List of payments to relatives upon death of an employee

The death of an employee at an enterprise requires financial compensation to the close relatives of the deceased, which is made on behalf of the management of the organization. Among the main payments the following material compensations are noted:

- Wages for the period worked, which the accounting department did not manage to issue to the employee;

- Compensation for unused vacation days;

- Subsidies and benefits that were due to the employee, but were not paid as a result of the incident (benefits for temporary inability to perform work duties, etc.);

- Other payments stipulated by the employment agreement (bonuses, incentives, salary supplements).

It should be noted that personal income tax is not levied on the deceased employee’s final salary. Other payments and compensation are also not subject to taxation (the exception is royalties).

Also, Article 1183 of the Civil Code of the Russian Federation establishes a period of 4 months for relatives to apply for payment of amounts not received by a deceased employee. If this deadline is missed, then these amounts are included in the inheritance.

Who has the right to receive payments for the deceased?

The general rule is that for an employee who has died, relatives and dependents can receive his payments (Labor Code of the Russian Federation, Article 141). However, in practice, determining who should receive the money is not so simple.

Example: the deceased’s wife and granddaughter applied to the accounting department for payment. At the same time, the marriage with his wife was dissolved, and his granddaughter is an adopted child. It is not possible to determine the whereabouts of blood children. What should the company management do?

Let's turn to the legislation. Family Code (RF IC) in Art. 2 family members include:

- spouse of the deceased - legal husband or wife;

- children of the deceased;

- his parents.

When determining the recipient of payments, you should first of all be guided by these provisions. At the same time, in Chap. 15 of the same document states that other relatives can also be recognized as family members: brothers, sisters, grandparents, grandchildren, non-natural parents and children. The employer decides what to do. He has the right to make a payment to the first of the applicants named in the Investigative Committee.

Question: Should an employer pay the wages of a deceased employee to his only relative (his aunt) and on the basis of what documents? View answer

If several people apply for money at once, considering themselves members of the deceased’s family or his dependents, the issue, as a rule, is resolved by agreement between relatives or by the latter’s appeal to the courts.

If the employer has doubts about who and how legally he will make the payment, it is advisable to transfer this money to the bank account of the deceased employee, notifying the bank of his death.

Thus, the money will become part of the inheritance mass, it will be received by the heirs according to the law, no matter who they are to the deceased. The organization will not be responsible for payment. But a transfer to a bank account with inclusion in the inheritance can be made only 4 months after the death of a citizen (Civil Code of the Russian Federation, Art. 1183). You can leave the money in the organization by depositing it until the moment when the already identified heirs apply for payments.

If you decide to give money to one of your relatives, you should remember that according to the Civil Code of the Russian Federation, only those of them who lived together with the employee or were dependents have this right, regardless of place of residence (Civil Code of the Russian Federation, the same article).

In the example we gave, none of the applicants has the right to receive the salary of the deceased.

On a note! The organization is not obliged to search for relatives and dependents of a deceased employee for the purpose of delivering uncollected amounts of wages and equivalents.

Amount of financial assistance upon death of an employee

The amount of payments provided for by local charters, as well as the employment agreement, is negotiated personally by the head of the enterprise and the relatives of the deceased person, if a specific amount is not provided for in the documents themselves.

The same applies to compensation that the head of the enterprise pays on his own initiative. There are different calculation rules when paying funeral benefits for a deceased employee, since this is a type of insurance coverage for citizens. The funeral benefit is paid to the person who has assumed the responsibility for burying the deceased, and is due to both citizens of the Russian Federation and foreign persons (Clause 1, Article 10 of the Federal Law of January 12, 1996 N 8-FZ “On Burial and Funeral Business” ( (hereinafter referred to as Law No. 8-FZ) Even if the relatives of the deceased person buried him at their own expense, they have the right to submit an application addressed to the head of the enterprise in order to compensate for the losses incurred.

Important! You can receive compensation for the funeral of a deceased employee only within 6 months from the date of the citizen’s death. If this deadline is missed, payment may be refused (Clause 3, Article 10 of Law No. 8-FZ).

