How to draw up an order granting the right to sign and what does its sample look like?

Among the situations when the chief accountant is given the right to sign, the following can be listed:

- the need to transfer part of the authority to sign documentation from the head of the company or other official during the absence of these persons;

- granting the chief accountant the right to sign certain documents if this right was not granted to him when he was hired;

- granting the chief accountant the right to sign documents for the manager when representing the interests of the company individually outside the territory of its location;

- in other situations.

In addition to specially specified situations, the chief accountant, by virtue of his position, has to deal with a huge number of documents. Find out how to regulate the process of signing them by the chief accountant and what the legislation prescribes in this regard from the subsequent sections of the article.

The order granting signature rights to the chief accountant does not have a mandatory, legally established form. The period for which the right to sign must be indicated (for the entire duration of the chief accountant’s position, or for a certain period of time) and clarifying information regarding those documents that can be signed - either all documents or a specific list.

“Due to the expansion of the product sales market, an increase in the number of counterparties and an increase in the volume of primary accounting documentation

I ORDER:

- From 07/01/2018, grant the right to sign universal transfer documents (UDD) to the chief accountant Tamara Nikolaevna Selezneva.

- Responsibility for organizing the timely execution of UPD and their signing is assigned to the chief accountant T. N. Selezneva.

- For the performance of additional duties from 07/01/2018, pay T.N. Selezneva an increase in the amount of 1% of the salary.

- Control over the execution of this order shall be entrusted to commercial director A. Yu. Devyatov.”

The right of the second signature of the chief accountant on documents

the right of the second signature belonged to the chief accountant - this was the wording contained in clause.

7.6 of the Bank of Russia Instruction No. 28-I dated September 14, 2006, devoted to the procedure for opening and closing bank accounts.

No one questioned the status of the second signature of the chief accountant if an order was issued for his appointment to the position.

After Law No. 129-FZ and Instruction No. 28-I were replaced by a pair of updated regulatory documents of the same name (Law No. 402-FZ and Bank of Russia Instruction No. 153-I dated May 30, 2014), on the legislatively established powers of the chief accountant in affixing a signature There is no need to talk about documents for the following reasons:

- the mention of the second signature of the chief accountant disappeared from the text of instruction No. 153-I;

- Law No. 402-FZ does not have a separate article dedicated to the chief accountant and a phrase prohibiting the acceptance for execution of documents without his signature.

Invoice without the signature of the chief accountant: is the deduction legal?

In the resolution of the Federal Antimonopoly Service of the North-Western District dated November 17, 2006 in case No. A56-35103/2005, the court indicated that the identity of the signatures of the general director and chief accountant in the disputed invoices does not deprive the organization of the right to claim a refund of the VAT paid to the supplier on the basis of this document. But this is provided that it contains all the necessary details and information required by tax legislation.

“The presence in invoices of transcripts of the signatures of the manager and chief accountant is not provided for by the provisions of paragraph 6 of Article 169 of the Tax Code of the Russian Federation and the requirements for the preparation of primary accounting documents given in Article 9 of the Federal Law of November 21, 1996 No. 129-FZ,” the resolution states.

A similar conclusion is contained in other resolutions. For example, in the resolution of the Federal Antimonopoly Service of the North Caucasus District dated October 29, 2008 No. F08-6533/2008 in case No. A53-2656/2008-C5-14, the court recognized the deduction on an invoice signed by the manager as legitimate. And all because, according to the order, he reserved the right to sign accounting and financial documents for the chief accountant.

A similar decision, motivated by the fact that the general director of the company simultaneously performs the duties of the chief accountant, was announced by the court in the decision of the Federal Antimonopoly Service of the North Caucasus District dated 06/03/2009 in case No. A53-17547/2008-C5-23.

That is, detailed planning of the business organization - in the charter and other constituent documents - plays an important role in the ability to defend the legitimacy of the absence of the signature of the company's chief accountant on the invoice.

The risk-based approach of 1C-WiseAdvice specialists to the management of processes that are strategically important for business - accounting and tax accounting, document flow, including personnel, etc. - will free the company from the need to make changes to the constituent documents or issue orders retroactively.

