The simplified tax system declaration is a relatively simple reporting. You can fill it out yourself by hand on paper or prepare it on a computer. Declaration and a sample form can be found here.

But there is an even easier way to prepare the simplified tax system declaration for 2021 - in the online service. As a result, you will receive a report file ready for printing in Excel or pdf format. We will tell you how to do this in our article.

Prepare a simplified taxation system declaration online

How to work in the online service for preparing a simplified taxation system declaration

First, you need to register in the service by indicating your email address and accepting the terms of processing of personal data.

When you go to your personal account to the page for generating a simplified taxation system declaration, the following window opens.

Here you need to select the category of taxpayer and the taxation option for the simplified tax system: Income or Income minus expenses.

Pay attention to the line “Title Page”. If, for some reason, you do not want to indicate the registration data of an individual entrepreneur or LLC in the service itself, then you can prepare a declaration without them. In this case, choose the excel format and, after downloading the declaration with numerical indicators, enter your data yourself.

But, of course, it’s easier to provide the necessary data directly in the service. We guarantee our users compliance with the privacy policy.

If you check the “Fill in” box next to the title page, new fields will open in the interface. Next to each of them there are corresponding footnotes and hints.

Now, using examples, let's see what a completed simplified taxation system declaration looks like in the service interface and in finished form for printing.

An example of filling out a simplified taxation system Income declaration in the online service

First, we will select the payer category of the simplified tax system 6 percent. In our example, this will be a declaration for individual entrepreneurs without employees. We prepare the title page directly in the online service, so we have a checkmark next to the “Fill in” field.

Please note: for example, we have indicated a conditional TIN, but you need to enter your real tax number, otherwise the declaration will not be generated.

If the declaration is not submitted by the taxpayer himself, then in the field “Submits the declaration” you must select the “Representative” option. In this case, additional fields will open to indicate the details of the power of attorney.

As for the date of filing the declaration, if you are not sure that you will file the report on a specific day, you do not need to tick the appropriate box. In this case, you will add the date and personal signature later by hand.

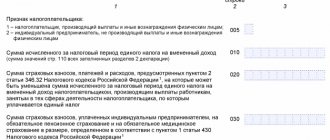

We proceed to filling out the second part of the simplified tax system declaration - income received and insurance premiums paid. According to tax accounting rules, these indicators are reflected in the declaration in an increasing order from the beginning of the year.

However, in the service fields you need to indicate income and contributions separately for each quarter, and not from the beginning of the year. This is stated in the footnotes of the corresponding fields.

Let's assume our entrepreneur received the following income:

- 1st quarter – 100,000 rubles;

- 2nd quarter – 230,000 rubles;

- 3rd quarter – 170,000 rubles;

- 4th quarter – 220,000 rubles.

It is in this form that income data must be entered into the fields of the service. In the finished declaration, they will be displayed, as expected, on an accrual basis from the beginning of the reporting year.

Next, you need to indicate in the service fields the insurance premiums paid in each quarter separately. The declaration will reflect not just the contributions paid, but those amounts that reduce the calculated tax payment.

For example, the individual entrepreneur from our example paid 7,000 rubles in contributions for himself in the 1st quarter. But since the advance payment for the 1st quarter is equal to 6,000 rubles, then this amount will appear in the corresponding line of the declaration (the maximum possible to reduce the tax), and not the 7,000 rubles that were paid.

All that remains is to indicate the tax rate. The standard simplified tax rate is 6%, but individual entrepreneurs apply a zero tax rate during the holidays, then they need to indicate 0% in these fields.

If there was no income in a certain quarter or the individual entrepreneur was registered in the last months of the year, then you still need to fill out all the fields at the rate that was in effect during the year. An exception is USN Income payers who moved to or left Crimea during the year. Then some quarters may be taxed at a rate of 6%, and some at a rate of 3%.

In addition, the service for generating simplified taxation tax declarations allows you to take into account expenses when paying the trade tax (currently valid only in Moscow). If necessary, indicate the paid trading fee, you must check the appropriate box.

The entrepreneur from our example does not pay a trade tax, so the fields of his declaration in the interface look like this.

All that remains is to choose in what format you want to receive the completed simplified taxation system declaration and download it for printing. The finished declaration following our example, prepared in the online service, can be downloaded here for review.

Your simplified taxation system declaration will, of course, indicate the data that you entered into the service fields.

How to pay tax according to the simplified tax system

Advance payments under the simplified tax system are paid:

- 1 quarter until April 25,

- half a year before July 25,

- 9 months before October 25th.

The tax payment deadline under the simplified tax system for LLCs is March 31, for individual entrepreneurs - April 30.

If an individual entrepreneur does not have employees, then he can reduce the tax according to the simplified tax system by the entire amount of insurance premiums paid during the year. LLCs and individual entrepreneurs that have employees can reduce the tax by no more than 50%.

For failure to pay advance payments (tax) under the simplified tax system, penalties may be charged in the amount of 1/300 of the refinancing rate of the Central Bank of the Russian Federation for each day of delay. Failure to pay tax may also result in a fine ranging from 20 to 40% of the unpaid amount.

An example of filling out a simplified taxation system declaration in the online service: Income minus expenses

The first part of the declaration for the simplified tax system Income minus expenses is filled out in the same way as the declaration for the simplified tax system Income, so we will not repeat it.

