The legislative framework

Order of the Ministry of Agriculture No. 750 dated May 16, 2003 suggests using specialized form No. 423-APK. However, since it relates to primary documentation, you can develop the form yourself.

You can also take as a basis the intersectoral form No. MB-2 from the appendix to the Resolution of the State Statistics Committee of the Russian Federation No. 71 of October 30, 1997. It is simpler and more personalized.

IMPORTANT!

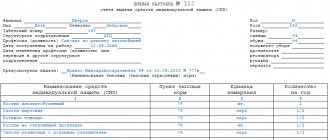

MB-2 is maintained for a specific employee. Therefore, his full name and the position appears there initially above the table.

Sample of filling out the MB-2 form

The personal instrument issuance card is designed to control inventory with a small book value. Until 2003, there was even a limit - no more than 2000 rubles. Now this rule does not apply. Each company can set its own limits in accordance with its accounting policies.

Record sheet for tools and equipment in operation form n m 31p

To properly organize accounting and resolve the issue of the moment of repayment of the cost when transferring inventory and accessories into operation, it is advisable in the accounting policy to define their types (groups), which can be classified as follows: - household supplies (for which the organization approves a limit, for example, up to 100 rubles per unit and writes them off in full as expenses); — items of multiple and individual use (written off at full cost as expenses); — reusable items (written off at a cost reduced by the cost of their standard possible use); — seasonal items (written off as expenses at a cost calculated based on the remaining time of their use in the reporting year). After the transfer of inventory and household supplies from the warehouse to operation, it is recommended to promptly monitor their availability, movement and compliance with the deadlines for their use. The statement is written out for one or more names in the accounting department in two copies, one of which remains with the recipient of the valuables with a receipt for release by the warehouse manager (storekeeper), and the second - with the warehouse manager (storekeeper) with a receipt from the recipient for acceptance of the valuables.

Within the time limits established by the document flow, the statements are submitted to the accounting department as part of the documents attached to the reports on the movement of material assets. Access to the full contents of this document is restricted. In this case, only part of the document is provided for familiarization and avoidance of plagiarism of our work.

To gain access to the full and free resources of the portal, you only need to log into the system. It is convenient to work in extended mode while gaining access to paid portal resources, according to. — — — — — — — — — — © 2019119361, Russia, Moscow, st. font size ORDER of the Ministry of Agriculture of the Russian Federation dated May 16, 2003 750 ON THE APPROVAL OF SPECIALIZED FORMS OF PRIMARY ACCOUNTING DOCUMENTATION (2018) Relevant in 2021 Designed to account for the release of inventory, tools and household supplies with a useful life of up to 12 months (based on the adopted accounting policy) within pre-approved standards. Serves as a supporting document for released and received material assets from the warehouse and their attribution to production costs. N 750 AGREED by letter of the State Statistics Committee of Russia dated April 10, 2003 N KL-01-21/1381 Form N 422-APK Codes Form according to OKUD Date (day, month, year) Organization according to OKPO Structural unit N Last name, first name, patronymic Personnel number Inventory and household supplies Unit of measurement Quantity, units. Date of entry into service Service life Signature on receipt (delivery) name nomenclature number OKEI code name 1 2 3 4 5 6 7 8 9 10 11 Reverse side of form N 422-APKN last name, first name, patronymic Personnel number Inventory and household supplies accessories Unit of measurement Quantity, units. Only after a specified period of time has passed after the start of operation do they begin to lose their technical characteristics. For example, these are metalwork tools, farming tools, various instruments, industrial and household equipment.

Download the card form on our website: The inventory and household supplies accounting card takes into account labor tools whose useful life exceeds 12 months and whose cost is no more than 2,000 rubles.

How to fill out

A typical card for recording an employee's instrument has two sides. On the front (after the name of the organization and structural unit, as well as the full name of the financially responsible person) information about the equipment issued should be placed:

- his name;

- inventory number;

- useful life;

- information about receipt (when, in what quantity and at what cost);

- similar information about the issue;

- relevant entries (debit and credit);

- data on balances (by quantity and value);

- signature MOL.

If necessary, you can add a column with information about the employee who receives the inventory. This will allow you to track not only the period of use and the degree of wear, but also who is responsible for possible damage or theft.

