UTII Declaration 2021: changes

[email protected] is still in effect.

Declaration form for UTII for the 1st quarter of 2021

Despite the fact that there were no amendments, when preparing reports it is necessary to take into account changes in the procedure for accounting for expenses for the purchase of cash registers: from 01/01/2020, tax collectors can no longer reduce the tax on expenses for the purchase of online cash registers.

Let us remind you that individual entrepreneurs who purchased and registered an online cash register before 07/01/2019 had the right to take into account expenses (no more than 18,000 rubles) when calculating the imputed tax. If the amount of expenses was not completely exhausted at one time, it could be transferred to other periods.

From 01/01/2020, the cash register deduction no longer applies. Accordingly, Section 4 no longer needs to be filled out, but it is still included in the reporting.

Results

The UTII declaration is prepared on a form that is updated annually due to changes made to tax legislation. The next update (in connection with the introduction of a deduction for individual entrepreneurs for the costs of purchasing online cash registers) occurred with the reporting for the 4th quarter of 2021. It is on this form that you need to report for the 1st quarter of 2020. The tax calculation procedure reflected in section 2 of the declaration has not undergone any fundamental changes.

Sources:

- Tax Code of the Russian Federation

- Order of the Ministry of Economic Development of Russia dated October 30, 2018 N 595

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

When, where and how is the UTII declaration for the 1st quarter of 2020 submitted?

Reporting on UTII is quarterly. The deadline for submitting it to the Federal Tax Service is until the 20th day of the month following the previous quarter. If the due date falls on a holiday or weekend, it is postponed to the first working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

The UTII declaration for the 1st quarter of 2021 must be submitted to the Federal Tax Service by 04/20/2020.

Delivery methods:

- On paper (in person or through a representative).

If a representative submits the declaration, he must have a notarized power of attorney.

- By mail.

It is better to send reports by mail by registered mail with a list of attachments and acknowledgment of delivery.

- Via TCS through electronic document management operators.

When sending a declaration in this way, it must be signed with an enhanced qualified digital signature. You can learn about what this is from the article “Electronic signature tools - what are they?”

Reporting on UTII is submitted to the Federal Tax Service at the place of business, except for those types of activities that require a traveling nature of the work:

- delivery or distribution retail trade;

- placement of advertising objects on vehicles;

- provision of services for the transportation of passengers and cargo.

When carrying out these types of activities, a report on UTII must be submitted to the Federal Tax Service at the location of the imputed organization or place of residence of the individual entrepreneur.

When to take it

They report on “imputation” quarterly. Unlike other regimes, UTII is calculated for each quarter separately. There is no talk of cumulative calculation.

The deadline is the 20th day of the month following the reporting quarter. If the due date falls on a non-working day or holiday, then it is permissible to report on the first working day after.

The deadlines for submitting the UTII declaration are collected in the table:

| Reporting period | Deadline for submission |

| 4th quarter 2020 | 20.01.2021 |

| 1st quarter 2021 | They don't rent |

| 2nd quarter 2021 | They don't rent |

| 3rd quarter 2021 | They don't rent |

| 4th quarter 2021 | They don't rent |

IMPORTANT!

The 4th quarter of 2021 is the last time we submit the report. The special tax regime for imputed income is valid until the end of 2020. It will be canceled starting from 2021 (letter of the Federal Tax Service No. AB-4-19/ [email protected] dated 03/11/2020). For 2021, reports on UTII are no longer provided.

Filling out the UTII declaration 2021: general requirements

The UTII declaration must be filled out in strict accordance with the requirements given in Appendix No. 3 to Order No. MMV-7-3 / [email protected] :

- Data is entered into the report from left to right from the first acquaintance. Numerical indicators are aligned to the right (when filled out using software).

- When filling out on a computer, you must use the Courier New 16-18 font.

- The data is recorded in printed capital letters, regardless of the method of filling out the declaration.

- If there are no indicators in any line or field, they need to be marked with dashes. This need not be done if the declaration is drawn up in a special program.

- When completing the report by hand, use black ink only.

- Changes cannot be made to the finished report either using special means (putty, proofreader) or by crossing out errors. This is due to the fact that the declaration is checked by a machine, not a person.