At the legislative level, the funeral amount is set at 5,946.47 rubles. According to legal norms, it is subject to annual indexation approved by the Government of the Russian Federation. In 2021, the payment amount was 6,124.86, taking into account indexation equal to 1.03 (Resolution of the Government of the Russian Federation No. 61 of January 29, 2021).

It is possible that a regional coefficient increasing the amount of payments may also apply. The amount indicated above is valid at the federal level, however, each enterprise may set its own amount of compensation, which is greater than that established by law. Then funeral payments are paid from the enterprise budget.

The procedure for payments to close relatives and the necessary documents

Citizens who are entitled to payment of funds from a deceased employee must submit the following documents:

- Statement;

- Identity document (passport);

- Sick leave (if available);

- Receipts and invoices confirming funeral expenses;

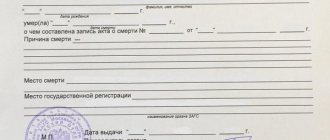

- Death certificate of the deceased employee;

- A document confirming relationship with the deceased.

Let's celebrate! Cash payments are paid to the relative who first applies for payment. If there are several applicants, they must agree on their own. If there is no agreement, it is proposed to clarify this in court and then payment will occur according to the court's decision.

The calculation takes place within a week, but no later than four months from the date of death of the deceased. If no one applies for the funds, they are inherited.

Calculation of payments

The calculation of payments due to the deceased employee is carried out by the accounting department.

Wages depend on the number of days the employee has worked. Compensation for unused vacation is calculated in a different way. To calculate compensation for unused vacation periods, the accountant must calculate two important points: the number of days of unused annual leave, the average daily income.

The average daily income level is calculated using the following formula:

OT annual/12/29.3, where:

- OT annual is the salary for 12 months;

- 12 - number of months in a year;

- 29.3 is the coefficient for calculating the average monthly number of days in the calendar, regulated by law (Article 139 of the Labor Code of the Russian Federation).

Salary does not include all payments received by an employee. Thus, the following funds are not taken into account:

- Performing job duties while maintaining salary (business trip);

- Compensation for sick leave.

If a deceased employee has accumulated unused vacation days over several years, they are added up. For the final calculation of compensation, it is necessary to calculate using the following formula:

Average salary per day * total number of unused vacation days

Download for viewing and printing:

Article 139 of the Labor Code of the Russian Federation “Calculation of average wages”

Who receives the money of a deceased employee?

Material payments due to the death of an employee at the enterprise are awarded to close relatives of the person, as regulated by labor legislation. Among this list of persons are noted (Article 2 of the Family Code of the Russian Federation):

- Spouse.

- Parents or adoptive parents.

- Natural or adopted children.

Also, funds can be issued to citizens who were dependent on the deceased employee. To confirm this fact, you must obtain a certificate from the judicial authority.

How to issue money?

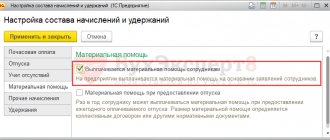

The provision of material support is reflected in accounting documents in account 91 “Other income and expenses”, since it is not directly related to business activities. You can provide separate subaccounts (91-1 - “Other income”, 91-2 - “Other expenses”).

According to accounting, this is carried out in accordance with Order of the Ministry of Finance No. 94N dated October 31, 2000:

| Operation | Debit | Credit | A document base |

| Calculation of financial assistance | 91(91-2) | 76 | Manager's order |

| Payment of funds | 76 | 50 | Account cash warrant |

In certificates and tax documents (2-NDFL, 6-NDFL), cash flows are reflected using special income codes (Federal Tax Order No. ММВ-7-11 / [email protected] dated 09/10/2015).

However, among the codes there are no ones assigned to financial assistance to the employee’s relatives in connection with his death. Therefore, there is no need to indicate it.

Arranging for funeral compensation

One of the additional compensations that relatives of a deceased person can count on is subsidies for the burial of the deceased. Payments are made from the budget of the organization in which the deceased employee worked. So, in order to receive this compensation, the organization must provide:

- Application in any form.

- Employee's death certificate.

This package of documents remains with management for further confirmation of payments made during the inspection of the Social Insurance Fund.