IMPORTANT!

Form No. 423-APK is most often created for a certain group of means of labor.

The reverse side of 423-APK should only be filled out when it is time to write off a means of production. The initial data must be taken from the conclusion of a specially assembled commission.

Form 423-APK

Card for inventory and household supplies

Therefore, the card can take into account those low-value fixed assets whose value does not exceed the value limit established by the accounting policy for such assets.

In accounting, an organization can use a unified document form or an independently developed one, which must contain mandatory details. Find out what details the primary document should contain in the article “Primary accounting documents - list”.

Explanations for filling out the card To enter data into the card, inventory and accessories should be grouped according to the same type of application or the same cost. The card indicates the name of the property group and its purpose.

The card is issued in one copy for each financially responsible person. Data on the receipt and disposal of inventory is entered into the card on the basis of primary documents.

Card for inventory and household supplies

Only after a specified period of time has passed after the start of operation do they begin to lose their technical characteristics. For example, these are metalwork tools, farming tools, various instruments, industrial and household equipment.

Download the card form on our website: Download form The card for inventory and household supplies takes into account means of labor whose useful life exceeds 12 months and whose cost is no more than 2,000 rubles.

Important That is, the card is intended for accounting for low-value fixed assets. It allows you to obtain operational data on the availability of inventory and household supplies of a certain production area and maintain proper control over the movement of such property.

IMPORTANT! Currently, the limit on the cost of inventory for accounting in a card (2,000 rubles), established back in 2003, is irrelevant.

The procedure for accounting for inventory and household supplies: postings

Attention Control ratios in tax reporting (2) Filling out tax reporting forms (12) Unjustified tax benefit (1) Insurance contributions to the Federal Tax Service (24) Payment of taxes and contributions (2) Accounting (168) Fixed assets (27) Intangible assets (8 ) Materials (17) Goods (3) Works, Services (0) Bank, current account (6) Cash. KKT. Strict reporting forms (4) Financial investments. Loans (6) Settlements and liabilities (6) Settlements with personnel (19) Settlements for taxes and contributions (8) Costs (14) Sales (5) Other income / expenses (2) Profit (0) Capital and reserves (5) Dividends (7) Authorized capital (5) Reserves (2) Accounting statements (5) Accounting accounts (7) Accounting principles (2) Accounting entries (81) Primary accounting (10) PBU (accounting provisions (1) Inventory (1 ) Other accounting issues (399) Total exchange rate differences (0) Following PBU.

Blanker.ru

The front side of the form is intended to indicate:

- asset name,

- inventory number,

- service life,

- details of the document for admission,

- cost,

- issuance data,

- invoice correspondence,

- the remainder of the materiel value,

- signature of the responsible person.

Information about the disposal of the asset is entered on the back of the card. Disposal is carried out on the basis of a decision of a special commission and is documented in an act. How to draw up a write-off act, see the article “Act for write-off of fixed assets - a sample of filling out.”

Results Organization of reliable and timely accounting of receipt, storage, operation, disposal of inventory and household supplies contributes to the control of these assets, their timely replenishment and renewal.

Form No. 423-APK helps to accomplish these important tasks.

Form 423-apk: household supplies inventory cards

Loans to individuals (4) Accountability (4) Registration of legal entities (6) Liquidation of legal entities (6) Tax control (12) Trademarks (1) Letters from the Federal Tax Service of Russia (99) Letters from the Ministry of Finance (55) Other regulatory documents (62) Examples of agreements (22 ) Methodological recommendations (9) Guidelines (10) Arbitration practice (12) Foreign companies (2) Benefits (4) Calendars and dates (1) Orders of the Federal Tax Service (6) Controlled transactions (2) Tax evasion (14) Services ( 4) Self-employed citizens (3) Individual entrepreneurs (5) 4-FSS (1) KBK (2) Webinars (1) Personnel (66) Registration of labor relations (4) Wages and other payments (8) Military registration (1) Professional standards ( 1) Termination of employment contracts (4) Fixed-term employment contracts (1) Sick leave (12) Annual leave (2) Financial assistance (1) One-time benefit (2) Labor protection (1) Average number of employees (1) Property deduction (5) Labor book (2) FMS.