Managers of companies that have outsourced their accounting to 1C-WiseAdvice spend their time on business development rather than its day-to-day maintenance.

When the director has the right to sign documents instead of the chief accountant

Current legislation determines whether the director has the right to sign documents for the chief accountant, allowing the director to exercise functions without a power of attorney on behalf of the organization on the basis of:

- Federal Law No. 208-FZ dated December 26, 1995, Art. 69;

- Federal Law No. 14-FZ dated 02/08/1998, Art. 40;

- Federal Law No. 402-FZ dated December 6, 2011, art. 7 (for individual categories).

The requirements for accounting in an institution are established by 402-FZ: Part 1, Art. 7 says that its maintenance and storage of documents on it is organized by the head of the economic entity.

Director by virtue of Part 3 of Art. 7 Federal Law No. 402 assigns the process to:

- chief accountant;

- another official of the enterprise.

The director, if necessary, maintains records independently. When conducting the process independently, the director is the sole executive body and performs duties in two areas - management and accounting.

This provision applies to:

- organizations on a simplified system;

- medium-sized business entity.

In the following types of economic entities, the right to sign for the chief accountant is not delegated to the director (Part 3, Article 7 of Federal Law No. 402):

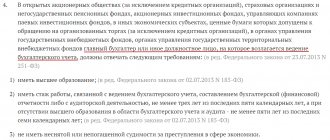

- institutions in which reporting goes through a mandatory audit;

- housing, housing-construction cooperatives;

- credit consumer cooperatives;

- microfinance institutions;

- budgetary institutions;

- political parties;

- Bar associations and bureaus;

- notary and bar associations;

- NPO with the functions of a foreign agent.

How to fill out documents that require two signatures?

Since mid-2015, an appendix to the Order of the Ministry of Finance of Russia dated April 6, 2015 No. 57n, the signature of the chief accountant was excluded from a number of documents, including from:

- balance sheet;

- financial results report;

- statement of changes in capital;

- statement of cash flows and intended use of funds;

- simplified forms of balance sheet.

Completion of one of the key accounting documents - accounting (financial) statements is regulated by Article 13 of Law No. 402-FZ. Thus, the reporting is considered completed after it has been signed by the head of the organization. The law does not provide for any other requirements for its approval.

This provision is confirmed by the Resolution of the Arbitration Court of the Far Eastern District dated 02/05/2019 No. F03-6116/2018 in case No. A73-8993/2018. In it, the court, referring to the above-mentioned article, confirmed that the reporting is considered drawn up after the general director has put his signature on it.

At the same time, clause 17 of PBU 4/99 and clause 38 of the Regulations on accounting and financial reporting in the Russian Federation insist that this document is signed by both the director and the accountant.

The contradictory content of the mentioned standards was explained by the Ministry of Finance in the information message dated May 19, 2015 No. IS-accounting-2. It states that “the authority to sign accounting (financial) statements is established, as a rule, by the constituent documents of an economic entity, or by decisions of the relevant management bodies of the economic entity.”

Expert outsourced accounting services will save any company from all the delights of studying numerous and sometimes contradictory requirements for filling out reports, as well as from errors and financial risks.

Why the accounting outsourcing market is developing faster than many other business areas, read the publication “Accounting by a Third Party Organization.”

Invoice, in accordance with clause 6 of Art. 169 of the Tax Code of the Russian Federation, in addition to the manager, must be signed by the chief accountant or another person authorized to do so through a special order. In the case of an individual entrepreneur, the document is endorsed either by the entrepreneur himself or by his authorized representative acting under a power of attorney.

What should the head of an organization do if there is no accountant on staff, and the invoice is the basis for deducting the tax amounts presented to the buyer by the seller? Sign both for yourself and for the chief accountant.

The court terminated the right to sign for the chief accountant sample

In this case, the organization does not “show” its accountant to the Bank, and, accordingly, does not include him in the bank card.

This scheme for opening a current account in a bank seems quite controversial in view of the provisions of paragraph 3 of part 3 of article 7 of the Federal Law “On Accounting”, which was cited above, however, it is widely used by bank employees to attract new clients for settlement and cash services. Do you have any questions? We will help you solve them. All consultations are free!

