Home / Bankruptcy / Bankruptcy of legal entities

Back

Published: 09/06/2019

Reading time: 4 min

0

332

In financial relations between various types of legal entities and individual entrepreneurs, there are mutual obligations of debtors and creditors. They all boil down to the emergence of receivables and payables.

- Limitation period for accounts receivable Moment of occurrence, taking into account weekends and holidays

- Determining the beginning of the limitation period for late obligations

- How to determine the beginning of the statute of limitations if the deadline for fulfilling the obligation is not determined

Accounts receivable is a type of debt when a company does not receive payment for services provided to it or goods supplied. That is, in this case, the company acts as a creditor to whom its counterparties have debts.

Accounts payable are debts that a company has to its counterparties.

One company simultaneously has both receivables and payables. Repayment of these types of debts must occur in accordance with the conditions formulated in the concluded agreement. At the same time, the use of the word “debt” cannot always be interpreted as a delay in fulfilling a financial obligation - in financial and economic relations, this term is used to determine mutual settlements with counterparties. The use of the term “debt” lasts until all calculations are fully completed.

Limitation period for accounts receivable

The limitation period for accounts receivable (RA) is set at 3 years from the date of its formation.

This time period is established by Article 196 of the Civil Code of the Russian Federation. Here, in addition, a 10-year maximum duration of such a period is defined. Exceptions are possible, but only in circumstances specified by law. You can learn what accounts receivable is from the article “Accounts receivable is...”.

The limitation period for accounts receivable should be counted from the day following the day when the contractual terms were violated. The start date for the limitation period for receivables depends on whether the deadline for fulfilling the obligation (debt repayment period) has been established. In particular, the following situations are possible.

Each obligation must be separately reflected, even if there is only one counterparty. This is the only way to properly organize remote control accounting.

The following is a description of the features that must be taken into account when determining the limitation period for receivables.

See also “How to view accounts receivable in 1C correctly.”

EXAMPLES of determining the expiration date of accounts receivable from ConsultantPlus: 1. The lease agreement stipulates that rent is transferred within 10 calendar days from the date of invoice by the lessor. The invoice for January was issued to the tenant on January 30, 2021... For the continuation of the example, see the Ready-made solution from K+.

From what day is this period calculated?

When filing a claim in court, the deadline for collecting receivables is calculated from the day the debt became overdue. Most companies work with deferred payment. If the contract sets a payment date, for example, 45 calendar days from the date of shipment of the goods, then the receivables become overdue starting from the 46th day. The moment of shipment is the date of receipt of the goods by the warehouse employee, which is marked in the delivery note, or the date of signing the certificate of work (services) performed.

When drawing up a claim, you should take into account the date from which to collect receivables within three years by court decision: the company has the right to receive money from the date when the debt was considered overdue (this is determined by the terms of the contract) until the expiration of 3 years from that moment.

If companies operate using a factoring agreement, then the procedure for paying receivables is established by a tripartite agreement with the participation of the factor bank. The buyer is not always aware of the existence of such an agreement. In this case, the statute of limitations for overdue receivables begins from the settlement date established by the contract for the supply of goods.

Is it impossible to collect the debt? ConsultantPlus experts figured out how to write it off correctly in such a situation. Use these instructions for free.

Interruption of the limitation period

The period during which a claim must be filed may be interrupted in the following circumstances:

- the debtor acknowledged the debt;

- the debtor has repaid some of the debt;

- the debtor acknowledged the existence of the debt and asks to change the agreement so that it includes clarifications on debt restructuring.

The full circumstances and grounds for the legal interruption of the statute of limitations are given in the Resolution of the Plenum of the Armed Forces of the Russian Federation dated September 29, 2015 No. 43.

At the end of the break, the period discussed in the article starts anew, and the period that passed before the break is not excluded from the new period. There is an explanation on this matter given in the letter of the Federal Tax Service of Russia dated December 6, 2010 No. ШС-37-3/16955. To document the fact of debt recognition, a statement of reconciliation of calculations should be drawn up. The document must bear the signatures and seals of both parties.

If we are talking about repaying part of the debt or recognizing some of its share, such actions will not be considered recognition of the full amount of the debt.

It may happen that the court leaves the creditor's claim without consideration. In such circumstances, according to the provisions of Art. 203 of the Civil Code of the Russian Federation, the limitation period will continue to run without interruption, as usual.

If the court makes a decision in which the debt is recognized in a certain amount, then it is not allowed to write off the debt after the expiration of the statute of limitations. This PD can be recognized as hopeless only in 2 cases (clause 2 of Article 266 of the Tax Code of the Russian Federation):

- Enforcement proceedings have been completed. The basis is the order of the bailiff.

- The debtor organization went through the liquidation procedure. The basis is a sheet of record about the withdrawal of this organization from the Unified State Register of Legal Entities.

What documents are needed to confirm the existence of a bad debt?

Overdue accounts receivable, like any other expenses of the organization, must be supported by proper documents. Only in this case, amounts of expired debt reduce the tax base on the basis of which income tax is calculated.