Card for inventory and household supplies. form n 423-apk

Reporting on corporate income tax (7) VAT (34) Object of taxation for VAT (2) Tax base for VAT (0) Invoice (3) Tax deductions for VAT (1) Restoration of previously accepted VAT amounts for payment to the budget deductible (0) VAT refund (0) VAT benefits (0) Tax agents for VAT (6) Tax period and deadline for payment of VAT (0) Zero VAT rate (3) Filling out a VAT return (3) Clarifications and explanations for VAT (1) Purchase book (1) Sales book (1) Simplified taxation system (18) Unified tax on imputed income (6) Unified agricultural tax (0) Organizational property tax (4) Land tax (2) Transport tax (1) Personal income tax (41) Insurance contributions to the Social Insurance Fund (29) Insurance contributions to the Pension Fund of the Russian Federation and Compulsory Medical Insurance (39) Patent taxation system (10) Trade fee (2) Mineral extraction tax (2) Tax sanctions (3) Penalties . For this purpose, it is recommended to combine them into the following homogeneous types (groups):

- general purpose tools and devices (cutting, plumbing, universal measuring instruments and devices, etc.);

- special tools and devices (tools, molds, etc.);

- production equipment (desks, workbenches, racks, cabinets, bedside tables, etc.);

- household supplies (office furniture - tables, chairs, cabinets, etc.), telephones, fire-fighting equipment, etc.;

- other equipment (dinnerware and cutlery, equipment for cultural events, sports equipment, etc.).

On the front side of the card they indicate the name, inventory numbers of the objects, their location, useful life, and initial cost at the time of commissioning.

What applies to low-value OS

To answer this question, you need to check the balance sheet and depreciation groups. Most often, funds accounted for in this way have a useful life of up to a year.

For example, let’s see if a card for issuing power tools is needed. Usually it lasts longer than a year, and it can be attributed to at least the first depreciation group. Then this document is not needed.

But if the cost of a power tool is below the limit established by the accounting policy, then you can count it as inventory. Then you will need an inventory card issued to the employee.

423-APK, tool issue record card, form

MB-2, instrument registration card form

Accountant's Directory

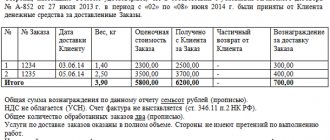

Issued by: mechanic Ivanov Mikhail Pavlovich

———————————————————————————————————————————— ¦ ¦ ¦ Issued ¦ Returned ¦ Note ¦ ¦ N ¦Name+———————————————————+————————————-+————-+ ¦п/ p¦ ¦ Date ¦Inventory¦Depreciation,¦ On ¦Quantity¦ Receipt ¦ Date ¦Depreciation,¦Quantity¦Receipt¦ ¦ ¦ ¦ ¦ ¦ number ¦ % ¦term¦ ¦in receipt¦ ¦ % ¦ ¦ in delivery¦ ¦ +— +————+———-+————+——+—-+———-+————+———-+——+———-+———+— ———-+ ¦ 1 ¦ 2 ¦ 3 ¦ 4 ¦ 5 ¦ 6 ¦ 7 ¦ 8 ¦ 9 ¦ 10 ¦ 11 ¦ 12 ¦ 13 ¦ +—+————+———-+————+ ——+—-+———-+————+———-+——+———-+———+————-+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ Term ¦ ¦ ¦Pliers for ¦05.03.2010¦ 85 ¦ 50 ¦ 30 ¦ 1 ¦ Ivanov ¦ — ¦ ¦ — ¦ Ivanov ¦uses¦ ¦ 1 ¦installation ¦ ¦ ¦ ¦days¦ ¦ ¦ ¦ ¦ ¦ ¦ extended ¦ ¦ ¦ piston ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ for 10 days ¦ ¦ ¦ rings +———-+————+——+—-+———-+————+—— —-+——+———-+———+————-+ ¦ ¦ ¦ Total...

