The person acting as the authorized signatory of the financial statements is the head of the business entity, or the manager who is charged with such powers in accordance with the decision of the governing bodies of the entity. Unless the organization's charter provides otherwise, the head of the company has the right to delegate his powers regarding the signing of financial statements to another person. The transfer of this right is accompanied by the drawing up of an appropriate power of attorney and does not require notification of this to the company’s management bodies. In the article we will consider on the basis of what documents and who signs the financial statements.

Who signs the financial statements in accordance with the law?

Law 402-FZ “On Accounting” does not contain provisions that strictly regulate the restriction of the rights of the head of the company to delegate the authority to sign statements to other persons. According to Art. 13 of this law, financial statements are recognized as drawn up after they are signed on paper by the head of the company. A copy of the financial statements signed by the manager must be kept in the company. In this case, the manager’s signature must also contain the date of signing the copy of the reporting.

The head of a company is understood as a person who is the sole executive body or is responsible for conducting affairs in the company. A manager may also be considered a manager, to whom the functions of the sole executive body are transferred.

Only the head of the company has the right to sign financial statements. The authority to sign financial statements is prescribed in the company's constituent documents by decision of the governing body (meeting of founders). This decision is formalized in the appropriate protocol (

On persons authorized to sign financial statements on the basis of a power of attorney

Publication date: 07/04/2013 06:28 (archive)

Information message from the Department of Work with Taxpayers of the Federal Tax Service of Russia for the Irkutsk Region

The Federal Tax Service, by Letter dated June 25, 2013 No. ED-4-3/ [email protected] , regarding the possibility of the head of an economic entity transferring his powers to sign accounting (financial) statements to another person on the basis of a power of attorney, reports the following.

According to paragraph 8 of Art. 13 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting” (hereinafter referred to as Federal Law No. 402-FZ), accounting (financial) statements are considered prepared after signing a copy of it on paper by the head of an economic entity.

In accordance with the Information of the Ministry of Finance of Russia dated December 4, 2012 No. P3-10/2012 “On the entry into force of the Federal Law dated December 6, 2011 No. 402-FZ “On Accounting” on January 1, 2013, a copy of the accounting report must be kept in the affairs of an economic entity ( financial statements signed by the head of the economic entity; Moreover, the signature of the head of the economic entity must contain the date of signing of this copy. In cases of submission of accounting (financial) statements to several addresses, such statements must be signed by the same authorized persons.

In paragraph 7 of Art. 3 of Federal Law No. 402-FZ states that the head of an economic entity is a person who is the sole executive body of the economic entity, or a person responsible for conducting the affairs of the economic entity, or a manager to whom the functions of the sole executive body have been transferred.

In accordance with paragraphs. 2 p. 3 art. 91 of the Civil Code of the Russian Federation (hereinafter referred to as the Civil Code of the Russian Federation), the competence of the general meeting of participants of a limited liability company includes the formation of the executive bodies of the company and the early termination of their powers, as well as the adoption of a decision on the transfer of powers of the sole executive body of the company to the manager, approval of such a manager and the terms of the agreement with him, if the company's charter does not include the resolution of these issues within the competence of the board of directors (supervisory board) of the company.

According to paragraph 4 of Art. 40 of the Federal Law of 02/08/1998 No. 14-FZ “On Limited Liability Companies” (hereinafter referred to as Federal Law No. 14-FZ), the procedure for the activities of the sole executive body of the company and its decision-making is established by the charter of the company, internal documents of the company, as well as the agreement, concluded between the company and the person performing the functions of its sole executive body. At the same time, in paragraphs. 2 p. 3 art. 40 of Federal Law No. 14-FZ states that the sole executive body of a company issues powers of attorney for the right of representation on behalf of the company, including powers of attorney with the right of substitution.

In accordance with paragraphs. 1 and 3 paragraphs 1 art. 103 of the Civil Code of the Russian Federation, the competence of the general meeting of shareholders of the company includes changing the charter of the company; formation of the executive bodies of the company and early termination of their powers, if the company's charter does not include the resolution of these issues within the competence of the board of directors (supervisory board). At the same time, on the basis of clause 3 of Art. 103 of the Civil Code of the Russian Federation, by decision of the general meeting of shareholders, the powers of the executive body of the company can be transferred under an agreement to another commercial organization or to an individual entrepreneur (manager).

According to paragraph 2 of Art. 69 of the Federal Law of December 26, 1995 No. 208-FZ “On Joint-Stock Companies”, the competence of the executive body of the company includes all issues of managing the current activities of the company, with the exception of issues falling within the competence of the general meeting of shareholders or the board of directors (supervisory board) of the company.

Based on the above, the Federal Tax Service of Russia reports that accounting (financial) statements must be signed by persons authorized to do so by the legislation of the Russian Federation or the constituent documents of an economic entity, or decisions of the relevant management bodies of the economic entity. Such persons include the head of an economic entity, that is, the sole executive body or manager, to whom the powers of the former were transferred based on a decision of the management bodies of the economic entity. At the same time, unless otherwise provided by the charter of an economic entity, the head of an economic entity has the right to transfer his powers on the basis of a power of attorney, including the signing of accounting (financial) statements, without notifying the management bodies of the economic entity.

