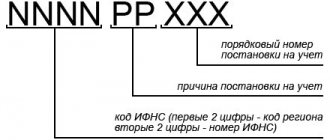

Features and differences

The main difference between reporting by an entrepreneur and a legal entity is the independent management of document flow by the business owner, and not by a separate accounting department. Therefore, an individual entrepreneur is given 5 calendar days, not working days, to issue an invoice.

The starting point is the day of receipt of property rights to the goods, the date of shipment, receipt of services, acceptance of work or receipt of an advance. In cases of prepayment, an invoice is drawn up twice, upon receipt of the advance payment and upon fulfillment of the terms of the transaction. You can find out how an advance invoice is prepared here.

Reference. Invoices are drawn up in the form approved by Decree of the Government of the Russian Federation No. 1137 of December 26, 2011. The main requirements for the document details are given in Article 169 of the Tax Code of the Russian Federation.

Article 169 of the Tax Code of the Russian Federation contains the basic requirements for indicating to an individual entrepreneur the features of a transaction in an invoice:

- Number, date of compilation and corrections.

- TIN and other data to identify the parties to the transaction.

- Address for delivery of goods or provision of services.

- Invoice or advance invoice number to confirm the amount.

- Names and units of measurement of transferred goods.

- The number of goods, works or services transferred in the specified unit of measurement.

- Settlement currency.

- Country of origin and customs declaration number for imported goods. Read about import and export invoices here.

- The cost of each specified unit.

- Total transaction amount.

- Tax rate and excise duty amount.

- Calculated tax amount.

Important! Reliable and correct indication of all the listed information in the invoice gives the individual entrepreneur the right to receive a tax deduction when transferring the purchase book to the tax service.

More information about what an invoice is and the features of using the document can be found here.

Invoice or universal transfer document for individual entrepreneurs, which is better?

Invoice

for an entrepreneur it is necessary when an individual entrepreneur applies the General Taxation System or is a tax agent for value added tax. When an entrepreneur uses an invoice in document flow, it is mandatory that an act of completion of work, a bill of lading, a consignment note, and a consignment note are formed as the primary document - these are documents that confirm the shipment of material assets and goods for sale. It is almost impossible to refuse these documents, due to the fact that the entrepreneur needs to document his expenses.

IP

a universal transfer document (UDD)

instead of an invoice . The use of UPD does not violate any legal norms. The use of a universal document is a recommendation, but the form proposed by law has many advantages.

Do you need a document?

Clause 4 of Article 169 and Clause 7 of Article 168 of the Tax Code of the Russian Federation indicate cases in which the individual entrepreneur seller is not required to draw up an invoice. For transactions between private entrepreneurs, in the areas of retail trade, provision of services and hired work, invoices are not required.

Also, there is no obligation to draw up such securities in case of cash payment and sale of securities, provided that the parties to the transaction are not intermediaries or brokers.

An individual entrepreneur should not issue invoices when making a transaction with an LLC, individual entrepreneur or a company operating under a special tax regime with simplified taxation.

Invoice without VAT and erroneous payment purpose

A situation may arise where a tax-exempt person using the special regime issues an invoice without tax, and the buyer mistakenly makes a payment and displays the rate and amount in the payment details.

Once the tax service notices the purpose of the payment during the audit process, clarification will be required. There is a risk of suspension of transactions on the account, write-off of arrears by mistake. To prevent such a situation from arising, it is necessary to carefully study all receipts.

If the accountant independently identifies an incorrect assignment of the contribution, the buyer will need to request a letter clarifying the details. In practice, the fiscal authorities, when identifying a deficiency after submitting a letter, do not require additional paperwork.

The peculiarity of an invoice for individual entrepreneurs without VAT is that it has a similar form and columns as a simple document that is used by persons on OSNO. There are differences only in filling out the seventh and eighth columns.

Should I issue a document if I work without VAT?

The obligation to issue an invoice under the conditions of the seller’s exemption from VAT, in accordance with paragraph 5 of Article 168, occurs in cases provided for in Article 145 of the Tax Code of the Russian Federation. We are talking about individual entrepreneurs with revenue of less than 2 million rubles per quarter, who do not work with excisable goods.

Such entrepreneurs, after notifying the Federal Tax Service, are exempt from VAT for 12 calendar months, unless conditions arise for the cancellation of such a right. The exemption is then reviewed and updated annually.

