What is an act of offset

An act of offset is a document confirming the fact of settlement of mutual debt of similar claims, that is, in case of financial debt, an offset of funds is necessary.

It is drawn up upon the application of one of the parties to conduct mutual reconciliation and reduce the number of requirements for each other.

When drawing up a document, it is not important what kind of debt the counterparties have - the main thing is that it is of a homogeneous nature.

You can see how to carry out offsets and how to complete such a transaction here:

By whom and when is the document drawn up?

A document is drawn up at the request of one of the counterparties, and in the event of unequal debt, one company’s debt can be fully repaid, while another’s can only partially repay it.

Such a document must have the signature of the head of the company, and a seal is not required from 2021.

What is offset and when is it acceptable?

Offsetting is a complex and complex operation, but it is permissible because it is reflected in accounting like financial transactions, like mutual settlement for the provision of services. How to draw up a statement of reconciliation of mutual settlements - read the step-by-step instructions at the link.

Offsetting has a number of features, one of them is the acceptance of many departments in carrying out the operation and drawing up the act:

- Accounting;

- Financial;

- Supply and household;

- Legal.

Important: only with close cooperation of all these services is it possible to create a legally competent document.

In this case, the entities must be parties to several obligations for which homogeneous claims arise, that is, there are different agreements concluded by counterparties, but it is possible to use offset for one obligation, for example, in case of failure to fulfill obligations, a claim for compensation for losses arises as a counterclaim there may be a payment of remuneration here.

The key features of the occurrence of mutual offset are the following: the presence of debt to the organization, while being its creditor, who can receive claims for payment of the debt and make them counter; usually such claims arise regarding the payment of funds. Here you will find out the procedure for filing a claim for payment of debt under a supply agreement.

At the same time, if a deadline has been established for demanding the fulfillment of obligations to the counterparty, at the onset of this day it is possible to submit counter-claims of the same type, if any.

Sample of filling out the netting act. Photo: towhite.win

When offset is not allowed

According to the law, there are debts, the fulfillment of which is strict; in this case, the use of mutual offset is unacceptable.

The list of such debts includes:

- Expiration of the statute of limitations or the presence of one of the counterparties in the lists of bankrupts. What is the statute of limitations for taxes for individuals - read the publication at the link;

- Collection of alimony or payment of compensation to the victim;

- Investment in the authorized capital of a deposit by one of the shareholders;

- When set-off is intended for heterogeneous claims;

- When conducting offsets for transactions performed in different currencies;

- In other cases when the operation is contrary to the law.

Offsetting: postings

A triple netting agreement is an example of a joint settlement by counterparties of debts arising under supply or service contracts in the event of a shortage of financial resources.

The conclusion of such an agreement is recognized as a transaction in accordance with the provisions of Art. 153 Civil Code of the Russian Federation, Art. 154 allows the implementation of agreements between several participants by concluding a multilateral treaty.

The basis for offset of funds is the existence of debts to each other by three organizations that agree to offset.

Regardless of the number of parties to the contractual relationship, the document indicates a full set of mandatory details approved by the legislator for primary documentation. The tripartite netting agreement must include information about:

- names of the enterprises participating in the transaction;

- personal data of representatives of organizations that have the authority to conclude transactions and approve contracts with their signatures;

- the grounds for the emergence of powers among representatives of legal entities;

- tripartite settlement of mutual claims (sample document) requires listing the obligations of each party in relation to the counterparties participating in the transaction;

- if there are financial obligations and a desire to offset them, it is necessary to register the details of the documents on the basis of which the debt arose in the accounting;

- an agreement on the offset of mutual claims, a tripartite sample agreement must limit the period for repayment of debts - the document specifies the deadline for the implementation of debt write-off;

- the amounts of the claim that can be repaid by offset are given;

- At the end of the document form, registration information about each participant in the transaction is written down and the signatures of the responsible persons are affixed.

A tripartite netting agreement must be based on reconciliation acts between all parties. This is necessary to prevent controversial situations and subsequent legal proceedings regarding the part of the debt remaining after the offset procedure.

Mutual repayment of debts between counterparties without the use of non-cash and cash payments is possible subject to a number of conditions:

- the debt of all parties to the transaction can be characterized as homogeneous;

- all companies agree to set off;

- This procedure is not systematic.

Tripartite netting is possible in the following situations:

- Transaction participant “1” did not pay, a possible reason is a violation of payment terms for products that previously entered into an agreement with transaction participant “1”.

- has a receivable to enterprise “3”, the balance sheet shows the outstanding amount of payment from organization “1”.

- acts as a debtor for legal entity “1”, while simultaneously performing the role of a creditor for institution “2”.

Triple offset, subject to partial debt write-off, can be used for the following case:

- LLC "Class" owed LLC "Svoe" 50,000 rubles for goods supplied;

- Svoe LLC has an outstanding invoice from Mel LLC in the amount of 43,000 rubles;

- Mel LLC did not pay Class LLC the amount of 77,000 rubles on the agreed dates.

Triple offset for these companies is possible in the amount of the smallest debt - 43,000 rubles.

As a result, LLC “Class”, after concluding the transaction, will have to repay LLC “Svoe” a debt in the amount of 7,000 rubles (50,000-43,000), LLC “Mel” undertakes to repay the debt to LLC “Class” in the amount of 34,000 rubles (77,000- 43,000).

The obligations of Svoe LLC to Mel LLC after signing the agreement and recording it in accounting will be considered repaid in full.

The desire to repay existing debts without transferring funds to the counterparty can be realized if this counterparty has counter-obligations.

