The concept of accounts receivable and its types

The very concept of accounts receivable includes the amount of a certain debt that an organization or individual owes to your company. There is always a receivable, without it the company practically cannot function; someone takes the goods in advance, paying later, and only then does this debt arise.

| Types of debt | classification |

| By date | 1. Short-term, a type of debt that must be repaid within a year 2. Long-term - it is planned to be repaid in more than one year |

| For debts | 1. Normal - when the product or service is paid in advance 2. overdue - the buyer received the goods, but did not pay the invoice on time · Doubtful: due to the unstable financial condition of the buyer, his debt falls under the category of doubtful, but is subject to repayment in the future · Non-refundable - in case your counterparty goes bankrupt · unclaimed |

Determination of receivables that cannot be collected

Order of the Ministry of Finance of the Russian Federation “On approval of the Methodological Instructions for Inventory of Property and Financial Liabilities” dated June 13, 1995 No. 49 is also valid for BUs.

According to clause 1.5 of this regulation, an inventory of RD is carried out at least once a year before preparing annual reports. At the same time, the correctness of the amounts of receivables and the legality of their reflection in accounting as assets are checked (clause 3.48 of Order No. 49). In addition, institutions may develop additional procedures for identifying and monitoring expired credit. For example, monthly checking of loan balances by counterparties and by periods of delinquency, quarterly signing of reconciliation reports with counterparties, checking the real existence at the moment of a counterparty whose debt has not been repaid within a year, etc.

The following types of expired credits may be formed in the BU:

- for settlements with buyers of goods, works, services;

- on advances issued to suppliers;

- overpayment of wages;

- on loans issued;

- for settlements with accountable persons;

- according to settlements with persons who must compensate for damage.

A loan becomes overdue if the debtor has not repaid the amount due within the time period specified in the contract or other documents. In turn, an expired loan can become hopeless. This means that the debt cannot be collected. Reflection of bad debts on accounting accounts and in reporting leads to incorrect information provided about the organization's activities. Such debt is not an asset and should be written off.

ATTENTION! Identification of an expired loan must be documented.

One of the documents that ConsultantPlus experts suggest using for this is a certificate. Get free access to K+ and you can. Also in the system you will find samples of a reconciliation report, memo and other documents for writing off the property.

Its analysis can also help in identifying problems with payment of remote payments. Read about it in the article “Analysis of receivables and payables (nuances).”

In what cases are the debts of counterparties considered bad?

Uncollectible accounts receivable is the amount of money that the company cannot collect from the debtor for any reason.

1. The statute of limitations on the case has expired; it is three years and begins from the moment the client is notified and can reach ten years.

2. the debtor’s obligation is terminated, according to a decision of a higher authority, or the organization is liquidated

3. there is a decree from the bailiffs about the impossibility of writing off the debt, this may happen due to the debtor’s lack of property and funds in the accounts on which collection can be imposed

Important! If there are several grounds for recognizing the receivables as uncollectible, for example, the statute of limitations has expired and the client cannot be found at the actual address, then the debt can be recognized as uncollectible in the period when the first confirmation arose.

Grounds for writing off remote control

The legislation stipulates the following cases in which remote control may be considered hopeless:

- upon the occurrence of an event beyond the control of the parties, which makes the fulfillment of the obligation unrealistic (Article 416 of the Civil Code of the Russian Federation);

- in accordance with the decision of the state body, confirmed by the act (Article 417 of the Civil Code of the Russian Federation);

- upon the death of the debtor (Article 418 of the Civil Code of the Russian Federation);

- upon liquidation of a counterparty (Article 419 of the Civil Code of the Russian Federation);

- when the limitation period has passed (Chapter 12 of the Civil Code of the Russian Federation).

If the statute of limitations has passed, an act of writing off receivables is used. Such an act is signed by members of the inventory commission.

A sample form for filling out the act was prepared by ConsultantPlus experts. If you do not have access to the K+ system, get a trial online access for free.

Events beyond the control of the parties can be emergencies, disasters, military actions, and natural disasters.

