Let's consider why an organization or individual entrepreneur may need to switch to one of the special tax regimes - a taxation system in the form of a single tax on imputed income for certain types of activities, as well as how to make the transition to UTII (register as a single tax payer), where and what kind of application to apply for this.

The taxation system in the form of a single tax on imputed income for certain types of activities (UTII) is regulated by Chapter 26.3 of the Tax Code of the Russian Federation, and in the regions it is put into effect by decisions of the relevant representative bodies in these Subjects of the Federation.

Can be used simultaneously with other taxation systems (regimes).

From 2021, regions have the right to adopt their own laws on the abolition of UTII. And from 2021, UTII should be abolished throughout the Russian Federation.

Why declare a transition to UTII

UTII is one of the most used tax regimes in small businesses. This is explained by:

- One imputed tax replaces several other taxes - on profit, on the property of organizations, VAT, personal income tax (on the income of individual entrepreneurs);

- is paid in a fixed amount, regardless of the amount of income;

- quite simple to calculate;

- the amount of tax depends on the type of activity and, compared to the income received, can be very small;

- the tax can be reduced by the amount of insurance premiums paid;

- Tax accounting and reporting is not complicated. The tax return only needs to be filed once a quarter and is easy to prepare;

- you can switch to it at any time, and not only from the beginning of the year or newly registered;

- the ability to apply it simultaneously with other tax regimes.

Therefore, the transition to UTII has clear advantages and is very beneficial for small businesses.

Registration procedure

To register as a UTII payer, an organization needs to submit an application to the tax office using the UTII-1 form, approved by order of the Federal Tax Service of Russia dated December 11, 2012 No. ММВ-7-6/941. Entrepreneurs submit an application using the UTII-2 form, approved by order of the Federal Tax Service of Russia dated December 11, 2012 No. ММВ-7-6/941.

The application must be submitted within five working days from the date on which the imputed activity began. This date must be indicated in the application. This procedure is provided for in paragraph 3 of Article 346.28, paragraph 6 of Article 6.1 of the Tax Code of the Russian Federation. Application forms approved by order of the Federal Tax Service of Russia dated December 11, 2012 No. ММВ-7-6/941 are applied from January 1, 2013 (letter of the Federal Tax Service of Russia dated December 25, 2012 No. PA-4-6/22023).

The tax inspectorate, having received an application for registration as a UTII payer, is obliged to notify the organization (entrepreneur) of the registration within five working days thereafter. The date of registration as a single tax payer will be the date of commencement of application of UTII specified in the application. This procedure is provided for in paragraph 3 of Article 346.28 of the Tax Code of the Russian Federation.

Situation: should an organization re-register as a UTII payer in the municipality in which it will conduct imputed activities if it is already registered there for other reasons?

Answer: yes, it should.

As a general rule, you need to register as a UTII payer in each municipality where the organization conducts activities for which it intends to apply this special regime. This is provided for in paragraph 2 of Article 346.28 of the Tax Code of the Russian Federation. There are no exceptions in the tax legislation for those who are already registered in these municipalities for tax purposes on other grounds. And without registering as a UTII payer, the organization simply will not be able to exercise its right to apply this special regime. This procedure follows from the provisions of paragraph 1 of Article 346.28 of the Tax Code of the Russian Federation.

An example of registering an organization as a UTII payer

The organization begins to engage in activities subject to UTII without creating a separate division. In the municipality where the organization will conduct activities subject to UTII, the organization is already registered for tax purposes on a different basis.

The organization in the city of Pushkino, Moscow region, has a property (building). At the location of this facility, the organization is registered with the tax office.

In May 2015, the organization installed a vending machine for selling newspapers and magazines in Pushkino. This activity is not related to the creation of a separate unit.

Despite the fact that the organization is already registered with this municipal entity for tax purposes on a different basis, the organization’s accountant sent an application in the form of UTII-1 to the tax office at the location of the vending machine.

How to switch to UTII, application procedure

To determine whether an organization or individual entrepreneur can switch to imputed tax, you need to make sure that a number of conditions are met.

Conditions of transition and application

First of all, the application of a tax in relation to a specific type of activity must be legislatively introduced by a decision of a representative body in the region and municipal area (urban district) where the work is to be done. The list of possible types of activities is established by clause 2 of Article 346.26 of the Tax Code of the Russian Federation, however, in specific regions not the entire list may be applied.

