Offsetting is the repayment of debt obligations in which there is no movement of funds. This operation is possible if the companies have obligations to each other with the same amount.

For example, you have a debt to the Beta organization in the amount of 100,000 rubles. But we also have obligations to Alpha in a similar amount. When offset, there is, in fact, annulment of mutual claims. There is no movement of money during the process. This operation involves the use of appropriate transactions.

Question: Does an organization need to use cash register systems when offsetting mutual claims with an individual purchasing goods (work, services) from it? View answer

Terms of netting

Settlement is not, according to the law, a transaction. Its implementation requires compliance with the following conditions:

- Enterprises initiated at least two transactions, which resulted in their debts to each other.

- Obligations are counter-obligations. That is, each participant in the netting is both a debtor and a creditor.

- The requirements are similar. That is, the amount of one debt is equal to the amount of another debt. However, debts are often not completely homogeneous. In this case, offset occurs for the amount of the smallest debt. The balance of the larger debt can be paid in cash. The amount payable is calculated on the basis of the Settlement Reconciliation Report.

How to offset counterclaims based on a unilateral notification?

IMPORTANT! If the debt to the company is paid by providing goods for a similar amount, such a transaction will not be offset. This is barter, which involves a different accounting procedure.

ATTENTION! Settlement does not apply to compensation for damage or payment of alimony.

Let's consider the basic rules of offset:

- Using the method under consideration, it is possible to repay debts with different repayment periods: due, not due, indefinite. If the debt payment deadline has passed, it is required to cover it within a week after submitting the claim.

- Typically there are two parties involved in the transaction. However, three or more companies can take part in the offset. In this case, there are circular requirements.

Accounting is carried out depending on the nuances of a specific mutual settlement.

How to arrange a settlement ?

What are the transactions for tripartite netting?

The Federal Tax Service has edited the control ratios of VAT declaration indicators. This is due to the entry into force of the order amending the VAT reporting form. In the case when a “physicist”, not registered as an individual entrepreneur, purchases goods using a foreign Internet service (for example, eBay), the duties of a tax agent for VAT are not assigned to him.

On the eve of the next deadline for paying insurance premiums, tax officials decided to draw the attention of payers to the most common mistakes made when filling out payment orders for transferring contributions to the budget.

For the first time, a new unified calculation of contributions must be submitted to the Federal Tax Service no later than May 2.

Settlement of mutual claims: when and how to carry out

In practice, situations often arise when the same counterparty acts as a debtor and as a creditor at the same time.

For example, organization “A” supplies organization “B” with drinking water for the office, and at the same time purchases advertising services from organization “B”.

There can be a lot of similar examples, the main thing that unites them is the presence of mutual debt, which the parties have the right to pay off by offsetting mutual claims.

How to set off in 1c

If one counterparty is both a supplier and a buyer in relation to the enterprise, then the debt of this organization can be offset; let’s look at how to carry out offset in 1C.

https://www.youtube.com/watch?v=qjGcFZ2o7Qk

I talked about how this can be done in the 1C Accounting 8, edition 2.0 program in this article. Today we will look at netting in 1C Accounting 2, edition 3.0. To carry out offsets, use the “Debt Adjustment” document, which is located on the “Purchases and Sales” tab in the “Settlements with counterparties” section.

My debriefing did not reach the point of losses.

I was tormented by vague doubts all day and all evening. Somehow collecting them in a heap, the next morning I tried to dump them in front of the Chief Accountant.

The main question of our time at this stage of mastering accounting for me sounded like this: if Debit and Credit show that money went from one place and immediately to another, then is it possible to put any accounts in Debit and Credit? The Chief Accountant looked at this wiring: such wiring takes place in life.

Like in 1C 8

A situation often arises when it is necessary to adjust mutual settlements with counterparties.

The data from the supplier or buyer may not match the data from our organization, and vice versa. This may occur as a result of:

- when incorrect information was transmitted to the accounting department;

- changing data as agreed by the parties;

- writing off bad debts;

- errors in accounting;

- you need to transfer the debt to another person and so on.