Personal instrument issuance card

¦ 1 ¦ Total... ¦ — ¦ Х ¦ +—+————+———————————-+———-+——————————+——— -+———————-+ ¦ ¦ 05.03.2010¦ 125 ¦ 0 ¦ 30 ¦ 1 ¦ Ivanov ¦23.03.2010¦ 50 ¦ 1 ¦ Ivanov ¦ — ¦ ¦ ¦ ¦ ¦ ¦ ¦ days¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +———-+————+——+—-+———-+————+———-+——+———-+——— +————-+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ Deadline ¦ ¦ ¦ ¦05.03.

2010¦ 126 ¦ 0 ¦ 30 ¦ 1 ¦ Ivanov ¦ — ¦ — ¦ — ¦ ¦uses¦ ¦ ¦Protective ¦ ¦ ¦ ¦days¦ ¦ ¦ ¦ ¦ ¦ ¦ extended ¦ ¦ ¦cape ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ for 3 days ¦ ¦ 2 ¦ per wing +———-+————+——+—-+———-+————+———-+——+———- +———+————-+ ¦ ¦ (magnet) ¦03/05/2010¦ 127 ¦ 0 ¦ 30 ¦ 1 ¦ Ivanov ¦29.03.

2010¦ 50 ¦ 1 ¦ Ivanov ¦ — ¦ ¦ ¦ ¦ ¦ ¦ ¦ days¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +———-+————+——+—-+———-+— ———+———-+——+———-+———+————-+ ¦ ¦ 05.03.2010¦ 133 ¦ 0 ¦ 30 ¦ 1 ¦ Ivanov ¦29.03.

2010¦ 100 ¦ 1 ¦ Ivanov ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ days¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +———-+————+——+—-+———-+—— ——+———-+——+———-+———+————-+ ¦ ¦ ¦ Total... ¦ 4 ¦ Total... ¦ 3 ¦ Х ¦ +—+————+— ——————————-+———-+——————————+———-+———————-+ ¦Total for March...¦ ¦ 5 ¦ ¦ 3 ¦ Х ¦ ——————+———————————-+———-+——————————+———-+——— —————

Source - “Everything for an accountant”, 2010, No. 4

Medical examination record card. form no. 131/у-86

Appendix No. 12 to the Order of the USSR Ministry of Health of May 30, 1986

N 770¦ 1¦ 2¦ 3¦ 4¦ 5¦ 6¦ 7¦ 8¦ 9¦10¦11¦12¦ L—+—+—+—+—+—+—+—+—+—+—+ —Form code according to OKUD ¦ 5¦ 1¦ 0¦ 2¦ 8¦ 8¦ 6¦ 2¦ Institution code according to OKPO ¦ ¦ ¦ ¦ ¦ ¦ ¦ L—+—+—+—+—+—+—+— L —+—+—+—+—+— USSR Ministry of Health Medical documentation, form N 131/u-86 Approved by the USSR Ministry of Health on May 30.

86 N 770 DISPANSERIZATION RECORD CARD N ¦ ¦ ¦ ¦ ¦ ¦ L—+—+—+—+— (outpatient medical record N ¦ ¦ ¦ ¦ ¦ ¦) L—+—+—+—+—1. Last name, first name, patronymic ________ 2. Gender ___ 3. Date of birth (day, month, year) ______ tel. servant _____ 4. Address: district _________ city (village) __________ st.

________________ house N __ bldg. __ sq. __ 5. Place of work (study) __ workshop __ 6. Profession, position ____ 7. Attached to this institution: 7.1. For annual medical examination (number/name

medical area) ________ 7.2. For periodic honey.

Form 423-APK. Card for inventory and household supplies

examination for occupational hazards, other grounds _____ once a year ____ 8. Attached to another institution (name, department) ________________________________________________________________________________________________ Year of medical. inspection |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| according to plan (enter) Month of medical.

