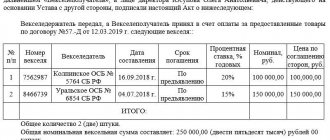

What is primary documentation in accounting?

An example of a “primary document” in accounting is any document confirming transactions of a taxpayer. We are talking about transactions that are related to the economic activities of the organization and make economic sense.

All primary accounting documentation is described in Federal Law No. 402-FZ “On Accounting”. Documents must be collected and executed in accordance with this law in order to confirm expenses and prove to the Federal Tax Service the correctness of the calculation of the tax base.

The primary document must be drawn up at the time of the business transaction, since the document confirms its completion. Typically this is done by the supplier. The list of primary accounting documentation accompanying the transaction depends on the type of transaction and may differ. You need to be especially careful about the documents for transactions in which you are the buyer, since these are your expenses and you are more interested in the correct execution of documents than the supplier. The tax office may not credit the “primary” with errors.

Storage of primary documents

The primary product must be stored for at least 5 years. During this period, the Federal Tax Service may request documents from you or your counterparties at any day in order to conduct an inspection. Documents will also be needed in case of legal disputes.

Previously, storing documents required racks, folders and a lot of paper. Now, to free up space in the office and save time and money, transfer the primary archive to electronic form. Accounting services help organize documents and store scans of them in an electronic archive - this makes it easier to search for documents. In the service list, it is easier to track the shortage of primary goods, closure, payment and transaction documents. Electronic documents are certified with an electronic signature.

If a company does not have a primary document whose mandatory storage period has not yet expired, it will receive a fine of 10 to 30 thousand rubles. Another problem with loss of documents is the inability to take into account expenses to calculate the tax base. In this case, the tax office will charge additional tax, and the company will have to pay extra.

Primary documents are divided by business stage

All transactions of the company can be divided into three stages:

The first stage is an agreement on the terms of the transaction . The result will be an agreement and an invoice for payment.

The second stage is payment for the transaction . Primary documents confirming payment:

- Cash payments - cash receipt, receipt for cash receipt order, strict reporting form. Organizations rarely pay each other in cash, since the amount of payments through the cash register is limited to 100 thousand rubles. Employees usually receive advances or accountable money in cash.

- Electronic payments, including acquiring, payment systems or transfers from a current account - bank account statement.

The third stage is receiving products . Confirmation is required that the buyer has received the product or service, and the seller has received payment. Without supporting documents, the tax office will not allow you to include the funds spent in expenses. Receipt is confirmed:

- waybill;

- sales receipt;

- act of work performed or services rendered.

Invoice as the basis for the obligation to pay

Very often, the parties enter into an agreement (whether it is a supply agreement or a contract for the provision of paid services) a condition that the buyer (customer) is obliged to pay for the goods (work, service) within the agreed period after the invoice is issued by the supplier (contractor, performer). And in the future, the obligated party (buyer, customer) does not transfer money in the absence of an invoice, regardless of the actual transfer of goods (performance of work, provision of services).

To answer this question, it is necessary to establish whether the buyer (customer) had the opportunity to pay for goods (work, services) without receiving invoices from the supplier (contractor, performer). In other words, is the absence of an invoice after the parties have signed invoices for the transfer of goods, certificates of work performed, services rendered an obstacle to payment under the contract?

We suggest that you familiarize yourself with How to draw up an application for removal from the position of chairman in an HOA. — question No. 10967965.

If the court determines that the fact of transfer and the cost of goods, works, services are confirmed in invoices, acts (bilateral documents signed by representatives of the parties and certified by the seals of organizations), the buyer (customer) does not have the right to evade payment, regardless of the presence or absence of an invoice (FAS Resolutions VVO from N A39-3128/2008-138/21, FAS ZSO from N F04-2923/2009(6367-A70-16), FAS MO from N KG-A40/9159-09, from N KG-A40/5039- 09, FAS PO from N A57-19791/2008, FAS SZO from N A56-46127/2008).

