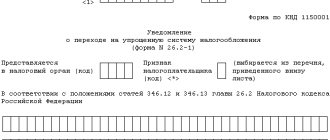

Notification of transition to simplified

Before switching to the simplified tax system, submit a notification about the transition to the simplified tax system to the tax office where the organization is registered. This is stated in paragraph 1 of Article 346.13 of the Tax Code of the Russian Federation. The recommended form of notification was approved by order of the Federal Tax Service of Russia dated November 2, 2012 No. ММВ-7-3/829.

As a general rule, the inspection must be notified no later than December 31 of the year preceding the year from which the organization will apply the simplification. The notification must indicate:

- selected object of taxation;

- residual value of fixed assets;

- the amount of income as of October 1 of the year preceding the year in which the simplified tax system began to be applied.

This procedure is provided for in paragraph 1 of Article 346.13 of the Tax Code of the Russian Federation.

Organizations that have not notified the tax inspectorate of the decision to switch from the general tax system to the simplified tax system within the prescribed period do not have the right to apply this special regime (subclause 19, clause 3, article 346.12 of the Tax Code of the Russian Federation).

Where to enter information on restored VAT when switching to the simplified tax system

The answer to this question is contained in clause 14 of the rules for maintaining a sales book (Appendix 5 to Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137). There are also corresponding clarifications from the Ministry of Finance in letter dated November 16, 2006 No. 03-04-09/22 and the Federal Tax Service in letter dated September 20, 2016 No. SD-4-3 / [email protected] , which contain recommendations for filling out the purchase book and sales book.

Important! Recommendation from ConsultantPlus Register the invoice on the basis of which you accepted VAT for deduction in the sales book for the amount that needs to be restored (clause 14 of the Rules for maintaining the sales book). If the established storage period for the invoice has expired and you do not have it, register... (for more details, see K+).

In the VAT return, the restored tax is reflected in line 080 of section 3 with a breakdown in section 9 for each operation. If VAT is restored on a property, then for the year in the 4th quarter declaration it is necessary to fill out Appendix 1 to Section 3.

What VAT transaction codes are indicated in the declaration and accounting registers, read in this article.

How to fill out and submit a VAT return, read the materials in our special section, which is dedicated to VAT reporting.

Tax base of the transition period

Before starting the transition to the simplified tax system, it is necessary to create a tax base for the transition period. The procedure for determining it depends on how the organization calculated income tax:

- accrual method;

- cash method.

Special rules for the formation of the tax base of the transition period are established only for organizations that determined income and expenses using the accrual method. This follows from the provisions of paragraph 1 of Article 346.25 of the Tax Code of the Russian Federation.

Income

Such organizations must include unclosed advances received during the period of application of the general taxation system as part of “transitional” income. This is explained by the fact that under the accrual method, income must be reflected on the date of sale of goods (work, services). The date of payment does not affect the amount of income (clause 3 of Article 271 of the Tax Code of the Russian Federation). When simplified, the cash method applies. With it, income is generated as payment is received, regardless of the date of sale of goods (work, services) on account of which it was received. Such rules are provided for in paragraph 1 of Article 346.17 of the Tax Code of the Russian Federation.

Advances received for upcoming supplies during the period of application of the general taxation system should be included in the single tax base as of January 1 of the year in which the organization begins to apply the simplification (subclause 1, clause 1, article 346.25 of the Tax Code of the Russian Federation). At the same time, take into account the specifics of calculating and paying VAT received as part of advances.

In the future, advances received before the transition to the simplified tax regime must be taken into account when determining the maximum amount of revenue that limits the use of the special regime. This follows from the provisions of paragraph 4.1 of Article 346.13 and subparagraph 1 of paragraph 1 of Article 346.25 of the Tax Code of the Russian Federation.

In 2021, the maximum amount of revenue that allows the application of the simplification, taking into account the deflator coefficient, is RUB 79,740,000. (RUB 60,000,000 × 1.329) (clauses 4 and 4.1 of Article 346.13 of the Tax Code of the Russian Federation).

