According to the law, a company cannot unilaterally waive its obligations and debts. But there is a chance to offset mutual obligations. For example, if an organization has debts to a counterparty, but at the same time the latter has outstanding obligations to this company. That is, there is a mutual “exchange” of obligations - as a result of which an act of offset is drawn up. But it cannot be compiled at random. Otherwise, the Federal Tax Service may have questions, and the matter will come to court proceedings.

Below we will tell you how to draw up an act of offset, when is it relevant and what does it lead to? You will also be able to document.

What is an act of offset?

First, let's look at the purpose.

An act of offset of mutual obligations is an official document between two counterparties about the write-off of debts or obligations towards each other.

The main goal is to avoid disputes. At the same time, other problems are being solved:

- Legal disposal of debts and obligations;

- Preservation of working capital;

- Reduction of financial transactions, including savings on fees for interbank transfers.

Both full and partial offset of mutual obligations between organizations or individuals are allowed.

Example:

Company A has a debt to company B in the amount of 10,000 rubles, but at the same time, receivables (from company B) are also 10,000 rubles. Both companies act as both a debtor and a debtor to each other, with the same amount of debt. If both parties agree, they can sign an act of offset, thereby writing off mutual debts.

If one of the companies has a debt of not 10,000, but, say, 7,000 rubles, only partial offset is possible. In this case, the Act also records the balance in the amount of 3,000 rubles - it will have to be returned separately within the allotted time frame.

Nuances of forming a tripartite netting act

Sometimes it becomes necessary to draw up an act of mutual settlement between three parties to cooperation, or even more.

Such a need arises if the parties provide each other with homogeneous interconnected services, then a document is drawn up that contains the following data:

- Information about documents that are evidence of the provision of mutual services by companies to each other;

- The amount of debt of each of the counterparties as of the date of document generation;

- The final amount, previously agreed upon, to be withdrawn from the receivables and payables of each participant. Here you will learn how to write off accounts receivable with an expired statute of limitations;

- The amount of remaining debt to the counterparties of each of the parties to the transaction.

Next, the act is certified and signed. Important: reconciliation reports must be attached to it, and all amounts in all documents existing for the offset must have a separate indication of VAT.

In what cases is it needed?

The specifics of terminating an obligation by offset are noted in Art. 410 of the Civil Code of the Russian Federation. To do this, three mandatory conditions must be met:

- Firstly, there must be counterclaims to each other - that is, under at least two different agreements. In one case, the organization acts as a debtor, and in the second, as a creditor (the second is similar).

- Secondly, the homogeneity of the requirements - otherwise the act of offset will not have legal force. That is, you cannot “exchange” monetary obligations for services or work. If you have a debt to your counterparty of 3,000 rubles, then your opponent must also have a financial debt to you.

- Thirdly, the deadline for execution has already arrived, the time of demand has not been specified or the moments of demand have been determined.

The execution of the document guarantees the legal conduct of business transactions between two companies or individuals. If the Federal Tax Service or another body wants to challenge the transaction, the Act will act as evidence in favor of the participants in the netting of obligations.

What does it mean to offset counterclaims of the same type and why is it important?

One of the conditions for drawing up an act on mutual offset of claims is the homogeneity of obligations, which are offset both in subject and in essence (Article 410 of the Civil Code of the Russian Federation). That is, this is the offset of only monetary (property) debts or the provision of services, performance of work, etc. If the requirements are heterogeneous, the document will not have legal force.

In the text of the act, in addition to indicating the amount of the obligation, it is necessary to clarify which part of it is counted. If obligations are not subject to mutual offset in full, it is necessary to indicate the fate of the remaining part of the debt.

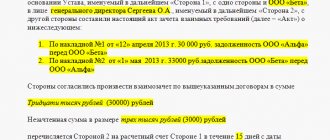

For example, the wording may be as follows: “The parties agreed to offset the above agreements in the amount of 7,500 rubles. The remaining debt in the amount of 12,000 rubles. Vasilek LLC undertakes to transfer to the current account of Doors to the World LLC no later than 02/12/2019.

The amount of sanctions in the event of failure to fulfill the terms of the agreement by one of the parties does not need to be indicated in the act, since in fact the parties have already entered into a transaction in pursuance of which the act is drawn up, and, accordingly, all fines are specified in its terms.