The fact is that the basis for the emergence of the customer’s obligation to pay for services by virtue of Art. Art. 779 and 781 of the Civil Code of the Russian Federation is the fact of their proper provision. Similarly, the basis for the customer’s obligation to pay for work performed is the delivery of the result of the work to the customer (Articles 702, 740 of the Civil Code of the Russian Federation).

In the same way, on the basis of paragraph 1 of Art. 486 of the Civil Code of the Russian Federation, the buyer is obliged to pay for the goods immediately before or after the seller transfers the goods to him, unless otherwise provided by the Civil Code of the Russian Federation, another law, other legal acts or a purchase and sale agreement and does not follow from the essence of the obligation (based on the general provisions of the Civil Code of the Russian Federation, based on According to the principle of compensation in civil legal relations, the receipt and acceptance of goods by one of the parties predetermines the obligation of the other party to provide consideration).

Meanwhile, in the case where the absence of an invoice is an obstacle to payment under the contract, the court considers the demands of the supplier (contractor, performer) to recover from the buyer (customer) the cost of goods (work, services) in case of non-compliance with the obligation to issue an invoice for payment stipulated in the contract, unfounded.

For example, the court recognizes that the debtor did not delay the fulfillment of the obligation if the start of the payment period by the parties is associated with the fact of issuing invoices (the contract states: payments for work performed are made by the client within three banking days from the date of invoice). In this situation, it is impossible to establish the beginning of the delay in fulfilling a monetary obligation; therefore, the debtor cannot be required to pay a penalty (Resolutions of the Federal Antimonopoly Service of the North-West District dated N A56-30104/2008, FAS Moscow Region dated N. KG-A40/12867-08). This situation is especially typical for communication services (Resolution of the Federal Antimonopoly Service of the Moscow Region No. KG-A40/3894-09).

Thus, suppliers who are unable to provide timely invoices may be advised not to include provisions in their supply agreements that make the buyer's obligation to remit payment amounts solely at the time of receipt of the invoice.

E.V. Ermolaeva

Journal expert

Accounting

and taxation"

Primary documentation in accounting list of documents 2020

Transactions vary significantly from company to company. Despite this, there is a list of primary documentation that is required in accounting:

- Agreement.

- An invoice for payment.

- Payment documents: cash receipts, strict reporting forms.

- Packing list.

- Certificate of work performed or services provided.

- Invoice.

This list of transaction documents is not exhaustive; it can expand depending on the types of transactions and accounting features in the organization.

The invoice was not received on time: will there be a delay in payment?

- Any documents related to monetary transactions are accepted from the client or from his representative at a certain (operational) time announced earlier at the bank branch where the account is opened.

- Payments are made in cash or non-cash form.

- When the corresponding amount is written off from the bank's correspondent account or when money is credited to the client's account, the bank's obligations under this payment document are considered fulfilled.

- Enrollment is made the next day after receipt of payment documents.

- Payments are made only within the amount that is currently available in the account.

- The way for non-cash payments is determined by the bank.

- Payments are made in the order in which payment documents were received.

- Any transactions are confirmed on paper, which can be received the next day after the operation.

- If transactions and account balance are not disputed within 10 days, they are considered confirmed.

- The bank does not accrue interest for using funds in the current account.

- To receive cash, the client is given a checkbook.

- All copies of documents provided to the bank or bank must be certified.

Formation of primary accounting documentation

The rules for maintaining primary documentation allow for its compilation using independently developed or unified forms (Article 9 No. 402-FZ). But remember that only a document containing all the necessary details has legal force:

- Title of the document.

- Date of creation.

- The name of the organization or the name of the entrepreneur of the compiler.

- Contents of a document or business transaction.

- Natural and monetary indicators.

- Data of responsible persons.

- Signatures of the parties.

The primary forms that the organization uses are fixed in the accounting policies. In the process of work, there may be a need to update or supplement forms - this is also recorded in the accounting policy.