The Ministry of Finance of the Russian Federation in Letter dated April 30, 2013 No. 07-01-10/15212 also expressed the opinion that Federal Law No. 402-FZ does not contain provisions limiting the right of the head of an economic entity to delegate his authority to sign accounting (financial) statements this economic entity to another person on the basis of a power of attorney.

Contact numbers: 28-93-89, 28-93-83

What is meant by financial statements?

Accounting statements are understood as any reporting document that contains information about the financial and economic operations carried out by the company. As a rule, these are reports that are submitted at a certain frequency (for example, every quarter, every six months or annually) to regulatory authorities:

- Federal Tax Service;

- Goskomstat;

- FSS;

- Pension Fund.

Important! Who exactly signs the reports submitted to these authorities will depend on what standards of responsibility for the approval of reports are assigned to the company.

Power of attorney for the right to sign financial statements

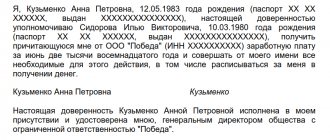

The head of the company has the right to draw up a power of attorney for the right to sign the financial statements to another person, who, as a rule, is:

- Chief Accountant;

- head of one of the company's divisions;

- company lawyer;

- another employee.

Such a document can be drawn up by a secretary or lawyer, after which the document is signed by the manager. A power of attorney to sign statements represents the right to sign strictly defined documents, so they should be clearly indicated (Read also the article ⇒ Zero LLC reporting - list of mandatory reports).

There are no special requirements for drawing up a power of attorney, but when drawing up a document, you should adhere to the rules of office work for such documents. The main requirement for such a power of attorney is to indicate information about the principal, as well as the personal data of the authorized person. In addition, the power of attorney indicates the validity period of the document, as well as the signatures of the principal and the authorized representative.

Important! The wider the range of powers assigned to the trustee, the more detailed information about the parties should be indicated.

Can a director delegate the authority to sign statements to another person?

The issue of transferring the authority of the head of an economic entity to sign accounting (financial) statements to another person on the basis of a power of attorney was considered by the Federal Tax Service in Letter dated June 26, 2013 N ED-4-3 / [email protected] Tax department specialists clarified: according to clause 7 of Art. 3 of Federal Law N 402-FZ, the head of an economic entity is recognized as a person who is its sole executive body, or a person responsible for conducting the affairs of an economic entity, or a manager to whom the functions of the sole executive body have been transferred.

It should be taken into account that in accordance with paragraphs. 2 p. 3 art. 91 of the Civil Code of the Russian Federation, the competence of the general meeting of LLC participants includes the formation of the executive bodies of the company and the early termination of their powers, as well as the adoption of decisions on the transfer of powers of the sole executive body of the company to the manager, approval of such a manager and the terms of the agreement with him, if the company’s charter does not cover the resolution of these issues within the competence of the board of directors (supervisory board) of the company.

According to paragraph 4 of Art. 40 of Federal Law N 14-FZ (Federal Law of 02/08/1998 N 14-FZ “On Limited Liability Companies”) the procedure for conducting activities by the sole executive body of the company and making decisions by it is established by the charter, internal documents of the company, as well as an agreement concluded between the company and the person performing the functions of its sole executive body. At the same time, in paragraphs. 2 p. 3 art. 40 of Federal Law No. 14-FZ states that the sole executive body of a company issues powers of attorney for the right of representation on behalf of the company, including powers of attorney with the right of substitution.

In accordance with paragraphs. 1 and 3 paragraphs 1 art. 103 of the Civil Code of the Russian Federation, the competence of the general meeting of shareholders of the company includes changing the charter of the company, the formation of the executive bodies of the company and the early termination of their powers, if the charter of the company does not include the resolution of these issues within the competence of the board of directors (supervisory board). At the same time, on the basis of clause 3 of Art. 103 of the Civil Code of the Russian Federation, by decision of the general meeting of shareholders, the powers of the executive body of the company can be transferred under an agreement to another commercial organization or to an individual entrepreneur (manager).

By virtue of clause 2 of Art. 69 of Federal Law N 208-FZ (Federal Law of December 26, 1995 N 208-FZ “On Joint-Stock Companies”) the competence of the executive body of the company includes all issues of managing the current activities of the company, with the exception of issues falling within the competence of the general meeting of shareholders or the board of directors (supervisory board) of the company.

Based on the above, the Federal Tax Service came to the conclusion: accounting (financial) statements must be signed by persons authorized to do so by the legislation of the Russian Federation or the constituent documents of an economic entity, decisions of the relevant management bodies of the economic entity. Such persons include the head of an economic entity, that is, the sole executive body, or the manager to whom the powers of the former were transferred based on a decision of the management bodies of the economic entity. At the same time, unless otherwise provided by the charter of an economic entity, its director has the right to transfer his powers on the basis of a power of attorney, including the signing of accounting (financial) statements, without informing the management bodies of the economic entity about this.