In such situations, acts or multilateral mutual offset agreements are used.

On this page:

- Terms of netting

- Forms of offset

- Accounting entries

- Triple netting

Offsetting is the repayment of debt obligations in which there is no movement of funds. This operation is possible if the companies have obligations to each other with the same amount. For example, you have a debt to the Beta organization in the amount of 100,000 rubles.

But we also have obligations to Alpha in a similar amount. When offset, there is, in fact, annulment of mutual claims. There is no movement of money during the process. This operation involves the use of appropriate transactions.

Conditions for the implementation of offset Offset is not, according to the law, a transaction.

However, even being only, for example, a buyer, an organization may have accounts payable and receivable under the same invoice or invoice.

For example, organization A received an advance on the current account from organization B for the supply of goods: Debit of account 51 “Settlement accounts” - Credit of account 62/B, subaccount “Advances received” Subsequently, a shipment was made against the received advance: Debit of account 62/ B, subaccount “Debt for goods supplied (work, services)” - Account credit 90 Under automation conditions, the accounting program will offset debts independently.

The cost of the repairs performed is 15,340 rubles. (VAT – 2340 rub.). And the cost of work is estimated at 11,000 rubles.

Under the supply agreement, I shipped construction material in the amount of 8,260 rubles. (VAT – 1260 rub.). The cost of the shipped material is estimated at 5,600 rubles.

By mutual agreement of the parties, counter debt claims under the above agreements are offset.

The World of Books organization donated products worth 120 thousand rubles. The tax amounted to 18,305 rubles. entered into a contract with the organization “Angelina” for the amount of 90 thousand rubles. VAT amounted to 13,729.

All companies almost simultaneously acquired debt obligations. The parties made a decision on mutual settlement. For this purpose, an appropriate agreement was drawn up. Repayment is carried out according to the amount of the smallest debt, which is 90,000 (VAT is 13,729).

). KT 62 (subaccount: settlements with).

Bilateral offset In this case, the signing of a bilateral agreement on offset is provided: just like the application for offset, it is filled out in free form indicating the required details.

Settlement through a bilateral agreement is more preferable, since in this case the fact of agreement with the counterparty cannot be disputed. The basis for offset is the document Certificate of Settlement of Mutual Claims.

Example of an act: There is no approved form of an act of offset of mutual claims; each organization can develop its own form that is convenient for it.

Postings for offset between organizations After drawing up the Act on offset of counterclaims, the fact of offset is reflected in accounting by posting to accounts 60, 62 or 76.

Debit 19 Credit 60 subaccount “Settlements with OJSC “Proizvodstvennaya” - 13,729 rubles. – reflected “input” VAT on work performed; Debit 68 subaccount “Calculations for VAT” Credit 19–13,729 rub. – accepted for deduction of “input” VAT on work performed.

February 1: Debit 60 subaccount “Settlements with JSC “Proizvodstvennaya” Credit 62 subaccount “Settlements with JSC “Alfa”” - 90,000 rubles. – reflects the repayment of receivables and payables on the basis of an agreement on mutual settlements.

We suggest you familiarize yourself with How to clear customs a car from Japan

Debit 51 Credit 62 “Settlements with CJSC Alfa” – 10,000 rubles. – payment has been received for shipped goods.

Goods received from organization A 41 “Goods” 60/A 250,000 Work was completed for organization A 62/A 90 180,000 Thus, the accounting records of both organizations will include simultaneously receivables and payables to the same company, therefore, By drawing up an act of offset, the debt for a smaller amount can be offset.

Then, in the accounting records of organization A, the offset will be reflected as follows: Debit of account 60/B – Credit of account 62/B in the amount of 180,000. And organization A will make the following accounting entries for offset: Debit of account 60/A – Credit of account 62/A in the amount of 180 000 More than two parties can participate in mutual settlement.

Offsetting advances Often in accounting, offsetting refers to the closing of debts that have arisen on the same basis.

In the above cases, the same organization is both the supplier and the buyer.

To simplify, analytical accounting, for example, on account 62 will be reflected as 62/B, which will mean the debt of the buyer, organization B.

Let's present the accounting records for reflecting the debts incurred by organization A: Operation Account debit Account credit Amount, rub.

60/B 180,000 A organization B will reflect the transactions in its accounting as follows: Operation Debit account Credit account Amount, rub. Its implementation requires compliance with the following conditions:

- Enterprises initiated at least two transactions, which resulted in their debts to each other.

- Obligations are counter-obligations. That is, each participant in the netting is both a debtor and a creditor.

- The requirements are similar. That is, the amount of one debt is equal to the amount of another debt. However, debts are often not completely homogeneous. In this case, offset occurs for the amount of the smallest debt. The balance of the larger debt can be paid in cash. The amount payable is calculated on the basis of the Settlement Reconciliation Report.

- DT 60 (subaccount: Settlements with the organization “Books for Children”). KT 62 (subaccount: settlements with).

- DT 68 CT 19. Explanation: tax deductible. Amount: 3,905 rubles. Primary documentation: book of acquisitions.

- Using the method under consideration, it is possible to repay debts with different repayment periods: due, not due, indefinite. If the debt payment deadline has passed, it is required to cover it within a week after submitting the claim.

- Typically there are two parties involved in the transaction.

- DT 60 CT 62.

- DT 68 CT 19. Explanation: tax deductible. Amount: 1,800 rubles. Primary documentation: book of acquisitions.

- DT 51 CT 62. Explanation: fixation of the amount of funds paid under the contract. Amount: 13,800 rubles. Primary documentation: extract from a banking institution.

