, the declaration indicates the code of the municipality at the place of residence (or registration) of the person (or individual entrepreneur). Individuals may need OKTMO of the company from which the income was received in Sheet A of 3-NDFL. Find out the number from the tax office or on the Federal Tax Service website.

If OKTMO contains less than 11 characters, then do not forget to put dashes in the remaining empty cells. Read more about the rules for filling out a tax return in the article “How to fill out 3-NDFL”.

About the author of the article

Lidia Ivanova I am the editor-in-chief of the Sashka Bukashki website. More than 15 years of experience working with legal information.

Results

Appendix 7 in 3-NDFL is formed in cases where the personal income tax payer has the right to a tax deduction as a result of transactions to improve housing conditions. The rules for filling out the sheet are established by order of the Federal Tax Service dated August 28, 2020 No. ED-7-11 / [email protected] There are nuances in filling out Appendix 7 in cases where the tax deduction declaration is submitted for the first time or is submitted again, for the balance of the confirmed deduction for previous periods ( years).

Learn more about the nuances of forming 3-NDFL from the article “Sample of filling out a 3-NDFL tax return.”

Read more about the specifics of registering a deduction when purchasing real estate in the article “Procedure for compensation (return) of personal income tax when purchasing an apartment.”

Sources:

- Tax Code of the Russian Federation

- Order of the Federal Tax Service of Russia dated August 28, 2020 No. ED-7-11/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.