In other cases, the taxpayer has the right, but not the obligation, to draw up an invoice , and can use it solely for his own convenience.

An example of such a situation is the exemption from tax of part of the consignment indicated in the invoice together with goods subject to tax. Also, an optional invoice for tax-free goods will help maintain consistency in document numbering.

Read about when you need an invoice without VAT here.

Application of invoices for individual entrepreneurs

A popular question is whether an invoice is needed for an individual entrepreneur without VAT, and whether the seller should issue a form in this case. VAT payers (entrepreneurs and companies) cannot issue documents without tax, regardless of who their buyer is. It doesn't matter that the buyer is running a simplified system.

If a person is not a VAT payer, is it necessary to submit a form? When applying a special regime or exemption, invoices are issued at the request of the buyer or according to the requirements of the Tax Code. According to Article 168 of the Tax Code, a person who does not pay tax under Article 145 must issue invoices marked “Without VAT”.

Column 7 of this document displays the payment tax rate. If the form is completed by a person who is not paying the fee, there is no need to enter numbers in the box. This type of document is called zero, which means that the seller has no obligation to pay the fee; the buyer cannot claim compensation.

One of the features of such an account is that you should not indicate the number zero. If an entrepreneur writes this figure, tax authorities may take this as a zero-rated transaction, and then a declaration will be required. A fee may be required to be paid to the budget. To avoid problems, you should put “Without VAT”.

According to the rules, the buyer must register the invoice in the purchase ledger. Based on these records, a deduction is drawn up. If the form is zero, it is impossible to issue compensation. There is no indication in the law that invoices without VAT should not be registered. However, this document does not affect the amount of the deduction, therefore, it is possible not to reflect the invoice received from the individual entrepreneur on a simplified basis without VAT.

How to display?

In paragraph 6 of Article 169 of the Tax Code of the Russian Federation it is stated that when issuing an invoice, an individual entrepreneur must personally sign it and indicate his own details of state registration of himself as an individual entrepreneur. Details mean a certificate of state registration of an individual entrepreneur to identify the taxpayer. Unlike an LLC, an entrepreneur cannot delegate this responsibility to a trustee.

Note! Although the right to participate in relations of an authorized representative is confirmed by paragraph 1 of Article 26 of the Tax Code of the Russian Federation, it also states that it may be limited by other legislative acts.

Therefore, the legal representative can conduct the transaction, but cannot sign the invoice on behalf of the individual entrepreneur.

VAT payable

It is necessary to pay a fee on the sale of goods if the law does not apply to individual entrepreneurs. VAT will be added to the price of goods. To do this, the cost of the product is multiplied by the tax rate. When carrying out trade operations, a businessman transfers VAT. It includes the cost of the transaction. The buyer is given documents indicating the price including tax. The burden of paying the tax lies with the buyer. The individual entrepreneur is an intermediary between the consumer and the state treasury.

If a business entity is on OSNO and works with added tax, it performs the following actions:

- calculates sales tax;

- issues a VAT invoice;

- prepares a purchase/sales book;

- submits a declaration at the end of the quarter on electronic media;

- transfers money to the budget, dividing payments into three parts.

On video: Changes in invoices dated 10/01/2017

Providing an invoice entitles the businessman to a tax deduction, including all taxable transactions. By choosing a special tax regime, a businessman is exempt from paying tax. Except for a few cases when you have to pay it.

Situations when VAT is taken into account for deduction from individual entrepreneurs on the simplified tax system:

- Individual entrepreneurs buy goods and services from companies without a representative office in the Russian Federation.

- As an intermediary, he receives payment in cooperation with a foreign company.

- The issued invoice is indicated by the VAT amount.

- Pays for the rent or purchase of state property to the owner - the government authority.

- Acts as a trustee during transactions.

Filling rules

To send a VAT deduction to the buyer to the tax service, the supplier, along with the invoice, must issue an invoice (in which cases the invoice and invoice are needed, read here). In addition to the fact of having the document, you need to fill out the invoice correctly. The law has introduced the following procedure for compiling the title part of the form:

- Document number in the supplier's accounting and date of completion. 1a is intended for dating the corrective version and is left blank during the initial drafting.

- Full name of the entrepreneur. 2a IP registration address. 2b TIN of an individual.

- The name of the shipper may duplicate the data in line 2.

- Name and address of the buyer-receiver.