The second part of the declaration is filled out differently. Firstly, there are separate fields for indicating expenses incurred. Secondly, insurance premiums for this version of the simplified system are included in the total amount of expenses and are therefore not indicated separately. Thirdly, for the simplified tax system Income minus expenses, other tax rates are applied: from 5% to 15% (rates are established by regulations of the constituent entities of the Russian Federation). Fourthly, there is a separate field for reflecting losses from previous years in the declaration, if any.

Tax accounting rules for the simplified tax system Income minus expenses are close to the calculation of income tax. In addition, there are features of accounting for certain types of costs, for example, goods purchased for resale. If you are unsure whether you have accounted for your expenses correctly, we recommend that you seek a free tax consultation.

For an example of online filling out a declaration under the simplified tax system Income minus expenses, let’s take Vega LLC. The organization did not have any losses in previous years, the tax rate is standard – 15%. This is what the completed interface fields look like.

In the completed declaration for this example, income and expenses are reflected in an accrual order, as for the simplified tax system Income.

Filling out a declaration using a specific example

The rules for filling out a document in the event of termination of activity are similar to the rules used when preparing annual reports. But there are several differences:

- The tax period code is not 34, as in annual reporting, but 50;

- since the individual entrepreneur ceased operations before the end of the year, there will be dashes in those reporting periods that were not completed.

- Insurance premiums paid after the date of termination of activity are not taken into account.

Let's consider filling out a declaration on the occasion of termination of the activities of an individual entrepreneur. This sample was generated automatically using the form located in the left column of the site.

Initial data to fill:

IP Vosmerkin Nikodim Panteleevich.

The date of entry into the Unified State Register of Entrepreneurs about the termination of activities is 08/13/2019.

Income received in the 1st quarter - 454,551 rubles, in the 2nd quarter - 333,211 rubles, in the 3rd quarter - 123,041 rubles.

Contributions to the Pension Fund and the Federal Compulsory Medical Insurance Fund in the 1st quarter - 9059.5 rubles, in the 2nd quarter - 9059.5 rubles. The entrepreneur paid the remaining amount in the 3rd quarter (you can calculate it using our individual entrepreneur insurance premium calculator), but since this amount was paid after the date of termination of activity, it is not taken into account in the calculations.

Individual entrepreneur is a payer of trade tax, paid in the 1st quarter - 3433 rubles, in the 2nd quarter - 3323 rubles. In the 3rd quarter, the trade tax debt was paid, but since this amount was paid after the date of termination of activity, it is not taken into account in the declaration.

We fill out the form fields using the original data, check the “Generate declaration for printing” checkbox, and fill out “Data for the title page”.

Click the “Calculate” button and download the finished declaration using the link that appears. Despite the fact that the entrepreneur “closed” in August, there were dashes in the lines of the document for the reporting period of 9 months.

As already mentioned, when terminating the activities of an individual entrepreneur, the tax period is considered to be the period from January 1 to the date of closure of the individual entrepreneur, so there is simply no reporting period of 9 months in our example.

You can download this sample declaration when closing an individual entrepreneur in PDF format with calculations and explanations.

Deadlines for submitting the simplified tax system declaration

Please note - due to the coronavirus pandemic, for some individual entrepreneurs and organizations the deadlines for paying taxes and filing reports may be postponed, brief information in the summary table from the Federal Tax Service, details are described in this article.

The deadline for submitting a declaration under the simplified taxation system depends on the legal form of the taxpayer:

- organizations - no later than March 31 of the year following the reporting year;

- individual entrepreneurs - no later than April 30 of the year following the reporting year.

The zero declaration for the year is submitted within the same deadlines. In addition, special deadlines have also been established for filing a simplified taxation system declaration for certain situations: deregistration or violation of the requirements for this regime.

How to submit a declaration using the simplified tax system

A declaration under the simplified tax system at the end of the year must be submitted for LLCs by March 31, for individual entrepreneurs by April 30.

When switching to another taxation regime or terminating activities, the declaration must be submitted no later than the 25th of the next month.

The declaration can be submitted in person or through a representative with a notarized power of attorney, or sent by mail with a letter with the declared value and a description of the investment.

Attention ! If you delay filing your return for more than 10 business days, the tax office may block your current account.

For failure to submit a declaration under the simplified tax system, a fine may be imposed in the amount of 5% of the unpaid tax amount for each month of delay, but not more than 30% and not less than 1000 rubles.

Is a two-dimensional barcode required for a simplified taxation system declaration?

Note! Some tax inspectorates have a practice of refusing to accept declarations without a two-dimensional barcode. Refusal for such a reason is not legal.

An exhaustive list of legal grounds is contained in clause 28 of Order No. 99n of the Ministry of Finance of Russia dated 07/02/2012 and does not contain a requirement for a two-dimensional barcode. The Federal Tax Service writes about the same in a letter dated April 18, 2014 N PA-4-6/7440: “The absence of a two-dimensional barcode on the tax return form or the submission of a tax return in a form that corresponds in terms of the composition of indicators to the approved form, but is not subject to processing in an automated way, are not reasons for refusing to accept the corresponding tax return.”

If you are denied acceptance of a declaration for this reason, request a written refusal indicating the reason (most likely at this stage the problem will be resolved in your favor) and appeal it through pre-trial dispute resolution.