When will new forms be needed?

If, according to Article 78 of the Tax Code of the Russian Federation, taxpayers who have overpaid want to dispose of the overpaid amounts:

- offset them as future payments;

- pay off arrears on other mandatory payments;

- reduce or completely eliminate the debt on penalties and fines for offenses;

- demand a refund -

they will need a tax overpayment claim form. These rules apply to all fees and taxes introduced in the Russian Federation, including state duty (with some features listed in Article 333.40 of the Tax Code of the Russian Federation), VAT, and advance payments. But you must understand that the tax service will not return or offset the overpaid amount against future payments until the debt is paid off.

How to fill out such a document

If the taxpayer decides to redistribute his own funds, he needs to write a corresponding appeal to the tax service. The application form for offset of overpayment of taxes is presented in the Federal Tax Service order dated February 14, 2017 No. ММВ-7-8/ [email protected] , Appendix No. 9. You can download it at the bottom of the page.

Let's say Kolosok LLC filed a transport tax return for 2021, but when paying it made a mistake, paying 3,112 rubles more. The organization applies to the inter-district Federal Tax Service, writes a tax offset application, where it requests that the overpaid amount be credited against the upcoming payments of corporate property tax. Let's take a step-by-step look at how to fill out such a document.

Step 1. Traditionally, the TIN and KPP should be indicated at the very top. The individual entrepreneur’s identification number consists of 12 digits, so there should be no free cells left. Organizations enter only 10 numbers in the appropriate fields, and put dashes in the remaining two. When filling out the line intended for the checkpoint, applicants must act in the same way: if there are numbers, enter them, if not, put dashes.

Step 2. Enter the request number. Here they put down the number of times in the current year they applied for the test. Don’t forget about dashes if the number of numbers to be entered is less than the number of cells.

Step 3. Enter the code of the tax authority where the application is sent. This is an inspection of the Federal Tax Service at the place of registration of the individual entrepreneur or organization. In a consolidated group of taxpayers, the responsible participant in this group requests a credit for the overpayment of income tax.

Step 4. We write down the full name of the applicant organization, for example, limited liability company “Kolosok”. Fill in the remaining cells with dashes. None of them should be left empty. When filling out this field by an individual entrepreneur, he must indicate his last name, first name and patronymic, if any. In addition, the status of the applicant, as whom he is applying, should be indicated in accordance with the instructions:

- taxpayer – code “1”;

- fee payer – code “2”;

- payer of insurance premiums – code “3”;

- tax agent – code “4”.

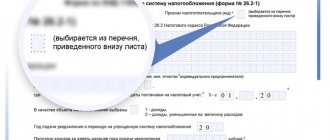

Step 5. We indicate the article of the Tax Code of the Russian Federation on the basis of which the offset is made. It depends on which payment was overpaid. The Federal Tax Service left 5 cells to indicate a specific article. If some of them are not needed, dashes must be added. Here are the options for filling out this field:

- Article 78 of the Tax Code of the Russian Federation - for offset or return of overpaid amounts of fees, insurance premiums, penalties, fines;

- Article 79 of the Tax Code of the Russian Federation - for the return of excessively collected amounts;

- Article 176 of the Tax Code of the Russian Federation - for VAT refund;

- Article 203 of the Tax Code of the Russian Federation - for the return of overpayments of excise tax;

- Article 333.40 of the Tax Code of the Russian Federation - for the return or offset of state duty.

Step 6. We write down what the overpayment was for - taxes, fees, insurance premiums, penalties, fines.

Step 7. The applicant specifies for what period the overpayment occurred. The developers provided 10 familiar places to indicate the code, of which two are dots. The first two of them are filled in with one of the following options:

- MS - monthly;

- KV - quarterly;

- PL - six-monthly;

- GD - annual.

Specific values will depend on the reporting period provided for by law for the payment for which offset is planned.

In the 4th and 5th acquaintances, the reporting period is specified:

- if a monthly billing period is approved for payment, then enter the numerical value of the month (from 01 to 12) in the provided columns;

- if quarterly, indicate the value of the quarter (from 01 to 04);

- for payments with a semi-annual reporting period, enter values 01 or 02, depending on the semi-annual period;

- For the annual fee, zero values are provided, that is, “0” must be entered in both cells.

The last four familiar places are intended to indicate a specific year, say 2021.

Instead of alphanumeric combinations, we also write down a specific date: 01/25/2020. Such an entry is permitted if the legislation provides for a specific date for paying the fee or submitting a declaration.