What is a power of attorney for the chief accountant with the right to sign and a sample document

Regarding the law, they are both legal and equivalent.

A handwritten version can be implemented faster in a situation where there is an urgent need to issue a power of attorney on a business trip or at work. It is important that any chosen design option contains all the necessary information and is compiled and certified in accordance with the requirements of Russian legislation. Who in the company delegates their authority?

Most common

The right to sign primary documents

These documents can be divided into primary personnel and accounting documents, the main ones are presented in the table below.

We recommend reading: For driving on oncoming traffic

Type of primary documents Type of documents HR records Personal card of the employee; Staffing table; Vacation schedule; Timesheets for recording working hours and calculating wages; Time sheet.

Based on these documents, the accounting department calculates benefits, vacation pay and travel allowances, accruals based on piecework and temporary rates, calculates tax deductions and payments for insurance contributions to extra-budgetary funds.

The right of the second signature of the chief accountant on documents

If the authority to sign has not been delegated to anyone, the chief accountant must be formally recalled from vacation to sign this document.

This conclusion follows from the general definition of rest time and “vacation” nuances:

- affixing a signature on documents is the performance of a labor function that is subject to payment in accordance with the employment contract.

- the vacation period is not considered working time (Article 107 of the Labor Code of the Russian Federation), the employee only retains his workplace during the vacation and the average salary;

- rest time is the time during which the employee is free from performing work duties and which he can use at his own discretion (Article 106 of the Labor Code of the Russian Federation);

Thus, in the absence of a chief accountant, the right of second signature on certain documents, secured by internal company regulations, must be delegated to another employee (financial director, senior accountant, etc.). The right of the second signature of the chief accountant is secured in the order or power of attorney.

What risks does the LLC bear if the card with sample signatures does not contain the signature of the chief accountant?

In accordance with paragraph.

7.6 of the Instructions, the right of the second signature belongs to the chief accountant of the client (legal entity) and (or) persons authorized to maintain accounting records, based on the administrative act of the client - legal entity.

Consequently, the chief accountant of the organization and (or) persons authorized to maintain accounting records are given the right, following the signature of the head of the organization (other persons), to put a second signature on documents on the transfer and withdrawal of funds from a bank account.

It should be noted that if the head of a client - a legal entity, conducts accounting in person in cases provided for by the legislation of the Russian Federation, the handwritten signature (signatures) of the person (persons) vested with the right of only the first signature is affixed to the card.

In this case, in the card opposite the field “Second signature” in the fields “Last name, first name, patronymic” and “Sample signature” it is indicated that the person entitled to the second signature is absent (clause

7.10 Instructions).

Order granting signature rights to the chief accountant

In Bank of Russia Instruction No. 153-I dated May 30, 2014 with the same name, which replaced Instruction No. 280-I, the concept of “right of first and second signature” is not applied.

https://www.youtube.com/watch?v=77Ykn23XlzM

Thus, the specified concept by law:

- not provided as mandatory;

- can be used for internal purposes by any business entity.

Typically, this two-stage (or multi-stage) document signing model is used in large companies.

It is provided for the approval of documents of various types and purposes with specific officials of the company (their list is established by internal company documents), and the head of the company, who by default has the right of first signature, puts it on the document only after all intermediate signatures appear on the approval form.

For most small and medium-sized merchants, the issue of distinguishing signatures into the first and second ones is not considered at all.

Legal Russia

Based on a power of attorney from. .20 09 provide the right to sign the manager and chief accountant when preparing the following documents on behalf and at the expense of the LLC, accounts, invoices, certificates of work performed for communication services.

The right of first signature is assigned to the person indicated in the Charter; other employees can act on behalf of the legal entity only by proxy. faces.

The performance of duties can be entrusted to the accountant, but in this case, by decision of the general meeting that the accountant has the right to perform the duties of the General Manager and in the presence of an appropriate order. That’s right!

Chief accountant and general director For documentation with amounts of money, the right of the first signature is allowed to the director, and the second to the accountant. Several employees have the rights to the first and second signature at the same time. Their names are indicated in the power of attorney. The balance sheet itself contains the answer. If two signatures are provided - the director and the accountant, then both; If one is the director and that’s it.

