Tax risks. Due diligence disputes

11.10.19

The article was published in the newspaper “First Page” No. 9 (114), October 2021.

The legislation does not clearly define tax risks. However, back in 2007, the Federal Tax Service, by Order dated May 30, 2007 No. MM-3-06/ [email protected] “On approval of the Concept of the planning system for on-site tax audits” (hereinafter referred to as the Concept), approved publicly available criteria for self-assessment of risks for taxpayers, used by tax authorities in the process of selecting objects for conducting on-site tax audits.

According to the Concept, planning on-site tax audits is an open process based on the selection of taxpayers to conduct on-site tax audits based on the risk criteria of committing a tax offense.

Previously, planning on-site tax audits was a purely internal confidential procedure of the tax authorities.

In order to ensure a systematic approach to the selection of objects for conducting on-site tax audits, the Concept defines an algorithm for such selection.

The selection is based on a qualitative and comprehensive analysis of all information available to the tax authorities (including from external sources), and on its basis the determination of “risk zones” for committing tax offenses.

Thus, in this Concept, planning on-site tax audits is interconnected with the formation and development among taxpayers of a correct understanding of the legislation on taxes and fees, the conviction that its violation is inadmissible and the need for strict compliance with the laws.

At the same time, the taxpayer can use his right to independently assess risks and evaluate the advantage of independently identifying and correcting errors made when calculating taxes.

According to the Concept, every taxpayer must understand that the possibility of not including an organization in the plan of on-site tax audits depends on the transparency of its activities, the completeness of calculation and payment of taxes to the budget.

Thus, in accordance with this Concept, planning of on-site tax audits is carried out on the basis of the principle of bilateral responsibility of taxpayers and tax authorities, in compliance with which the former strive to fulfill their tax obligations, and the latter - to a reasonable selection of taxpayers for conducting on-site tax audits.

Systematic self-assessment of risks based on the results of its financial and economic activities will allow the taxpayer to timely assess tax risks and clarify their tax obligations.

This Concept contains 12 main criteria for assessing tax risks:

- the tax burden of a given taxpayer is below its average level for business entities in a specific industry (type of economic activity);

- reflection of losses in accounting or tax reporting over several tax periods;

- reflection in tax reporting of significant amounts of tax deductions for a certain period;

- the outstripping growth rate of expenses over the growth rate of income from the sale of goods (works, services);

- payment of average monthly wages per employee below the average level for the type of economic activity in the constituent entity of the Russian Federation;

- repeated approach to the maximum value of indicators established by the Tax Code of the Russian Federation that grant taxpayers the right to apply special tax regimes;

- reflection by an individual entrepreneur of the amount of expenses as close as possible to the amount of his income received for the calendar year;

- building financial and economic activities on the basis of concluding agreements with counterparties, resellers or intermediaries (“chains of counterparties”) without reasonable economic or other reasons (business purpose);

- failure by the taxpayer to provide explanations for notifying the tax authority about the identification of discrepancies in performance indicators, and (or) failure to provide the tax authority with the requested documents, and (or) the availability of information about their destruction, damage, etc.;

- repeated deregistration and registration with the tax authorities of the taxpayer in connection with a change in location (“migration” between tax authorities);

- a significant deviation of the level of profitability according to accounting data from the level of profitability for a given field of activity according to statistics;

- Conducting financial and economic activities with high tax risk.

All of the above criteria differ by type of activity, industry, and region of location of the taxpayer. For example, the criterion for the significance of the amounts of tax deductions differs depending on the region, but is within 89%. The profitability criterion depends on the industry and type of activity, etc.

Publicly available tax risk criteria: regulatory framework

“Tax risks” should be understood as factors in the presence of which a business entity is likely to evade taxes (receive an unjustified tax benefit). These factors were systematized by the Federal Tax Service.

The order of the Federal Tax Service on the concept of planning on-site inspection activities dated May 30, 2007 No. MM-3-06 / [email protected] contains tax audit risk criteria: if they detect compliance with them in the activities of an enterprise, tax officials “diagnose” a likely decrease in the solvency or payment discipline of an economic entity, a possible participation in tax evasion schemes and appoint an on-site control and supervisory event.

Initially, the Federal Tax Service (in the first edition of Order No. MM-3-06/ [email protected] ) identified 11 criteria by which the economic activities of taxpayers were assessed for tax risks. But already in the second edition of the normative act, 12 tax risk criteria appeared. Since then, the number of relevant criteria has remained unchanged. Let's take a closer look at them.

Legal aspect of tax risks

In its Letter dated 06/03/2016 No. ED-4-15/ [email protected] “On the assessment of RMS risk indicators”, the Federal Tax Service of Russia for the first time disclosed information that taxpayers in the risk management system of the automated VAT-2 control system (ASK VAT-2 RMS) 2) are divided by risk level automatically - based on the results of the risk management system. The tax inspector only needs system indicators to assess the potential risks of auditing a taxpayer.

In practice, things are not so simple. An on-site inspection is assigned not only on the basis of these criteria, but they enable the analytical department of the Federal Tax Service to begin to develop the connections and activities of those taxpayers who have not passed “through the sieve” of the ASK VAT RMS (now ASK VAT-3).