Thus, the letter from the Federal Tax Service dated December 6, 2010 reflects that in order to include receivables as expenses, the following documents are required:

- proving the fact and date of debt occurrence (invoices for goods release, work acceptance certificates, other primary documents);

- confirming the end of the statute of limitations.

At the same time, the Federal Tax Service notes that a written agreement between counterparties, as a rule, does not prove the completion of a business transaction and the occurrence of debt.

Judicial practice does not have a clear opinion on the issue of what documents are sufficient to confirm bad debts.

The following documents are not considered supporting documents:

- formally executed, in the absence of real business transactions (the formality of document flow is confirmed, in particular, by the interdependence of counterparties, the signing of documents on behalf of the counterparty by an unidentified person, etc.) - this opinion is expressed in the ruling of the Supreme Arbitration Court of the Russian Federation dated November 15, 2012 No. VAS-14642/12 ;

- with defects in registration, resulting in the impossibility of establishing the grounds and date of occurrence of the debt, as well as the moment when the statute of limitations expired (determination of the Armed Forces of the Russian Federation dated April 29, 2015 No. 309-KG15-3698).

Note! At the same time, taking into account the specific circumstances of the case, payment orders and accounting registers can be considered sufficient evidence of accounts receivable, even in the absence of contracts and invoices (Resolution of the Moscow District Court No. A40-70551/14 dated May 24, 2015).

Suspension of the limitation period

The limitation period may be suspended if the following circumstances arise:

- Emergencies such as natural disasters, accidents, strikes, etc.

- Obligations are not fulfilled due to the introduction of a moratorium.

- The law on the basis of which the relations between the parties were regulated is temporarily not in force (suspended).

- One of the parties is part of the Russian Armed Forces, and they have been placed under martial law.

The limitation period can be suspended if the circumstances leading to the delay arose in the last six months of its course. If the statute of limitations is six months or less, then at any time during it.

It is also possible to suspend the limitation period in a situation where the parties intend to resolve the dispute out of court (clause 3 of Article 202 of the Civil Code of the Russian Federation). According to paragraph 16 of the resolution of the Plenum of the Armed Forces of the Russian Federation dated September 29, 2015 No. 43, the suspension of this period is carried out for the period provided for by law for an out-of-court procedure. If such a period is not established, then you should focus on a 6-month period. The countdown starts from the moment this procedure begins.

According to the norm contained in paragraph 4 of Art. 202 of the Civil Code of the Russian Federation, the claim period starts again from the moment when the suspension occurred.

Reinstating the statute of limitations

For this period, it is possible to restore it if the plaintiff has good reasons for missing it. Usually, in this capacity, the court perceives circumstances related to illness, serious condition and other personal situations.

The court will consider the reason for omission to be valid when the circumstances leading to the violation of the regulations arose during the last 6 months of the limitation period. If this period is six months or less, then at any time during its course. The corresponding norm is contained in Art. 205 of the Civil Code of the Russian Federation.

Let us point out separately that all the above preferences apply only to individuals. There is no such possibility for organizations and individual entrepreneurs, and restoration will not be made - regardless of the reasons why the deadline was missed. The rationale for this rule is contained in the resolution of the Plenum of the RF Armed Forces and the Plenum of the Supreme Arbitration Court of the Russian Federation dated February 28, 1995 No. 2/1.

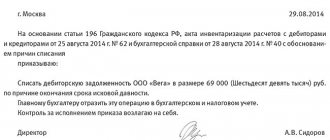

How to write off debt in accounting

If, after an inventory count, receivables are discovered, the company draws up an inventory order, and the results are entered into the INV-17 form. The next stage of writing off accounts receivable: creating a management order to liquidate the debt based on the inventory report and accounting certificate.

To avoid receiving claims from the Federal Tax Service after writing off the receivables, you should attach to the act a document with the history of the debt and paperwork about the transaction: contracts, invoices, invoices, certificates of services rendered and reconciliations. As a document confirming the hopelessness of the debt, you can send an extract from the Unified State Register of Legal Entities or a resolution of the bailiff.

Note!

The debt of a company expelled from the Unified State Register of Legal Entities after 2014 can be considered bad. However, this will not work with IP. It is impossible to write off a businessman’s debt only on the basis of an exception from the Unified State Register of Individual Entrepreneurs, since he is liable for the debts with all his property. This is possible if an individual has died, gone bankrupt or his whereabouts are unknown.

Procedure for writing off bad receivables

We found out that in order to write off an overdue debt, it must be converted into a bad debt. In addition, there must also be documentary evidence of this hopelessness.

In order to prove the completion of the period, you must present some primary documentation on which the operations were carried out; it can be:

- various acts;

- invoices;

- agreement on the purchase of products, provision of services, etc. Write-off of accounts receivable with expired statute of limitations

In this case, you will need an extract from the Register, which confirms that the organization was excluded from the Unified State Register of Legal Entities. Such an extract is an official document, which means it can be used as evidence of the liquidation of the counterparty.