examination _________ _________ _________ _________ _________ ________ The examination was carried out (date, month) by the therapist |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|Pediatrician |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|______________________________ |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|______________________________ |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|______________________________ |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|______________________________ |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|______________________________ |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|______________________________ |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| The study was carried out (date, month) Fluorography |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|Tuberculin tests |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|Mammography |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|Cytological examination of smears |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|Examination in the observation room. |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|Microreaction with cardiolipin |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| antigenWassermann reaction |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|Investigation of smears for gonococci |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|Visual acuity |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|Hearing acuity |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|ECG |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|______________________________ |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|______________________________ |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|______________________________ |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|______________________________ |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_| |_|_|_|_|Diseases and risk factors identified for the first time during clinical examination | Group | Signature | health | doctor 19__ ______________________________________________________________________________________________ 19__ ______________________________________________________________________________________________ 19__ ____________________________________________________________________________________________ 19__ ______________________________________________________________________________________________ 19__ _______________________________________________________________________________________________ 19__ _______________________________________________________________________________________________

Entries in the card can only be used directly in a medical institution when planning and organizing medical examinations and drawing up reports in the established form.

Return to the section Standard forms, contracts

Tool registration card

The inventory and household supplies accounting card in form 423-APK is intended for separate accounting of acquired property as part of fixed assets with a useful life of more than 12 months and a cost not exceeding 2,000 rubles per unit. Such objects act in the organization as unique means of labor, retaining their natural form during use and participating in several operating cycles, gradually losing their technical qualities.

The procedure for classifying low-value means of labor as fixed assets, their composition and write-off are regulated by internal regulations, depending on the adopted accounting policy of the organization.

The card is opened for property of the same type, having the same production or economic purpose and the same value. For this purpose, it is recommended to combine them into the following homogeneous types (groups):

- general purpose tools and devices (cutting, plumbing, universal measuring instruments and devices, etc.);

- special tools and devices (tools, molds, etc.);

- production equipment (desks, workbenches, racks, cabinets, bedside tables, etc.);

- household supplies (office furniture - tables, chairs, cabinets, etc.), telephones, fire-fighting equipment, etc.;

- other equipment (dinnerware and cutlery, equipment for cultural events, sports equipment, etc.).

On the front side of the card they indicate the name, inventory numbers of the objects, their location, useful life, and initial cost at the time of commissioning.

In order to ensure the safety of inventory and household supplies, operational records of their availability and movement to places of use and financially responsible persons are organized in off-balance sheet account 013 “Inventory and household supplies for responsible use.”

The card is filled out in one copy based on the primary documents for receipt (purchase) and transfer (disposal).

On the reverse side of the card, transactions for writing off objects and reflecting values received from liquidation in accounting accounts are indicated.

Reinforcement card for issued linen, bedding, clothing and shoes

Appendix 6 to the Methodological Instructions on the organization of accounting and inventory of property and material assets of financially responsible persons in institutions of the USSR Ministry of Education

_________________________(name of institution)

REINFORCEMENT CARD

Inscribed in the register book:

accountant __________________ (signature)

“__” ___________ 19__ Sizes ——-T——T———¬ ¦Clothing¦Shoes¦Headwear¦ ¦ ¦ ¦dressing ¦ +——+——+———+ ¦ ¦ ¦ ¦ L——+ ——+———-

For things issued by ________________________________________________ (last name, first name, patronymic of the person being provided)

—-T——-T——T——T—————T———————T——¬¦ N ¦Name- ¦Norm ¦Term ¦ Issued ¦ Delivered ¦Upon- ¦¦n/ request for issuance of socks+—-T—-T—-+——T—-T—-T——+swords-¦¦ ¦things ¦ ¦ko- ¦date¦ras-¦if-¦date ¦ras-¦ras- ¦nie ¦¦ ¦ ¦ ¦ ¦li- ¦you- ¦pis-¦honest-¦sda-¦pis-¦piska¦ ¦¦ ¦ ¦ ¦ ¦ches-¦dacha¦ka in¦in ¦ chi ¦ka in regards- ¦ ¦¦ ¦ ¦ ¦ ¦tvo ¦ ¦on- ¦pro- ¦ ¦sda-¦te- ¦ ¦¦ ¦ ¦ ¦ ¦ ¦ ¦lu- ¦in writing¦ ¦che ¦lanshi¦ ¦¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ni ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ - —- +——+——+—-+—-+—-+——+—-+—-+——+——+¦ 1¦ 2¦ 3¦ 4¦ 5¦ 6¦ 7¦ 8¦ 9¦ 10 ¦ 11 ¦ 12 ¦+—+——-+——+——+—-+—-+—-+——+—-+—-+——+——+¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦+—+——-+——+——+—-+—-+—-+——+—-+—-+——+——+¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦+—+——-+——+——+—-+—-+—-+——+—-+—-+——+——+¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦L—+——-+——+——+—-+—-+—-+——+—-+—-+——+——

Should I emboss the cover? Typically the form includes: the serial number of the entry; name of fire extinguishing agent; application area; serial (factory) number, production date; date of last and next recharge; column for notes; signature of the responsible person.