The position of the tax department, set out in the said Letter, is recommended for communication to subordinate tax authorities, as well as to taxpayers.

For your information. The Ministry of Finance in Letter dated 04/30/2013 N 07-01-10/15212 also expressed the opinion that Federal Law N 402-FZ does not contain provisions limiting the right of the head of an economic entity to delegate his powers to sign the accounting (financial) statements of this economic entity to another person on the basis of a power of attorney.

The procedure for drawing up a power of attorney for the right to sign statements

- In the header of the document, you should indicate the name of the document (“Power of Attorney”), and, if necessary, assign a document number. Next, the place where the document was drawn up and the date are indicated (as a rule, the date is indicated in words).

- Next are the details of the trustor company. The full name of the company, INN, KPP, OGRN, as well as the legal address of the organization should be indicated.

- After this, information about the principal is indicated, then if the person on whose behalf the power of attorney is drawn up (usually the director). You need to indicate his full name and the document on the basis of which he acts (for example, “based on the Charter”).

- The following is information about the principal. The power of attorney includes the employee’s full name, identification document details, and registration address.

- The main part of the power of attorney indicates the powers that the authorized person is vested with this power of attorney (the list of documents that the authorized person can sign).

- The conclusion indicates the period for which the power of attorney is issued, as well as the right to transfer the right of signature to an authorized person.

- Finally, both the authorized person and the head of the organization sign the document. The power of attorney is also stamped unless the company refuses to use it.

Sample power of attorney

Answers to common questions

Question: If the power of attorney to sign financial statements is assigned to the chief accountant, can he delegate this right to another person?

Answer: As a rule, powers of attorney of this kind are drawn up without the right of substitution, otherwise the new document will require certification by a notary.

Question: For how long can a power of attorney for the right to sign statements be issued?

Answer: The validity period of the power of attorney for the right to sign accounting and tax reporting can be any, for example, one year, three years or five years. If the power of attorney does not indicate a validity period, it is considered to be equal to one year from the date of signing the document.

Who has the right to sign tax returns? The Federal Tax Service explains

Question: A specialized company maintains accounting records for a taxpayer organization. Does the manager or other person on staff of this company have the right to act as an authorized representative of the taxpayer and sign tax returns? Answer: In accordance with paragraph 1 of Art. 80 of the Tax Code of the Russian Federation, a tax return is a written statement of the taxpayer about the objects of taxation, about income received and expenses incurred, about sources of income, about the tax base, tax benefits, about the calculated amount of tax and (or) about other data that serves as the basis for the calculation and payment of tax. Taxpayers submit tax returns on the prescribed form to the tax authority at their place of registration. The taxpayer (fee payer, tax agent) or his representative signs the tax return (calculation), confirming the accuracy and completeness of the information specified in the tax return (calculation). According to Art. Art. 26, 27 and 29 of the Tax Code of the Russian Federation, a taxpayer may participate in relations regulated by the legislation on taxes and fees through a legal or authorized representative, unless otherwise provided by the Tax Code of the Russian Federation. At the same time, the personal participation of a taxpayer in relations regulated by the legislation on taxes and fees does not deprive him of the right to have a representative, just as the participation of a representative does not deprive the taxpayer of the right to personal participation in these legal relations. An authorized representative of a taxpayer is an individual or legal entity authorized by the taxpayer to represent his interests in relations with tax authorities and other participants in relations regulated by the legislation on taxes and fees, exercising his powers on the basis of a notarized power of attorney, issued in the manner established by the civil legislation of the Russian Federation. In paragraph 5 of Art. 80 of the Tax Code of the Russian Federation stipulates that if the accuracy and completeness of the information specified in the tax return (calculation) is confirmed by an authorized representative of the taxpayer (fee payer, tax agent), then the tax return (calculation) indicates the basis of the representation (the name of the document confirming the availability of authority to signing a tax return (calculation)). In this case, a copy of the document confirming the authority of the representative to sign the tax return (calculation) is attached to the tax return (calculation). Thus, since nothing else is provided by the Tax Code of the Russian Federation, an authorized representative of the taxpayer, exercising his powers on the basis of a notarized power of attorney, has the right to sign the taxpayer’s tax returns, if the power of attorney provides for such a signature right. Consequently, the authorized representative of the taxpayer, who has the right to sign tax reports, can be either the head of a specialized company that maintains the accounting records of the taxpayer organization, or another person on the staff of this company, if, in accordance with Art. Art. 185 - 189 of the Civil Code of the Russian Federation, a notarized power of attorney for the right to sign tax returns was issued in the name of the head of the specified specialized organization with the right to delegate it to another person. At the same time, on the basis of clause 7 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated February 28, 2001 No. 5 “On some issues of application of part one of the Tax Code of the Russian Federation,” the subject of the tax legal relationship is the taxpayer himself, regardless of whether he personally participates in this legal relationship or through a legal or authorized representative . In this regard, when deciding whether to hold a taxpayer accountable for a particular violation of the legislation on taxes and fees, the actions (inaction) of his representative are regarded as the actions (inaction) of the taxpayer himself.