Legislators will change the form starting in 2021

The Federal Tax Service published order No. ED-7-11/ [email protected] , which changed the rules and sample for filling out 3-NDFL based on the results of 2021. This means that the report for the current year will have to be filled out in a new way; the order comes into force on 01/01/2021.

IMPORTANT!

For reporting for 2021, use the new form!

Main changes in the 3-NDFL declaration:

- the field “Registered under No.” has been removed from the title page of the form;

- Section 1 “Information on the amounts of tax subject to payment (addition) to the budget / refund from the budget” is divided into two paragraphs: in the first, taxpayers indicate information on the amounts of tax subject to payment (addition) to the budget (except for amounts of tax paid in accordance with from clause 7 of Article 227 of the Tax Code of the Russian Federation) or return from the budget; in the second - information about the advance payment paid in accordance with clause 7 of Article 227 of the Tax Code of the Russian Federation;

- an appendix to Section 1 “Application for offset (refund) of the amount of overpaid personal income tax” was introduced;

- a separate calculation sheet has been added to Appendix 3 “Calculation of advance payments paid in accordance with clause 7 of Article 227 of the Tax Code of the Russian Federation”.

IMPORTANT!

They will change the barcodes on all pages, which is why the old form will no longer be accepted. From 2021, the declaration will have to be filled out from scratch.

Last year, the rules for numbering adjustments changed. The new wording sounds like this: continuous numbering is provided, where the “adjustment number” for the primary declaration takes the value “0—”; for updated declarations, the number is indicated sequentially (“1—”, “2—”, “3—” and so on). It is not allowed to fill out an adjustment number for an updated declaration without a previously accepted primary declaration.

Filling out 3-NDFL when declaring income and filing tax deductions

The procedure for filling out 3-NDFL depends on the case for which you are filing a declaration. The declaration form contains 19 sheets, of which you should fill out only those that are necessary for you personally:

- Section 1 “Information on the amounts of tax subject to payment (addition) to the budget/refund from the budget”;

- Section 2 “Calculation of the tax base and the amount of tax on income taxed at the rate (001)”;

- Sheet A “Income from sources in the Russian Federation”;

- Sheet B “Income from sources outside the Russian Federation, taxed at the rate (001)”;

- sheet B “Income received from business, advocacy and private practice”;

- sheet D “Calculation of the amount of income not subject to taxation”;

- sheet D1 “Calculation of property deductions for expenses on new construction or acquisition of real estate”;

- Sheet D2 “Calculation of property deductions for income from the sale of property (property rights)”;

- sheet E1 “Calculation of standard and social tax deductions”;

- sheet E2 “Calculation of social deductions established by subparagraphs 4 and 5 of paragraph 1 of Article 219 of the Tax Code of the Russian Federation”;

- sheet J “Calculation of professional tax deductions established by paragraphs 2, 3 of Article 221 of the Tax Code of the Russian Federation, and deductions established by the second paragraph of subparagraph 2 of paragraph 2 of Article 220 of the Tax Code of the Russian Federation”;

- sheet 3 “Calculation of taxable income from transactions with securities and transactions with derivative financial instruments”;

- Sheet I “Calculation of taxable income from participation in investment partnerships.”

In addition to paying personal income tax, the declaration will be useful to receive a tax deduction. By law, every citizen has the right to return part of the tax previously paid to the state to cover the costs of education, treatment, purchase of real estate or payment of a mortgage loan. Submitting documents to receive a deduction is allowed on any day after the end of the year in which the money was spent. The deduction can be received within three years. In this case, the rules on how to correctly fill out the 3-NDFL declaration are as follows:

- When selling an apartment or car that has been owned for less than 3 years, fill out the title page, sheets A, D2 and sections 1 and 2 of the 3-NDFL declaration.

- To pay tax on renting out an apartment, fill out only the title page, sheet A and sections 1 and 2.

- When purchasing an apartment, in order to receive a tax deduction, fill out the title page, sheets A, D1 and sections 1 and 2. Fill out the same pages to receive a personal income tax refund when paying for a mortgage loan.

- You can receive a tax deduction for education or treatment by filling out the title page, sheets A, E1, sections 1 and 2.

- To receive a deduction when paying additional insurance contributions for a funded pension or for expenses under contracts for non-state pension provision and voluntary pension insurance or life insurance, fill out the title page, sheets A, E2, sections 1 and 2.

How to fill out 3-NDFL for different situations

Starting from 2021, tax officials are prohibited from correcting errors in forms! To submit your document to the tax office the first time and quickly receive a deduction, use the ConsultantPlus instructions (here is free access):

- deduction for treatment of yourself or a child;

- deduction for an apartment;

- mortgage interest deduction;

- when selling real estate.

to read.