Examples of filling out the billing period: “MS.02.2020”, “KV.03.2020”, “PL.01.2020”, “GD.00.2020”, “04.05.2020”.

Step 8. Enter the OKTMO code. If you don’t know it or have forgotten it, call the Federal Tax Service at the place of registration, or on the website nalog.ru you can find out the required code by the name of the municipality.

Step 9. We accurately enter the BCC to pay the appropriate payment, using Order of the Ministry of Finance of Russia No. 132n dated 06/08/2018. We find out the code using the Federal Tax Service website or we can look at it on a previously filled out payment order.

Step 10. We clarify to which Federal Tax Service the excess funds were transferred.

Step 11. On the first sheet, it remains to fill in how many sheets the application is submitted on and how many sheets of supporting documents are attached, and indicate information about the applicant himself. We recommend leaving these two small sections for later.

Let's continue filling on the second sheet. In the very first field where you need to indicate your last name, first name and patronymic, put dashes. Below we indicate what needs to be done with the overpayment - pay off the debt or leave funds for upcoming payments.

Step 12. We write down the specific amount that the applicant wants to offset. It is indicated in numbers, without text decoding.

Step 13. We fill in the period for the payment for which we plan to offset. In our case, the corporate property tax is quarterly, so we enter the quarter in which the overpayment should go.

Step 14. Write down the OKTMO code again. Usually it is duplicated.

Step 15. We specify the KBK for the transfer of funds, into which the excess amount will go. Ours is different from the previous KBK, since the taxes are different. If the overpayment goes towards future payments for the same fee, then the BCCs are the same. An exception is if the codes were previously changed by decision of the Ministry of Finance. Let us also recall that the offset is carried out according to certain rules: they must relate to the same type: federal, regional or local. For example, it is not possible to offset the federal portion of the income tax against upcoming trade tax payments.

Step 16. The code of the Federal Tax Service, which accepts receipts, is usually duplicated.

Step 17. Since there are no more overpayments, in our example the following lines are not filled in. We put spaces there. Also, organizations and individual entrepreneurs do not fill out the third sheet. It is intended for individuals who are not registered as individual entrepreneurs and who have not indicated their TIN.

Step 18. Return to the first sheet and enter the number of pages and attachments. Applicants indicate the relevant data in the provided fields.

Step 19. The last part of the application should not cause problems when filling out. Here you need to clarify who is submitting the appeal and when, and indicate a contact phone number. The right side remains blank: it is intended for marks from Federal Tax Service inspectors.

Where can I complain to the tax office?

Before filing a complaint with the Federal Tax Service of Russia or other government agencies, you should try to figure it out with your regional Federal Tax Service Inspectorate. It may be enough to point out the error to the employee over the phone or in person, and it will be corrected, and you won’t have to file a tax complaint.

If the problem is not solved in this way, you need to connect the appeal mechanism provided for by law.

Article 138 of the Tax Code of the Russian Federation establishes the following procedure for appealing actions and decisions of the tax authority:

- To a higher tax authority

- To court

This means that the first instance for filing a complaint against the tax inspectorate is always a higher tax authority. Next, the taxpayer has a choice: either continue appeals within the tax service, or file a lawsuit.

Within the tax service itself

If you choose the first option, a complaint about the actions or inaction of the tax authority can be submitted sequentially to the following authorities:

- District Federal Tax Service Inspectorate at your place of residence

- Department of the Federal Tax Service for the region

- Central office of the Federal Tax Service of Russia

There are several ways to file a complaint with the tax office at your place of residence:

- Come in person. To do this, you need to use the online booking service, where you can pre-book an appointment in the next 2 weeks. There you will need to fill in your personal and contact information, select an inspection for an appointment, as well as a suitable date and time. At a personal appointment, you can try to discuss the situation orally or submit an appeal in writing. We recommend that you always draw up a written document, because if during a conversation with the tax inspector it becomes clear that the problem cannot be solved on the spot, you can immediately submit a written appeal to the office addressed to the head of the inspectorate.

All written complaints to the tax service should be drawn up in two copies, so that on the second the Federal Tax Service employees sign a receipt for acceptance of the documents.

Important! Even for an oral conversation with an inspector, you need to properly prepare and document your claims. For example, if a tax was assessed on a car that has long been sold, then you need to provide documents confirming the sale of this car.

Note! You should not send original documents in your complaint letter: they may get lost. Photocopies will be enough for the tax authority to make a decision.