The list of activities includes:

- provision of household services (according to their classification determined by the Government of the Russian Federation;

- provision of veterinary services;

- provision of repair, maintenance and washing services for cars and motor vehicles;

- provision of parking spaces for cars and motor vehicles;

- provision of motor transport services for the transportation of passengers and cargo (no more than 20 vehicles);

- retail trade through shops and pavilions with a sales floor area of no more than 150 square meters;

- retail trade through stationary retail facilities without trading floors, as well as through non-stationary retail facilities;

- provision of catering services through facilities with a service area of no more than 150 square meters;

- provision of catering services through facilities without a customer service area;

- outdoor advertising using advertising structures;

- advertising using vehicle surfaces;

- temporary accommodation and accommodation services using a total area of premises of no more than 500 square meters;

- services for the transfer of temporary possession and (or) for use of retail space in stationary retail facilities without trading floors, non-stationary retail facilities, as well as public catering facilities without a customer service area;

- services for the transfer of temporary possession and (or) use of land plots for the placement of stationary and non-stationary retail facilities, as well as public catering facilities.

To switch to UTII, Article 346.26 of the Tax Code requires compliance with the following criteria:

a) the share in the authorized capital of a legal entity owned by another organization must not exceed 25%;

this restriction does not apply to:

- organizations established by public organizations of disabled people, if disabled employees in them have an average number of at least 50% and a wage fund of at least 25%;

- consumer cooperation organizations and societies established by consumer societies and their unions.

Can you apply UTII

To switch to UTII, your business must meet the following conditions:

- The average number of employees is up to 100 people

- Retail area (or service hall area in public catering) up to 150 sq. m.

- Vehicle fleet size - up to 20 units (for carriers)

- You are not a payer of the Unified Agricultural Tax

- The selected type of activity is subject to UTII in the region in which you conduct it

You cannot switch to UTII in the following cases:

- The activity chosen for UTII is carried out within the framework of a simple partnership agreement, joint activity or trust management

- You carry out trust transactions

- When providing medical services

- When working in social security

- When renting gas stations

An approximate list of activities for which UTII can be applied:

- Veterinary assistance

- Freight and passenger road transportation

- Household services (their list is established by the Government of the Russian Federation in accordance with OKVED)

- Placement of street and outdoor advertising

- Retail

- Catering

- Vehicle washing and repair

- Rental of real estate and land

- Car park services (except penalty fees)

Please note that the list of activities for which the Unified Tax on Imputed Income is allowed is different in each region. Local authorities cannot expand it, but they can reduce it. In some regions (for example, Moscow) this special tax regime does not apply at all. Therefore, before submitting an application to switch to UTII, check whether it can be applied specifically in your region and for your type of activity.

Are you planning to open a sole proprietorship?

Prepare all documents for registration with our service. Fill out a simple form and receive ready-made documents with submission instructions in just 15 minutes. It's secure and free.

Create documentsMore details

Create documentsMore details

Timing of transition to imputation

In accordance with Art. 346.28 of the Tax Code of the Russian Federation, an application for registration must be submitted to the tax authority within 5 working days from the beginning of the application of UTII.

The date of registration will be the date indicated in the corresponding line in the application (according to Article 346.28 of the Tax Code of the Russian Federation).

After receiving the application, within 5 working days the tax authority will issue (send) to the taxpayer a notice of registration under UTII.

According to Article 346.29 of the Tax Code of the Russian Federation, if an organization or individual entrepreneur is registered with the tax authorities as payers of a single tax (as well as their deregistration from such registration) not from the first day of the calendar month, then the amount of imputed income for this month is calculated based on the actual number of days of activity this month.

Violation of the registration deadline

For violation by a taxpayer of the deadline for filing a single tax application, liability may be imposed under Article 116 of the Tax Code of the Russian Federation “Violation of the procedure for registration with the tax authority” - a fine of 10 to 40 thousand rubles.

Presentation to third parties

Sometimes documents on the application of preferential treatment may be required by third parties, for example, during legal proceedings or to work with counterparties. Most often, the taxpayer is written: “I ask you to issue a scanned copy of the notice of application of UTII...”. What document should he prepare? The one issued by the Federal Tax Service. There is no special form that will confirm work under preferential treatment. Or the company can offer the interested person the latest tax return with a mark from the Federal Tax Service on its acceptance. The last option is to provide a copy of the statement of intent to pay a single tax, where it will be clear that it was accepted by an employee of the Federal Tax Service.

Legal documents

- Order of the Federal Tax Service of Russia dated August 11, 2011 No. YAK-7-6/ [email protected]

- Art. 84 Tax Code of the Russian Federation

Application form for UTII

Application forms for the transition to UTII for organizations and individual entrepreneurs are different.

