Off-balance sheet accounts summarize information about the presence and movement of material assets in the enterprise. They carry out some kind of budget control and are displayed in accounting in complex entries for the convenience of the report. With the help of off-balance sheet accounts, accountants have the opportunity to control individual business transactions of the organization. They belong to an economic entity, and their presence is temporary. The duration of the presence of these subaccounts in the program depends on the type and purpose of the position.

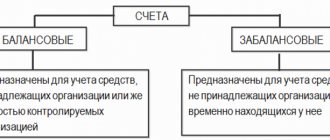

The concept of an off-balance sheet account

Off-balance sheet accounting includes a group of accounts and subgroups that summarize information on transactions and relate to the movement of inventory items of an enterprise. Postings with their participation are not constantly present in the company’s accounting and quarterly reporting, but are an important element in the preparation of reporting. Balance sheet accounting cannot be carried out correctly without off-balance sheet accounting, because such transactions are not reflected on the balance sheet. Despite this, after the processing process is completed, the balances appear as a final figure and are not taken into account in the balance sheets.

Application

These subaccounts have only an indirect impact on the final result of reporting on the main indicators and are not displayed in reporting or during inventory. Despite this, their structure is standard. There are debits and credits, and accounting occurs according to a standard simple scheme. They allow you to enter information about the receipt of goods and materials, which will be written off in the near future, but must be reflected in fact. These positions are not the property of the enterprise, and therefore are not taken into account in the balance sheet.

Important! Off-balance sheet accounts are a generalizing entry and they are created for analytical purposes, because even temporary positions require accounting.

Off-balance sheet accounting for leasing transactions

If the terms of the leasing agreement determine that the property will be taken into account on the lessor’s balance sheet, then the lessee reflects this property off the balance sheet. The received asset is accepted for accounting in off-balance sheet account 001 “Leased fixed assets”. When the leased property is redeemed, the value on the date of transfer of ownership is written off from the off-balance sheet account and credited to account 01 “Fixed assets” and account 02 “Depreciation of fixed assets” is credited.

Materials from the newspaper “Progressive Accountant”, May 2021.

Regina Kashapova, implementation department specialist.

Purpose of use

The balance sheet of any enterprise should display receipts and write-offs of all positions, but it is not always convenient for some transactions to be placed on the organization’s balance sheet, because they will interfere with the generation of reporting. These accounts are also called budget or asset accounts because they are used to account for the following items:

- Receipt or disposal of property.

- Issue or termination of security.

- Movement of material assets, including property objects: real estate, transport, land plots that do not belong to the enterprise, but are received for safekeeping.

- The movement of material assets that belong to the organization, but the cost of which has already been written off as expenses.

- Off-balance sheet accounts may collect information that may later be needed to explain certain accounting entries and will be included in the income statement.

Varieties

Using these accounts, documentation is later generated for registering a new entity or debiting funds. Despite the fact that it is not reflected in the balance sheet, correct accounting is impossible without off-balance sheet accounts. With their help, the creditworthiness, reliability and stability of the organization in the financial market are also assessed.

Not only business transactions are monitored, but also the fulfillment of obligations, write-off of debts and fulfillment of guarantee obligations. Despite the fact that accounting is kept for funds that are not owned, company employees bear full responsibility for them. Property held in subaccounts should not affect the balance sheets in any way.

On a note! The main tasks are the collection of information, as well as functions that will allow you to control the process of using values that are not the property of the company, but require accounting.

Varieties

Additional accounting is always required for individual items. In order to understand which account means what, the company always develops an account plan by accountants, but postings of this kind may appear unplanned. Accounting for temporary units cannot be neglected, because some need to pay income tax. The following accounts help keep records.

001 Off-balance sheet accounting of fixed assets is taken into account in this position. We are talking about rented properties. This position displays the assets of fixed assets that are leased by the enterprise. The amount is fixed according to the expert assessment of the concluded contract, unless otherwise specified in the contract.

002 Account 002 contains information on inventory items that are not the property of the company, but can be transferred to the balance sheet after certain conditions are met or obligations are fulfilled, for example, payment is transferred. Account 002 in accounting reflects the value of the object according to the signed contract.

003 The accounting program can report items of materials that have not been paid for, but have been placed on balance for production or future use. For example, in the production of products.

004 To find commission assets, you need to consider the positions of account 004. Here, inventory items that were taken on commission are recorded.