In recent years, the tax authority has methodically issued letters of explanation to taxpayers to independently assess their activities from the point of view of tax risks. These clarification letters contain criteria for business fragmentation, criteria for unjustified tax benefits, and judicial practice in tax disputes, and the tax authority is so confident in its abilities that it publishes both losing and winning decisions of judges for taxpayers.

Based on the above, the following conclusions can be drawn:

- tax risks are the likelihood of committing tax offenses leading to negative economic and legal consequences (collection of arrears, penalties, fines, tax, administrative and criminal liability, subsidiary liability of persons controlling the debtor (KDL), etc.) for the taxpayer or tax agent;

- Taxpayers can assess tax risks on their own, since most of the criteria are public;

- if the tax authority has appointed an on-site tax audit, it means that the tax risk of this taxpayer is not just high, but the fact of committing a tax crime is obvious to the tax authority, i.e. the tax risk has been realized.

One of the main criteria that entails significant tax risks is still criterion No. 8: the construction of financial and economic activities based on the conclusion of agreements with counterparties-resellers or intermediaries (“chains of counterparties”) without the presence of reasonable economic or other reasons (business goals).

This criterion, after the Plenum of the Supreme Arbitration Court No. 53 of October 12, 2006, “On the assessment by arbitration courts of the validity of a taxpayer receiving a tax benefit,” became decisive in various tax disputes and, despite the introduction of Art. 54.1 remains in demand at the current time.

Courts and tax authorities carefully apply (or rather, carefully do not apply) Art. 54.1 Tax Code of the Russian Federation. This is because if you start using it, then most taxpayers will have no chance of running a business, since it will be difficult to prove that the taxpayer incurred expenses not for the purpose of reducing the tax base for income tax or to obtain deductions for personal income tax or VAT.

Proving the existence of reasonable economic and other reasons (a business purpose) is based on the old approach of due diligence and economic justification.

In Art. 252 of the Tax Code of the Russian Federation introduces the concept of “economic feasibility,” which a group of deputies of the State Duma of the Russian Federation tried to challenge and reduce to the term “economic feasibility.” The Constitutional Court in its rulings No. 320-O-P and No. 366-O-P dated 06/04/2007 indicated: “Tax legislation does not use the concept of economic feasibility and does not regulate the procedure and conditions for conducting financial and economic activities, and therefore the validity of expenses that reduce For tax purposes, income received cannot be assessed from the point of view of its expediency, rationality, efficiency or the result obtained. By virtue of the principle of freedom of economic activity (Article 8, Part 1, of the Constitution of the Russian Federation), the taxpayer carries out it independently at his own risk and has the right to independently and individually assess its effectiveness and expediency.

Within the meaning of the legal position of the Constitutional Court of the Russian Federation, expressed in Resolution No. 3-P dated February 24, 2004, judicial control is not intended to check the economic feasibility of decisions made by business entities that have independence and wide discretion in the business sphere, since due to their risky nature Such activities have objective limits on the courts’ ability to detect the presence of business miscalculations in them.

Consequently, the norms contained in the second and third paragraphs of paragraph 1 of Art. 252 of the Tax Code of the Russian Federation do not allow their arbitrary application, since they require the establishment of an objective connection between the expenses incurred by the taxpayer and the focus of his activities on making a profit, and the burden of proving the unfoundedness of the taxpayer’s expenses rests with the tax authorities.”

The Ministry of Finance of the Russian Federation and the Federal Tax Service have repeatedly confirmed this approach in their letters. In one of the latest appeals (Letter of the Ministry of Finance of the Russian Federation dated April 19, 2019 No. 03-0307/28232), officials indicated: “At the same time, we note that the validity of expenses taken into account when calculating the tax base should be assessed taking into account the circumstances indicating the taxpayer’s intentions to receive economic benefits.” effect as a result of real business or other economic activity.

Considering that tax legislation does not use the concept of economic feasibility and does not regulate the procedure and conditions for conducting financial and economic activities, the validity of expenses that reduce income received for tax purposes cannot be assessed from the point of view of their feasibility, rationality, efficiency or the result obtained. By virtue of the principle of freedom of economic activity (Part 1 of Article 8 of the Constitution of the Russian Federation), the taxpayer carries out it independently at his own risk and has the right to independently and individually assess its effectiveness and expediency.”

Features of tax control

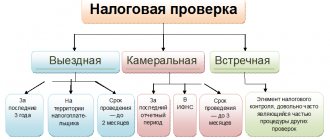

Forms of tax control are certain methods of checking an organization and the procedure for its taxation, provided for by the Tax Code of the Russian Federation. The subject and objectives of tax control, as well as its criteria, functions, procedure and general provisions, are always aimed at collecting information about the taxation of a particular organization and its subsequent analysis.

A desk audit, which is part of the types of tax control, is carried out at the location of the taxpayer. In the course of performing its functions, in order to identify a particular offense within a prescribed period, the documents submitted by the taxpayer, as well as those documents that the tax authority has, are checked.