Source: https://ukpravoedelo.ru/sud-prekratil-pravo-podpisi-za-glavnogo-buhgaltera-obrazec-74558/

Who has the right to sign primary documents

- Risks of non-contractual delivery: if the contract and the invoice are not on friendly terms, No. 11

- 2016

- Document flow, No. 24

- Recovering lost documents, No. 20

- Accounting documents: prepare, fill out, sign, No. 20

- It is advisable to include a time stamp in the electronic signature, No. 15

- The Federal Tax Service can accept electronic documents only in approved formats, No. 13

- Correcting the primary accounting system, No. 10

- An electronic document is not just created on a computer, No. 5

- We issue an order assigning the duties of the chief accountant to the director, No. 4

- We transfer accounting to an outsourcer, No. 3

2015 All documents accompanying the execution of business transactions must be signed by the first persons. Without this, they are considered invalid. Who has the right to sign primary documentation? Any document is recognized as valid only if properly executed. At the same time, depending on the type of documentation, the methods of its certification also differ.

- Basic information

- Who can sign primary documents

- Required shelf life

Thus, a very narrow circle of people has the right to sign primary documents. Who has the right to sign primary documentation? Any business transactions carried out in the organization must be documented with supporting documentation. These are called primary accounting documents. Based on them, accounting is carried out.

How to certify the signatures of the director and chief accountant

In order for another employee to perform his duties during the vacation, the director signed an order to perform additional work in order to fulfill the duties of the temporarily absent employee. Does an acting manager need to indicate “and” when signing personnel and primary documents?

No, you can't do that. Requirements for the preparation of details of organizational and administrative documents of an organization are established by GOSTGOST R 6.30-2003; OK 011-93. And although it is advisory in nature, it can be used when preparing documents.

It states that when filling out the “Signature” details in the documents, you must indicate, in particular, the name of the position of the person who signed the document. 3.22 GOST R 6.30-2003.

There are several ways to resolve this situation:

- Provide in the constituent documents the possibility of signature for the deputy director or other official.

- Issue a power of attorney for signature by an authorized person (you can do this immediately for a long period, for example, for a year).

- Issue an order or instruction for the right to sign a specific document (one-time option).

- Use a facsimile version of the signature in cases where this does not contradict the law.

Signed by I.O. If the document is signed by the acting director or his deputy, the right to sign is delegated to him on the basis of the above documents.

Currently, it is not recommended to capture part of the personal signature (personal stroke) of an official with a seal impression. But the legal meaning of affixing a seal remains the same: the official whose personal stroke (signature) is written on this document actually occupies this position in the organization whose name is carved on the seal and has the right to sign this document. In some cases, a special area is allocated for affixing a seal on a sheet of paper, which is designated as “MP” (“print place”). “Best practices” of organizations recommend developing a separate regulation on seals and stamps, which should establish the types of seals used, the procedure for their recording, issuance, etc.

If the accountant and the director are one person, how to sign certificates

The amount of taxes deducted from wages in accordance with the requirements of Chapter 23 of the Tax Code of the Russian Federation is also indicated here. The certificate is issued by the employer at the request of the employee.

An authorized person is responsible for the formation of this document.

This may be one of the accountants, personnel officers, or another employee who, according to the relevant order, is charged with filling out 2-NDFL certificates.

Only employees employed under an employment contract have the right to request the issuance of a corresponding certificate.

Signing the document: what, where and how

For this it is necessary (hereinafter referred to as Law No. 63-FZ):

- include a clause on the “transfer” of the digital signature in the order transferring powers to the deputy during the maternity leave of the chief accountant;

- issue a separate order to “transfer” the digital signature to the deputy chief accountant.

In this case, the responsibility for using the digital signature of the chief accountant will be borne by the deputy.

O. Anishina, Suzdal Our director is going on vacation. All documents for the purchase and sale of goods (invoices, invoices, powers of attorney for receiving inventory items) will be signed for him by other employees.

: Invoices are signed by the manager or persons authorized by order or power of attorney.

If the company does not have a chief accountant position

Accordingly, the absence of this employee in the organization may create additional difficulties. Let's figure out how to solve possible problems. According to the law, the situation with the absence of an accounting service and the position of chief accountant in an organization is quite typical.