005 Subaccounts also reflect machinery or equipment that was received by the company for repair or installation work. The positions will then be written off, and funds for installation will be credited to the customer’s balance sheet.

006 Payment orders, receipts, forms, diplomas, certificates and shipping documents that require strict reporting are stored here. This documentation shows the arrival and departure of funds. If this position is missing, then the accounting department will not be able to store important papers and document the completion of a particular process.

Account 006

007 This is a passive account. It contains debt written off at a loss and creates a list of insolvent debtors. This liability remains on the balance sheet for 5 years, and then must be written off. This period can be set for repaying the debt.

008 Account 008 performs a generalizing function. It contains information about warranty obligations and their implementation, and also controls payments under guarantees.

009 Account 009 also has a generalizing function. It contains information about warranty obligations that have already been fulfilled. The amount of guarantees is taken from the contracts.

010 With its help you can take into account the company's inventories. This may include not only the main raw materials and materials, but also components and semi-finished products purchased by the company.

011 Some institutions lease out their fixed assets and accounting occurs using account 011, but in this case the fixed assets must be displayed on the tenant’s balance sheet.

Off-balance sheet accounts are synonymous with off-balance sheet sub-accounts, but this name is most often used in banking departments. In addition to the main ones, there is also account 012. It displays low-value and high-wear items. For example: household equipment, tools for daily work of employees, consumables. Despite the low value of some items, it is customary to display them in accounting.

Account No. 16 may also participate. Here we are talking about property that is not the property of the organization, but when there are shared property rights. 17 records the receipt of funds from suppliers for the provision of any services, and 18, on the contrary, identifies the withdrawal of funds from the institution’s balance sheet in favor of the supplier.

What can be transferred to account 012

If an accountant decides to introduce an off-balance sheet account. 012, then he must record the innovation in the company’s working chart of accounts. We remind you that the working chart of accounts is a mandatory appendix to the accounting policy of the organization (clause 4 of PBU 1/08).

In the working chart of accounts, the accountant must indicate:

- name of the new off-balance sheet account;

- what values or obligations will be taken into account.

You will find an example of a working chart of accounts in the article “Working chart of accounts for accounting - sample 2015”.

According to the purpose of off-balance sheet accounts on the account. 012 you can transfer values or liabilities that require separate accounting from balance sheet assets. Or values with a special accounting procedure.

The most common example is low-value property. This includes something whose useful life is more than 12 months, and its cost is below 40,000 rubles. In accounting, property within the limit fixed in the accounting policy (but not more than 40,000 rubles) can be taken into account as part of the inventory and attributed to expenses at the time of commencement of use.

However, due to the fact that such valuables are used for a long time, it is necessary to organize control over their safety (paragraph 4, paragraph 5 of PBU 6/01, approved by order of the Ministry of Finance of the Russian Federation dated March 30, 2001 No. 26n). The legislation does not establish methods of such control. A common method is to create an off-balance sheet account. 012 “Low-valued property” and reflect on it the assets transferred for operation in a conditional valuation - for example, the cost of 1 object is equal to 1 ruble.

Then the accounting records for writing off the “low value” into operation will look like this:

| Debit | Credit |

| 20, 23, 25, 26, 29, 44 | Low-value property transferred to exploitation |

| Low-value property is included off the balance sheet in the conditional valuation | |

| Low-value property has been disposed of (wear and tear, sale, loss, etc.) |

Another accounting object that can be transferred to the account. 012, is an intangible asset (IMA) received for use under a license agreement. According to clause 39 of PBU 14/2007 (approved by order of the Ministry of Finance of the Russian Federation dated December 27, 2007 No. 153n), the user of such intangible asset must take it into account in an off-balance sheet account in a valuation comparable to the amount of remuneration for the use of the asset.