- accounts payable to Hermes amounted to 10,000 rubles. (including VAT – 1525 rub.);

- Master's receivables amounted to 30,000 rubles. (including VAT - 4576 rubles).

- DT 60 (sub-account: Settlements with the organization "Angelina") KT 62 (sub-account: Settlements with). The following amounts will need to be reflected: 10 thousand rubles (the balance of the debt to “Angelina”), 30 thousand rubles (the balance of the debt of “Books for Children” to), 90 thousand rubles (the amount of repayment of obligations).

- DT 60 (subaccount: Settlements with) CT 51. Amount: 10 thousand rubles were transferred towards the balance of the debt.

- DT 51 CT 62 CT 62 (subaccount: Settlements with the organization “Books for Children”).

Nuances of forming a tripartite netting act

Such a need arises if the parties provide each other with homogeneous interconnected services, then a document is drawn up that contains the following data:

- Information about documents that are evidence of the provision of mutual services by companies to each other;

- The amount of debt of each of the counterparties as of the date of document generation;

- The final amount, previously agreed upon, to be withdrawn from the receivables and payables of each participant. Here you will learn how to write off accounts receivable with an expired statute of limitations;

- The amount of remaining debt to the counterparties of each of the parties to the transaction.

Next, the act is certified and signed. Important: reconciliation reports must be attached to it, and all amounts in all documents existing for the offset must have a separate indication of VAT.

How to carry out trilateral netting between organizations example

Explanation: fixation of the amount of funds paid under the contract. Amount: 13,800 rubles. Primary documentation: extract from a banking institution.

When you select the “Carry out netting” operation, the debts are closed.

For example, one got the shipment, the other paid, both need to pay off their debts.

To carry out offsets between contracts in 1C 8.3, it is required that in the document the amounts of the supplier’s debt and the debt to the supplier are the same. Settlement is carried out for this amount. For this purpose, we correct the value in the “Settlement Amount” column. At the bottom of the document, the difference between accounts receivable and accounts payable is displayed; this difference should be equal to zero.

In a similar way, a mutual settlement with the buyer counterparty is drawn up. To do this, you need to indicate the following details: type of transaction - select “Debt offset”, to offset the debt - select “Buyer”, to offset the debt - “Our organization to the buyer”.

Table of contents

Example

Preliminary actions

The procedure for registering a netting transaction

The examples given in the article were reproduced in the “Accounting for Ukraine” configuration (revision 1.2). The methodology described in the article is relevant for the configurations “Management of a trading enterprise for Ukraine” (revision 1.2) and “Management of a manufacturing enterprise for Ukraine” (revision 1.3).

According to Article 528 “Fulfillment of the debtor’s obligation by another person” of the Civil Code of Ukraine dated 16.01.

https://www.youtube.com/watch?v=3yX-hIUz748

2003 No. 435-IV: “The debtor may assign the fulfillment of an obligation to another person unless the terms of the contract, the requirements of this Code, other acts of civil law or the essence of the obligation imply that the debtor is obliged to fulfill the obligation personally. In this case, the creditor is obliged to accept the performance offered for the debtor by another person.”

The article provides a description of the situation for reflecting the offset of debt between counterparties.

Settlement act - form and details

The act does not have a unified form, but the following information must be included in it:

- Details of the parties;

- Date and place of compilation;

- List of persons participating in the compilation;

- Title of the document;

- The basis for its formation;

- Details of the documents on which the debt was formed;

- Amounts of debt including VAT;

- Amount to be credited;

- Availability of remaining debt;

- Signatures of the parties.

Instructions for compilation

- A document is generated in any form, according to the expressed requirements of the parties.

- It can be compiled either by hand or in printed form.

- To compile it, you can take A4 paper.

Important: after drawing up the document, each party is required to have its own copy signed by all authorized persons and certified by the head of the enterprise.

- In this case, the act must necessarily contain the following data:

- Information about enterprises conducting mutual offsets;

- Reasons for the occurrence of debts;

- List of obligations;

- The final amount.

Settlement under contracts

Let's consider an example when our company ordered 3 office chairs from a supplier for the amount of 6 thousand rubles, but has not yet paid for this delivery. After some time, we provided lawn mowing services for 4 thousand rubles. In the program, it is necessary to offset and reduce the debt to 2 thousand rubles.

You can find acts of offset in the 1C “Purchases” menu, or “Sales” select the “Debt Adjustment” item.

All previously entered documents on debt adjustments will open in front of you. Create a new document. The most important thing here is to correctly indicate the type of operation. In this case, we will offset with the same company, but under different agreements: supply and provision of services. Therefore, “Debt Settlement” was chosen.

In the “Off the Debt” position, select “To Supplier”. In the case where it is owed not to us, but to us, the “Buyer” item is selected.

Next, in the “On account of debt” item, select the value “Supplier to our organization.”

In the “Supplier (creditor)” detail, select the company with which you need to make a settlement. In our case, accounting in the program is kept for several organizations at once, so in the header we will also select the necessary one (which has a debt).

In the document on offsetting in 1C 8.3 there are two tabs reflecting the list of documents on which accounts payable (ours) and accounts receivable (to us) were formed. You can fill in the data either manually or automatically. To automatically fill, click the “Fill” button on the desired tab and select the appropriate item from the menu that appears. Both tabs are completed separately, but the interface is the same.

On the first tab, a document for the purchase of office chairs in the amount of 6 thousand rubles appeared. The second – provision of lawn mowing services for 4 thousand rubles. The amounts vary and this can be seen at the bottom of the form (- 2 thousand rubles).