Let's look at the primary documents in more detail.

Agreement

When concluding a transaction, the parties enter into an agreement between themselves, which stipulates all the conditions and details of future business transactions: terms of shipment of goods, performance of work or provision of services, time for payment, payment method, etc.

Additionally, the contract records data on the subject of the transaction and the price. The rights and obligations of the parties also need to be spelled out to make it easier to resolve possible disputes in court.

It is optimal if each transaction is formalized in a separate agreement. But companies often enter into one general agreement with regular counterparties for a number of similar transactions at once. Draw up two copies of the agreement with seals and signatures of the parties on each.

A written form of agreement is not always necessary. For example, for a purchase and sale transaction, the document confirming the conclusion is a cash receipt or sales receipt.

An invoice for payment

An invoice is a document in which the seller sets the price for his services or goods.

The buyer agrees to the supplier's terms and conditions at the time of payment. The legislator does not establish the form of the invoice, so each company draws it up in its own way. The invoice specifies the terms of the transaction, terms, payment and delivery procedures, etc.

The signature of the director or chief accountant on this document is not required (Article 9 No. 402-FZ). But to avoid any questions from the tax authorities or counterparties, it is better not to neglect them. An invoice for payment does not provide an opportunity to present demands to the supplier - it only records the purchase price. The buyer retains the right to demand a refund in case of violation of the terms of the contract or illegal enrichment of the supplier.

Payment of invoice within 5 banking days

Federal Law No. 129 of 1996, which regulates the basics of accounting in the Russian Federation, establishes that an invoice for payment is not included in the list of primary accounting documents.

In addition to the provisions of the law, the legal field uses such a concept as business customs, which have legal force by analogy with the law.

According to them, in the event of a controversial legal relationship between the parties to the contract, it is considered by the court as the primary document of the financial statements.

At the enterprise, invoices are stored in the “Payment Documents” folders. Its presence is necessary for the seller, since it indicates payment has been made for the product or service. In most cases, an invoice for payment for products (services) is issued in advance. It does not have a strict form, since the law did not include this document in the primary documentation.

Based on this, enterprises independently create forms, approving the document as an annex to the accounting policy. How long an invoice is valid for payment may not be indicated, since there is no direct legal requirement for it to be recorded in a document - this rule applies both to organizations and to issuing invoices from individual entrepreneurs.

Article 9, paragraph 2 of this law establishes the details of primary accounting documents:

- account number, date of its creation;

- payment details of the recipient of funds;

- payment details of the payer for the invoice;

- name of the organization (enterprise), address, contacts;

- a list of paid goods and services, indicating their list, name, VAT.

The list is closed: based on this, we can say that the invoice payment period is not included in the content of the primary documentation. Consequently, according to business customs, it can be equated to such documents. Failure to sign the payment deadline will not be considered a violation of the law.

If the party issuing the invoice decided to include a validity period in it, it is specified additionally in the contract. This may be 5 days or more.

In this case, the seller is obliged not to set a new price for the product in the direction of its increase until the invoice is paid.

Typically, contracts drawn up between business entities provide for penalties for late payment. Their accrual begins to take effect the next day after the expiration of the specified period.

Article 9 No. 129-FZ does not establish the mandatory presence of provisions on payment terms in the payment document. The validity period of the invoice for payment according to the legislation of the Russian Federation is not specified.

If everything is clear with the deadline specified in it - the parties to the transaction established it by agreement with each other, what to do in another situation when the deadline is not specified?

Firstly, there is a situation in which the parties did not indicate the period for how many days the invoice for payment is valid, but stated it in the contract. In this case, you should rely on the provisions of the contract.

Secondly, the situation may be complicated by the fact that the duration of the invoice for payment will not be indicated, just like in the contract. In this case, it will be considered issued without specifying a period.

Thirdly, it can be written out as an offer: in this agreement, addressed to a circle of people, a period is always indicated. If it has expired, the invoice has not been paid, the agreement is no longer considered an offer (Article 443 of the Civil Code of the Russian Federation).

