Let's get acquainted with the balance sheet items for 2021: their codes and explanations

Everyone who has ever held a balance sheet in their hands, much less drawn it up, paid attention to the “Code” column.

Thanks to this column, statistical authorities are able to systematize the information contained in the balance sheets of all companies. Therefore, it is necessary to indicate codes in the balance sheet only when this report is submitted to state statistics bodies and other executive authorities (Article 18 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ, clause 5 of the order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n). Let us remind you that only organizations whose reports contain information classified as state secrets, as well as in cases established by the Government of the Russian Federation, need to submit their balance sheet for 2021 to the statistics. Other companies do not need to submit a balance sheet.

If the balance is not annual and is needed only by owners or other users, it is not necessary to indicate the codes.

ATTENTION! From 2021, financial statements will be submitted exclusively in electronic form. Paper forms will no longer be accepted. Read more about changes to the rules for presenting financial statements here.

From 06/01/2019, the balance sheet form is valid as amended by Order of the Ministry of Finance dated 04/19/2019 No. 61n.

The key changes in it (as well as in other financial statements) are as follows:

- now reporting can only be prepared in thousand rubles, millions can no longer be used as a unit of measurement;

- OKVED in the header has been replaced by OKVED 2;

- The balance sheet must contain information about the audit organization (auditor).

The auditor mark should only be given to those companies that are subject to mandatory audit. Tax authorities will use it both to impose a fine on the organization itself if it ignored the obligation to undergo an audit, and in order to know from which auditor they can request information on the organization in accordance with Art. 93 Tax Code of the Russian Federation.

What negative consequences are possible if the auditor’s report is not yet ready at the time of reporting, find out from a typical situation from ConsultantPlus. If you do not have access to the K+ system, get a trial online access for free.

In the balance sheet, line codes from 2014 must correspond to the codes specified in Appendix 4 to Order No. 66n. At the same time, outdated codes from the expired order No. 67n with the same name, dated July 22, 2003, are no longer applied.

It is not difficult to distinguish previously used codes from modern ones - by the number of digits: modern codes are 4-digit (for example, lines 1230, 1170 of the balance sheet), while outdated ones contained only 3 digits (for example, 700, 140).

For information on what the form of the current balance sheet with line codes looks like, read the article “Filling out Form 1 of the balance sheet (sample)” .

Assignment of codes and numbers

Codes for certain lines must be indicated in a certain column. It is worth noting that codes are needed mainly so that statistical authorities can combine information presented in different types of balance sheets into one whole. The codes are mandatory to fill out when the balance sheet being compiled must be transferred to state executive structures with further use of information on them.

In a situation where the balance sheet is prepared for a quarter or other reporting period, in order for it to be considered at internal meetings for the purpose of introducing the state of affairs or analyzing the company’s activities, it is not necessary to fill in the code lines, since they do not carry any responsibility in this case no functions.

Line coding is performed only if this reporting documentation is submitted to government agencies and is not an obligation for the internal preparation of reporting balances. Since financial statements are submitted to the tax authorities only once a year, the coding applies only to annual balance sheets.

Useful video about filling out your balance from scratch:

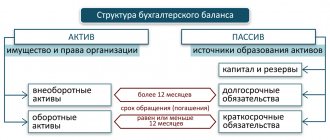

How to decipher balance sheet asset lines

Before deciphering an asset item, let’s consider its code - it carries certain information. So, the first digit shows that this line refers to the balance sheet (and not to another accounting report); 2nd - indicates the section of the asset (for example, 1 - non-current assets, etc.); The 3rd digit reflects assets in increasing order of their liquidity. The last digit of the code (initially it is 0) is intended to help in line-by-line detailing of indicators considered significant - this allows you to fulfill the requirement of PBU 4/99 (clause 11).

NOTE! The requirement for detail may not be fulfilled by small businesses (clause 6 of Order No. 66n).

Read about what distinguishes accounting carried out by small businesses in the material “Features of accounting in small enterprises” .

The asset lines of the balance sheet with codes and explanations are shown in the table:

| Line name | Code | Decoding the string | |

| By order No. 66n | By order No. 67n | ||

| Fixed assets | 1100 | 190 | The total amount of non-current assets is reflected |

| Intangible assets | 1110 | 110 | The information reflected in lines 1110–1170 is explained in the notes to the statements (information on the availability of assets at the reporting dates and changes for the period is disclosed) |

| Fixed assets | 1150 | 120 | |

| Profitable investments in material assets | 1160 | 135 | |

| Financial investments | 1170 | 140 | |

| Deferred tax assets | 1180 | 145 | The debit balance of account 09 is indicated |

| Other noncurrent assets | 1190 | 150 | Filled in if there is information about non-current assets that are not reflected in the previous lines |