To ensure correct settlement, we will adjust our debt to the supplier on the first tab. Let's set 4 thousand rubles instead of 6 thousand rubles.

Next, we will record and post the document. We have created a netting transaction with our counterparty in the amount of 4 thousand rubles.

In the same way, you can set off with the buyer. The only difference is in the other parameters of the document header.

Rules for mutual settlement

The amount of debt when performing a netting operation can be differentiated. In case of unequal value of the debt, the offset will be carried out at the minimum amount. Then one counterparty pays off the entire debt, and the second only partially.

Cases when offset is possible

Art. 410 of the Civil Code of the Russian Federation provides for the possibility of repaying the obligations of companies to each other through offsets. This article specifies the requirements that are mandatory for the test:

- The presence of mutual debt, that is, all participants in the transaction are simultaneously creditors and debtors.

- The time has come to fulfill obligations; if there is no deadline, then the fulfillment of obligations will occur after a reasonable period of time; if the period is specified on demand, then the fulfillment of the obligation must be completed within seven days from the date of demand.

- The offset requirement must be uniform, that is, for example, all obligations of the offset participants must be monetary.

Impossibility of offset

Art. 411 of the Civil Code of the Russian Federation also describes cases of impossibility of offset:

- If the statute of limitations has expired for any of the claims, and this has been reported.

- Claim for compensation for harm to life or health.

- Maintenance requirement for life.

- Request for payment of alimony.

- In other cases provided for by the contract.

Accounting entries for netting between organizations

Offsetting is the repayment of counterclaims without additional cash flow.

As a result of offset, the homogeneous claims of the parties to each other are canceled. Let's look at an example of how to carry out netting between organizations and the transactions generated for this operation.

Contents Settlement is not considered a transaction. To be able to mutually settle the claims of the parties, several conditions must be met:

- Counterclaims must be homogeneous, most often they are presented in monetary form;

- The parties to the netting took part in at least two transactions that led to the emergence of obligations;

- The nature of the claims is counter, that is, each of the subjects is both a debtor and a creditor for the other;

- These demands must arise.

With the help of offset you can pay off

Settlement between two organizations

The company has the right to offset mutual obligations in two ways:

- unilateral statement by any of the participating parties;

- mutual agreement of both participants.

Unilateral procedure for offsetting mutual claims

Art. 410 of the Civil Code of the Russian Federation provides for the possibility of mutual offset at the request of any of the companies.

Documents for registration:

- Act of reconciliation;

- application for offset of mutual claims;

- agreements on the conclusion and terms of the transaction (required);

- invoices (required);

- invoices (required);

- acts on the provision of services (required).

Act of reconciliation

The reconciliation report plays a big role in the netting process (this is an optional document, but it is recommended to draw it up before the offset). It helps to study the information available to both organizations and determine the exact amount of debt. Subsequently, this will help prevent possible disagreements and court proceedings.

The reconciliation report includes a table of two columns containing information about the amount of debts according to each counterparty

The reconciliation report includes:

- date at the time of reconciliation;

- the names of both organizations;

- amount of liabilities;

- commitment agreements;

- balance as of the reporting date;

- signatures;

- print.

Settlement application

In the absence of a unified statement, it is written in any form with the presence of the main details of the primary accounting documents (Clause 2, Article 9 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting”). And also the application must include information about the terminated obligations, the amount of offset, and the time of offset of mutual claims.

A prerequisite for carrying out offset at the request of any of the companies is to receive information confirming that the partner was notified of the termination of obligations by offsetting mutual claims, otherwise the offset requirement will be rejected.

You should draw up an application according to the sample, not forgetting the details, date and place of its execution

Bilateral settlement procedure

This option is more reliable than the previous one. To carry out mutual offset, the same documents are required as for unilateral, only the application for offset of mutual claims is changed to a mutual agreement, which implies the signing of a mutual act (agreement) by both parties. This eliminates the possibility of cancellation. This document is also drawn up in any form with all the details.

The bilateral agreement should indicate the addresses and bank details of the parties

Accounting entries

Offsetting reflected in accounting does not lead to the formation of new expense or income items in the balance sheet.

Table: accounting of claims offset operations

| Account debit | Account credit | |

| Account 60 “Settlements with suppliers and contractors” (Account 76 “Settlements with various debtors and creditors”) | Account 62 “Settlements with buyers and customers” (Account 76 “Settlements with various debtors and creditors”) | Settlement |

Example of unilateral netting

On January 14, 2021, Alpha LLC purchased 60 sets of tools for repairing various equipment from Beta LLC in the amount of 75,000 rubles. Payment is made after successful receipt of the goods, until February 10, 2021. Alpha LLC provided repairs to production equipment worth 80,000 rubles with a payment date of February 10, 2018.

How to reflect netting in accounting

Offsetting mutual claims is one of the methods of settlements between organizations.

Offsetting is possible, determined by civil law. Since the offset of mutual claims reflects only the fact of payment of received or transferred assets (repayment of receivables or payables), in accounting it does not lead to the emergence of income or expenses (clause 2 of PBU 9/99, clause 2 PBU 10/99). The article: “” describes the terms debit, credit, balance using simple examples. In accounting, the offset of mutual claims is reflected in the subaccounts opened for each counterparty to accounts 60 “Settlements with suppliers and contractors”, 62 “Settlements with buyers and customers”, 76 “Settlements with various debtors and creditors.” When carrying out offsets, make the following entries: Debit 60 (76) Credit 62 (76) - reflects the termination of the counter obligation to pay for goods (works, services) by offsetting mutual claims. Situation: possible

What accounting entries does the new contractor need to create to reflect mutual settlements with the original contractor and the customer? Accounting consultations at the company Garant-Victoria

\ \ \ What accounting entries does the new contractor need to create to reflect mutual settlements with the original contractor and the customer?