An act of a government body, in accordance with which debt can be written off, is, for example, a court decision that the debt cannot be collected. If an organization sues its debtor and the court orders him to repay the debt, then the writ of execution issued in court is forwarded to the bailiffs. From this moment, collection is carried out in accordance with the Law “On Enforcement Proceedings” dated October 2, 2007 No. 229-FZ. If the bailiff service, having carried out all the required actions, has made a decision that it is impossible to collect the debt, a corresponding decree is issued to terminate enforcement proceedings. The reason specified in the decision may be:

- liquidation of the organization;

- impossibility of determining the actual location of the counterparty;

- lack of property and funds from the debtor.

The death of the debtor is the reason for recognizing the debt as bad if the obligation can be repaid only with his participation or is directly related to his person.

The BU can obtain data on the liquidation of a legal entity from an extract from the Unified State Register of Legal Entities. Such information is available on the website of the Federal Tax Service or in person. There you can also check the reliability of the counterparty before making any transactions with him: find out the status of the organization, check whether the counterparty’s registered address is not a mass one, whether it submits reports to the tax authorities, etc.

According to general rules, the limitation period is 3 years, but in some cases, in accordance with the law, it may be different. The beginning of the limitation period under the contract is the first day of delay in fulfilling the obligation. If the debtor carries out any actions indicating recognition of the debt, then the limitation period begins to count anew from the day such actions were committed. So, the debtor can sign a reconciliation report, issue a letter of guarantee, transfer some part of the debt, etc.

Doubtful debts are considered uncollectible and are removed from the accounting balance sheet based on the decision of a special commission on the receipt and disposal of assets (clause 339 of the instructions to the unified chart of accounts, approved by order of the Ministry of Finance of the Russian Federation dated December 1, 2010 No. 157n). The composition of the commission is established by order of the head of the institution. A special provision may also be created to regulate the activities of the commission.

Algorithm for writing off receivables to off-balance sheet

If a receivable is deemed uncollectible, it can be written off.

- First you need to take inventory of all accounts

- Provide a written rationale

- Issue an order from the manager to write off

Order to write off accounts receivable:

If, based on the results of the inventory, the commission determines that there really is a receivable for which the debt can be considered bad, it is necessary to issue an order to write it off. There is no specific form of this order enshrined in regulations. The company itself develops a form that is convenient for itself.

| Name | Content |

| Top of the order | Full name of the enterprise; Last name, first name and patronymic of the manager; Date and number of the order to write off receivables. |

| Text part | The name of the debtor's enterprise or last name, first name, patronymic if it is an individual is written down; The amount of accounts receivable, which, based on the results of the inventory, is considered unrealistic to be collected; Documents that are the basis for debt write-off; How will the write-off be carried out? If a reserve for doubtful debts has been formed, then the write-off must be made from the reserve. If the company does not have such a fund, then the amount of debt should be included in other expenses. |

Important! Each organization is required to create a reserve for doubtful debts

Even a receivable written off to an off-balance sheet account is not considered cancelled; it will hang there for at least five years, until the situation with the counterparty improves to collect it.

What accounts receivable can be written off?

In accounting, accounts receivable can be written off in the following cases:

- upon expiration of the limitation period;

- the debt has become impossible to collect (clause 77 of regulation No. 34n).

As a general rule, the statute of limitations is 3 years. If the deadline for fulfilling the obligation is determined, then the limitation period is counted from the end of the period for fulfilling the obligation. If such a period is not defined or is established as the “moment of demand”, then 3 years must be counted from the date of presentation of the requirement to fulfill the obligation (Articles 196, 200 of the Civil Code of the Russian Federation).

However, there are many nuances in determining the limitation period for liquidation of receivables.

Firstly, the statute of limitations may be interrupted if the counterparty acknowledges the debt (Article 203 of the Civil Code of the Russian Federation). Recognition of debt can be in the form of:

- partial transfer of receivables;

- payment of interest on arrears;

- requests to defer payment;

- submitting an application for offset;

- signing the reconciliation report;

- recognition of a claim with simultaneous recognition of a debt;

- amendments to the contract - indicating the recognition of the existence of a debt (clause 20 of the resolution of the Plenum of the Supreme Court of the Russian Federation dated September 29, 2015 No. 43).