An example of accounting for advances received by an organization before the transition to a simplified tax system

Alpha LLC is engaged in wholesale trade. In 2015, the organization applied a general tax system; from January 1, 2016, it switched to a simplified system. As of the date of transition, Alpha's accounting reflected unclosed advances received for upcoming deliveries in the total amount of RUB 7,000,000. (without VAT).

In 2021, the organization’s current account received revenue in the amount of RUB 60,000,000, including:

- in the first quarter – 16,000,000 rubles;

- in the second quarter - 20,000,000 rubles;

- in the third quarter – 10,000,000 rubles;

- in the fourth quarter – 14,000,000 rubles.

In 2021, Alpha's accountant determines the income limit that allows the application of the simplified tax regime, in accordance with paragraphs 4 and 4.1 of Article 346.13 of the Tax Code of the Russian Federation. That is, it focuses on the figure of 79,740,000 rubles.

Taking into account the advances of the transition period, Alpha’s income amounted to:

- according to the results of the first quarter - 23,000,000 rubles. (RUB 7,000,000 + RUB 16,000,000);

- at the end of the half year - 43,000,000 rubles. (RUB 23,000,000 + RUB 20,000,000);

- based on the results of nine months - 53,000,000 rubles. (RUB 43,000,000 + RUB 10,000,000);

- at the end of the year - 67,000,000 rubles. (RUB 53,000,000 + RUB 14,000,000).

Thus, throughout the year, Alpha complied with the established income limit and retained the right to apply the simplified procedure.

Receivables from buyers, which have accumulated during the application of the general taxation system, do not increase the tax base of the transition period. With the accrual method, revenue is included in income as it is shipped (Clause 1, Article 271 of the Tax Code of the Russian Federation). Consequently, once it was already taken into account for tax purposes. Amounts received to pay off accounts receivable after the transition to the simplified tax system do not need to be re-included in the tax base. This follows from subparagraph 3 of paragraph 1 of Article 346.25 of the Tax Code of the Russian Federation.

An example of accounting for amounts received in repayment of receivables that arose during the period of application of the general taxation system. The organization applies simplification. Before the transition to the simplified system, the organization calculated income tax using the accrual method

Under the terms of the agreement, the buyer pays for the equipment supplied by Alfa LLC in two stages:

- 50 percent – prepayment upon signing the contract in November 2015;

- 50 percent – within 15 days after completion of installation and testing of equipment.

The cost of the equipment is 260,000 rubles. (without VAT).

The acceptance certificate for installed and tested equipment was signed on December 31, 2015. In 2015, Alpha calculated income tax using the accrual method. In December 2015, the organization’s accountant included all proceeds from the sale of equipment (RUB 260,000) as income. From January 1, 2021, Alpha switched to a simplified system. On January 14, the second part of the payment for the equipment (RUB 130,000) was received into the organization’s bank account. When calculating the single tax for the first quarter of 2021, Alpha’s accountant did not take this amount into account as income.

No VAT recovery required for work performed (services provided)

Quite often, a company that has switched from a general taxation system to a simplified one faces the following situation: work or services were paid for and taken into account during the period of application of the simplified taxation system, but continue to be partially used under the simplified taxation system (for example, repairs of industrial premises).

According to the author, this fact is not a reason for reinstating VAT. After all, as a rule, work (services) are performed, paid for, accepted, and also mainly used during the period of application of the OSN. At the same time, the legislation does not stipulate the procedure for recovering VAT amounts for work and services used both in carrying out activities on the special tax system, and in the future when applying the simplified tax system (constant.

FAS SZO dated 04.06.2013 No. F07-1913/13 (by the decision of the Supreme Arbitration Court of the Russian Federation dated 10.10.2013 No. VAS-13490/13, the review of the case was denied)).

Expenses

Organizations that used the accrual method must include unrecognized expenses paid during the period of application of the general tax system as part of the “transition” expenses. This is explained by the fact that with the accrual method, expenses are taken into account on the date of their implementation (clause 1 of Article 272 of the Tax Code of the Russian Federation). The date of payment does not affect the date of recognition of expenses. When simplified, the cash method applies (clause 2 of Article 346.17 of the Tax Code of the Russian Federation). With it, expenses are formed as they are paid. Moreover, additional conditions have been established for the recognition of certain types of costs.