For organizations - this is form No. UTII-1, for individual entrepreneurs - form No. UTII-2, each consists of two pages.

Both forms were approved by order of the Federal Tax Service of the Russian Federation No. ММВ-7-6 / [email protected] dated December 11, 2012.

Application forms for tax registration under UTII can be downloaded from the following links:

on registration of an organization as a taxpayer of a single tax on imputed income for certain types of activities.

on registration of an individual entrepreneur as a taxpayer of a single tax on imputed income for certain types of activities.

These same statements are in PDF format, if this option is more convenient for someone to fill out:

- according to the UTII-1 form for organizations ().

- according to the UTII-2 form for individual entrepreneurs ().

Content

- Can you apply UTII

- Filling out an application to switch to UTII in 2021

- Submitting an application for UTII at the place of business

You can apply the Unified Tax on Imputed Income (UTII) from the moment of registration as an individual entrepreneur (IP). To do this, you need to indicate in the application for registration of individual entrepreneurs (R21001) the codes of types of economic activities (OKVED) that fall under this special taxation regime in your region, and submit an application for the transition to UTII within 5 days after registration.

The single tax on imputed income is a special regime aimed at small and medium-sized businesses for a limited number of activities. Under this tax regime, taxes of the general system - VAT, income tax, personal income tax and property tax - are not paid. These taxes are replaced by a flat tax, which is calculated based on what the government considers the average income for your type of activity. When calculating the tax, the tax rate, physical indicator (area of a retail outlet, number of employees or units of transport, etc.) and adjustment factors are also taken into account. The amount of tax payable is not affected in any way by the amount of revenue received - regardless of the amount of income and its availability, UTII must be paid quarterly.

Sample of filling out an application for UTII

Let's consider filling out samples for organizations and individual entrepreneurs.

For organizations

When filling out an application on the UTII-1 form for an organization, you need to enter the following data:

a) on the first page

- TIN and checkpoint of the organization;

- code of the tax authority to which the application is submitted;

- select and enter in the field a number indicating that the organization is Russian or foreign;

- full name of the organization;

- OGRN of the organization;

- start date of activities under UTII;

- depending on the person signing the application, enter the number “1” or “2” in the field;

- Full name, tax identification number and telephone number of the head or representative of the organization;

- power of attorney data if the application is signed by a representative;

- date of signing the application.

When signing an application by a representative, a power of attorney is attached as an attachment.

b) on the second page

- activity type code (given in Appendix No. 5 to the Procedure for filling out the UTII declaration, approved by order of the Ministry of Finance and the Federal Tax Service of the Russian Federation No. ММВ-7-3 / [email protected] dated 07/04/2014);

- address of the place of business (postal code, code and name of the region, district, city, town, street, house, office/apartment);

- applicant's signature.

On this page it is possible to indicate details of three different places (or types) of activity. If there are more than three, you should fill out the required number of such pages.

The second and subsequent pages are also appendices to the first page. The number of applications must be indicated on the first page of the application.

Form UTII-1 for legal entities in 2021

Any company operating under the general taxation regime (OSNO) and the simplified taxation regime (USN) has the right to switch to the UTII regime, however, OSNO taxpayers can do this at any time, and taxpayers under the “simplified taxation regime” - only from the beginning of the calendar year.

Application structure:

- The name of the company indicating its residence (Russian or foreign);

- OGRN (main state registration number) of the organization;

- TIN and checkpoint of the organization;

- Code of the Federal Tax Service accepting the application;

- Start date of application of the Single tax on imputed income;

- Personal data of the applicant: full name, telephone number, signature and position (manager or representative of the manager - by proxy);

- Date of application.

About the rules for filling out: The form is filled out in printed capital letters, which are entered one by one into the empty cells. Each punctuation mark will also occupy one cell. About attachments: documents are attached to the application for the use of UTII, which list the types of activities of the legal entity and the address where they are carried out.

Important point: If the company has been reorganized, then the special tax regime in force until the moment of reorganization does not transfer to the already reorganized company, that is, the application for the transfer of UTII must be submitted again, according to the letter of the Ministry of Finance of the Russian Federation No. GD-4-3/ 9560 dated July 4, 2015.

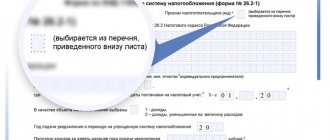

A sample of UTII-1 is shown in the figure below.