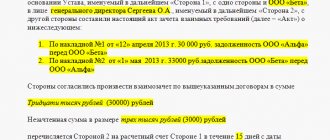

The provider issued certificates in the amount of 4,460.40 rubles.

Settlement: how to carry out and process it correctly

Settlement is a convenient and quick way to repay a debt to a counterparty.

To eliminate tax risks, it is important to correctly draw up the netting act.

You will learn how to complete such an operation from this article. An organization can enter into two different agreements with its counterparty. Under one of the agreements, she can act as a seller, and under the other, as a buyer.

Debts that arise can be repaid in a convenient way - offset.

Settlement: when no one owes

Norms Art. 410 of the Civil Code of the Russian Federation contains general provisions on the offset of mutual claims, which means one of the ways to pay off an obligation.

In other words, an obligation is considered fulfilled at the request of one of the parties or by mutual agreement if it is covered by a counter similar obligation. Offsetting can be carried out between any participants in civil relations - legal entities, individual entrepreneurs, individuals - in various variants of their relationship in the transaction.

If an organization has a debt to a counterparty-supplier, it can provide services to the counterparty or supply goods in exchange for the debt. Likewise, the buyer counterparty can supply services or goods against its debt.

To correctly display such transactions in accounting, it is necessary to carry out the netting procedure. Example. Our organization owes the supplier 88,500 rubles.

Settlement of counterclaims of the same type

Offsetting counter homogeneous claims (offsetting) is a fairly convenient way to “close” settlements with a counterparty. We hope that the information presented below will allow the reader to more confidently apply this method of terminating obligations in their business activities.

According to Part 1 of Art. 601 Civil Code,

“the obligation is terminated by offsetting counterclaims of the same type, the deadline for fulfillment of which has arrived, as well as claims for which the deadline for fulfillment has not been established or is determined by the moment of presentation of the demand”

.

Source: https://vigor24.ru/kakie-provodki-pri-trehstoronnij-vzaimozachet-48275/

Forms of offset

The following forms of mutual settlement can be distinguished:

- One-sided . The initiating party draws up an application indicating the proposal for mutual offset. The document is sent to the company's creditor. The application is drawn up in free form, but it must contain a list of mandatory information: details of the organization, name of the application, date of execution, operation as a result of which the debt arose. The date of offset can be considered the day on which the application was received by the creditor.

- Double-sided . A bilateral agreement on the offset is drawn up. Representatives of both companies put up their murals. The document is also drawn up in free form, it indicates details and information about the parties to the offset. The bilateral form is considered preferable, since the document concluded between the companies is a reliable confirmation of the consent of the parties to carry out the transaction. In the future, the creditor will not be able to challenge the fact of his consent.

The procedure is carried out on the basis of an Act of Settlement of Mutual Claims. The law does not stipulate the form of this document, and therefore it can be developed by the enterprise itself.

When netting between legal entities is impossible

Offsetting mutual claims for the following obligations is not permitted:

- for which the statute of limitations has already expired;

- which are related to compensation for damage caused to health or life;

- related to the collection of alimony;

- which are associated with the lifelong maintenance of individuals.

It is also impossible to carry out offsets if this is directly provided for by law. Also, the legislation does not allow offset if one of the parties is in bankruptcy proceedings (411 of the Civil Code of the Russian Federation).

Accounting entries

In accounting, the transaction performed is recorded after the Certificate is issued. In this case, postings to accounts 60, 62 and 76 are used.

Example

entered into a contract with the organization “Health” for 25,600 rubles. VAT amounted to 3,905 rubles. The costs of carrying out contract work are 14 thousand rubles. The Health organization previously entered into an agreement for the supply of goods in the amount of 11,800 rubles with Vita. The tax amounted to 1,800 rubles. The cost of goods is 6,500 rubles. The organizations decided to offset each other.

Postings performed:

- DT 60 CT 62. Explanation: fixation of mutual obligations. Amount: 11,800 rubles. The document on the basis of which accounting is kept: accounting certificate.

- DT 60 CT 51. Explanation: transfer of the amount for the remaining obligations. Amount: 13,800 rubles. Primary documentation: payment order.