| Current assets | 1200 | 290 | The final result of current assets is determined |

| Reserves | 1210 | 210 | The total balance of inventories is given (debit balance of accounts 10, 11, 15, 16, 20, 21, 23, 28, 29, 41, 43, 44, 45, 97 without taking into account the credit balance of accounts 14, 42) |

| Value added tax on purchased assets | 1220 | 220 | Indicate account balance 19 |

| Accounts receivable | 1230 | 240 | The result of adding the debit balances of accounts 60, 62, 68, 69, 70, 71, 73, 75, 76 minus account 63 is reflected |

| Financial investments (excluding cash equivalents) | 1240 | 250 | The debit balance of accounts 55, 58, 73 (minus account 59) is given - information on financial investments with a circulation period of no more than a year |

| Cash and cash equivalents | 1250 | 260 | The line contains the balance of accounts 50, 51, 52, 55, 57, 58 and 76 (in terms of cash equivalents) |

| Other current assets | 1260 | 270 | Filled in if data is available (for the amount of current assets not indicated in other lines of the section) |

| Total assets | 1600 | 300 | Total of all assets |

You can see line-by-line comments on filling out asset lines in the ConsultantPlus system. Get trial access to the K+ system and proceed to the explanations for free.

* * *

So, the balances accumulated on account 20 by the end of the reporting period should be entered into balance sheet line 1210 called “Inventories.” When a certain balance is formed in the “Main Production” account at the end of the reporting period, this indicates a balance of work in progress at the enterprise.

Direct production costs should be recorded on account 20. In addition, at the end of each month, a certain share of expenses from accounts 23, 25, 26 should be attributed to this account.

The accounting policy should be formulated so that this document provides a criterion for distinguishing direct costs from indirect ones, principles for assessing oil refineries, and methods for closing the account of indirect costs.

Care must be taken to ensure that work in progress is recorded correctly, since such data is entered into the balance sheet and, if incorrectly calculated, can significantly distort the financial performance of the organization.

Similar articles

- Direct material costs

- Accounting for costs of auxiliary production

- Production costs

- Direct and indirect production costs

- Finished products are reflected in the balance sheet...

Interpretation of individual balance sheet liability indicators

Liability codes are also 4-digit: the 1st digit is the line’s belonging to the balance sheet, the 2nd is the number of the liability section (for example, 3 is capital and reserves). The next digit of the code reflects obligations in order of increasing urgency of their repayment. The last digit of the code is for detail purposes. Total liabilities in the balance sheet are line 1700 of the balance sheet. In other words, total liabilities in the balance sheet are the sum of lines 1300, 1400, 1500.

Liability items of the balance sheet with codes and explanations are shown in the table:

| Line name | Code | Decoding the string | |

| By order No. 66n | By order No. 67n | ||

| TOTAL capital | 1300 | 490 | The line contains information about the company's capital as of the reporting date |

| Authorized capital (share capital, authorized capital, contributions of partners) | 1310 | 410 | Information on lines 1300–1370 is detailed in the statement of changes in equity and the statement of financial results (in terms of net profit for the reporting period). The company has the right to determine the additional amount of explanations about capital. |

| Revaluation of non-current assets | 1340 | 420 | |

| Additional capital (without revaluation) | 1350 | ||

| Reserve capital | 1360 | 430 | |

| Retained earnings (uncovered loss) | 1370 | 470 | |

| Long-term borrowed funds | 1410 | 510 | The information is deciphered in tabular (Form 5) or text form in the explanations to the balance sheet |

| Deferred tax liabilities | 1420 | — | Indicate the credit balance of account 77 |

| Estimated liabilities | 1430 | — | The credit balance of account 96 is reflected - estimated liabilities, the expected fulfillment period of which exceeds 12 months |

| Other long-term liabilities | 1450 | 520 | Provides information about long-term liabilities not indicated in the previous lines of the section |

| TOTAL long-term liabilities | 1400 | 590 | The final result of long-term liabilities is reflected |

| Short-term debt obligations | 1510 | 610 | Account credit balance 66 |

| Short-term accounts payable | 1520 | 620 | The total credit balance of accounts 60, 62, 68, 69, 70, 71, 73, 75, 76 is reflected. The information is deciphered in the notes to the balance sheet (for example, in Form 5) |

| Other current liabilities | 1550 | 660 | Filled in if not all short-term liabilities are reflected in other lines of the section |

| Total current liabilities | 1500 | 690 | The total total of short-term liabilities is indicated |

| Liabilities of everything | 1700 | 700 | Summary of all liabilities |

ConsultantPlus experts have prepared a line-by-line commentary on filling out the balance sheet, including liability lines. If you don't have access to K+, get it for free.

Read about what characterizes simplified accounting in the article “Simplified reporting for small businesses.”