There are also several options for filing a complaint with the regional department of the Federal Tax Service and the Central Office. Contacts of these structures can be found on the Federal Tax Service website.

You can also contact the Central Office of the Federal Tax Service by way of pre-trial appeal through the State Services service.

To court

Complaints from individuals are mainly resolved within the tax service itself and rarely go to court. However, if the dispute cannot be resolved, and even more so if there is a financial dispute, for example, regarding a deduction, you can go to court through litigation.

To file a claim in court, you must:

- Pay the state fee. For statements of claim challenging the actions and decisions of an authority, the state duty is 300 rubles. If claims are made for the collection of funds, the state duty is calculated based on the amount of claims according to the rules of Article 333.19 of the Tax Code of the Russian Federation. Pensioners and disabled people of groups I and II are exempt from paying state duty. A receipt for payment is attached to the statement of claim.

- If the application is submitted in paper form, you need to print out the applications with copies of the attachments according to the number of persons participating in the case: for yourself, the tax office and the court.

- Take to the post office a copy of the claim for the defendant along with the attachments and send it to the Federal Tax Service by registered mail with acknowledgment of receipt. Receipts of delivery will also need to be attached to the claim in court.

- Apply to the court. This can be done in three ways:

- come to the court office and hand in the documents in person. Then the secretary will mark your copy as having been received and take away the claim along with all the attachments;

- send the claim by registered mail;

- use the electronic system of GAS Justice and send documents electronically in PDF format. This will require authorization through the ESIA.

The period for consideration of the case in the first instance takes about two months. When filing an appeal or cassation complaint, the dispute can drag on for up to a year.

How to get your money back

If an entrepreneur (company) decides to return the overpayment amount, he needs to use another form from the Federal Tax Service order No. ММВ-7-8 / [email protected] dated 02.14.2017, proposed in Appendix No. 8. It contains a form for returning the excess amount.

The rules for filling out this document are basically the same. We will not consider them in detail, but will give an example of a completed document. Let's say Kolosok LLC overpaid VAT for the first quarter of 2021 in the amount of 15,732 rubles and now wants to return it. This is what an appeal from the head of an LLC looks like.

When and how to submit an appeal

According to Article 78 of the Tax Code of the Russian Federation, applying for offset and refund is allowed within 3 years from the date of payment of the fee. There are three ways to deliver documents:

- personally;

- by mail with a valuable letter with an inventory;

- in electronic form via telecommunication channels or through a personal account.

Having received such an application to offset the overpayment of taxes, the tax authority decides whether to satisfy it or not. The service notifies the entrepreneur of its decision within 10 days from the date of receipt of the application. Usually, if the initiative comes from an organization or individual entrepreneur, the Federal Tax Service does a reconciliation of the calculations. If the inspector himself discovers the overpayment, the reconciliation may be refused. The entrepreneur is not relieved of the obligation to submit an application.

Legal documents

- Article 78 of the Tax Code of the Russian Federation

- Article 333.40 of the Tax Code of the Russian Federation

- 02/14/2017 No. ММВ-7-8/ [email protected]

- Article 79 of the Tax Code of the Russian Federation

- Article 176 of the Tax Code of the Russian Federation

- Article 203 of the Tax Code of the Russian Federation

- Order of the Ministry of Finance of Russia No. 132n dated 06/08/2018

- Order of the Federal Tax Service No. ММВ-7-8/ [email protected] dated 02/14/2017

How to write an application (sample and submission methods)

It is not difficult to make a statement to the regulatory authorities. The main thing before this is to collect all possible evidence of receiving illegal wages, testimony of witnesses.

If there are compelling arguments, the tax service may initiate an audit based on an employee’s complaint, which will establish a violation of the law. An application to the tax office for an employer who issues black wages can be submitted in one of three ways:

- When contacting the territorial tax office in person. You can submit the application personally to the head of the department or register the appeal in the office;

- Through the official website of the tax office. In a special section of the portal it is possible to write a complaint, as well as attaching an electronic application to it;

- By sending an application by registered mail via mail. You can draw up an application, attach the necessary documents to it and send it to the tax office. It is advisable to choose a shipment with return notification of receipt by the addressee.

According to legal regulations, the applicant must receive a response to the complaint from the tax service within 30 days from the date of registration of the appeal. The tax inspectorate also has another 30 days left to conduct an audit and determine whether the employer has violated the law.

Upon completion of all activities, the labor tax inspectorate must send an appeal to the applicant about the progress of the audit and its results.