Advances issued during the period of application of the general taxation system against future deliveries (excluding VAT) should be included in the single tax base on the date of receipt of goods (work, services). At the same time, take into account the restrictions associated with the write-off of purchased goods and fixed assets. Include paid but unrecognized expenses as expenses as the conditions under which they reduce the tax base for the single tax are met. Such rules are provided for in subparagraph 4 of paragraph 1 of Article 346.25 of the Tax Code of the Russian Federation.

Situation: is it possible for an organization to take into account rental costs in a simplified manner? The rent was paid in advance for several years in advance during the period of application of OSNO (before the transition to the special regime) /

Yes, you can.

Expenses for renting an office, which the organization paid using the accrual method, are taken into account when calculating the single tax on the date of their implementation (subclause 4, clause 1, article 346.25 of the Tax Code of the Russian Federation). Reduce the tax base monthly as you actually receive services under the lease agreement. A similar point of view is reflected in the letter of the Ministry of Finance of Russia dated November 14, 2005 No. 03-11-04/2/132.

An example of accounting for rental expenses paid before the transition to the simplified system. The organization pays a single tax on the difference between income and expenses

Alpha LLC rents office space. The lease agreement was concluded for the period from January 1, 2021 to December 31, 2021 inclusive (24 months). The amount of rent for the entire term of the contract is 480,000 rubles.

In December 2015, Alpha applied the general taxation system and calculated income tax on an accrual basis. This month, the organization transferred the entire amount of rent for two years in advance to the landlord.

Since January 2021, Alpha has switched to a simplified version. The object of taxation is “income reduced by the amount of expenses.”

Starting from January 2021, the organization's accountant monthly reduces the tax base for the single tax by the amount of rent in the amount of: 480,000 rubles. : 24 months = 20,000 rub.

Accounts payable for expenses that were taken into account when calculating income tax do not reduce the tax base for the single tax. Amounts paid to repay this debt after the transition to the simplified system cannot be re-included in expenses. For example, if unpaid goods were sold before the transition to the simplified system, then there is no need to take their cost into account when calculating the single tax after payment. This follows from subparagraph 5 of paragraph 1 of Article 346.25 of the Tax Code of the Russian Federation.

Situation: is it possible for an organization to take into account in a simplified manner the income tax and VAT accrued for the period in which the organization applied OSNO? Taxes were transferred to the budget after the transition to simplified taxation.

No you can not.

Any expenses named in paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation can be recognized only if they meet the criteria specified in paragraph 1 of Article 252 of the Tax Code of the Russian Federation (Clause 2 of Article 346.16 of the Tax Code of the Russian Federation). That is, regardless of classification, the expenses specified in paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation reduce the tax base for the single tax if they:

- documented;

- economically justified;

- are associated with activities aimed at generating income;

- are not named in Article 270 of the Tax Code of the Russian Federation.

Payment of income tax and VAT on obligations that arose during the period of application of the general taxation system cannot be recognized as an expense that meets the criteria of paragraph 1 of Article 252 of the Tax Code of the Russian Federation. After the transition to a simplified procedure, this operation is no longer associated with activities aimed at generating income, therefore, it is not economically justified. In addition, amounts of income tax and VAT accrued for payment to the budget cannot be taken into account for taxation due to the provisions of paragraphs 4 and 19 of Article 270 of the Tax Code of the Russian Federation.

Thus, an organization that has switched to a simplified tax system has no reason to reduce the tax base for a single tax by paying taxes accrued during the period of application of the general taxation system. The validity of this conclusion is confirmed by letters from the Ministry of Finance of Russia dated October 16, 2007 No. 03-11-05/251, dated December 19, 2006 No. 03-11-04/2/281.

Transition to the simplified tax system from 2021: procedure, restrictions, advantages

However, the servants of Themis do not support officials in this matter. Take, for example, the Resolution of the AS of the West Siberian District dated May 6, 2021 No. F04-1942/2016, which states: the taxpayer has the right to independently, in the absence of approval from the Federal Tax Service, before the application of the “simplified procedure”, change his decision and remain on the OSN, regardless of causes. The determining factor is the actual conduct of activities in accordance with the tax regime chosen from the beginning of the year.