- Printing is only allowed on one side.

- You cannot fasten declaration sheets with a stapler or other methods that damage the barcode in the upper corner of the page. It is advisable not to even use paperclips as they can damage the barcode, causing the machine to be unable to “read” the report and causing it to be returned. It is better to submit the declaration to the inspector in a separate file.

- Write down the values of physical indicators in full rubles (discard anything less than 50 kopecks, and round up anything more to the nearest ruble).

Title page of the UTII declaration

On the title page, as well as on all subsequent pages, the TIN and KPP of the legal entity are indicated. The IP field of the checkpoint is not filled in due to lack of data.

If the declaration is original, then the adjustment number “0” is indicated; in case of clarification, it is necessary to indicate “1”, “2”, “3”, etc., respectively.

For the declaration for the fourth quarter of 2021, the period of “24” is indicated.

Next, you must indicate the code of the tax authority to which the declaration is being submitted.

The “Taxpayer” field is intended to indicate the full name of the legal entity.

Next, indicate the code of the reorganization form, as well as the TIN/KPP of the reorganized organization, if relevant information is available.

The title page contains information about the contact telephone number and reflects the number of completed pages of the declaration.

The full name of the director or representative responsible for the accuracy of the information provided is indicated in a separate block. This is followed by a signature and date.

Title page

Sample UTII declaration 2021 + instructions for filling out

Let's look at the procedure and features of reporting on UTII using an example. The order of filling out the sections is presented in the order in which it is used in practice: Title page, Section 2, Section 3 and Section 1.

Example

The example conditions are presented in the table:

| Taxpayer | LLC "Kadrovik" |

| Kind of activity | Providing repair, maintenance and washing services for motor vehicles |

| Place of business | Voskresensk, Moscow region |

| Data for tax calculation |

|

| Insurance premiums for employees | RUB 84,230 |

Deadlines for filing UTII declaration in 2021

In 2021, the deadline for filing UTII declarations has been preserved for business entities. As in 2021, reports are submitted quarterly, by the 20th day of the month following the reporting period.

If the deadline for filing a declaration falls on a weekend, the document can be submitted no later than the next business day.

The place of filing the UTII declaration for an organization is the territorial body of the Federal Tax Service at the place of registration of the legal entity, for individual entrepreneurs - at the place of residence of the entrepreneur.

General information about the deadlines for filing a declaration and paying UTII is presented in the table below: (click to expand)

| UTII reporting period | Deadline for filing UTII declaration | Deadline for payment of UTII tax |

| 1 sq. 2021 | 04/22/2021 (04/20/2021 is a day off) | 25.04.2021 |

| 2 sq. 2021 | 07/22/2021 (07/20/2021 is a day off) | 25.07.2021 |

| 3 sq. 2021 | 10/21/2021 (10/20/2021 – day off) | 25.10.2021 |

| 4 sq. 2021 | 20.01.2021 | 01/27/2021 (01/25/2021 is a day off) |

Filling out the Title Page

The title page contains basic information about the imputator:

| TIN and checkpoint | We enter the TIN in accordance with the tax registration certificate. Organizations indicate a 10-digit TIN and KPP. IP - only TIN, consisting of 12 characters. In empty cells, the TIN (for organizations the TIN is 2 digits shorter) and the checkpoint (the individual checkpoint is not filled out) must be filled in with dashes |

| Correction number | |

| Reporting year | We indicate the year for which the declaration is being submitted - 2020 |

| Submitted to the tax authority | We enter the code of the Federal Tax Service to which the report is submitted. You can find it in the registration certificate or on the website of the Federal Tax Service of the Russian Federation |

| By place of registration (code) | We reflect the code of the place of reporting. You can find it in Appendix No. 3 to the Procedure[/cplink]. Organizations in relation to repair, maintenance and washing services for motor vehicles indicate code “214”. Individual entrepreneurs for this type of activity enter code “120”. The rest of the codes can be found here: |

| Taxpayer | Enter the full name of the organization or full name of the individual entrepreneur (line by line, without indicating the status of “Individual”) |

| Contact phone number | We indicate the current phone number in the format: country code - city code - phone number |

| On... application pages... | We enter the number of pages that make up the declaration (4) and the total number of sheets of documents attached to the report (for example, a power of attorney for a representative) |

| Reliability and completeness... | When submitting the declaration in person, enter code “1”; when submitting through a representative, enter code “2.” The lines “Full name” must only be filled in:

The lines “Name of the organization-representative of the taxpayer” are filled in only if the report is submitted for the imputed organization by the representative organization. Representatives enter information about the power of attorney (the word “power of attorney”, number and date of preparation) in the line “Name and details of the document...” |

| Signature and date | If the declaration is submitted by a representative, then his signature is affixed. When submitting the report in person, the imputation officer himself signs. The date of signing the document is also indicated |

The procedure for filing a UTII declaration

The UTII declaration can be submitted to the tax authority both on paper and electronically using TKS.

If a taxpayer fills out a paper return manually, black, blue or purple ink may be used. If computer technology will be used to fill out, then you can use the capabilities of Word or Excel.

Companies can also use special software “Legal Taxpayer”, which allows them to fill out declarations, including UTII. The program installation file and the necessary updates are posted on the Federal Tax Service website.

Filling out Section 2

This section contains information about the main indicators and types of imputed activities carried out.

If several types of activities are transferred to UTII, you will need to fill out as many Sections 2 as there are types of imputed activities you carry out.

Several Sections 2 will need to be completed if there is only one type of imputed activity, but there are several places where it is carried out. For example, several stores with different addresses within one OKTMO.

| Page 010 | We enter the code of the type of activity transferred to UTII. You can find it out in Appendix No. 5 to the Procedure: |

| Page 020 | We indicate the address at which the imputed activity is carried out. The subject code is selected from Appendix No. 6 to the Procedure. The Moscow region corresponds to the code “50”, Moscow - “77”, St. Petersburg - “78” |

| Page 030 | Enter the OKTMO code at the address from page 020 |

| Page 040 | We reflect the amount of basic profitability by type of imputed activity. You can find it out in paragraph 3 of Art. 346.29 Tax Code of the Russian Federation. To provide services for repair, maintenance and washing of motor vehicles, the base income is 12,000 |

| Page 050 | Enter the deflator coefficient K1. It is established once a year and applies to all types of activities. In 2021, K1 is 2.005 (approved by Order of the Ministry of Economic Development of Russia dated December 10, 2019 No. 793) |

| Page 060 | We indicate the size of the correction factor K2. You can find it out from the legal act of the local government authority. It is established separately for each type of activity, depending on the place of its implementation and other features. You can find out which legal act approves the value of K2 on the Federal Tax Service website. To do this, in the upper left corner, select the region in which the imputed activity is carried out. Then we go to the very bottom of the page “Features of regional legislation” and select the municipality in which the activity is carried out (if there are several of them): |

| Page 070-090 | In column 2 we enter the size of the physical indicator monthly. You can find it out in paragraph 3 of Art. 346.29 Tax Code of the Russian Federation. This value is individual for each type of activity and depends on the number of employees, premises area, number of vehicles, etc. When providing services for repair, maintenance and washing of motor vehicles, the physical indicator is the number of employees, including individual entrepreneurs. We enter information in column 3 only if the imputed activity began (ended) in the middle of the quarter (reporting period). When switching to UTII, enter the number of days from the date of transition to the end of the month. When deregistering, we indicate the number of days from the beginning of the month to the day specified in the UTII-3 or UTII-4 notification. In column 4 we indicate the size of the tax base, calculated using the formula: page 040 x page 050 x page 060 x 070 (080 or 090) |

| Page 100 | We indicate the total amount of the tax base for all 3 months. To do this, add up the values of lines 070, 080 and 090 from column 4 |

| Page 105. | Enter the rate for UTII. If the municipality does not apply a reduced rate, indicate the value “15.0” |

| Page 110. | We determine the amount of imputed tax using the formula: line 100 x line 105: 100 |

Filling out the declaration

In 2021, the declaration form was not changed, so the form from the Federal Tax Service Order No. ММВ-7-3/ [email protected] dated 06/26/2018 (hereinafter referred to as the Order) is used. It has 4 sections, but the last one has lost its relevance since the reporting for the current quarter. It is convenient to fill out the declaration in the following sequence: title page, sections 2, 3, 4 and, as a result, section 1.