Main production in the balance sheet line

This section shows the formed funds and reserves of the organization, the amount of profit or loss of the reporting year and previous years, target income and income of future periods. A decrease or increase in the authorized capital must be reflected in the constituent documents of the organization.

It should be borne in mind that the data in this line are subtracted when calculating the results for Section III of the balance sheet. Line 440 “Profit (loss) of the reporting period” shows the financial result obtained by the organization for the reporting period and accounted for in account 99 “Profits and losses”. The amount of loss is shown in this line with a minus sign.

Taxpayers are given the right to independently determine in their accounting policies for profit tax purposes a list of direct expenses associated with production and sales.

This also includes products or components that did not pass quality control or were rejected by the customer.

Work in progress in the balance sheet is reflected as a debit balance in the following accounts:

- Account 20 “Main production”;

- Account 23 “Auxiliary production”;

- Account 29 “Servicing industries and farms”;

- Account 44 “Sales expenses”;

- Account 46 “Completed stages of unfinished work.”

If at the end of the reporting period there are balances on the above accounts, then this is work in progress.

It is worth keeping in mind that Account 20 can only be applied if the production process is not divided into separate stages (phases).

The item relating to work in progress is classified as inventory. Accordingly, all kinds of data related to this category will be reflected in line number 1210, reserved for the item - reserves. In addition, in some cases, work in progress is not entered as a separate line if we are talking about a simplified reporting form.

https://www..com/watch?v=WO-EIElrn-c

Account 26 can be distributed similarly to account 25 (then the full cost will be collected on the corresponding accounts), or you can write off the entire amount collected on it every month to the financial result (to the debit of account 90). In the latter case, the cost of a specific product (work, service) will not include its data.

Composition of main production costs

Account 20 is used to account for direct and indirect expenses incurred in connection with:

- with the production of products of any kind;

- provision of all types of services;

- performing construction and contracting, design, survey and geological exploration work;

- carrying out repair work;

- carrying out design and research work, etc.

The main production on the balance sheet is

Read more about the structure of the balance sheet in the article “Balance sheet (assets and liabilities, sections, types).”

You will find information on the procedure for filling out a balance sheet in the material “Preparing a balance sheet.”

You will learn how to fill out a balance sheet for “simplified” people by reading the material “How to fill out a balance sheet under the simplified tax system?”

Work in progress: accounting account

Costs in work in progress are taken into account in production cost accounts: 20 “Main production”, 23 “Auxiliary production”, 29 “Service production and facilities”.

The main production on the balance sheet is an asset or liability

They did not go through all the necessary phases, were not fully staffed, or simply did not pass the suitability test.

The group of such goods includes:

- Materials and raw materials, work with which has already begun, but they do not yet constitute a finished product, but are in the process of processing or assembly;

- Products not yet assembled;

- Products that have not passed the required quality and safety tests;

- Work completed but awaiting customer approval.

How is work in progress reflected in the accounting accounts?

Account 20 “The main production accumulates all the main costs. Its use is approved by the “Instructions for the use of the chart of accounts.”

All expenses, both direct and indirect, as well as expenses of other workshops that relate to this product are transferred to its debit.

Results

Decoding the balance sheet allows users to extract as much useful information as possible from its meager figures. For automated processing of data from accounting reports carried out by statistical authorities, accounting lines are encoded.

Sources:

- Federal Law of December 6, 2011 N 402-FZ “On Accounting”

- Order of the Ministry of Finance of Russia dated July 2, 2010 N 66n

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Formation of the balance of work in progress

The actual cost of manufactured products (works, services) is written off from the credit of the “Main production” account. In this case, account 20, depending on the adopted accounting policy, corresponds with accounts 40, 43, 90.

The balance of account 20 remaining at the end of the month reflects the value of the main work in progress (WIP).

Balances on accounts 23 “Auxiliary production” and 29 “Service farms” are formed in a similar way. Accordingly, the balance on account 23 shows the cost of auxiliary work in progress, and the balance on account 29 shows the cost of work in progress at service farms.

The balance of work in progress in accounts 20, 23, 29 is the balance of work in progress in accounting for the organization as a whole. Work in progress - account 20 + account 23 + account 29, not closed at the end of the reporting period - the balances on them are summed up with other data entered in the “Inventories” line in the balance sheet.

The procedure for filling out a balance with a breakdown of accounts is discussed in detail in the Guide from ConsultantPlus. Get free trial access to the system and study the material.

Does not apply to work in progress:

- raw materials, supplies, purchased finished products transferred to workshops (sites), but not processed;

- rejected semi-finished products that cannot be corrected.

Read about the entries that arise when accounting for irreparable defects in the article “Accounting for defects in production - accounting entries.”