Here the question may arise - how to understand whether my company belongs to these types of legal entities?

Let me remind you that in Russia there is a Federal Law

“On the development of small and medium-sized businesses in the Russian Federation”

. It defines the criteria for classifying organizations as small and medium-sized businesses, including: the total share of participation of the state and large businesses (up to 25%); average annual number of employees (up to 250 people); the amount of annual revenue (no more than one billion rubles) and the book value of assets.

How to sign documents correctly

Its data must be contained in the state register (Unified State Register of Legal Entities or Unified State Register of Individual Entrepreneurs).

IMPORTANT INFORMATION! If, when registering an enterprise, the manager gives the right to sign without a power of attorney along with himself to another person or persons, this information is also entered into the register.

An individual entrepreneur who has the right to perform the functions of a chief accountant can put his signature not only on documents requiring a director’s visa, but also sign in the “chief accountant” column, for example, on a bill of lading.

A power of attorney is a written document that delegates certain powers.

In our case, this is the transfer of the right to sign. This can only be issued by a person who has this right unconditionally according to the constituent data, that is, most often, a representative of the management.

Who should sign a certificate of income for 3 months of the general director if he himself is the chief accountant?

The sole executive body of the company may also be elected not from among its participants.

An agreement between the company and the person carrying out the activities is signed on behalf of the company by the person who chaired the general meeting of the company's participants, at which the person performing the functions of the sole executive body of the company was elected, or by a company participant authorized by the decision of the general meeting of the company's participants, or, if the resolution of these issues is within the competence of the board of directors (supervisory board) of the company, the chairman of the board of directors (supervisory board) of the company or a person authorized by a decision of the board of directors (supervisory board) of the company.

2. Only an individual can act as the sole executive body of a company, except for the case provided for in Article 42 of this Federal Law.

3.

Order on assigning the duties of chief accountant to the director

According to the staff of any LLC, two main positions are a priori defined: director and chief accountant.

It should be noted that sometimes the transfer of responsibilities occurs during the period of active activity of the organization: this is not prohibited by law and this procedure does not require any special explanation. After the order is issued, full responsibility for the financial part of the enterprise’s work, including submission of reports, calculations, payment of taxes, etc.

falls on the director. The right to sign payment documents is automatically transferred to him.

When entrusting the function of chief accountant to a director, no additional entries need to be made either in the manager’s personal file or in his work book. There is no need to conclude an additional agreement to the employment contract.

Any employee of the enterprise who has the necessary knowledge and skills can directly formulate the order.

How to obtain the signature of the chief accountant if he is not on the company’s staff

There are a number of nuances here that are undoubtedly worth paying attention to.

This will allow you to avoid being held accountable for violating the rules for accounting for the organization’s income and expenses (due to the signing of primary documents by unauthorized persons and the subsequent possible recognition by tax authorities of the organization’s expenses based on these primary documents as unfounded and unconfirmed). After all, according to the provisions of Art. 120 of the Tax Code of the Russian Federation, the fine imposed on an organization for this violation can range from 10,000 to 40,000 rubles and more, depending on the specific type of violation.

In addition, in accordance with paragraph 4 of Art. 108 of the Tax Code of the Russian Federation, if an organization is brought to justice, its officials, if there are necessary grounds, are not exempt from administrative, criminal and other liability for violations committed.

When the CEO becomes the chief accountant

In other words, combining positions by the general director is not allowed. However, by the ruling of the Cassation Board of the Supreme Court of the Russian Federation dated March 25, 2003

Source: https://domprava76.ru/esli-buhgalter-i-direktor-v-odnom-lice-kak-podpisyvat-spravki-81741/

Order on the right to sign primary documents - sample

The procedure for granting signature rights First of all, the management of the enterprise identifies employees who, due to their line of work, constantly encounter various types of documents. Then it is decided how to grant them the right to sign.

We draw up an order for the right to sign primary documents

Office waste also requires a waste passport. Companies whose activities generate waste of hazard class I-IV (for example, unsorted waste from office and household premises of organizations) are required to draw up a waste passport, as well as establish standards for waste generation and limits on their disposal.