- on paper (the recommended form is approved by Order of the Federal Tax Service of the Russian Federation dated November 2, 2012 No. ММВ-7-3/ [email protected] ). Let us note that the company has the right to submit a notification in any form, taking into account the requirements of Art. 346.13 Code;

- in electronic form (format approved by Order of the Federal Tax Service of the Russian Federation dated November 16, 2012 No. ММВ-7-6/ [email protected] ).

Let us pay attention to some features of filling out the notification form recommended by the fiscal authorities by an organization switching to the simplified tax system from the general tax regime. In the “Taxpayer Identification” field, enter “3”, and in the line “Switches to a simplified taxation system” - “1”. And do not forget that the amount of income for 9 months of this year is shown without VAT. The general conditions for using the simplified version must also be met. Namely, the enterprise should not have branches, the average number of its employees should not exceed 100 people, and the maximum share of other companies in the authorized capital should be 25 percent.

In addition, banks, insurers, non-state pension funds, pawnshops, government and budget institutions, as well as a number of other organizations are not entitled to operate on the simplified tax system. In practice, there are cases when an organization actually applies a taxation object that is not specified in the notification. The Federal Tax Service will probably consider this unlawful and will recalculate the company’s tax liabilities with all the ensuing consequences. And the judges will most likely agree with the fiscals. For example, in the Resolution of the Sixth AAS dated 01.10.2014 No. 06AP-5107/2014 it is noted: the transition to a simplified regime, the choice of an object of taxation, despite its voluntary nature, is carried out by the payer not arbitrarily, but in compliance with the conditions and procedures clearly specified in Chapter .

26. 2 Tax Code of the Russian Federation. And if an organization, in violation of the established procedure, actually changed the simplified tax system object, it will have to answer for it.

Cash method

For organizations that used the cash method, a special procedure for generating income and expenses when switching to the simplified system has not been developed. This is due to the fact that such organizations previously recognized their income and expenses as they were paid (clauses 2, 3 of Article 273 of the Tax Code of the Russian Federation). Therefore, for them, when switching to simplified language, nothing fundamentally will change.

The only thing you should pay attention to is the procedure for determining the residual value of depreciable property acquired before the transition to the special regime. If the organization paid for such property and put it into operation before the transition to the simplified system, then determine its residual value as follows. From the purchase price (construction, manufacturing, creation), subtract the amount of depreciation accrued during the period of application of the general taxation system. In this case, use tax accounting data (clause 2.1 of Article 346.25 of the Tax Code of the Russian Federation). If, before the transition to the simplification, fixed assets or intangible assets were acquired (constructed, manufactured, created), but not paid for, then reflect their residual value in accounting later: starting from the reporting period in which the payment occurred. As a general rule, the residual value should be determined as the difference between the acquisition price (construction, manufacturing, creation) and the amount of depreciation accrued during the period of application of the general taxation system. However, for organizations that calculated income tax using the cash method, the residual value of such property will be equal to the original one. This is explained by the fact that under the cash method, only fully paid-for property is depreciated. This follows from subparagraph 2 of paragraph 3 of Article 273 of the Tax Code of the Russian Federation.

For more information on writing off expenses for depreciable property taken onto the balance sheet before the transition to the simplified tax system, see How to account for expenses on fixed assets (intangible assets) acquired before the transition to the simplified tax system.

* * *

There will be no problems with the tax inspectorate if the newly minted “simplified” interprets clause 5 of Art. 346.25 of the Tax Code of the Russian Federation literally, namely, it will qualify for the deduction of “advance” VAT only if it is returned to the buyer. To justify the return, the value of contracts concluded before the transition to the simplified tax system should be reviewed. To justify the deduction, you must have documents confirming the return. The organization has the right to pay the amount of VAT for the last quarter preceding the transition to the simplified tax system in accordance with the general procedure. That is, VAT for the fourth quarter of 2021 can be paid in three installments of 1/3 of the total amount of calculated tax: 01/25/2018, 02/26/2018 and 03/26/2018 (taking into account the rule for calculating the period in accordance with clause 7 of article 6.1 Tax Code of the Russian Federation).