Read more about the rules for registering an account...

The invoicing period is clearly defined by the Tax Code of the Russian Federation; when selling products, the seller has 5 days to issue an invoice.

Porcelain LLC sells tea sets. In September 2021, the company shipped a batch of goods in accordance with the concluded contracts, and, by agreement with another buyer, received an advance payment for the upcoming delivery. Terms of shipment and receipt of advance payment:

- JSC "Uyut" - delivery of tea sets was made on September 8;

- JSC "Mir" - issued an advance on September 12 for the supply of tea sets (upcoming).

When should an invoice be issued to Porcelain LLC for these counterparties? For the first company - no later than September 13, for the second company - no later than 19 of the same month.

JSC "Maks and Tovarishchi" sells building materials. In particular, the buyer is IP "Ivanov". The agreement of the parties established that the individual entrepreneur will be able to own construction materials only after they have been paid for.

The goods were shipped to the entrepreneur on September 10, he paid on September 17, therefore, he acquired ownership of the building materials on September 17. JSC "Max" must issue an invoice no later than the 15th of the current month, since the fact of shipment is recorded on the 10th.

Mandatory – is there a deadline for payment on time?

Important: In supply contracts, the term (Article 506 of the Civil Code of the Russian Federation) is an essential condition; without it being fixed in the text of the document, the contract is invalid. Consequently, the parties always write it down when concluding a transaction; it is mandatory, as it affects the settlement period between the partners. It is not necessary to include it in the bill.

Penalty

A penalty is a way to ensure the obligations provided for in the agreement of the parties. Applies to a participant in legal relations who has violated obligations.

The penalty is charged as a percentage for each day of delay: the parties themselves set the percentage amount. The penalty is not subject to VAT.

We invite you to read Which document states that the employer must provide the employee with the means of production - question No. 1209559.

If a penalty is applied by the parties as an element of pricing (that is, it increases the cost of products), then the tax authorities, in the process of checking a legal entity, assess a tax.

If the contract includes a condition that if the buyer is late in paying for the goods by no more than 10 days, the cost of the goods (initial) increases by 20%.

Forms and samples of invoices for payment

Mandatory details include the names of the parties, their bank details, addresses, name of goods, works, services, price per unit of goods, quantity, mandatory indication of the rate and amount of taxes included in the price of the goods, the total amount payable.

Conditions for reflecting the validity period Fulfillment of obligations (validity period) The period is not indicated in the invoice for payment, but is reflected in the agreement, contract concluded by the parties. Obligations must be fulfilled within the time limits reflected in the agreement. The deadline is not indicated in the invoice for payment and is not reflected in the agreement concluded by the parties to the transaction. Obligations can be fulfilled at any time, since in this case the invoice is considered to be issued without a time limit.

Based on this, enterprises independently create forms, approving the document as an annex to the accounting policy. How long an invoice is valid for payment may not be indicated, since there is no direct legal requirement for it to be recorded in a document - this rule applies both to organizations and to issuing invoices from individual entrepreneurs.

OPTION 2. The payment period is determined solely by the moment of receipt of the invoice. For example, the contract may say: “The buyer makes an advance payment for the goods no later than 5 banking days from the date of invoice.” In such cases, the courts do not consider the time limit set.

Since it is not allowed to tie the deadlines for the fulfillment of obligations to events that depend on the will or actions of the parties. Therefore, the obligation must be fulfilled within a reasonable time, which is counted from the deadlines established by the Civil Code of the Russian Federation.

And counterparties sometimes take advantage of this and delay payment, citing the fact that the invoice has not been received. Is the counterparty considered to be late in payment in such a situation? And should he pay the penalty provided for by the contract or law, and if it is not provided for, interest for the use of other people’s funds (hereinafter referred to as interest under Art.