- DT 68 CT 19. Explanation: tax deductible. Amount: 3,905 rubles. Primary documentation: book of acquisitions.

Postings performed:

- DT 60 CT 62. Explanation: fixation of mutual obligations. Amount: 11,800 rubles. Primary documentation: accounting.

- DT 68 CT 19. Explanation: tax deductible. Amount: 1,800 rubles. Primary documentation: book of acquisitions.

- DT 51 CT 62. Explanation: fixation of the amount of funds paid under the contract. Amount: 13,800 rubles. Primary documentation: extract from a banking institution.

Any transaction in accounting must be confirmed by a primary document. Otherwise, the reflected actions will raise questions from the tax authorities.

Accounting entries for offsetting mutual claims of the triple agreement

The World of Books organization donated products worth 120 thousand rubles. The tax amounted to 18,305 rubles. entered into a contract with the organization “Angelina” for the amount of 90 thousand rubles. VAT amounted to 13,729.

All companies almost simultaneously acquired debt obligations. The parties made a decision on mutual settlement. For this purpose, an appropriate agreement was drawn up. Repayment is carried out according to the amount of the smallest debt, which is 90,000 (VAT is 13,729).

). KT 62 (subaccount: settlements with).

Netting between three organizations in 2021: postings, sample

Offsetting is the repayment of counterclaims without additional cash flow. As a result of offset, the homogeneous claims of the parties to each other are canceled. Let's look at an example of how to carry out netting between organizations and the transactions generated for this operation.

Rules for netting Mutual netting is not considered a transaction.

Accounting entries for netting between organizations

Reflected revenue from the sale of goods to the buyer-organization B 62/B 90 “Sales” 250,000 Accepted work performed by organization B 20 “Main production”, 26 “General expenses”, 44 “Sales expenses”, etc. 60/B 180,000 A organization B will reflect the transactions in its accounting as follows: Operation Account debit Account credit Amount, rub.

Goods received from organization A 41 “Goods” 60/A 250,000 Work was completed for organization A 62/A 90 180,000 Thus, the accounting records of both organizations will include simultaneously receivables and payables to the same company, therefore, By drawing up an act of offset, the debt for a smaller amount can be offset.

Postings when working on netting

Attention LLC "V" owes the enterprise LLC "S" for the supply of goods an amount equal to 25,000 rubles. LLC “S” has a debt obligation in the amount of 16,000 rubles to the organization LLC “D” for the goods supplied.

LLC "D" has a debt to LLC "A" in the amount of 10,000 rubles for the goods received.

On the date of the offset, the time for fulfilling all mutual obligations has come. The offset amount is equal to the minimum debt, that is, 10,000 rubles.

Table: accounting for the enterprise LLC “A” At the end of the accounting, LLC “A” will owe LLC “B” 2,000 rubles.

Offsetting: postings

On approval of the Chart of Accounts for accounting of financial and economic activities of organizations and Instructions for its application” Chart of Accounts Art. 153 of the Civil Code of the Russian Federation The concept of a transaction Art.

154 of the Civil Code of the Russian Federation Agreements and transactions Information letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated December 29.

2001 No. 65 “Review of the practice of resolving disputes related to the termination of obligations by offsetting counter-similar claims” Presence of a statement on the part of one of the legal entities Errors in offset between three organizations When carrying out offset, it is necessary to very carefully monitor all stages of the procedure in order to avoid errors that often occur : Errors Explanation Lack of statement According to Article 410 of the Civil Code of the Russian Federation, a statement from one of the parties proposing offset must be provided.

Offsets

Table: netting in the accounting of LLC “A” Table: netting in the balance sheet of LLC “B” Table: netting transactions in LLC “C” So, an incomplete offset was carried out, equal to the amount of 15,000 rubles, between , LLC “B”, LLC “ WITH".

Multilateral netting To multilateral netting, you can apply the rules and regulations that are also characteristic of trilateral netting.

Requirements for conditions and documents for the implementation of offsets Each accountant needs to study the legal sources regulating the possibility of multilateral offsets, as well as become familiar with the specifics of drawing up supporting documents.