VAT: problems and solutions, No. 2, 2021

VAT recovery

When switching to a simplified tax system from the general taxation system, the organization is obliged to restore the amount of input VAT accepted for deduction (clause 3 of Article 170 of the Tax Code of the Russian Federation). The tax must be restored on assets that were acquired before the transition to the special regime, but were not used in transactions subject to VAT. Carry out the restoration according to the accounting in the last tax period preceding the transition (paragraph 5, subparagraph 2, paragraph 3, article 170 of the Tax Code of the Russian Federation).

For unsold goods and unused materials, refund VAT in full. For fixed assets and intangible assets - in an amount proportional to their residual (book) value. This is stated in paragraph 2 of subparagraph 2 of paragraph 3 of Article 170 of the Tax Code of the Russian Federation.

It will not be possible to use the special procedure for VAT recovery provided for in Article 171.1 of the Tax Code of the Russian Federation. In relation to real estate, construction projects and some types of fixed assets, legislation allows the tax to be restored gradually over a long period of time. However, this procedure applies only to VAT payers. It is impossible to be guided by it after the transition to the simplified version (clause 2 of Article 346.11 of the Tax Code of the Russian Federation).

Situation: does the legal successor need to restore input VAT when switching to a simplified system from OSNO? Part of the property on which VAT was previously accepted for deduction by the reorganized organization passes to the legal successor.

Yes need.

The organization is obliged to restore the VAT previously accepted for deduction on the grounds specified in paragraph 3 of Article 170 of the Tax Code of the Russian Federation. In particular, this must be done when using in transactions not subject to VAT, goods, works or services (including fixed assets, intangible assets and property rights) originally acquired for transactions subject to this tax (subclause 2, paragraph. 3, Article 170 of the Tax Code of the Russian Federation).

As a general rule, organizations that use the simplified tax system are not recognized as VAT payers (clause 2 of Article 346.11 of the Tax Code of the Russian Federation). Thus, after the reorganization, the property transferred to the legal successor will be used in activities not subject to VAT. Consequently, the amount of tax on this property, previously accepted for deduction by the reorganized organization, must be restored. The legal successor is obliged to transfer the restored amount of VAT to the budget.

Similar clarifications are contained in letters of the Ministry of Finance of Russia dated July 30, 2010 No. 03-07-11/323, dated November 10, 2009 No. 03-07-11/290 and the Federal Tax Service of Russia dated March 14, 2012 No. ED-4- 3/4270.

Advice: there are arguments that allow a successor organization that has switched to the simplified tax system not to restore VAT on property received as a result of the reorganization. They are as follows.

Firstly, the conditions under which an organization is obliged to restore VAT on purchased goods (works, services) are defined in paragraph 3 of Article 170 of the Tax Code of the Russian Federation. From this rule it follows that the organization that previously accepted the tax as a deduction must restore VAT. The successor organization did not claim input VAT on the received property for deduction, so there is no reason to restore it. In addition, the requirements for VAT restoration do not apply to transactions involving the transfer of property to legal successors during reorganization (subclause 2, clause 3, article 170 of the Tax Code of the Russian Federation).

Secondly, during reorganization, the legal successor is charged with paying taxes accrued by the reorganized organization (Clause 1, Article 50 of the Tax Code of the Russian Federation). Neither Article 50 nor Article 162.1 of the Tax Code of the Russian Federation contains provisions obliging the successor to restore the VAT accepted for deduction by the reorganized organization.

Thirdly, as a general rule, an organization applying a simplified tax regime after reorganization is not a VAT payer, and the provisions of Chapter 21 of the Tax Code of the Russian Federation do not apply to it (clause 2 of Article 346.11 of the Tax Code of the Russian Federation). Tax legislation does not provide for any exceptions regarding the restoration of VAT during reorganization.