If the counterparty has acknowledged the debt, then the limitation period must be recalculated from the moment of recognition. The time elapsed before recognition cannot be included in the new period.

IMPORTANT! The limitation period is not interrupted due to the inaction of the debtor: if he has not challenged the direct debiting of money from his current account, this does not mean automatic recognition of the debt (clause 23 of the resolution of the Plenum of the Supreme Court of the Russian Federation dated September 29, 2015 No. 43).

Secondly, if the statute of limitations has expired, and the debtor suddenly acknowledges the debt he owes, the countdown of the statute of limitations begins anew (Article 206 of the Civil Code of the Russian Federation).

IMPORTANT! Even if the limitation period has been interrupted several times, it cannot be more than 10 years from the date of direct failure to fulfill the obligation by the counterparty (Article 181 of the Civil Code of the Russian Federation).

Thirdly, if the contract states that the obligation is fulfilled in parts, and the debtor acknowledged one of these parts, then the limitation period for other parts is not interrupted (clause 20 of the resolution of the Plenum of the Supreme Court of the Russian Federation dated September 29, 2015 No. 43).

The second criterion for recognizing a receivable as uncollectible is the proven impossibility of the debtor to fulfill the obligation in the event of:

- liquidation of the debtor (Article 417 of the Civil Code of the Russian Federation);

- exclusion of the debtor from the Unified State Register of Legal Entities after 09/01/2014, which is equivalent to the liquidation of the company;

- force majeure, emergency (Article 416 of the Civil Code of the Russian Federation);

- a court ruling on the impossibility of collecting a debt or in the event that the debtor does not have property to collect (Article 266 of the Tax Code of the Russian Federation).

IMPORTANT! If another individual entrepreneur owes money to a legal entity or individual entrepreneur, then it is impossible to consider the receivable as uncollectible just because the debtor-individual entrepreneur is excluded from the register - businessmen are liable for debts with all their property even after the end of business activity (letter of the Ministry of Finance of the Russian Federation dated September 16, 2015 No. 03-03 -06/53157). An entrepreneur’s debt can be written off on a general basis either in the event of his death or upon completion of bankruptcy proceedings.

A closed list of criteria for recognizing a debt as bad is established by Art. 266 of the Tax Code of the Russian Federation and is not subject to expansion for tax accounting purposes.

But in accounting, debt can be written off for one more reason - the impossibility of collection in the opinion of the creditor himself. This method should be used only if the company has exhausted all ways to obtain money from the debtor without the help of the court, and the expected costs of the trial will exceed the amount of the receivable.

Is untimely write-off of accounts receivable considered a gross violation of accounting requirements? The answer to this question is in ConsultantPlus. Study the material by getting trial access to the K+ system for free.

Accounting for accounts receivable on the balance sheet

The accountant records this amount of debt on account 007 as the debt of insolvent debtors written off at a loss. If the debtor has the financial ability to repay the debt, it is necessary to reflect this in the organization’s other income.

In accounting, reflect the write-off of accounts receivable from the reserve for doubtful debts by posting:

Debit 63 Credit 62 (58-3, 71, 73, 76...) – accounts receivable are written off from the created reserve.

The use of the reserve is possible only within the limits of the reserved amounts, and if during the year the amount of expenses exceeds the created reserve, the difference must be reflected in other expenses for 91 accounts. Then you should make the following wiring:

Debit 91-2 Credit 62 (58-3, 71, 73, 76...) – accounts receivable not covered by the reserve are written off.

What are accounts receivable?

Accounts receivable are funds owed to a legal entity or entrepreneur by counterparties.

Below are the main cases of occurrence of receivables and accounts for their accounting according to the Chart of Accounts (approved by order of the Ministry of Finance of the Russian Federation dated October 31, 2001 No. 94n):

| Situation | Accounting account |

| The supplier received an advance payment, but did not ship goods and materials or did not perform the agreed services | 76, 60 |

| The buyer did not pay for the valuables supplied or services received | 76, 62 |

| The borrower did not repay the loan received | 73, 76, 58 |

| The employee did not report on accountable amounts | 71 |

NOTE! We consider the nuances of accounting and writing off receivables from legal entities. Entrepreneurs are not required to keep accounting on the basis of Art. 6 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ, but they can, at their own discretion, reflect receivables according to accounting rules.