Documents for receiving payments

Any legal procedure requires documentary evidence of the actions of the parties. Thus, relatives of a deceased employee of an enterprise must provide management with the following information:

- Passport of a relative of the deceased person;

- Application for the issuance of funds;

- A copy of the death certificate;

- Certificate of relationship with the deceased (marriage certificate, birth certificate).

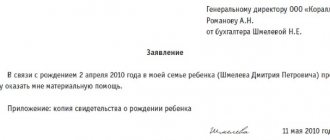

Sample application:

To whom does the employer provide swearing support?

As a rule, financial assistance in connection with death is provided to family members of the deceased employee.

The circle of these persons is determined in accordance with Art. 2 of the RF IC, which is confirmed by letter of the Ministry of Finance No. 03-05-01-04/234 dated 08/03/2006.

A citizen’s family includes:

- his husband;

- children (natural and adopted);

- parents (natural and adoptive parents).

The court may include other people from the family of the deceased as family members, most often close relatives and dependents . Established family and household connections are taken into account.

In practice, the courts recognized the family of the deceased as their common-law spouses and grandparents, who were actually supported by the deceased.

The employer has the right to pay financial assistance to persons who do not belong to the family members of the deceased employee. But in this case it will be subject to personal income tax (13%).

How to pay money to relatives?

To receive financial assistance in the event of the death of an employee, an application is written to the last employer of the deceased . There is no exact sample, you can fill it out in free form by hand.

Many companies produce their own forms and stipulate their use in internal regulations. This should be clarified with the secretary, accountant or HR specialist.

Additionally you will need:

- certificate of an employee from the registry office or a court decision declaring him dead or missing;

- documents confirming family relationships or other connections with the deceased employee. Birth certificates, marriage certificates, court documents, etc. are suitable.

Read more: How to write a character reference for a person for court

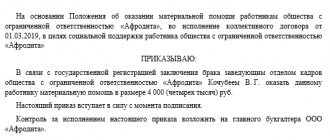

If financial assistance is provided for by the company’s regulatory documents, its appointment is formalized by an order signed by the director .

Otherwise, the decision on payment is made by the founders of the company (not the director or other hired employees, even the management team).

If there are several owners, the issue is considered at a general meeting. Based on the results, a protocol is drawn up.

It must indicate the date, location of the meeting, a list of all participants, topics on the agenda, the form of voting, and its results.

The organization has the right to develop its own protocol form.

The sole founder considers the petitioner’s application independently and puts a resolution on it.

After the owners’ decision, the director issues and signs an order to issue financial assistance.

Funds are paid either in cash from the company’s cash desk or by bank transfer. In any case, an expense cash order is generated.

Amount of payment to the family of a deceased employee

The law does not establish limits on the amount of financial assistance in the event of the death of an employee: everything depends on the financial capabilities of the company. They are usually regulated by internal regulations.

The source of payments is the organization’s own funds. Most often, companies form a fund using retained earnings from previous periods or the current year.

Taxation - personal income tax and insurance premiums

The application of personal income tax (personal income tax, 13%) depends on who received the financial assistance:

- family members - not taxed in full (Article 217 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance No. 03-04-05/70419 dated October 26, 2017);

- other relatives - not subject to personal income tax only up to 4,000 rubles. in year.

In the first case, one more condition must be met: financial assistance is provided at a time . This is understood as a payment that is provided for specific purposes no more than once in a tax period (year), for a certain circumstance.

It doesn’t matter whether it’s a lump sum or in parts. This definition is given by the Tax Service of the Russian Federation in letter No. 3-5-04 / [email protected] dated March 10, 2009.

Payments on the same basis, but issued by different orders of the head of the company, are not considered one-time payments. What does this mean in practice?

For example, due to the death of an employee, his wife contacted the company twice.

Both times the founders decided to help her. Accordingly, the director issued 2 orders.

Such assistance can no longer be called one-time; it is subject to personal income tax.

Financial support for a relative of a deceased employee is not wages or other remuneration for work.

Therefore, she does not pay insurance premiums to the Social Insurance Fund or the Pension Fund of the Russian Federation - read more about the assessment of contributions.

This is confirmed by Art. 422 of the Tax Code of the Russian Federation and Art. 20.2 Federal Law No. 125 dated July 24, 1998. Expenses associated with the payment of financial assistance are not taken into account when calculating income tax.