- Number and date of the payment receipt, in cases of prepayment.

- 6a, 6b – data about the buyer, identical in form to lines 2 and 3.

- Name and code of the settlement currency. The code can be found out from the classifier, for example, the ruble is numbered 643.

Next, the form contains a table where for each product from the invoice you must enter:

- Name;

- quantity;

- unit of measurement;

- price;

- amount and rate of VAT;

- final price.

The document is filled out in two copies and signed personally by the entrepreneur, if drawn up on behalf of an individual entrepreneur. The invoice is not stamped.

- You will learn more about correctly filling out an invoice in this article.

Option with VAT

When receiving invoices from contractors who are individual entrepreneurs, the buyer should especially carefully monitor their authenticity and especially the presence of the signature of the entrepreneur himself. The main difference from receiving a document from an LLC is the requirement for a personal visa.

Important! The absence of one of the key details, such as a personal signature or duplication of data in column 3, is grounds for refusal of a deduction during an inspection.

If an entrepreneur has issued an invoice, but the form contains an error, then it will be impossible to obtain a VAT deduction even through the court.

In case of tax exemption

Drawing up an invoice for goods “without VAT” is possible in 2 variations:

- If all the goods in the batch have such a mark, then in line 8 of the form with the total tax amount this mark is duplicated, and such a tax document is not considered.

- If some services or goods are exempt from tax, then column 8 indicates the actual amount excluding these data.

An invoice without VAT is filled out in accordance with the general rules for the preparation of this document, since Government Decree No. 1137 of December 26, 2011 was updated by Appendix 2 to the resolution, dated February 1, 2021. It is enough to enter the entry “excluding VAT” in the appropriate section of the table. The mark can be made separately, in a printed document by hand, for example, when signing a document.

Closing documents for individual entrepreneurs without VAT

When carrying out transactions, it is necessary to take into account the availability and correct completion of closing documents. In this case, it is necessary to submit receipts and payment papers, as well as statements.

In addition, papers are required in which each party confirms the completion of the transaction upon fulfillment of obligations under the contract. To ensure that counterparties do not have questions about the specifics of performing operations, all conditions must be described in detail in the contract. Individual entrepreneurs and companies operating without VAT or with tax must indicate what documents are required for the agreement to be fulfilled.

Confirmation of completion of the transaction must be in writing. Any enterprise requires strict accounting of transactions. When transferring funds for goods or services, you need a document of receipt. There are different types of contracts for different transactions.

The document that closes the contract for the supply of products or raw materials is the invoice. Only the original documentation has legal force. When selling products, the supplier must write an invoice in two copies. The following details are required - name and number, supplier data, information about the product and quantity, price, signatures of responsible persons are required.

If the subject of the contract is work, the main document for closing the contract will be the act. Only the original is required. The form confirms that the buyer has no comments. There is no unified form of the document, but a number of mandatory data must be entered: the name and number of the document, the date of execution, who the contractor and the customer are, what work was carried out and to what extent. The signatures of the responsible persons must be present.

The absence of these documents causes additional taxes to be assessed. To avoid negative consequences, all paperwork must be completed in a timely manner.

Actions after issue

When receiving an invoice from the entrepreneur's authorized representative, the buyer has a high chance of being denied a deduction from the tax service and will have to go to court. The judge will check the authenticity of the transaction and, most likely, will grant the request to annul the refusal on a formal basis, but this will take the buyer time and money.

To avoid legal costs and other unpleasant moments associated with the incorrectness of this document, the nuances of issuing an invoice should be specified in the supply agreement. In any case, the supplier is not responsible for issuing an invoice, unless otherwise specified in the contract.

Entrepreneur at OSN

It is necessary to take into account the important points of adding VAT to the deduction for individual entrepreneurs on OSNO. An entrepreneur is required by law to add tax at a rate of 10% (18%) unless tax incentives apply.

Individual entrepreneurs are exempt from paying the fee for the following reasons:

- income for the quarter amounted to less than 2 million rubles. Profit does not include added tax, funds for non-taxable transactions, prepayments;

- goods with excise taxes were not sold at this time.

According to Article 149 of the Tax Code of the Russian Federation, individual entrepreneurs are exempt from the need to add VAT according to the list of transactions.