For example, is it necessary to issue a check if an individual pays for a legal entity and vice versa? When to generate an “expenses” cash receipt?

Order for the right to sign primary documents

In the current legislation there is no rule that imperatively establishes a method for vesting employees with such powers, therefore, in this matter, one should focus on the established customs of document flow, according to which the authority to sign can be transferred:

- by approving the relevant order;

- using a power of attorney to sign the primary document.

The principle of distinguishing between these two approaches is that the effect of the order applies only to the employees of the organization, while the power of attorney applies to any persons specified in the paper. The preparation of these documents is regulated by different sources of law - in the first case, this is the Labor Code of the Russian Federation, and in the second, the Civil Code.

Order for the right to sign

Individual entrepreneurs should not rush to pay 1% contributions for 2021. Firstly, because from this year the deadline for paying such contributions has been postponed from April 1 to July 1. Accordingly, 1% contributions for 2021 must be transferred to the budget no later than 07/02/2021 (July 1 - Sunday).

The transition from one Federal Tax Service Inspectorate to another will not require mandatory reconciliation. The Tax Service has updated the regulations for organizing work with payers of taxes, fees, insurance contributions for compulsory pension insurance, as well as tax agents. The amendments concern activities that are mandatory when a taxpayer transfers from one Federal Tax Service Inspectorate to another.

Required signatures in the UPD

Issued upon completion of the fact or after the completion of the transaction. orders for the right to sign financial documents Financial papers show solvency and profitability. In this sense, the balance is informative. It reflects the financial position at the end of the period.

By looking at the balance sheet, a specialist can easily determine whether the counterparty has sources of funds, property, or only debts and obligations. Other financial papers: consolidated income statement, statement of funds and their use. Loans and credit agreements can also be classified as financial securities.

order on the right to sign invoices An invoice is proof of the completed shipment of goods or provision of services. The cost is also indicated.

The choice between two regulatory sources depends on the goals pursued by the manager: if it is assumed that it will be necessary to sign internal corporate documentation, then the optimal solution is to issue an order.

If you plan to sign and transfer papers outside the company (for example, cover letters for the shipment of goods or invoices), then it is preferable to choose a power of attorney.

For security purposes and protection of trade secrets, many are afraid to transfer such serious powers to third parties who are not employees of the company, so the practice of orders is the most common. However, in cases where the manager intends to entrust an employee with a number of small tasks and is not ready to give him the right to sign in a global sense, then he can also issue a power of attorney for him.

Source: https://jurist-company.com/prikaz-na-pravo-podpisi-upd-direktora-za-glavnogo-buhgaltera/

How is the “signature” requisite completed?

It would seem that what could be simpler - to put your signature? Meanwhile, this is as serious a requisite as the name of the organization and its banking attributes. Therefore, the correctness of its execution must coincide with the requirements for office work.

Signature elements

The signature as a prop consists of three parts.

- The title of the position must be indicated in full in accordance with the staffing table. If the signature is not on official letterhead, then the name of the organization must be added to the title of the position. It is written with a capital letter. This element is located on the left edge of the document.

- A personal signature is what is commonly called a painting. There are no special requirements for it: it can be either a stroke or a surname with one or more initials. According to unspoken rules, at least one letter from the first name and three from the surname must be clear from the stroke.

- Deciphering the signature – initials and surname. It must completely match the passport data, down to the dots in the letter e, if they are present on the identity card. Placed at the level of the last line of the signature.

Signature location

The signature is inseparable from the text of the document. If the text ends at the bottom of the page, then the signature cannot be transferred to a separate sheet if there is no other text on the sheet besides it. It is customary to move at least the last paragraph, but do not forget about the correct page numbering.

If several signatures are provided, then they are located one below the other in descending order of the nomenclature importance of the positions.

FOR YOUR INFORMATION! If members of the commission sign, then it is necessary to indicate not their actual positions, but their role in the commission (“Chairman”, “Member of the commission”). But they need to be arranged in order of subordination.

IOF or Full Name?

The order of placement of initials - before or after the surname - is determined by Decree of the State Standard of the Russian Federation dated 03.03.2003 N 65-st and the Unified System of Organizational and Administrative Documentation “Requirements for the preparation of documents. GOST R 6.30-2003".