The legislative framework for accounting for accounts receivable is represented by the following standards:

- Civil Code of the Russian Federation;

- Tax Code of the Russian Federation;

- regulations on accounting and accounting in the Russian Federation (approved by order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n, hereinafter referred to as Regulation No. 34n);

Unfortunately, counterparties are not always in a hurry to pay off their debts. Therefore, in a number of situations, accounts receivable are considered uncollectible and are written off.

If you doubt the return of receivables, you must create a reserve for doubtful debts in your accounting. In tax accounting, such a reserve is not created in all cases.

ConsultantPlus experts explained how to properly form a reserve for doubtful debts. To do everything correctly, get trial access to the system and go to the Ready solution. It's free.

Write-off of accounts receivable from off-balance sheet

The decision to write off the debt from the balance sheet after a period of time must be made by a commission. The debt must be considered uncollectible. Prepare the grounds for this, namely:

1. supporting documents upon the death of the creditor or its complete liquidation

2. the period by which it was possible to resume the collection process has expired

3. You can also get rid of off-balance sheet receivables if the debtor contributed funds in another way, but for this it is necessary to restore the debt on the balance sheet account

Important! If you have full confirmation of the fact that the debtor is more likely not to appear and you have sent requests to all possible authorities to find him and received official answers, only then can you write off the debt.

Results

An institution can write off debt that is unrealistic for collection only for legally established reasons. However, after write-off, it is necessary to periodically check the change in the status of the debtor; for this, the debt continues to be listed on the balance sheet.

Read about writing off debt in non-governmental organizations in the article “Procedure for writing off accounts receivable”.

Sources:

- Federal Law of October 2, 2007 No. 229-FZ

- Order of the Ministry of Finance of the Russian Federation dated December 1, 2010 No. 157n

- Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n

- Order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Write-off of receivables from off-balance sheet accounts

To carry out such an operation, it is necessary to record the grounds for such actions permitted by law. Accordingly, the grounds for writing off the “debt,” in addition to the expiration of the statute of limitations for collection, are the death or liquidation of the counterparty, force majeure circumstances and a resolution of the body authorized in such matters.

Thus, a court decision on the impossibility of collecting funds from the debtor is a reason for writing off the “hanging” amount. The second option for this outcome is the end of enforcement proceedings against the defaulter. To understand the details of these issues, let’s consider a detailed algorithm of the likely actions of accounting employees of budgetary structures.

In addition, it is appropriate here to dwell on the study of the legislative framework that omits these actions.

Writing off accounts receivable to an off-balance sheet account

Writing off accounts receivable to an off-balance sheet account

In practice, to speed up payments by counterparties for shipped goods, various systems of discounts and incentives are used. For example, a 10% discount for prepayment of goods. Sources of formation of receivables Let us highlight the main sources of formation of receivables:

- debts of buyers and customers;

- advances issued;

- debts of subsidiaries;

- debts of the founders for contributions to the authorized capital;

- bills;

Types of receivables Based on the maturity of obligations, receivables are divided into:

- Short-term accounts receivable – payments due within 12 months.

- Long-term accounts receivable – payments due over 12 months.

-lesson “Settlements with buyers and customers.

Write-off of accounts receivable in a budgetary institution

Write-off of accounts receivable in a budgetary institution

Important Note that an example of such an entry is appropriate to consider in the following form: Procedure Posting debit Entry credit Amount of funds Write-off of arrears 401,010 50,000.00 Closing an account at the end of the period 401,033 50,000.00 Accounting for debtor's debt 04 50,000.00 End of the reporting year in Such situations are also reflected by posting in the ledger. Please note! The last entry in the table below becomes a mandatory requirement. In this situation, economists keep records of the written-off amount in off-balance sheet account 04 for five years from the date of the procedure. Attention This point is taken into account by legislators for circumstances when the defaulter repays financial obligations recognized by the creditor as a bad debt. Keep in mind that situations with the return of such funds are rare, but the legal requirements in this case are logical.