A busy schedule prevents you from attending professional development events? We found a way out! Consultation provided on 02/05/2016 Previously, a contract for the performance of work was concluded between the customer and the contractor (general taxation system). As part of the contract, the contractor received an advance, calculated and paid VAT.

The organizations then entered into a tripartite agreement to change the parties to the contract.

Netting between three organizations

Situations arise when not two, but three organizations become participants in the mutual settlement.

Conditions, documents

Cases when offset is possible and impossible are also regulated by Art. 410 and Art. 411 of the Civil Code of the Russian Federation. However, there are certain conditions for carrying out trilateral netting:

- each company is both a creditor and a debtor to the other at the same time (company A is a debtor to company B and a creditor to company C; company B is a debtor to company C and a creditor to company A; company C is a debtor to company A and a creditor to company B);

- there is cyclicality and homogeneity of obligations;

- the debt is not overdue;

- obligations and the amount of debt are confirmed by a tripartite reconciliation act.

A bilateral agreement can serve as an example of a netting agreement. It must include:

- All participants;

- amount of debt;

- terms of obligations;

- offset amount;

- time spending;

- accounts receivable and payable before and after offset;

- approved acts of reconciliation of the parties.

All amounts subject to offset must be indicated including VAT.

Accounting entries as an example

has a debt obligation to LLC "B" in the amount of 20,000 rubles, LLC "B" has a debt obligation to LLC in the amount of 40,000 rubles, LLC "C" has a debt to LLC "A" in the amount of 15,000 rubles. A tripartite agreement was adopted to carry out a netting operation in order to partially repay the debt in the amount of 15,000 rubles.

Table: netting in the accounting of LLC “A”

| Account debit | Account credit | Amount (rub.) | |

| D 62/C | K 90 | Supply of goods for LLC "S" | 15 000 |

| D 41 | K 60/B | Acceptance of goods from the supplier LLC "V" | 20 000 |

| D 60/B | K 62/S | Settlement | 15 000 |

Table: netting in the balance sheet of LLC “B”

| Account debit | Account credit | Amount (rub.) | |

| D 62/A | K 90 | Supply of goods for LLC "A" | 20 000 |

| D 41 | K 60/C | Acceptance of goods from the supplier "S" LLC | 40 000 |

| D 60/C | K 62/A | Settlement | 15 000 |

Table: netting transactions in LLC “S”

| Account debit | Account credit | Amount (rub.) | |

| D 62/B | K 90 | Supply of goods for LLC “V” | 40 000 |

| D 41 | K 60/A | Acceptance of goods from supplier LLC "A" | 15 000 |

| D 60/A | K 62/V | Settlement | 15 000 |

So, an incomplete offset was carried out, equal to the amount of 15,000 rubles, between LLC “V” and LLC “S”.

Postings when working on netting

- 2.1 Unilateral offset

- 2.2 Bilateral scoring

- 3 Postings for netting between organizations

- expenses for lifelong maintenance of citizens;

- payment of alimony;

- compensation for harm caused to human health;

- one side of the offsets is involved in its bankruptcy case.

Rules for netting Mutual netting is not considered a transaction.

Prices and training mode: accounting courses Course 1C: Accounting “1C 8.2 for professionals” Course “Accounting 1C: Accounting 8.2 for beginners”

Table of contents

The procedure for applying the mutual offset act is prescribed in Article 410 of the Civil Code of the Russian Federation. In practice, organizations draw up a standard document signed by all parties to the transaction. Before signing it, all calculations and mutual obligations are reconciled. The advantage of the act of offset is its ability to neutralize the objections of the other party.

According to the law, the act must include: the date of preparation, details of the parties to the transaction, basic requirements, an indication of the repayment of mutual obligations by offset, the seal and signatures of the parties. A correctly drafted document like this can become a means of optimizing the payment system of both enterprises.

Article 410. Termination of an obligation by offset

General points

The netting act is used when it becomes necessary to reconcile the total liabilities of one company with another. The contract includes all debts or only part of them for a certain period of time.

The legislation of the Russian Federation has not approved a unified model of such a document.

Lawyers still advise adhering to the structure that has developed during the practical use of this offset instrument.

You cannot use the act of mutual offset of debt in the following situations:

Such a document is drawn up in two copies: the first remains with the organization that initiated the transaction, the second is transferred to the counterparty. If the act contained references to related documents, for example, contracts, invoices, copies of them must be attached to it.

Rules

By analyzing receivables and payables, enterprise specialists identify the presence of possible mutual requirements with partner organizations. Settlement is possible at the request of one party. In practice, as a rule, the decision is made by all participants in the future transaction.

The rules for conducting mutual offsets are as follows:

- This operation can be carried out by organizations between which there are two or more obligations;

- Requirements from both organizations must have the same units of measurement, for example, cash;

- Documented evidence of the occurrence of mutual obligations.

After reconciling the amounts of debts, the parties decide to sign an act of mutual settlement. The closing entry in accounting is an important rule in offsets of liabilities.

Purpose of the document

The main purpose of the document is to simplify the procedure for paying company bills after the expiration of the main agreement between the two companies.

Positive aspects of the netting act:

- significant money savings;

- reduction of overall costs;

- helps pay off debts that have existed for a long time.

With this document, you can settle obligations between two, three or more organizations without using funds.