Before operating a gas station, you must: open the doors and secure them in the latches; ventilate the room for 15 minutes; prepare fire-fighting equipment and fire extinguishing equipment for use; Inspect the tightness of the connections of the pipelines and the dispenser; if leakage of petroleum product is detected, fix the problem or immediately call the service on duty.

Spare parts for cars, oil filters, brake fluid and other goods for sale are accepted from the warehouse of the enterprise to which the gas station is subordinated, by the boss, foreman or other financially responsible person for reporting, and after sale they are written off from them.

It is strictly forbidden to use pipelines with flammable liquids and gases, as well as other pipelines, as grounding conductors.

All flange connections of pipelines and equipment must be tightly tightened on gaskets made of poranite, gasoline-oil-resistant rubber, or on special gaskets for petroleum products.

The gas station is equipped with measuring instruments, maintenance, operating procedures, storage and conservation must be carried out in accordance with the Gas Station Equipment Sheet with measuring instruments. Page numbers are located in the lower corners of the magazine.

Equipment and monitor its maintenance. This is a separate document for fire extinguishers and a separate document for the rest of the equipment.

Instrument issue record card (form)

Documentary accounting of property in the company. VSN 012-88 part ii form 1.2 sample form

However, the primary means of extinguishing fires include not only fire extinguishers. Concrete and asphalt surfaces of the territory of gas stations and entrances from highways should not have defects.

Each tank must be equipped with a full set of equipment provided for by the standard design or standards, and have inscriptions indicating the serial number of the tank, the base height (height stencil of the brand of the stored petroleum product.

There is no generally established form of the document, but it must contain the main technical characteristics of the equipment, columns for notes, notes on recharging, and signatures of the responsible person.

Cleaning of tanks must be carried out in accordance with the requirements of GOST 1510-84 at least once every two years, as well as if it is necessary to change the brand of petroleum product.

A square strip of paper is placed on the ends of the threads with the inscription: “sewn, numbered and sealed so many sheets.”

When repairing dispensers associated with replacing components and adjusting columns, the product poured into the measuring cup must be poured into the tank with a report drawn up, while the “underfilled” measuring cups are counted according to their nominal capacity. Heating of gas stations is carried out using only factory-made electric water heaters or water heating if it is possible to connect the gas station to a common network.

The inventory is intended for accounting of property (furniture, equipment and equipment located in the premises (room). (F-37) Open the document and download it and a sample of filling out this book Error. Pay attention to the register of measuring instruments! how to keep a food diary for a mother with allergies the child has a sample

Source: https://1atc.ru/kartochka-ucheta-instrumenta/

Form MB-2. Accounting card for low-value and high-wear items

6086 The formation of an accounting card for low-value and wearable items is necessary to control the movement of this type of property within the enterprise.

FILES Organizations, as a rule, have quite a lot of property and not all property, objects and products fall into this category. But there are signs by which you can distinguish this group of goods from the rest:

- first of all, these are those items that last less than one year and need constant replacement (regardless of how much they cost), for example, bags, nets, seines, stationery, detergents and cleaning products, etc.;

- The same list includes products with a relatively low cost (no more than 40 thousand rubles), which are not taken into account on the balance sheet of the enterprise as, including some types of workwear and shoes, computer and office equipment, bedding, dishes, household equipment, various spare parts etc.

Like any other property, low-value and wearable items are used in work by employees of the enterprise. The period for their use is quite often limited in time, and they must be issued only against receipt.

Most often, the MB-2 form is issued for such things as bags, gloves, stationery, hygiene products, etc.

The accounting card, which refers to primary documentation, allows you to track where, for what purposes and in what quantity items considered of low value were transferred.