***

As you can see, this act is drawn up quite simply. The sample act on the offset of mutual claims offered for download from the link above will help to correctly complete the offset for both citizens and organizations.

***

You will also be interested in reading the materials that we wrote specifically for our Zen channel.

When is it not suitable?

The act cannot always be drawn up. The most obvious situation is when one of the parties does not agree to the offset. In this case, coercion does not work.

Other situations where offsets are prohibited by law are noted in Art. 411 of the Civil Code of the Russian Federation - this includes:

- Alimony debts;

- Heterogeneity of obligations (for example, debt for services in exchange for credit offset or the use of different currencies);

- Expiration of deadlines for execution - the issue will be resolved in court;

- Debt for compensation for damage to health;

- Insolvency (bankruptcy) of one or both counterparties;

- Other situations that violate the law.

There is no point in even trying to conclude an act of mutual offset of obligations - it will not have legal force, and the parties may run into fines.

Procedure for drawing up the document

The act is drawn up in writing. The title indicates the correct name of the paper: “Act of Settlement of Mutual Claims.” If necessary, indicate the number. The document must be drawn up in a quantity equal to the number of signatories. At the same time, the legislator does not limit the number of participants in the transaction.

Next, the date and place of drawing up the paper are indicated. The preamble reflects information about the signatories - they can be both individuals and organizations. In this case, both of them can be represented by authorized representatives with the right to sign.

Next, it is necessary to reflect the nature of the obligations subject to offset. It is equally important to indicate the basis for their occurrence - details of contracts or other documents-bases (for example, administrative acts or court decisions), the amount of obligations (in numbers and in words), if we are talking about money, or data on other types of claims.

It then states how much of each liability is offset and determines the remaining debt, if any. In addition, it is recommended to specify the date of entry into force of the document. If it is not prescribed, the act begins to be valid from the moment of signing. The preparation is completed by affixing the signatures and seals (if any) of the parties.

For reference: it is recommended to attach copies of the documents that form the basis for the emergence of obligations to the act.

In some cases, the parties to the transaction, before drawing up an act of offset of claims, form a reconciliation act. Moreover, it is important to understand that these are two different documents that should not replace each other.

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

A sample act of offsetting mutual claims of legal entities can be downloaded from the link at the beginning of the article.

It will also be useful to those who are interested in a sample act of offsetting counter homogeneous claims for individuals, since it is drawn up in a similar way. Its only difference from the first is the indication in the document that the parties to the transaction are citizens.

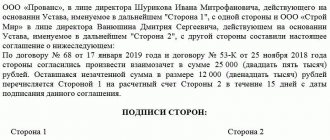

How to correctly draw up an act of mutual settlement between organizations?

The legislation does not approve a unified form. But there are requirements for primary documents, which are described in detail in Art. 9 Federal Law No. 402 “On Accounting”.

What sections does the contents of the Settlement Certificate consist of:

- Introductory part

The “cap” reflects the name – “Act of Settlement of Mutual Claims”. Below indicate the city and date of the document.

Next comes information about the parties: the first and second companies. In both cases, you need to specify the organizational and legal form (LLC, JSC, individual entrepreneur, etc.), then the full name and position of the authorized employee, as well as the basis document (for example, Charter, power of attorney). It's enough.

- Main part

Here you need to indicate on the basis of which agreements the mutual obligations of the parties arose. For example, a contract or service agreement. Be sure to enter the number and date of conclusion of such agreements. The amounts owed are indicated below: first in numbers and then in words.

Next, the parties inform about their agreement to offset, indicating the form - full or partial. If the second option, then it is necessary to record the remaining debt and the timing of its transfer to the counterparty’s current account.

- Final part

The document is signed by both authorized persons, indicating their full name, position and personal signature. There is no need to put a stamp; starting from 2021, this is an optional attribute when approving documents. But keep in mind that the Federal Tax Service may require the seal of a legal entity.

Carrying out mutual settlements between organizations

To better understand this issue, a simple example should be given. One bought office chairs from another for about 10 thousand rubles. To repay part of the debt for this amount, organization “A” provides its lawn mowing services to a completely different organization, but two and “B” have the same owner.