According to these regulations, initials are placed after the surname in the following cases:

- when addressing a document to an individual (for example, A.P. Koroleva);

- when declaring or imposing a resolution when specifying the executor (for example, “The order is entrusted to I.I. Romanov”).

If the signature is a requisite, then the initials are placed before the surname. There is a dot after the initials; they are not separated from the surname by a space.

Stamp on signature

The use of a seal is not mandatory for some forms of business activity, for example, for individual entrepreneurs. But for most documents, the presence of a seal will certify their authenticity. Its use is subject to mandatory requirements that must be observed.

- A seal cannot be placed before a signature, especially on a blank sheet of paper.

- If the document is drawn up on a special form, then the seal is placed in the place provided for this purpose, imprinted with the letters M.P. (“place of printing”).

- In other cases, the seal is placed next to the signature; it is allowed (but not required) to overlap part of the personal signature with the edge of the seal. The stroke cannot be completely covered up, since its authenticity must be verifiable.

Does the chief accountant have the right to sign documents for the director?

Info It’s very simple, change the signatures on the bank card to the person he has identified, he must first issue an order)) If he is not afraid to take risks, that’s his problem.)) Write a power of attorney.

An order, but a lot of nuances. If the CEO is the founder and what if not? here’s a question right away, because the second signature in some organizations is decided only by meetings of the founders. Well, what’s the point, the right to sign will be transferred, but the general will still be responsible. The right to sign does not always entail responsibility.

But the general director, even without a signature, cannot always avoid responsibility, and besides, according to the law, he has FULL responsibility. And responsibility for a “wrong” signature does not necessarily arise with the signatory.

With such success, you can issue an order on the right of the cleaner to sign financial documents.

To do this, you need to have an order appointing a person responsible for signing. The main thing is that they contain information about to whom the right to sign is transferred, and sample signatures of these employees.

Order for the right to sign the managing director for the chief accountant

→ → Update: June 7, 2021

Every day in their work, the chief accountant and the head of an organization are faced with the fact that they need to sign a large number of different documents: supply agreements, primary documentation, employment contracts or other financial documents.

But what to do if an employee gets sick, goes on vacation or is on a long business trip? A sample order on the right to sign primary documents with an example of completion in this article will solve this problem. In accordance with the legislative acts of the Russian Federation, there is a concept of the first and second signature.

The first signature always belongs to the head of the organization, the second signature belongs to the financial director or chief accountant of the company. The situation becomes more complicated if the first and second signatures belong to the same person, when the manager has assigned himself the duties of an accountant, which often happens in small enterprises.

Reasons why a manager can delegate powers and issue an order on the right to sign primary documents:

- The person in charge of the organization is on vacation, on sick leave, or on a long business trip;

- The organization’s work schedule does not coincide with the work schedule of the company’s top officials, for example, a wholesale warehouse is open 24 hours a day, seven days a week, but the manager has a different work schedule;

- The organization's document flow has too large a volume of incoming and outgoing documents; it is unrealistic for one person to cope with such a quantity.

It is impossible to prepare documents without the signature of the organization's top officials. In such cases or under other circumstances, an order is issued on the right to sign primary documents indicating the full list of persons who have the right to sign for the head of the company or chief accountant.

The right of first signature cannot be transferred to the chief accountant or other person who has the right of second signature on financial and other documents.

The right to sign financial or other documents can only be transferred to an employee of the organization, and since the organization’s staffing may change, it is advisable to draw up an order annually.

It is worth noting that this order does not apply to bank documents, for example, a checkbook, since the right to sign is limited to the circle of persons specified in the bank card of the organization’s sample signatures and cannot be transferred to other persons.

The mandatory points of the order are:

- Full names of employees;

- The position of the person who is trusted to sign documents;

- Deadline for granting signature rights;

- Sheet with sample signatures of principals and proxies.

If the head of an organization has concerns that employees may harm the company and sign “something wrong,” a list of documents is drawn up.

In normal financial and economic activities of an organization, it is advisable to transfer the right of signature to the manager and chief accountant for the following series of documents:

- Certificate of completion;

- Consignment note for shipment or acceptance of goods and materials;

- Invoice;

- Cashier-operator's journal, cash documents;

- Standard supply contracts concluded with buyers;

- Power of attorney for receiving inventory items.