Title page

The top two lines of the title, as well as the rest of the report sheets, are intended for the TIN and KPP. Individual entrepreneurs indicate only the TIN. In addition, the second line contains the page number.

Next, the title page is filled out as follows:

- adjustment number - “0—”, which means the primary nature of the report;

- The tax period code must be taken from Appendix No. 1 to the Order. Since we are filling out the UTII declaration for the 1st quarter of 2021, we put code 21;

- reporting year - 2020;

- tax authority code—indicate the Federal Tax Service code where the UTII payer is registered (in the example it is 5022);

- The code for the place of registration is taken from Appendix No. 3 to the Order. Most often, code 310 is suitable for an organization. This means that, as a UTII payer, it is registered with the Federal Tax Service at the place of business;

- the name of the company as in the charter. If the declaration is filled out by an individual entrepreneur, he should enter his name, surname and patronymic on a separate line;

- contact number;

- number of declaration sheets - 5;

- number of sheets of copies of supporting documents, if attached. In our example there are none.

We will separately consider the block for confirming the completeness and reliability of data. It is filled out like this:

- if the director signs the declaration independently, code 1 is reflected in the first field, and the name, surname and patronymic of the director are indicated in the three subsequent lines. In this case, any authorized person can submit a report by power of attorney - its data does not appear on the form. In addition, the date of signing is indicated. All other fields are filled in with dashes;

- if the declaration is signed by a representative citizen, code 2 is indicated in a single field. His full name is written in the next three lines, and the details of the power of attorney are written in the lower two;

- if the representative office is entrusted to the company, you also need to indicate code 2. And below, enter the full name of the employee whose signature will appear on the report. Next, write down the name of the representative company and details of the power of attorney.

Section 2

Here we will calculate UTII for the 1st quarter of 2021 for Vasilek LLC. The upper part is filled in like this:

- 010 - activity code from Appendix No. 5 to the Order. In our case it is 03;

- 020 - detailed address of the place of business. The region code must be taken from Appendix No. 6 to the Order;

- 030 - OKTMO;

- 040 - basic yield (BR), that is, 12,000;

- coefficient K1 - 2.005;

- coefficient K2 - 1.

In lines 070-090 you need to indicate monthly:

- in column 2 - physical indicator (PI), that is, 10;

- in column 3 - how many days in a month the activity was carried out, if registration or deregistration took place in it. If the month is fully worked, dashes are added;

- in column 4 - calculation of the tax base for UTII for the month according to the formula: DB x FP x K1 x K2. the calculation is as follows: 12,000 x 10 x 2.005 x 1 = 240,060 rubles. This amount will be for each month, since the number of employees did not change in the quarter.

The following indicates the base for the quarter and the tax amount by line:

- 100 - the sum of tax base indicators for all months of the quarter (columns 4 lines 070-090): 240,060 + 240,060 + 240,060 = 721,800 rubles;

- 105 — UTII rate 15%;

- 110 - tax for the period (excluding deductions for insurance premiums): 721,800 * 15% = 108,270 rubles.

Section 3

The section is intended to indicate deductions and calculate the final amount of UTII that must be paid for the quarter. You should fill out its lines like this:

- 005 - code 1. This means that the taxpayer makes payments to individuals;

- 010 - tax amount excluding contributions from line 110 of section 2;

- 020 - the amount of insurance premiums paid in the reporting quarter, by which the tax can be reduced. Organizations can reduce the payment by a maximum of 50%. The previously calculated UTII amount is 108,270 rubles, half of this amount will be 54,135 rubles. This is exactly how much can be deducted, even though contributions for employees of Vasilek LLC in the 1st quarter amounted to 270,000 rubles;

- 030 - dashes, since the line is intended for individual entrepreneurs. Here they indicate the amount of contributions for themselves by which they can reduce the tax;

- 040 - also dashes, since the cash deduction was available only for individual entrepreneurs and is no longer relevant;

- 050 - amount of tax to be paid: 108,270 / 2 = 54,135 rubles. This is exactly how much UTII should be paid by Vasilek LLC for the 1st quarter of 2021.