Expanded list of income codes to fill out

There will be 17 of them (from 10). Here is a table of updated codes:

| Code | Name |

| 01 | Income from the sale of residential houses, apartments, rooms, including privatized residential premises, dachas, garden houses or land plots or share(s) in the specified property, determined based on the price of the object specified in the agreement on the alienation of property |

| 02 | Income from the sale of residential houses, apartments, rooms, including privatized residential premises, dachas, garden houses or land plots or share(s) in the specified property, determined based on the cadastral value of this object, multiplied by a reduction factor of 0.7 |

| 03 | Income from the sale of other property (except for securities) |

| 04 | Income from transactions with securities |

| 05 | Income from property rental (hire) |

| 06 | Income in cash and in kind received as a gift |

| 07 | Income received on the basis of an employment (civil) contract, the tax from which is withheld by the tax agent |

| 08 | Income received on the basis of an employment (civil) contract, the tax from which is not withheld by the tax agent, including partially |

| 09 | Income from equity participation in the activities of organizations in the form of dividends |

| 10 | Other income |

| 11 | Income from the sale of other real estate, determined based on the price of the object specified in the agreement on the alienation of property |

| 12 | Income from the sale of other real estate, determined based on the cadastral value of this property, multiplied by a reduction factor of 0.7 |

| 13 | Income from the sale of vehicles |

| 14 | Income in the form of remuneration received by the heirs (legal successors) of the authors of works of science, literature, art and authors of inventions, utility models and industrial designs |

| 15 | Income in the form of winnings paid by lottery operators, distributors, organizers of gambling conducted in a bookmaker's office and totalizator |

| 16 | Income in the form of winnings paid by the organizers of gambling, not related to gambling in a bookmaker's office and totalizator |

| 17 | Income in the form of the cash equivalent of real estate and (or) securities transferred to replenish the endowment capital of non-profit organizations in the manner established by Federal Law dated December 30, 2006 No. 275-FZ “On the procedure for the formation and use of endowment capital of non-profit organizations” (Collected Legislation of the Russian Federation) Federation, 2007, No. 1 (Part 1), Article 38; 2013, No. 30 (Part 1), Article 4084) |

Other changes:

- new format for recording phone numbers;

- in line 030 you will have to indicate the method of purchasing a residential building;

- an additional line to indicate the social deduction for the purchase of medicines.

Who is obliged to take

Before moving on to step-by-step instructions for filling out 3-NDFL, we will consider the key requirements for this tax reporting form. Let’s determine who, when and how is obliged to report to the Federal Tax Service:

- Private traders and individual entrepreneurs, that is, those citizens who do business independently or carry out private practice.

- Citizens recognized as tax residents in the reporting period and who received income outside the Russian Federation. That is, these are those individuals who stayed in Russia for at least 183 days a year.

- Persons who sold real estate, land plots or vehicles during the reporting period.

- Citizens who received income in the form of lottery winnings, valuable gifts and other income exceeding the maximum permissible limit established for such types of income.

- Persons who received income in the reporting period under work contracts or civil contracts.

- Individuals applying for tax deductions (property, professional, social or treatment).

Where to submit 3-NDFL

The tax return should be submitted to the territorial office of the Federal Tax Service at the place of registration, permanent or temporary. The income statement is submitted to the Federal Tax Service in person, by mail, or by filling out the document online. For example, if you need help filling out the 3-NDFL declaration, then contact the Federal Tax Service or prepare a report online using special tips. Step-by-step instructions on how to fill out 3-NDFL online yourself and for free are given below.

How to calculate the amount of tax deductions in 3 personal income taxes

Line 040 is the amount of tax deductions in the 3-NDFL declaration (second section). The value that needs to be put in this field is displayed using the volumetric formula:

Thus, this field reflects the amount for all claimed deductions:

- standard;

- property;

- social, etc.

Please note that according to the formula, deductions already provided by the employer are also taken into account in line 040. The amount of personal income tax reimbursed in this way is taken into account in line 080.

Important!

If you are reporting on income for which personal income tax is 13%, put “0” in this field.

Detailed calculations for each deduction category separately are carried out in Appendices 3, 5-8 intended for this purpose.

Where to get the 3-NDFL tax return form

To prepare reports to the Federal Tax Service, use the unified tax return form KND 1151020, approved by order of the Federal Tax Service of Russia dated 10/03/2018 No. ММВ-7-11/ [email protected] (as amended by order dated 10/07/2019 No. ММВ-7-11/ [email protected] ] ). The same order established the procedure for filling out 3-NDFL.

IMPORTANT!

As of January 1, 2020, the new structure of form 3-NDFL is in effect. The changes should be applied when preparing reports for the previous year, 2021. If you fill out the old form for income received in 2021, representatives of the Federal Tax Service simply will not accept it.