There is a common misconception that there is no need to create any orders, it is easier to order a stamp and put a facsimile everywhere, but a facsimile signature can be used if it is expressly provided for by law or by agreement of the parties to the transaction.

If you want to avoid disagreements with tax inspectors, you should not sign documents with a facsimile signature.

Subscribe to our channel at

Order on granting the right to sign - we draw it up correctly

However, such operations entail increased responsibility for the employee, as they can cause serious damage to the organization. It is necessary that the employee has sufficient qualifications and that the new powers correspond to his job description. Subscribe to our channel on Telegram We will tell you about the latest news and publications.

Read us wherever it is convenient for you. Always be aware of the main thing! e-mail newsletter Subscribe to news for HR specialists! Once a week we will send the most important articles to your email Subscribe Dear readers, if you see an error or typo, help us fix it!

To do this, highlight the error and press the “Ctrl” and “Enter” keys simultaneously. We will learn about the inaccuracy and correct it.

Yeah, well, yes, the right to sign when signing contracts.

The right of the General Director to sign for the Chief Accountant

- when may it be necessary to transfer such powers and what will need to be formalized so that the director’s signature for the chief accountant has legal force?

We will talk about this in our article.

If the director, upon taking office, indicated in the order that he takes over the accounting, it is not necessary to issue orders or powers of attorney specifically for the right to sign for the chief accountant, since:

Source: https://civilyur.ru/prikaz-na-pravo-podpisi-upd-direktora-za-glavnogo-buhgaltera-92947/

Who should sign the document if the director is absent?

If the person with the absolute right to sign is for any reason absent from his/her workplace at the time the signature is required, this option should be provided in advance. There are several ways to resolve this situation:

- Provide in the constituent documents the possibility of signature for the deputy director or other official.

- Issue a power of attorney for signature by an authorized person (you can do this immediately for a long period, for example, for a year).

- Issue an order or instruction for the right to sign a specific document (one-time option).

- Use a facsimile version of the signature in cases where this does not contradict the law.

Signed by I.O.

If the document is signed by the acting director or his deputy, the right to sign is delegated to him on the basis of the above documents. At the same time, there is no need to indicate “acting” in the signature itself; according to GOST rules, only the name of the position is required, which for the employee who temporarily assumed management responsibilities remained the same. This must be indicated when the document is endorsed. It is also unacceptable to use a slash and the use of the preposition “for” before the signature.

IMPORTANT INFORMATION! Documents signed by the acting official in violation of the design of this detail (with the letters “i.o”, slash or preposition “for”) cannot be notarized, they can be challenged in court.

In the place of the director - the signature of the acting director

If on the form the position of director is in the place intended for signature, and the person signing is acting, then you need to cross out the printed phrase and enter the name of the real position of the signatory. The same should be done if the surname and initials of the absent manager are printed. Corrections are made in handwritten form.

What cannot be a facsimile?

An imprint of a sample signature, which is so easy to give to any employee and therefore very convenient to use, cannot be left on all documents. Legal grounds prohibit placing such a signature, which does not require the “live” participation of an authorized person, on the following documents:

- related to bank payments;

- various statements;

- personnel papers;

- declarations;

- invoices;

- cash documents;

- contracts that need to be registered;

- powers of attorney.

You can leave a facsimile signature when exchanging documents within the framework of one contract if:

- a contract signed in the usual way provides for this possibility;

- There is an agreement between the partners on the use of facsimile clichés.

Such papers can be commercial offers, letters, acts, specifications, etc.

Order

It applies only to those persons who work in the company and receive the right to certify strictly internal corporate documents.

After drawing up the decree, the director must certify the signatures of the employees indicated in it with his autograph. The duration of the order is determined on an individual basis: an order for the right to sign primary documents can be of an indefinite nature, or can be drawn up for a specific period, depending on the situation within the company.

Regardless of whether an administrative act will be drawn up or the manager will give his preference to a power of attorney, the form must indicate:

- personal data of the authorized person;

- names of papers that it will be able to sign;

- If a power of attorney is issued, its validity period should be additionally indicated.