From the totality of the above rules, we can conclude that successors applying the simplification and receiving any property during the reorganization should not restore input VAT on this property, previously accepted for deduction by the reorganized organization. However, given the position of regulatory agencies, the application of this conclusion in practice will most likely entail a dispute with inspectors. Such a dispute will have to be resolved in court. Stable arbitration practice confirms the legality of the successor’s refusal to restore VAT (see, for example, the ruling of the Supreme Court of the Russian Federation dated October 17, 2014 No. 307-KG14-1534, resolution of the Federal Antimonopoly Service of the North-Western District dated April 30, 2014 No. A52-1617/ 2013, West Siberian District dated March 14, 2014 No. A81-2538/2013, Ural District dated December 21, 2012 No. F09-12394/12, Moscow District dated May 21, 2007 No. KA-A40/3985-07 ).

Situation: should an organization, when switching to the simplified tax system, restore the input VAT accepted for deduction on the costs of constructing a building? Construction began when the organization applied OSNO.

Yes, I should.

In this situation, the VAT amounts previously accepted for deduction relate to fixed assets that the organization will not use in activities subject to VAT. Therefore, before switching to simplification, such deductions need to be restored. This is stated in subparagraph 2 of paragraph 3 of Article 170 of the Tax Code of the Russian Federation.

Transfer the restored amounts of input VAT to the budget based on the results of the last tax period preceding the transition to the special regime (clause 1 of Article 174 of the Tax Code of the Russian Federation).

When calculating income tax, include the amount of recovered VAT as part of other expenses. This procedure follows from the provisions of paragraph 3 of subparagraph 2 of paragraph 3 of Article 170 and subparagraph 1 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation and is confirmed by letters of the Ministry of Finance of Russia dated April 1, 2010 No. 03-03-06/1/205, dated January 27, 2010 No. 03-07-14/03.

An example of restoration of input VAT on fixed assets. The organization switched to a simplified system of taxation

In June 2015, Alpha LLC purchased equipment (fixed assets) at a price of RUB 236,000. (including VAT – 36,000 rubles). The organization was a VAT payer and accepted the submitted input tax for deduction. There was no revaluation of the value of the fixed asset.

From January 1, 2021, Alpha switched to a simplified system. Therefore, in December 2015, the accountant calculated the amount of VAT to be restored.

As of December 31, 2015, the residual value of the equipment is RUB 164,664. The organization's accountant restored the amount of VAT previously accepted for deduction and included it in expenses when calculating income tax for 2015. The amount of VAT to be recovered was:

36,000 rub. × RUB 164,664 : (236,000 rub. – 36,000 rub.) = 29,640 rub.

Situation: when switching to a simplified system, is it necessary to restore input VAT, previously accepted for deduction on raw materials (materials, works, services) spent on the production of finished products?

Yes need. At the same time, develop the methodology by which you will determine the amount of VAT to be restored.

As a general rule, when switching to the simplified tax system from the general taxation system, the amounts of VAT previously accepted for deduction must be restored.

In particular, this must be done in relation to input VAT on goods (services, works), the cost of which is included in the cost of finished products that were not sold before the transition to simplification. In this case, the fact of payment for such goods (works, services) does not matter. That is, the previously adopted tax must be restored, even if the organization has accounts payable for such goods (works, services). After all, the main thing is not this, but the fact that such costs formed the cost of products that they did not have time to sell, being under the general taxation regime.

VAT must be restored in the last quarter preceding the transition. This conclusion follows from the provisions of paragraph 2 and paragraph 5 of subparagraph 2 of paragraph 3 of Article 170 of the Tax Code of the Russian Federation.

However, there is no specific methodology for calculating the amount of VAT to be recovered on finished products. There are no official clarifications on this issue. Therefore, the recovery procedure must be determined independently and specified in the accounting policy for tax purposes. In this case, it is worth considering the method by which you form the cost of finished products. For example, you can determine the amount of VAT to be restored based on the share of expenses for which the tax was deducted and which were included in the cost of finished products remaining in warehouses.

An example of calculating VAT for recovery from expenses included in the cost of finished products

Alpha LLC is engaged in the production of furniture. The cost of finished products is determined based on actual costs.

In December 2015, the organization produced: – 125 garden benches; – 50 garden tables.