Table: documents required to offset claims and obligations An example of multilateral offset with accounting entries is a debt obligation in the amount of 12,000 rubles for a product received from the organization V LLC.

Settlement between two, three or more organizations in 2018

Important After settlement:

- accounts payable to Hermes amounted to 10,000 rubles. (including VAT – 1525 rub.);

- Master's receivables amounted to 30,000 rubles. (including VAT - 4576 rubles).

The parties repaid the remaining debts to each other in cash: Debit 60 subaccount “Settlements with Torgovaya LLC” Credit 51–10,000 rubles.

https://www.youtube.com/watch?v=Ng4Ifp0Mgog

LLC "GDE" has a debt to LLC "ZhZI" in the amount of 560,000 rubles, LLC "ZhZI" has a debt to LLC "ABV" in the amount of 150,000 rubles.

The parties decided to enter into an agreement on mutual settlement between three organizations in order to partially repay obligations, namely for the amount of the smallest debt (150,000 rubles).

Thus, the offset looks like this: from LLC “ABV” to LLC “ZhZI”, from LLC “ZhZI” to LLC “GDE”, from LLC “GDE” to LLC “ABV”. As a result of the transaction, the remaining debt is as follows:

Accounting entries for netting between three organizations For correct accounting, it is necessary to very carefully monitor accounting entries to avoid errors. To be able to mutually settle the claims of the parties, several conditions must be met:

With the help of offsets, you can pay off claims that have both arrived and have not yet arrived, as well as claims with an indefinite period. Claims of the first type must be paid within 7 days from the date of their presentation.

The homogeneity of demands means that the situation of repaying a monetary obligation with goods is not an offset - such repayment is called barter.

GDE LLC) 430,000 D 60/GDE K 62/ZhZI Offsetting 150,000 GDE LLC reflects the following data in its accounting: Accounting entry Explanation Amount (rub.

) D 62/ABV K 90 Sale of goods ABC LLC 430,000 D 41 K 60/ZhZI Capitalization of goods received from the supplier (ZhZI LLC) 560,000 D 60/ZhZI K 62/ABV Offsetting 150,000 ZhZI LLC reflects the following data in its accounting records: Accounting entry Explanation Amount (rub.

) D 62/GDE K 90 Sale of goods LLC "GDE" 560,000 D 41 K 60/ABV Receipt of goods received from the supplier (LLC "ABV") 150,000 D 60/ABV K 62/GDE Offsetting 150,000 Thus, from The example shows that, based on a mutual agreement on netting, each of the three organizations in its accounting records reflects an accounting entry that makes it possible to track the complete or partial termination of the obligations of one legal entity to the other.

Source: https://2440453.ru/buhgalterskie-provodki-zacheta-vzaimnyh-trebovanij-trojstvennogo-soglasheniya/

Triple netting

The offset can be made between three or more organizations. However, such an operation does not comply with all the conditions of mutual offsets stipulated in Article 410 of the Civil Code of the Russian Federation. In any case, multilateral offset can be carried out in accordance with Article 421 of the Civil Code of the Russian Federation. It is carried out on the basis of a contract. A document is drawn up based on the general requirements for contracts. However, it should not contradict the specifics of a multilateral transaction, as specified in paragraph 4 of Article 420 of the Civil Code of the Russian Federation. Typically, companies draw up an agreement for mutual settlements. Its form is not established by law. When compiling, you must be guided by the general provisions for primary accounting documentation.

How to compose a paper

The netting agreement does not have a unified form, so representatives of enterprises and organizations can write it in any form or according to a model developed and approved within the company. The main thing is that the structure of this document complies with certain standards of office work; in addition, in terms of content, it must include some mandatory information.

This is important to know: Fragmentation of purchases under 44 Federal Laws: responsibility

These include:

- the name of the organizations between which the agreement is being formed, their details;

- place and date of drawing up the form.

In the main part of the document it is necessary to record:

- the fact of an agreement reached;

- reference to the agreements under which it is carried out.

If there are any additional conditions or documents that are attached to this agreement, they must be noted as a separate paragraph.