Such an operation will not only help reduce the time it takes to transfer money from one account to another, but will also save money on bank commissions.

The act of offset is used when there is a shortage of working capital, as well as to pay off debt that has been going on for many years.

Sample act of offset

The procedure for using this settlement tool is quite simple. To begin with, the parties agree on mutual reconciliation of obligations. Each party sets its own demands, for example, in monetary terms.

Next, a standard document is signed, where both parties clearly state the amounts for which they are willing to write off each other’s debts.

We suggest you familiarize yourself with Check the car by owner's last name using the traffic police database

Based on this, the accountants of the counterparties write off their debt and also reduce the amount of their expected profit from the partner organization.

All stages of mutual settlements must be supported by cover letters, the necessary documents with signatures and seals must be drawn up. For example, it is necessary to write off obligations between organizations “A” and “B”.

Lawyers prepare the contract, managers sign it, and accountants display this entry in accounting.

Documentation

| Settlement Act | It can be considered the primary document for calculation. The main text must contain a detailed calculation of the debt and the final amount of the claim. The amount of taxes that must be paid by both organizations is separately highlighted. Particular attention should be paid to dates and indicate the time of shipment of the goods and the deadline for the obligations. |

| Application for offset | Such a document is drawn up unilaterally and sent to partners. In the future, it will be formalized as an act of mutual settlement. If there are not many obligations, a text version of the document is suitable. A large number of requirements should be presented in table form. |

Special forums of practicing accountants will tell you where to find such documents and how to fill them out.

Application for offset of mutual claims

Primary requirements

The basic requirements for the use of such documents as a payment instrument for services provided are specified in the Civil Code of the Russian Federation. An important point in this regard is the deadline for completing the transaction, which is prescribed in the act. In a similar way, obligations can be written off, payment for which is provided upon the expiration of a certain period in the future or already in the past.

Only mutual, homogeneous obligations are counted: I owe you, you owe me money for goods or services in the same amount. The debt of the parties cannot be closed in this way where, for example, one party owes money for the delivered goods, and the other, according to the agreement, to do repair work.

There is a list of requirements that are prohibited from being satisfied using acts of offset (Article 411 of the Civil Code of the Russian Federation).

Article 411. Cases of inadmissibility of offset

Filling

Multilateral netting

Rules and regulations that are also characteristic of trilateral can be applied to multilateral offsets.

Requirements for conditions and documents for netting

Each accountant needs to study the legal sources regulating the possibility of multilateral offsets, as well as become familiar with the specifics of drawing up supporting documents.

Table: documents required to offset claims and obligations

| Legal sources | Regulatory area | Names of mutual settlement documents |

| Article 410 of the Civil Code of the Russian Federation | Termination of obligations by offset | Settlement agreements |

| Article 411 of the Civil Code of the Russian Federation | Cases of impossibility of credit | |

| clause 2 art. 9 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting” | Requirements for primary documents | Settlement agreement and reconciliation report |

Example of multilateral netting with accounting entries

has a debt obligation in the amount of 12,000 rubles for a product received from the organization V LLC. LLC “V” owes LLC “S” an amount equal to 25,000 rubles for the supply of goods. LLC “S” has a debt obligation in the amount of 16,000 rubles to the organization LLC “D” for the goods supplied. LLC "D" has a debt to LLC "A" in the amount of 10,000 rubles for the goods received.

On the date of the offset, the time for fulfilling all mutual obligations has come. The offset amount is equal to the minimum debt, that is, 10,000 rubles.

Table: accounting of the enterprise LLC "A"

| Account debit | Account credit |

Posting debt adjustment

Contents LLC "GDE" has a debt to LLC "ZhZI" in the amount of 560,000 rubles, LLC "ZhZI" has a debt to LLC "ABV" in the amount of 150,000 rubles.

The parties decided to enter into an agreement on mutual settlement between three organizations in order to partially repay obligations, namely for the amount of the smallest debt (150,000 rubles). Thus, the offset looks like this: from LLC “ABV” to LLC “ZhZI”, from LLC “ZhZI” to LLC “GDE”, from LLC “GDE” to LLC “ABV”.

As a result of the transaction, the remaining debt is as follows:

- ABV LLC to GDE LLC - 280,000 rubles;

- LLC ZhZI's obligations to LLC ABV have been terminated.

- LLC "GDE" to LLC "ZhZI" - 410,000 rubles;

Accounting entries for netting between three organizations For correct accounting, it is necessary to very carefully monitor accounting entries to avoid errors.

Procedure for drawing up the document

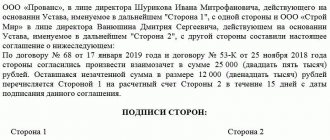

The act is drawn up in writing. The title indicates the correct name of the paper: “Act of Settlement of Mutual Claims.” If necessary, indicate the number. The document must be drawn up in a quantity equal to the number of signatories. At the same time, the legislator does not limit the number of participants in the transaction.

Next, the date and place of drawing up the paper are indicated. The preamble reflects information about the signatories - they can be both individuals and organizations. In this case, both of them can be represented by authorized representatives with the right to sign.

Next, it is necessary to reflect the nature of the obligations subject to offset. It is equally important to indicate the basis for their occurrence - details of contracts or other documents-bases (for example, administrative acts or court decisions), the amount of obligations (in numbers and in words), if we are talking about money, or data on other types of claims.

Preliminary actions

Information about counterparties must be entered into the “Counterparties” directory.

Since the obligatory analytical aspect of accounting for mutual settlements in the configuration is accounting under contracts, you need to select the option of conducting mutual settlements with counterparties.