On video: VAT deductions: complex and ambiguous issues, how to reflect them in accounting and draw up documents

Procedure for filling out an invoice without VAT

In 2021, there have been many changes in the regulatory framework of accounting and tax accounting that need to be applied.

Starting from January 1, 2021, individual entrepreneurs on OSN and special regimes are exempt from maintaining registers that duplicate the information reflected in the Book of Purchases and Sales. However, as before, all registration books are provided by those, regardless of the taxation system, who provide intermediary and audit services or are developers, and also enter into commission and agency agreements.

This obligation is specified in Article 174 of the Tax Code of the Russian Federation.

The journals are submitted to the supervising tax authority in the month following the reporting period (usually a quarter) no later than the 20th day. When concluding mediation agreements, “summary” invoices may be presented. All responsibilities are specified in Letter of the Ministry of Finance of the Russian Federation No. 03-07-14/2821 dated January 28, 2015 and Decree of the Government of the Russian Federation No. 1279 dated November 29, 2014.

Detailed filling procedure, which regulates the content of the following information:

- serial number and date of invoices;

- full name and tax identification number of the supplier and buyer;

- name and quantity of goods supplied or services provided;

- cost, in Russian rubles, for one unit and the entire batch;

- the tax rate in effect on the date of the transaction;

- the amount of tax to be transferred to the budget;

- information about the sender and recipient of the cargo;

- if the vacation was made on an advance payment, you must indicate the date and number of the payment document;

- unit of measurement of goods. Not specified when providing services.

Information in accordance with Article 169 of the Tax Code of the Russian Federation must be contained in electronic and paper format. When generating a paper invoice, it is necessary to generate 2 copies, one is received by the seller, the second is given to its customers.

Basic mistakes in preparing an invoice

All possible inaccuracies and errors in the document can be divided into two types: minor ones, which do not affect the amount of VAT deduction, and significant ones, in the presence of which the tax authorities will not accept the confirmation document.

Errors in which tax authorities will not accept an invoice:

- Incorrect information about the buyer or seller that does not allow the entity to be identified. Blots will not raise any questions. But if the TIN and name are indicated incorrectly, for example, there is an extra digit in the TIN, then such paper will not be accepted.

- Information that does not allow one to determine which products were sold or purchased. Tax authorities view errors of this type with particular doubt. Typos and abbreviations are acceptable. Documents that indicate another product will not be accepted. For example, an organization entered into an agreement for the supply of soccer balls, but indicated basketball balls in the invoice.

- It is impossible to determine the amount of production or prepayment. Mistakes are often made in indicating the currency in which payments are made between organizations or determining its code. Arithmetic errors in the general cost calculation are also unacceptable.

- Errors in determining the tax rate and amount. Such inaccuracies arise when the interest rate for a specific type of product is incorrectly indicated. For example, products subject to a zero rate are indicated on the invoice at a rate of 10%. Accordingly, the VAT amount will be calculated incorrectly in the document.

To correct errors, generate a new document - an adjustment invoice.

Sample of filling out an invoice from an individual entrepreneur with VAT

Let's see how to fill out an invoice from an individual entrepreneur with VAT using a sample.

Example

On September 13, 2021, individual entrepreneur Anatoly Viktorovich Kuznetsov, who uses OSNO, sold two machines to Moonlight LLC:

- screw-cutting lathe with PU (RUB 49,973, including VAT);

- tabletop drilling and milling machine (RUB 45,489 including VAT).

For a sample of filling out an invoice for individual entrepreneur A.V. Kuznetsov, see below:

This sample invoice for individual entrepreneurs in 2021 is drawn up on a form approved by Decree of the Government of the Russian Federation No. 1137 (as amended on 02/01/2018).

Continuation of the example

To receive an invoice from IP Kuznetsova A.V.

allowed the buyer of Moonlight LLC to receive a VAT deduction, the entrepreneur should pay special attention to those invoice details, errors in which are critical for the deduction. Tax authorities may deprive Moonlight LLC of a tax deduction if they are unable to reliably establish from the invoice the name of the product, its cost, rate and amount of VAT, and also cannot identify the seller and buyer

To avoid possible errors, the individual entrepreneur took the necessary information for the invoice from primary sources:

- buyer’s details - from the agreement with Moonlight LLC and copies of constituent and other documents submitted by it;

- the name of the supplied mechanisms is from the technical documentation for them.

In individual columns and lines of the invoice, the individual entrepreneur added dashes.