The cost of finished products is formed from the following costs:

- materials – 250,000 rub. (VAT accepted for deduction - 45,000 rubles);

- labor costs with accruals - 150,000 rubles. (without VAT);

- depreciation of equipment - 100,000 rubles. (without VAT);

- rent of a warehouse and workshop – 100,000 rubles. (VAT accepted for deduction is 18,000 rubles).

As of December 1, 2015, Alpha had no balances of finished products.

Of the total volume of finished products in December, the following were sold:

- 25 garden benches worth RUB 100,000. (100 pcs. × 4000 rub.);

- 30 garden tables worth RUB 300,000. (30 pcs. × 10,000 rub.).

Thus, as of December 31, 2015, the following balances of unsold finished products were recorded at the Alpha warehouse (at sales prices):

- 100 garden benches worth RUB 400,000. (100 pcs. × 4000 rub.);

- 20 garden tables worth RUB 200,000. (20 pieces × 10,000 rub.).

From January 1, 2021, Alpha will switch to a simplified version. The accountant decided to restore input VAT in proportion to the share of costs in the total volume of finished products. First, he determined the relationship between the amount of VAT accepted for deduction on the resources that were spent on the production of finished products and the actual cost of finished products produced in December:

(45,000 rub. + 18,000 rub.): (250,000 rub. + 150,000 rub. + 100,000 rub. + 100,000 rub.) = 0.105.

The accountant then determined the relationship between total costs and the cost of finished products in selling prices:

(250,000 rub. + 150,000 rub. + 100,000 rub. + 100,000 rub.) : (100,000 rub. + 300,000 rub. + 400,000 rub. + 200,000 rub.) = 0.6.

The amount of input VAT, which relates to the balances of unsold finished products and which is restored in connection with the transition to simplification, is:

(400,000 rub. + 200,000 rub.) × 0.6 × 0.105 = 37,800 rub.

The VAT amount is RUB 25,200. (45,000 rubles + 18,000 rubles – 37,800 rubles) refers to finished products sold during the period of application of the general taxation system, and therefore cannot be restored.

Advice: if an organization is ready for a dispute with the tax office, it may not recover VAT on materials (work, services) consumed in the production of finished products. Most likely, this position will have to be defended in court. The following arguments will help in the dispute.

The dispute about the need to restore VAT on finished products during the transition from the general taxation system to the simplified one was considered in the resolution of the Federal Antimonopoly Service of the North Caucasus District dated February 13, 2009 No. A32-2653/2008-30/40-16/224. The court concluded that in the situation under consideration, the organization should not restore the tax. The basis for this decision was the provisions of paragraph 2 and paragraph 5 of subparagraph 2 of paragraph 3 of Article 170 of the Tax Code of the Russian Federation. The accounting data presented to the court confirmed that the finished products were produced and delivered to the warehouse when the organization was conducting activities subject to VAT. Consequently, the resources used to produce finished goods were expended in the period in which the organization applied the general taxation system. Thus, the application of a VAT deduction in respect of these resources was legal. The organization will not be able to reuse used raw materials. Simplified activities will only use finished products created using these resources. But the organization does not have input VAT accepted for deduction on finished products, which means there are no grounds for restoring the tax.

The validity of this conclusion was confirmed by the Supreme Arbitration Court of the Russian Federation in its ruling dated June 19, 2009 No. 11995/08. However, it should be taken into account that when checking, the tax inspectorate may ignore a specific arbitration case. Therefore, when refusing to restore VAT on finished products during the transition from the general taxation system to a special regime, you need to prepare to defend your decision in court.

Situation: when switching to a simplified system, is it necessary to restore input VAT, previously accepted for deduction on low-value items (special equipment, work clothing), the cost of which was fully expensed in tax accounting? The property has not been written off from the organization's balance sheet.

Yes need.

In this situation, the amounts of VAT previously accepted for deduction relate to property that the organization ceases to use in activities subject to this tax. Therefore, when switching to a simplified system, such amounts need to be restored. This follows from the provisions of subparagraph 2 of paragraph 3 of Article 170 of the Tax Code of the Russian Federation.