In this example, you should draw up an agreement for a third party in the 1C 8.3 Accounting program. The value of the attribute “At the expense of debt” will be “A third party to our organization.” After this, you should immediately indicate two counterparties who are participating in this agreement. This will be the supplier and the third legal entity.

Now you need to fill in the fields in the program. The field, which is a requisite for “Supplier (lender)”, must be filled in with the name of the creditor company. This is the organization with which the offset is carried out. This also needs to be done with the “Third party (debtor)” attribute.

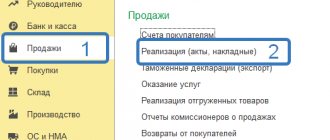

The next step is to manually or automatically fill in the data in a special table. Tabs will appear that will display information on accounts payable and receivable. Automatic filling is performed using the “Fill” button, where you need to select a single menu item. Now each tab will be filled out separately from each other. It is worth noting that they have the same interfaces.

Settlement between contracts has a similar procedure. The only difference is the presence of two counterparties at once, for which you need to fill in the required fields. After all the manipulations performed, you will be able to create a “Debt Adjustment” document. It can also be used to write off bad debts, credit advances, transfer debt and much more.

Other nuances

The act of offset of mutual obligations is drawn up in at least 2 copies. If other interested parties are involved in the transaction, copies are prepared for them as well. Each copy must be endorsed with the signatures of both parties.

The law classifies the act of offset as primary accounting documentation. Its shelf life is at least 5 years (Article 29 of Federal Law No. 402). For the Federal Tax Service, the shelf life is 3 years. This is necessary so that subsequently there are no misunderstandings regarding the accounting and tax accounting of the company.

An alternative to a bilateral act is to offset mutual obligations unilaterally. To do this, the accountant of one of the companies sends a statement of offset to the counterparty. In order to have proof of sending, it is better to use mail (registered or valuable mail). If the other party has no objections, the mutual offset of obligations will take place from the date specified in the application. And if there is no date, then from the date on which the application was received.

Peculiarities of execution of a unilateral act of offset

According to Russian legislation, it is not prohibited to offset mutual obligations at the request of one party. Thus, mutual obligations can be repaid unilaterally.

To do this, you must first notify your partners about this in writing. To do this, the initiator must send a registered letter to the other party with a notice inside.

This is done in order to subsequently have documentary evidence in the form of a notification of receipt as evidence.

It will definitely come in handy in the event of controversial situations and litigation.

The act of mutual settlements is a simple document and significantly facilitates the work of employees and interaction between organizations. It has many benefits and is designed to make life easier for businesses in general. It is easy to put together and has little nuance.

Dear readers! Our articles talk about typical ways to resolve legal issues, but each case is unique.

If you want to find out how to solve your particular problem, call

8 Moscow and Mos. region

8 St. Petersburg and Len. region

8 Regions of Russia

It's fast and free!

When it is possible and when it is impossible to offset

Settlement is an example of a civil transaction and is therefore regulated by the Russian Civil Code. Despite the fact that the legislation does not define a single sample of documents (acts, statements and agreements for offsets), the Code directly defines cases when offset is permitted and when it is not allowed. You can read more details in articles 410 and 411.

In accordance with the law, companies can offset liabilities:

- if the performance deadline has arrived, a specific one is not specified in the contract or is intended to be demanded (in rare cases that do not contradict the legislative norms of the Russian Federation, offset is possible for those obligations that have not yet occurred);

- if organizations are both creditors and debtors to each other;

- if the obligations are homogeneous (counterparties owe each other money in a single currency, in some cases, if there is a difference in currencies, offset is possible by agreeing on a transfer at the current exchange rate).

To count the requirements, a statement on one side is sufficient. However, it is best to have a mutual agreement.

Article 411 specifies cases when offset is prohibited:

- on claims for collection of alimony payments, compensation for damage to health and life, lifelong maintenance;

- on claims with an expired statute of limitations;

- in other cases provided by law.

Thus, offset is prohibited if the agreement prohibits it; in cases where one of the parties goes through bankruptcy; in cases of conducting foreign economic activity with a foreign organization and others.

Settlement cannot be carried out if the parties’ requirements for each other are not homogeneous. It is impossible to count when one organization must supply material resources (for example, construction), and the second must supply funds.

The article is over, do you have any questions? Contact the site's duty lawyer.

Don't forget to download sample acts for free.