In the business situations under consideration, there are no peculiarities in filling out contracts. In the example, agreements with mutual settlements “Under the agreement as a whole” were used.

See also: A contractual agreement is

What does it mean to offset counterclaims of the same type and why is it important?

One of the conditions for drawing up an act on mutual offset of claims is the homogeneity of obligations, which are offset both in subject and in essence (Article 410 of the Civil Code of the Russian Federation). That is, this is the offset of only monetary (property) debts or the provision of services, performance of work, etc. If the requirements are heterogeneous, the document will not have legal force.

In the text of the act, in addition to indicating the amount of the obligation, it is necessary to clarify which part of it is counted. If obligations are not subject to mutual offset in full, it is necessary to indicate the fate of the remaining part of the debt.

For example, the wording may be as follows: “The parties agreed to offset the above agreements in the amount of 7,500 rubles. The remaining debt in the amount of 12,000 rubles. Vasilek LLC undertakes to transfer to the current account of Doors to the World LLC no later than 02/12/2019.

The amount of sanctions in the event of failure to fulfill the terms of the agreement by one of the parties does not need to be indicated in the act, since in fact the parties have already entered into a transaction in pursuance of which the act is drawn up, and, accordingly, all fines are specified in its terms.

As you can see, this act is drawn up quite simply. The sample act on the offset of mutual claims offered for download from the link above will help to correctly complete the offset for both citizens and organizations.

You will also be interested in reading the materials that we wrote specifically for our Zen channel.

Tripartite netting act

The provisions of Russian civil legislation allow both the literal fulfillment of mutual obligations and their termination by offset. At the same time, domestic rulemaking provisions allow both the preparation of a bilateral agreement and the drawing up of an act of offset between three organizations. A sample of such a form can be downloaded from the text below.

The necessary conditions

Carrying out offsets allows you to pay for purchased goods or services in return.

Often in the small business sector there are simply no extra financial resources that are not invested in turnover, but it is necessary to pay off the counterparty. In this case, you can use mutual offset between business entities.

Please note! The following are the main points that you should pay attention to in order to complete the transaction:

- in the legal relationship between two legal entities there must be at least two contractual obligations. According to one of them, the organization acts as a creditor, and according to the second, as a debtor. In some agreements, netting occurs between three or more enterprises; remember, the law does not prohibit such a procedure;

- obligations must be of a homogeneous nature, for example, financial debt. The parties stipulate the timing of the offset and the potential possibility of claiming the arrears.

By agreement, business entities have the right to use offset not for the entire volume of existing obligations, but only for a certain part of them. The rest of the debt can be recovered in financial terms.

Watch the video. Settlement (barter). How to apply?

Termination of obligations by offset

Any obligation must be fulfilled in accordance with its essence.

It should also be noted that unilateral refusal to perform duties or their change is equally prohibited.

It should be emphasized that the norms of domestic acts of rule-making in the sphere of economic relations directly allow for alternative options for the execution of agreements. One of these methods is the conclusion of a tripartite netting act intended to pay off mutual claims between three companies.

This is directly stated in Art. 154 of the Civil Code of the Russian Federation, which allows both bilateral agreements and multilateral transactions.

Regardless of the number of participants in the competition, when drawing up the form, it is necessary to take into account the following mandatory requirements:

- the obligations of all persons must be of the same kind and essence;

- for companies repaying the relationship, the due date is due;

- Considering that the termination of obligations is a transaction, in order to conclude an act of offsetting the mutual claims of three legal entities, the intention of all parties to the specified operation is required.

In addition to what is described above, when drawing up an offset agreement, it should be put in writing and ensure that the text of the form contains the necessary information:

- it must contain the names of enterprises, full names of managers or authorized persons, indicating the documents giving them the right to sign the form;

- Each tripartite act of offsetting mutual claims, a sample of which is given at the link below, must describe the essence of the obligations, the grounds for their occurrence, the deadlines for fulfillment, as well as the amount of the initial claims and an indication of the part to be repaid.

Download the tripartite netting act

The formation of the described form is completed with the signature and seal of the enterprise.

It is important to note that at present, imprinting the organization's stamp on the text of the agreement is not a mandatory requirement. However, taking into account the established customs of business transactions, it is possible to affix the signatures of officials under the text of a tripartite act of offset with the seals of the parties.

Tripartite netting in 1s 8.3

Question:

How to carry out offsets in 1C:Accounting 8?

Publication date 10/04/2018

Release 3.0.65 used

Payments under the contract (offset)

Settlement

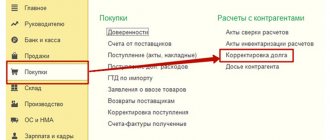

In the 1C: Accounting 8 program, to reflect the operation of offsetting mutual claims, the document “Debt Adjustment” is used (Fig. 1):

- Section: Sales

-

Debt Adjustment

(or section:

Purchases

-

Debt Adjustment

). - “Create” button, in the “Operation type” field, select “Debt offset”.

- In the “Off the Debt” field, select “To the Supplier” if the debt to the supplier is set off, or select “To the Buyer” if the buyer’s debt is set off.

- In the “On account of debt” field:

- if a debt to a supplier is being offset, select one of two options – “Supplier to our organization” or “Third party to our organization”;

- if the buyer’s debt is being offset, select one of two options – “Our organization to the buyer” or “Our organization to a third party.”

- If offset is made in a currency other than the currency of the Russian Federation, select it in the “Currency” field.