Section 4

In all fields of this section, in addition to the top two lines with TIN, KPP and page number, dashes are placed. Previously, it could be filled out by entrepreneurs claiming deductions through online cash registers, but from the beginning of 2021 they do not have this option.

Section 1

It remains to enter the calculation results in section 1. Here you should indicate:

- in line 010 - OKTMO;

- in line 020 - the amount of UTII that needs to be transferred to the budget, that is, 54,135 rubles.

This completes filling out the report. Do not forget to sign and date on the title page and in section 1. The UTII tax return for the 1st quarter of 2021 can be submitted to the Federal Tax Service in any convenient way - submitted in person or with a representative, sent by mail or electronically through an EDI operator. The main thing is to do this no later than April 20.

The tax payment deadline for the 1st quarter of 2021 is April 27 - it has been postponed due to the fact that the 25th falls on a Saturday.

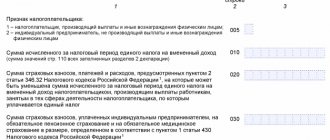

Filling out Section 3

Section 3 contains information on the amounts of insurance premiums paid for employees and individual entrepreneurs for themselves.

| Page 005 | If there are hired workers, enter code “1”; if they are absent, enter code “2”. Organizations always put the code “1” in this line, even if it employs only one person - the general director. Code “2” can only be set by individual entrepreneurs who do not have employees |

| Page 010 | We reflect the total amount of calculated imputed tax for all types of activities. To do this, we sum up lines 110 of all sections 2 (if there are several of them) |

| Page 020 | We indicate the amount of insurance premiums paid for employees (no more than 50% of the tax calculated for payment). We pay insurance premiums paid for employees, subject to a limit of 50% of the tax amount. In our case, the amount of contributions paid for employees was 84,230 rubles, but we can only take into account 10,827 rubles when calculating the tax. (21,654 x 50%). This procedure is enshrined in clause 2.1 of Art. 346.32 Tax Code of the Russian Federation. When combining several tax regimes, line 020 needs to reflect only those contributions paid for employees engaged in imputed activities |

| Page 030 | This line is filled in only by individual entrepreneurs who have paid fixed insurance premiums in the amounts established by clause 1 of Art. 430 Tax Code of the Russian Federation |

| Page 040 | From 01/01/2020 this line is not filled in. Previously, it included the amount of expenses for the purchase of an online cash register by an entrepreneur who purchased and registered it before 07/01/2019 |

| Page 050 | We indicate the final amount of imputed tax to be paid, taking into account insurance premiums. It is calculated according to the formula:

page 010 - (page 020 + page 030) Please note that the resulting result cannot be less than page 010 : 50%.

page 010 - page 030. If the result is negative, indicate the value “0” |

Section 3 of the UTII declaration

After Section 2, you should proceed to filling out Section 3, which displays the tax amounts for the tax period.

First, you need to indicate the appropriate value in the “Taxpayer Attribute” field.

Line 010 is intended to summarize the amounts of calculated tax on lines 110 from Section 2. Let us recall that the number of Sections 2 corresponds to the number of types of activities carried out in the company.

In the example under consideration, there is one type of activity, therefore, one Section 2.

Line 020 shows the amount of contributions in relation to hired personnel and other expenses, due to which the final amount of tax can be reduced (for example, payment of sick leave at the expense of the employer).

As a general rule, December contributions are transferred in January, but as you know, in 2021 the UTII regime is no longer valid. What should I do?

In this case, Federal Law No. 373-FZ of November 23, 2021 introduced a new condition: December contributions and benefits from line 020, transferred in January, can be used to reduce the amount of tax in the fourth quarter of 2021. It is worth noting that only those amounts that were calculated in relation to personnel involved in the activities of UTII can be taken into account.

Using the amount on line 020, you can reduce the amount of tax payable, but by no more than 50% of the value on line 010.

Line 030 in this case is not filled in, since it is intended for individual entrepreneurs paying a fixed amount of insurance premiums.