The owner of the intangible asset (licensor) remains the owner of the asset, and the user (licensee) receives the right only to temporarily use the intangible asset (Article 1235 of the Civil Code of the Russian Federation). Therefore, such assets should be accounted for separately from other intangible assets of the organization - that is, off the balance sheet. The Chart of Accounts does not provide for a special account for such cases, so an organization can introduce an account. 012 “Intangible assets received for use.” Then the licensee’s accountant will make the following entries in the accounting records:

| Debit | Credit | |

| Intangible assets were received for use under a license agreement | ||

| 60, 76 | A fixed one-time payment for obtaining intangible assets for use is taken into account | |

| 20, 23, 25, 26, 29, 44 | 60, 76 | Periodic payments for the use of intangible assets are taken into account |

| 20, 23, 25, 26, 29, 44 | A one-time fixed payment for the use of intangible assets is written off as expenses (in equal shares during the period of use of intangible assets or in accordance with another method specified in the accounting policy) | |

| Intangible assets received under a license agreement are written off due to termination of use |

Another off-balance sheet account. 012 can be used to account for purchased fuel cards and other similar smart cards. This is necessary for quantitative accounting of such cards and control over their movement. They can be reflected on the balance sheet in the conditional valuation. Accounting for accounting of transactions with fuel cards using an off-balance sheet account. 012:

| Debit | Credit |

Off-balance sheet accounting has its own characteristics, which are important not to miss for an accountant. Our selection will help with this - in one article about accounting for the balance sheet of fixed assets, raw materials and other material assets.

The chart of accounts contains eleven off-balance sheet accounts, of which seven accounts are intended for property accounting. Among the features of balance sheet accounting, we highlight two main ones:

- Off-balance sheet entries are made without using double entry. In other words, material assets on the balance sheet are reflected only in debit or only in credit of one account.

- None of the off-balance sheet accounts are closed at the end of the calendar year. If the property has fallen into disrepair or needs to be removed from off-balance sheet accounting for other reasons, the accountant must make an entry reflecting the value of the disposed property on the credit of the account.

Transactions with off-balance sheet accounts

In addition to the main functions of each position, complex operations are also carried out, where several subaccounts are involved in postings at once. For off-balance sheet accounts, accounting activities are carried out in the following areas:

- Reserve fund. For example, cash notes, coins.

- Obligations and guarantees of borrowers.

- Consumables.

- Settlement documentation.

- Accounting for material assets accepted for storage.

- Leased and leased fixed assets.

- Debt write-off.

Three main subgroups

There is no correspondence with the balance, as well as between subaccounts.

Accounting for materials on off-balance sheet accounts - regulatory nuances

The most common use of off-balance sheet subsidiary accounts is to record low value items or materials. At the same time, analytics is organized in the context of counterparties (retailers, consignors, suppliers, etc.), types of inventory items, storage locations, materially responsible persons (MRP). The basis is primary documents - acts of transfer for storage, acts of write-off, invoices, claims, etc.

Off-balance sheet accounts for inventory accounting:

- 002 – values that are accepted by the company for safekeeping or become property only after fulfillment of contractual conditions are reflected here. For example, after full payment of the purchase price.

- 003 – materials received by the organization for further customer processing are reflected here.

- 004 – here the commission agent takes into account goods received from the principal for sale.

Postings

Accounting does not use double entry for off-balance sheet accounts, which is clearly visible in the postings. In simple words, the balance reports the availability and type of funds, debit is the receipt, and credit is the expense or write-off. Postings provide accounting guarantee, and thanks to them, some items do not have to be shown in the financial statements. Example:

| Debit | Credit | Operation description | Total amount/RUB | Supporting documentation |

| 9 | Uncovered debt to the organization | 564000 | Standard contract | |

| 76 | 51 | Written off financial institution fees | 1340 | Standard contract |

| 8 | 60 | Receipt of new equipment from the supplier for installation work | 47868 | Equipment invoice |

| 8 | 76 | Adding commissions to the cost of equipment | 1340 | Standard contract |

| 19 | 60 | VAT | 73432 | Packing list |

| 1 | 8 | Equipment testing and commissioning | 446378 | A report drawn up by those responsible for commissioning |

| 68 | 19 | Acceptance of input VAT for deduction | 73432 | Invoice |

| 60 | 76 | Transfer of funds to an organization for outstanding debt | 564000 | Online payment |

| 76 | 51 | Repayment of debt to a financial institution | 564000 | Online payment |

| 9 | Complete debt write-off | 564000 | Debt cancellation act |

On a note! Calculation at the end of the month occurs according to the following formula: Final balance = beginning of the month + debit turnover – credit turnover.

Off-balance sheet accounts are not the main ones in accounting, but no less important because they take into account the movement of temporary assets of the enterprise. Their presence in accounting is temporary; they are not displayed in financial statements, but with their help it is easy to monitor the correctness of business transactions. The final balance must always be a debit balance. If it comes out with a minus in the program, it means that a system error occurred or the accountant entered inaccurate data.