Writing off debt from off-balance sheet accounts

Writing off debt from off-balance sheet accounts

Based on the received paper, the head of the institution signs an order to write off such funds. The next step here is to write off accounts receivable in a government institution, the transactions for which will be discussed below.

Attention! The mistake of inexperienced auditors in such circumstances is to ignore the statute of limitations for collection. Accordingly, the “receivable” is written off with violations.

For this reason, it is advisable for economists to study the instructions for carrying out the operation and support actions based on the above legislative framework.

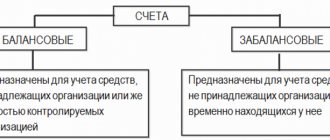

Account 007 “Debt of insolvent debtors written off at a loss”

Account 007 “Debt of insolvent debtors written off at a loss” is intended to summarize information on the status of receivables written off at a loss due to the insolvency of debtors.

This debt must be kept on the balance sheet for five years from the date of write-off to monitor the possibility of its collection in the event of a change in the property status of the debtors.

For amounts received in order to collect debts previously written off at a loss, accounts 50 “Cash”, 51 “Cash Accounts” or 52 “Currency Accounts” are debited in correspondence with account 91 “Other income and expenses”. Simultaneously to the indicated

the amount is credited to off-balance sheet account 007 “Debt of insolvent debtors written off at a loss.”

Analytical accounting for account 007 “Debt of insolvent debtors written off at a loss” is maintained for each debtor whose debt is written off at a loss, and for each debt written off at a loss.

It is considered incorrect to overstate the real value of assets if the accounts receivable include overdue debts and debts for which there is reason to assume that they will not be repaid by debtors. However, since there is some hope of collecting these debts in the future, such receivables are written off the balance sheet but recorded off the balance sheet. Here the question arises: when should it be written off and is it possible to write it off?

The Civil Code of the Russian Federation establishes a limitation period of three years. And there is an old rule regarding the procedure for maintaining account 007 “Debt written off at a loss of insolvent debtors”, which tacitly implies that on the balance sheet receivables should be taken into account throughout the entire limitation period, i.e. for three years, and then take this debt off balance sheet for another five years.

The fact that the drafters of the instructions referred to five years and not three years indicates that in fact they do not proceed from the priority of content over form, but, on the contrary, from the priority of form over content.

The best solution to the issue should be the reservation of doubtful debts during the limitation period, and after its expiration, this debt should be written off at the expense of a pre-created reserve.

In this case, no off-balance sheet accounting is required, and there is no need to open account 007 “Debt of insolvent debtors written off at a loss.”

If you open this account and strictly follow the Instructions, then for almost eight years bad receivables will appear in the accounting records - three years within the limitation period and five years after, just in case.

According to the Instructions, three years after the expiration of the statute of limitations, the accountant must write off doubtful debts from the balance sheet by debiting accounts 63 “Reserves for doubtful debts” (if such reserves have been accrued) and (or) 91-2 “Other expenses” for the amount of doubtful debts, exceeding reserves.

After this, based on the accounting department’s certificate about the debt being written off at a loss, account 007 “Debt of insolvent debtors written off at a loss” is debited, and this entry is kept for five years. If during this time it is suddenly possible to return what was lost, then the cash accounts are debited, and account 91-1 “Other income” is credited. If the debt is not repaid within five years, it should be written off from the balance sheet account. In both cases, account 007 “Debt of insolvent debtors written off at a loss” is credited.

The basis for such an entry is a certificate from the accounting department confirming the repayment of the debt or the end of the monitoring period for written off receivables.

Analytical accounting is maintained for each individual debt.

Write-off of receivables from off-balance sheet accounts

To carry out such an operation, it is necessary to record the grounds for such actions permitted by law. Accordingly, the grounds for writing off the “debt,” in addition to the expiration of the statute of limitations for collection, are the death or liquidation of the counterparty, force majeure circumstances and a resolution of the body authorized in such matters.

Thus, a court decision on the impossibility of collecting funds from the debtor is a reason for writing off the “hanging” amount. The second option for this outcome is the end of enforcement proceedings against the defaulter. To understand the details of these issues, let’s consider a detailed algorithm of the likely actions of accounting employees of budgetary structures.

In addition, it is appropriate here to dwell on the study of the legislative framework that omits these actions.