395 Civil Code of the Russian Federation)?

Within the framework of the law, the length of employment of any employee is calculated from the moment of concluding a joint cooperation agreement until the termination of legal relations, regardless of the length of annual and administrative leave, as well as other cases of exemption from immediate duties.

Moreover, according to Art.

9 Federal Law No. 255, the time spent on sick leave not only does not affect the duration of leave at the expense of the employee, but is also not subject to payment, due to the fact that the worker does not require release from immediate duties. Moreover, if the worker’s sick leave continues after the end of the unpaid release from work, the period of incapacity for work, which already coincides with working days, will be paid.

A current account with Sberbank is opened without any time limit. At the request of the client, it can be closed at any time after writing a written application.

The remaining funds from the account must either be transferred to another client account or issued in cash. The bank may terminate the agreement if there is no money in the account within 2 years and no transactions are made.

In this case, the account owner is sent a written notice two months before the expected closure of the account.

These documents are not mandatory, but their use helps management and accounting keep control of cash flow and compliance with the terms of contracts by both parties.

How long is an invoice valid for payment under the law? What happens if you miss the payment deadline? Answers to these and other questions can be found in the article.

- When contacting a bank, a citizen, using a pre-filled receipt or details, makes a payment in favor of one or another body, and in return receives a note from the bank about the payment.

- The transfer of funds can occur non-cash from account to account; the document confirming payment will be a payment order with a bank mark.

- Through automatic payment terminals using the same details, you can make a payment in favor of a particular organization.

- Through the personal account of the Online Bank service, the state fee can be paid at a convenient time anywhere from a mobile device or home computer.

- If you have a valid bank card and a personal account on the State Services portal, payment can be made directly through the website.

Bill of lading or sales receipt

Sales receipts are issued in two cases: when selling goods by individuals or when selling to individuals.

Invoices, as a rule, are used by organizations to document the sale of goods and their further receipt by the buyer.

Like the contract, the invoice is drawn up in two copies. One remains with the supplier to confirm the transfer of goods, and the second is received by the buyer to confirm receipt.

The data in the delivery note and invoice must match.

The person who releases the goods puts his personal signature and the company seal on the delivery note. And the buyer also certifies the document with a signature and seal.

Its functions

This documentation takes the form of a completely standard agreement, which specifies basic information: details of the parties, details, a list of products or services provided and the amount to be paid. An invoice agreement is used to reduce the volume of paperwork. It contains information only on the merits, and does not require additional accompanying documents or confirmatory agreements. Most often, such a contract is used:

- For the sale of goods or services.

- You can use it to issue an invoice to another organization.

- To complete a transaction with mandatory clauses.

- Used in the form of an accompanying statement.

- Hiring workers on a fixed-term contract.

Example. The company orders a repair team and enters into an invoice agreement with them, which immediately indicates the scope of work, deadlines and amount to be paid. Once the work is completed, the paper is posted through the accounting department and the invoice is due.

Goods supply

Delivery and shipment of products has long been carried out under this contract at many enterprises. It can replace several papers at once and speed up the payment process. The customer receives payment immediately after the goods are delivered. In this case, the buyer does not have to pay the invoice separately and enter into an agreement.

Simplified form

This documentation contains all the necessary information.

Provision of services

To carry out the provision of services through accounting, you do not need to prepare a lot of documentation; it is enough to draw up an invoice agreement and indicate in it the nuances of the transaction. For example, one company orders a batch of products from another. The paper immediately indicates the volume of goods, delivery times, details of the enterprises and responsible persons. After the product delivery process has been completed, the customer submits the contract to the accounting department, and it is paid upon delivery.

It may also talk about deadlines and penalties if the products are not delivered on time, or indicate payments for providing low-quality goods. That is, the compiler can make the documentation narrowly focused. Despite the fact that the document does not have a legal form, the employer can rest assured that the agreement is legally valid. The main thing is that the act contains the signatures and seals of all participants in the process.

Important! The accounting department most often draws up such an agreement together with lawyers so that all the nuances are taken into account.