Second year of application of the property deduction: repeated 3-NDFL declaration

The situation when a property deduction can be applied for several years is typical for real estate purchase situations. For example, if the amount of personal income tax withheld from the taxpayer’s income (taxed at 13% personal income tax) for the period of filing 3-personal income tax is less than 260,000 rubles, the right to the balance of the unused deduction does not expire, but is transferred to subsequent periods.

Example

In 2021, stamper E. B. Lakhtina bought an apartment on the secondary housing market for RUB 1,760,000. During the specified period, personal income tax = 81,120 rubles was transferred to the budget from her salary. Amount of personal income tax to be refunded from the budget:

- calculated from the purchase price: RUB 1,760,000. × 13% = RUB 228,800;

- possible return (for 2021): RUB 81,120.

The balance of personal income tax that can be returned from the budget in subsequent periods: 228,800 – 81,120 = 147,680 rubles.

In 2021, Lakhtina E.B. got an additional part-time job in another company. At the end of 2021, the personal income tax transferred to the budget from the salary she received from 2 employers amounted to 127,000 rubles. - Lakhtina E.B. can return this amount from the budget by again submitting 3-NDFL and other required documents to the inspection (2-NDFL certificate for 2021, application for personal income tax return, documents confirming the purchase of housing).

The balance of the deduction is 20,680 rubles. (147,680 – 127,000) Lakhtina E.B. will return based on the results of 2021 if she again provides the necessary documents to the tax office.

How to fill out 3-NDFL in 2021

Before you start preparing your tax return, please read the basic requirements and instructions for filling out 3-NDFL:

- Fill in the cells from left to right with blue or black ink, or using printing or computer technology.

- Place dashes in empty fields on your tax return. If the indicator value is missing, dashes should be placed in each cell of the indicator field.

- Indicate the amounts of income and expenses in rubles and kopecks, with the exception of personal income tax amounts.

- Specify tax amounts strictly in rubles, apply the rounding rule: up to 50 kopecks - discard, more - round up to the full ruble.

- Cash received in foreign currency and expenses incurred should be reflected in rubles. Recalculate amounts in foreign currency at the exchange rate of the Central Bank of the Russian Federation on the date of receiving the currency or making expenses.

Here are detailed step-by-step instructions for filling out the 3-NDFL declaration in 2021 for 2021 (2019 - last year).

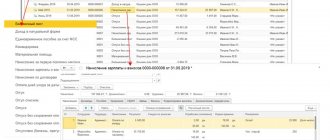

A visual example of filling out 3-NDFL

Let’s look at a specific situation to sample how to fill out the new 3-NDFL certificate form. As an example, let’s file a declaration to receive a professional tax deduction for 2021.

Morskaya Natalya Aleksandrovna worked at PPT LLC in 2021 under an author’s contract. According to paragraph 3 of Art. 221 of the Tax Code of the Russian Federation, the employee is entitled to a professional tax deduction. The amount of the deduction cannot be documented, so the amount is calculated according to the standard - 20% of the amount of taxable income.

For 2021 Morskaya N.A. received income in the amount of 620,000 rubles. The customer did not provide deductions under the author's order agreement. The deduction amount is 124,000 (620,000 × 20%) rubles. The amount of personal income tax to be refunded is 16,120 rubles.

The declaration is filled out as follows:

Where to get a 3-NDFL certificate

Let's start with the basics.

3-NDFL is not a certificate, but a tax return. A document that is drawn up and submitted to the tax authorities by the taxpayer (personal income tax). That is, if you have a question about where to get 3-NDFL for individuals, most likely you are the personal income tax payer, and therefore you must draw up and submit the form yourself. Note! The tax office will only accept a declaration on a current form. The report form for 2021 was updated by order of the Federal Tax Service of the Russian Federation dated 10/07/2019 No. ММВ-7-11/ [email protected] You can download it here. In the same article you will find tips and a sample of filling out the form.

As part of the relationship for paying personal income tax to the budget, there are also so-called tax agents. These are those who, by law, withhold personal income tax from the due payments at the time of settlements with you. The most common example of a tax agent is your employer. He immediately withholds tax from your salary and transfers it to the budget himself. In addition, the tax agent also reports annually on the amounts paid to you and the tax withheld from them. Such a tax agent report is called a 2-NDFL certificate.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

You can get a certificate of income and withheld tax from your employer (or from the one who paid you income, for example, under a civil contract). The certificate will be needed to prove to the tax authorities that personal income tax has already been paid on your working income. By the way, in the same certificate, the tax agent will also show the deductions due to you, which he has already taken into account when calculating personal income tax.

The need to submit 3-NDFL independently appears in two cases:

- During the year ended, there were incomes on which tax was not withheld at the source (accordingly, there was no payment to the budget from the tax agent and no 2-personal income tax).

- Last year there was a right to receive deductions, but tax agents did not take these deductions into account. That is, the tax has been overpaid, and it can be returned through the tax office. To do this, the tax authorities need to show the entire history of income and deductions for the year by filling out the 3-NDFL declaration.