- By clicking the “Fill” button in the tabular part of the document on each of the tabs, information on the corresponding debt (agreement, settlement document with the counterparty, amount) will be automatically selected. If the claim amounts are not equal, then in the “Settlement Amount” column, adjust the larger of the amounts on one of the tabs.

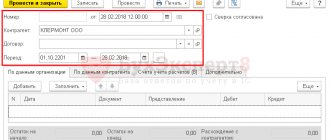

- "Pass" button. To view the result of document posting (Fig. 2), click the button.

- Use the “Act of Settlement” button to print the act.

Act of offset between three enterprises

The current system of civil legislation does not contain any special or specific requirements for the procedure for preparing, executing or signing an offset agreement between three enterprises.

To comply with the provisions of Russian rule-making acts, the relevant companies must comply with all mandatory requirements for offset reflected in the trilateral netting act, a sample of which is given at the link above.

The only peculiarity is that when offsetting obligations between three organizations, each company must be a debtor. Only by implementing such a condition will the principle of reciprocity of claims be observed and, accordingly, the legitimacy of the triple act of offset, a sample of which is given in this publication, will not raise doubts.

As a conclusion, we consider it important to emphasize that an agreement to set off counterclaims, like any other civil law contract, can be challenged and declared invalid. In this case, the obligations will not cease.

To minimize the labor costs for preparing the agreement in question, we recommend using a sample of a tripartite netting act, which can be downloaded from the link above.

Sep 10, 2019adminlawsexp

voice

Article rating

Postings under a tripartite agreement

To be able to mutually settle the claims of the parties, several conditions must be met:

- These demands must arise.

- Counterclaims must be homogeneous, most often they are presented in monetary form;

- The nature of the claims is counter, that is, each of the subjects is both a debtor and a creditor for the other;

- The parties to the netting took part in at least two transactions that led to the emergence of obligations;

With the help of offsets, you can pay off claims that have both arrived and have not yet arrived, as well as claims with an indefinite period.

Claims of the first type must be paid within 7 days from the date of their presentation. The homogeneity of demands means that the situation of repaying a monetary obligation with goods is not an offset - such repayment is called barter. As a result of the transaction, the remaining debt is as follows:

We recommend reading: Application to the management company for electricity connection

Offsetting and tax accounting: nuances

Tax accounting of legal relations for the offset of obligations is characterized by the fact that:

1. The fact of signing a netting agreement between organizations does not change the composition of the VAT tax base. It does not matter if, for example, the company received an advance from the counterparty on account of future deliveries, and it was set off under an agreement to offset obligations, while goods or services were not delivered to the counterparty.

2. Carrying out offset does not change the composition of the tax base for income tax, since under the accrual method, income and expenses under the agreement with the counterparty will be recognized before offset. Under the cash method, income and expenses will be determined based on the fact of offset.

3. With the simplification, the situation is similar to that observed with the cash method of accounting for income and expenses by the payer on the OSN. Income and expenses are recognized by the company using the simplified tax system only upon the fact of offsetting obligations with the counterparty.

When it is possible and when it is impossible to offset

Settlement is an example of a civil transaction and is therefore regulated by the Russian Civil Code. Despite the fact that the legislation does not define a single sample of documents (acts, statements and agreements for offsets), the Code directly defines cases when offset is permitted and when it is not allowed. You can read more details in articles 410 and 411.

In accordance with the law, companies can offset liabilities:

- if the performance deadline has arrived, a specific one is not specified in the contract or is intended to be demanded (in rare cases that do not contradict the legislative norms of the Russian Federation, offset is possible for those obligations that have not yet occurred);

- if organizations are both creditors and debtors to each other;

- if the obligations are homogeneous (counterparties owe each other money in a single currency, in some cases, if there is a difference in currencies, offset is possible by agreeing on a transfer at the current exchange rate).

Article 411 specifies cases when offset is prohibited:

- on claims for collection of alimony payments, compensation for damage to health and life, lifelong maintenance;

- on claims with an expired statute of limitations;

- in other cases provided by law.

Thus, offset is prohibited if the agreement prohibits it; in cases where one of the parties goes through bankruptcy; in cases of conducting foreign economic activity with a foreign organization and others.

Settlement cannot be carried out if the parties’ requirements for each other are not homogeneous. It is impossible to count when one organization must supply material resources (for example, construction), and the second must supply funds.

Don't forget to download sample acts for free.

Settlement between several organizations

As a general rule, repayment of mutual obligations between several organizations does not fall under the concept of offset. The fact is that offset is possible only if there are counter claims of the same type (Article 410 of the Civil Code of the Russian Federation). In the situation under consideration, this condition is not met. Because either party has receivables from the transaction. Completed with one organization, and accounts payable under the transaction. Committed with another organization.

Despite this, in practice, organizations can carry out multilateral netting of obligations. This right is provided for by the provisions of Article 421 of the Civil Code of the Russian Federation. It states that the parties may enter into an agreement as provided. It is not provided for by law or other legal acts. In this case, the general provisions on the contract apply to contracts concluded by more than two parties. If this does not contradict the multilateral nature of such agreements (clause 4 of Article 420 of the Civil Code of the Russian Federation).

As a rule, in multilateral offsets an agreement is concluded on mutual settlements. Such an agreement is not a uniform accounting document. Therefore, it can be compiled in any form in compliance with the requirements. Which are presented to the primary accounting documents.

When conducting a multilateral competition, follow the rules. Counterclaims submitted for offset.

- offset can only be carried out if each of the parties to the offset has reached the deadline for fulfilling the obligation;

- in case of unequal debts, offset is carried out for the amount of the least of them;

- the offset agreement must contain information reflecting the circumstances of the offset.

to menu