Documents that can confirm inability include:

- conclusion of the liquidation commission that the liquidated enterprise will not pay the debt due to lack of funds;

- a court order to terminate proceedings due to lack of information about the location of the debtor, lack of funds and property;

- a court decision on the bankruptcy of a counterparty.

Let us recall that one of the main tasks of accounting is the formation of complete and reliable information about the activities of the organization and its property status.

The presence in an organization of receivables or payables for which the statute of limitations has expired distorts the real picture of the organization’s property and obligations. After all, a debtor with an expired statute of limitations is a debt that the organization will no longer be able to collect in court. And if the debtor does not want to repay this debt on his own (which is unlikely, because he has already had 3 years to do this), such a debt becomes unrealistic for collection, and therefore must form losses for the creditor.

The same applies to accounts payable for which the statute of limitations has expired. The creditor no longer has the opportunity to forcibly collect the debt, therefore, the debtor may no longer pay off such debt.

It is indicated that receivables or payables for which the statute of limitations has expired are written off for each obligation on the basis of inventory, written justification and order of the manager. Written off debts are included in the financial results of the organization as part of other income (when writing off a creditor) and other expenses (when writing off accounts receivable).

Write-off of receivables and payables is possible even before the statute of limitations, if such debts are considered unrealistic for collection (repayment). This is possible, for example, when the debtor is excluded from the Unified State Register of Legal Entities in the event of liquidation.

Debit of accounts 60 “Settlements with suppliers and contractors”, 70 “Settlements with personnel for wages”, 76 “Settlements with various debtors and creditors”, 67 “Settlements for long-term loans and borrowings”, etc. – Credit of account 91 “Other income and expenses", subaccount "Other income"

Debit account 91, subaccount “Other expenses” - Credit accounts 62 “Settlements with buyers and customers”, 71 “Settlements with accountable persons”, 76, etc.

If accounts receivable are written off using funds from a previously created reserve, instead of account 91, account 63 “Provisions for doubtful debts” is debited.

However, writing off receivables due to the debtor's insolvency does not lead to complete cancellation of the debt. Such a debt must be listed on the balance sheet for 5 years from the date of writing off the debt in case of its collection in the event of a change in the debtor’s property status (paragraph 2, paragraph 77 of Order of the Ministry of Finance dated July 29, 1998 No. 34n).

Debit of account 007 “Debt of insolvent debtors written off at a loss”

Write-off of accounts receivable with expired statute of limitations

In accounting, debt is written off on the basis of documents specified by regulations. The following have been approved in this capacity:

- inventory act,

- certificate from the accounting department,

- order of the director, which contains an indication of the need for write-off.

The given list of documents is indicated in paragraph 77 of the Regulations on accounting and reporting of the Russian Federation, approved. by order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n.

According to clause 11 of PBU 10/99, receivables with an expired statute of limitations should be classified as other expenses. As for tax accounting, in accordance with the norms of sub. 2 p. 2 art. 265 of the Tax Code of the Russian Federation, such DZ should be recognized as a non-operating expense.

How to account for the write-off of accounts receivable in accounting, see here.

A ready-made solution from ConsultantPlus will help you write off debt in tax accounting. Trial access to the system can be obtained for free.

You can learn about the specifics of calculating VAT when writing off receivables from the article “How to take into account VAT amounts when writing off receivables?”

Write-off documentation

To write off debt and debt, you need to make an order to inventory the debt and place its indicators in the INV-17 form.

Next, the manager issues an order to write off the company's debt according to the inventory report, which must include the amount of debt, a description of the situation in which the debt was doomed, and a reference to the number and date of the inventory report.

Tax authorities are especially painstaking in inspecting written-off debts, so it is better to attach the history of its occurrence and documents that confirm the validity of the transaction to the company’s reporting.

As a result, three documents are needed to write off a loan:

- Inventory report (INV-17).

- Justification letter. It must indicate the name of the debtor, the date the debt arose, the grounds for the debt, what documents confirm the debt, the amount of debt for each debtor, and the calculation of the limitation period.

- Order.

Results

The general limitation period for receivables is 3 years. Moreover, this period is legally allowed to be interrupted, suspended, and even restored if it is missed with justification (though only for individuals).

At the end of the period (if there was no court decision), the company has the right to write off the debt as an expense.

Such an operation will be legal both in accounting and tax accounting. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

What happens if you file a claim in court when the claim period has already expired?

The judge will take such a claim to task - he will open a case, schedule a court hearing and, if necessary, request documents from the parties to the dispute. And based on the results of the trial, it may even decide to collect the entire debt in favor of the plaintiff.

But this will happen if, before the end of the case, the defendant for some reason does not inform the judge (orally or in writing) about the application of the limitation period, that is, does not ask the judge to reject the claim due to the delay in filing it in court.

If such a statement is made, the judge will close the case without further ado. And then it will no longer be possible to get the money back. The debt will have to be written off as hopeless.

The judge does not have the right to apply the statute of limitations on his own (without a statement from the debtor), even when he himself sees that on the day of going to court it has already expired.