Line 050 indicates the total amount of tax payable to the budget, which is calculated as the difference between lines 010-040.

The value of line 050 must be greater than or equal to zero.

Section 3

Filling out Section 1

This section is filled out last, it indicates the amount of tax to be paid to the budget at the end of the reporting period for each OKTMO.

| Page 010 | We indicate OKTMO at the address from page 020. If there are several OKTMOs, then fill in as many lines 010 as there are OKTMO codes |

| Page 020 | We enter the amount of imputed tax payable for each OKTMO code. The value of this line is calculated using the formula: page 050 x (page 110 of all Sections 2 for this OKTMO: page 010 of Section 3) When carrying out only one type of activity (in one OKTMO), dashes must be placed in all other lines |

Section 4

From 01/01/2020, this section of the declaration is no longer filled out, since individual entrepreneurs no longer have the right to take into account the costs of purchasing a cash register. Most likely, this section will be removed in the new declaration form, but until then it must be included in the reporting, even if only with dashes.

Sample UTII declaration for the 1st quarter of 2020

You can also see a sample of filling out the UTII declaration on the K+ website.

Fine for late submission of UTII declaration

| Type of offense | Type of sanction |

| Late submission of UTII declaration | Fine (Article 119 of the Tax Code of the Russian Federation):

|

| A fine for officials of the organization in the amount of 300 to 500 rubles. (Article 15.5 of the Code of Administrative Offenses of the Russian Federation). | |

| Late submission of reports by more than 10 days | Blocking of current account (clause 2 of article 76 of the Tax Code of the Russian Federation) |

UTII report for the 1st quarter of 2021: form and submission deadline

“Imputed” persons are obliged to report for the 1st quarter of 2021 until April 20, 2020 inclusive (clause 3 of Article 346.32 of the Tax Code of the Russian Federation), and pay tax no later than April 27, 2020.

For late filing of the report, a fine of 5 to 30% of the unpaid tax amount is imposed, but not less than 1000 rubles. (Clause 1 of Article 119 of the Tax Code of the Russian Federation). For delay in filing a report by more than 10 days, the Federal Tax Service may apply such an effective sanction as blocking the payer’s bank accounts. It is produced on the basis of clause 3 of Article 76 of the Tax Code of the Russian Federation. The blocking will be lifted after the taxpayer submits the return.

In case of late payment of the “imputed” tax, penalties are charged (Article of the Tax Code of the Russian Federation). And for late payment due to incorrect tax calculation, in which the tax base turned out to be underestimated, a fine in the amount of 20-40% of the calculated tax is imposed (Article 122 of the Tax Code of the Russian Federation).

You can submit a declaration:

- on paper (by Russian Post or by appearing in person at the Federal Tax Service);

- electronically through the “Taxpayer’s Personal Account”.

The UTII form for the 1st quarter of 2021 was approved by order of the Federal Tax Service of the Russian Federation No. MMV-7-3 / [email protected] dated June 26, 2018 (KND 1152016). That is, for the report for the 1st quarter of 2021, the same form is used in which payers reported for the 4th quarter of 2021. The procedure for filling out is given in Appendix No. 3 to the mentioned order.

The form includes a title page and sections:

- 1 – total amount of tax payable;

- 2 – calculation of UTII separately for each type of “imputed” activity, indicating the address of the place where it is carried out (the required number of sheets is filled out);

- 3 – calculation of the total tax amount (for all types).

Section 4 on expenses for the purchase of cash register systems in 2021 is not completed, because this deduction could be applied in 2021 and 2021.

Latest news: extension of UTII until 2024

On 02/11/2020, deputies of the Jewish Autonomous Region submitted a bill to extend the validity of the UTII for another 3 years: until 01/01/2024. The deputies explain the need for an extension by the fact that the abolition of the imputation will entail the loss of a significant part of the income from the budgets of municipalities. As an example, officials cite the income of one of the municipalities, in which the share of UTII deductions is 96.77%.

Now this bill is going through the stage of preliminary consideration and it is impossible to say unequivocally whether it will be approved. We will monitor events and post information on the website as soon as something becomes clearer