Reflect the restored tax amounts in the VAT return for the quarter that precedes the transition to the special regime (clause 1 of Article 174 of the Tax Code of the Russian Federation).

In the situation under consideration, it will not be possible to use arguments that would allow not to recover VAT on materials, the cost of which is included in the finished product. After all, equipment, workwear and other low-value property do not imply their one-time use. If such assets are reflected in the organization's balance sheet, this means that it continues to use them in its activities. But after the transition to simplified taxation, this activity becomes not subject to VAT, and therefore, the organization is deprived of the right to part of the deductions that it took advantage of when applying the general taxation system. Therefore, VAT must be restored in a part proportional to the value of low-value assets reflected in accounting as of the date of change of the tax regime.

An example of VAT restoration on low-value property during the transition from a general taxation system to a simplified one

In 2015, Alpha LLC applied a general taxation system. In January 2015, the organization purchased a set of workwear worth RUB 82,600, including VAT - RUB 12,600. In the same month, the workwear was transferred from the warehouse to the production departments of the organization.

In accordance with the accounting policy in tax accounting, the accountant writes off the cost of low-value assets as expenses at a time at the time of commissioning (subclause 3, clause 1, article 254 of the Tax Code of the Russian Federation). In accounting, the accountant transfers the cost of such property to expenses evenly over the useful life (clause 26 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated December 26, 2002 No. 135n).

The useful life of workwear is 2.5 years (30 months).

During 2015, the following expenses were recognized for the purchase of workwear:

- when calculating income tax - in the amount of 70,000 rubles. (RUB 82,600 – RUB 12,600);

- in accounting - in the amount of 28,000 rubles. ((RUB 82,600 – RUB 12,600): 30 months × 12 months).

Input VAT in the amount of RUB 12,600. was accepted for deduction in the first quarter of 2015.

From January 1, 2021, Alpha will switch to a simplified version.

Since in tax accounting the cost of workwear was completely transferred to expenses, these costs are not taken into account when calculating the single tax. In accounting, the organization continues to transfer the cost of workwear to expenses on a monthly basis until the end of the useful life of the property (18 months).

The amount of input VAT accepted for deduction is restored by the accountant in proportion to the outstanding cost of workwear in accounting as of December 31, 2015.

Input VAT for recovery is equal to:

RUB 12,600: RUB 70,000 × (RUB 70,000 – RUB 28,000) = RUB 7,560

About paying tax.

According to paragraph 1 of Art. 174 of the Tax Code of the Russian Federation, payment of VAT upon transition to the simplified tax system for transactions recognized as an object of taxation in accordance with paragraphs. 1 – 3 tbsp. 146 of the Tax Code of the Russian Federation, on the territory of the Russian Federation is carried out based on the results of each tax period based on the actual sale (transfer) of goods (performance, including for one’s own needs, work, provision, including for one’s own needs, services) for the expired tax period in equal shares no later than the 25th day of each of the three months following the expired tax period, unless otherwise provided by Chapter. 21 Tax Code of the Russian Federation.

This norm does not indicate that it applies only to persons who are VAT payers. Therefore, persons who have switched to the simplified tax system must be guided by the procedure from paragraph 1 of Art. 174 of the Tax Code of the Russian Federation when paying VAT for the last tax period preceding the transition to the special regime. Indirect confirmation of the correctness of this judgment is in the decisions of the AS TsO dated March 31, 2016 No. F10-614/2016 in case No. A09-2920/2015, the AS VSO dated December 1, 2017 No. F02-6060/2017 in case No. A33-166/2017. Essentially, they are devoted to other nuances of paying VAT by “simplified people”. However, both resolutions state that persons who are not taxpayers calculate the amount of VAT (if they issue an invoice to the buyer highlighting the amount of tax - clause 5 of Article 173 of the Tax Code of the Russian Federation) and pay it to the budget in the manner and time frame , which are established by clause 1 of Art. 174 Tax Code of the Russian Federation.

In other words, persons who are not recognized as VAT payers, but for one reason or another are obliged to pay this tax, must make payments based on the procedure from paragraph 1 of Art. 174 Tax Code of the Russian Federation.