Whether this is considered an error will be discussed in the next section.

Account form

Fill invoice online

How to fill out an invoice form online? Try creating and filling out an invoice online right now. You will also be able to issue invoices for payment, print and send them by email, you will have your own database of invoices. You will be able to create Acts, TORG-12 Invoices, Invoices, UPD and print Sberbank Receipts.

What is an Account?

An invoice for payment is a document from the Seller to the Buyer, which contains payment details and a list of goods and (or) services. Invoices for payment are usually sent to the Client by email.

- The following details are required in the Invoice:

- name of the organization or individual entrepreneur;

- TIN (and checkpoint for legal entities);

- bank details, current or personal account, cor. account, name of the bank and its BIC;

- listed goods (and services);

- total payment amount and VAT rate.

Invoice form 2018

There is no unified form of the Invoice; the company can independently develop its own form of the Invoice. Below you can see a sample and Invoices for payment 2021 for free.

How to fill out an invoice for payment

Recommendations for filling out an invoice for payment. The Invoice form below is the most preferable for use, as it may contain the full details of the Seller and Buyer. The invoice header contains a logo and the list of goods and services contains an additional column with VAT. The following fields must be completed in this invoice form.

- The logo is located in the header, the name of the organization, OGRN, INN, KPP, as well as the address of the organization with an index are filled in. Additionally, telephone and fax are indicated.

- The full name of the organization is indicated under the heading.

- Then the details of the Seller and Buyer are indicated. The seller's details must contain the name of the organization, address, INN, KPP, OGRN, current or personal account, bank name, BIC and correspondent account. Additionally, you can specify telephone, fax, e-mail and company website.

- The Buyer's details can be filled in completely by analogy with the Seller's details.

- The account number is indicated in accordance with the accounting policies of the organization. This can be a simple serial number (from the beginning of the year) or a special composite accounting number. The date of the invoice is indicated.

- Under the invoice number and date on the right, a short general name of the goods or services in the invoice is indicated. For example, “computer components”, “laptop”, “repair of office equipment”, “production of printed products”.

- The table lists goods and services, cost, quantity, unit of measurement, VAT.

- After the goods, you can indicate important features of the invoice, for example, “delivery time of the goods”, “due date for payment of the invoice”, etc.

- At the end of the account, you must indicate the head of the organization and the chief accountant. A signature and seal are not required, but many companies require that the invoice be signed and stamped.

Recommendations for filling out an invoice for payment (1C). The following invoice form is simplified and is used by default in many accounting programs.

- At the beginning of the invoice, a table resembling a payment order is filled out. It indicates the payment details of the Seller (payment recipient). This is the name of the organization, INN, KPP, current or personal account, name of the bank, BIC and correspondent account.

- Next, indicate the account number, which corresponds to the accounting policy of the organization. This can be a serial account number (since the beginning of the year) or a special composite number. The date of the invoice is indicated.

- The Seller's details must be provided in full. Name of the organization, INN, KPP, OGRN, address, current or personal account, bank name, BIC and correspondent account. You can also indicate telephone, fax, e-mail and company website.

- The Buyer's details are indicated in full or abbreviated form. It is enough to indicate only the name of the organization.

- The table lists goods and services, cost, quantity, unit of measurement.

- After the list of goods and services, you can specify the details of the invoice, for example, “payment period for goods”, “conditions of delivery or pickup”, etc.

- At the end of the invoice the full name of the head of the organization and the chief accountant are indicated. A signature and seal are not required, but some companies will not consider invoices without a signature and seal.

- If you need to constantly create invoices for payment, then use our Create an invoice service. Here you can create, print and send an invoice by e-mail.

- Additionally, using our service you can easily create a Certificate, Invoice, TORG-12, UPD.

- Try it now - Demo login (no registration). Don't forget to use the instructions on how to quickly create and fill out an invoice.

Invoice for VAT payers

Legal entities and other VAT payers use an invoice: a responsible financial document that is issued not in advance, but upon completion of work, services provided or goods shipped. It is no longer needed to speed up payment, but to confirm that excise duties and VAT have been paid in full, so that VAT can be withheld from the payer (buyer). This document has a prescribed form; it may also contain information about the origin of the goods, and if it is imported, then the number of the customs declaration for it.

The invoice is issued in two copies.

Tags: accountant, currency, tax, entrepreneur, order, problems, expense