If, after the result is received, there are any violations identified during the audit, the taxpayer is given a certain period for this violation of state law to be eliminated.

In cases where the tax control authorities have revealed that a previously established violation of the current legislation of Russia was not eliminated on time, other measures of responsibility may be applied to the taxpayer, the procedure for application and criteria of which, as well as the functions, content, subject and effectiveness, are established by the Tax Code of the Russian Federation .

The desk audit, which is part of tax control activities, also concerns tax benefits, the presence of which is confirmed by relevant government documents.

For each tax control event, a permissible period for conducting a particular audit is established, during which the organization’s documents can be checked, analyzed, functions, general provisions, content, criteria, effectiveness, etc. can be studied.

In cases where a desk audit was carried out unlawfully, its result is not correct. It can be refuted by interested parties who are participants in these legal relations.

At the same time, as a result of the violation, a certain liability may be applied, which is an integral part of the violations committed and is part of the specifics of tax control. Responsibility is chosen based on the result of the inspection, which is an indisputable basis.

Evidence of effectiveness and justification of costs

In practice, the question arises: “How to prove the effectiveness of expenses and their validity?”

The answer to this question is both simple and complex at the same time. It is simple, since you only need to prove the intention to make a profit, but complex, since this proof will require the ingenuity of the taxpayer and the preparation of a significant number of documents:

- prepared supporting documents (memorandums, orders, contracts, etc.), which will indicate the need for the taxpayer to incur costs: for example, by stipulating in the employment contract with the employee the obligation to feed him, the taxpayer has the opportunity to include these costs in the calculation of income tax (if compliance with other provisions of Article 252 of the Tax Code of the Russian Federation) on the basis of paragraph 25 of Art. 255 Tax Code of the Russian Federation;

- primary accounting documents recording completed facts of economic life;

- monitoring documents, i.e. related to confirmation of due diligence and subsequent control over the counterparty to the transaction or control of the internal operations of the taxpayer.

For a taxpayer, it is sometimes important to prove to himself the economic feasibility, namely expediency, and not justification, that is, to understand for himself why any expenses are needed, how they will affect the receipt of income in the future. If this is done, then there will be no problems with the economic justification of expenses for the tax authorities.

Indicative in this regard may be the case on the validity of loans (Decision of the Supreme Court of the Russian Federation dated June 17, 2019 No. 309ES19-7907 in case No. A7610867/2017). The case is interesting because of the amount charged to the taxpayer:

- additionally assessed corporate income tax in the amount of RUB 106,704,578;

- penalties for corporate income tax in the amount of RUB 21,756,772. 48 kopecks;

- fine for corporate income tax in the amount of RUB 15,190,100. 30 kopecks

The essence of the matter is that the taxpayer took out interest-bearing loans (and the interest was not inflated), and gave these loans at a lower interest rate or without interest to interdependent persons.

The decision in favor of the tax authority was firmly established in all instances.

It is obvious that in these transactions there is neither justification nor expediency of the expenses incurred. From the point of view of a group of companies, such transactions are quite reasonable, but from a tax point of view, they are not.

Moreover, an analysis of judicial practice shows that if the taxpayer has prepared and justified the expenses, then the tax authority does not dispute such circumstances, and if a tax dispute begins, then the tax authority has clear signs of unjustified expenses. Therefore, judicial practice is developing in favor of the tax authorities.

So, if the process of proving economic feasibility is often subject to the taxpayer and it is possible to justify expenses, then when it comes to due diligence, everything becomes more complicated: the parameters of diligence are not spelled out in the legislation and there are no absolute algorithms for exercising due diligence. To better understand this problem, let us turn to the history of the issue.

Types of tax control

The Tax Code of the Russian Federation does not provide an accurate interpretation of the types of tax control, so their classification is varied. For example, it could be like this:

| Types of tax control | |||

| Tax control by time | Tax control by verification method | Tax control at the location | Tax control by frequency |

|

|

|

|

The Ministry of Finance plans to introduce operational control over the correct recording of settlements, including the completeness of revenue accounting, from 2021. At the same time, the Law “On KKM” No. 54-FZ will be repealed, and the norms of administrative punishment will “move” from the Code of Administrative Offenses to the Tax Code of the Russian Federation. Read more about the planned innovations in the Review from ConsultantPlus. If you do not yet have access to the K+ legal reference system, get trial online access for free.

Read more about the inspection procedure in the following materials:

- “Procedure for conducting an on-site tax audit (nuances)”;

- “Features of conducting a counter tax audit.”

The importance of due diligence

When a taxpayer cares about the validity of expenses, then everything depends only on him (his employees and their timely actions). When it comes to due diligence, only the collected package of documents depends on the taxpayer himself, and everything else depends on the counterparty and the tax authority, which may decide that after three years the taxpayer worked with an unscrupulous supplier or buyer.

As a result, all tax risks are immediately transferred to the bona fide taxpayer only due to the dishonesty of his partners.

From the taxpayer’s point of view, this is the highest injustice, and from the point of view of the fiscal interests of the tax authority, it is an excellent opportunity to replenish the budget.

The concept of due diligence was first introduced in the Resolution of the Plenum of the Supreme Arbitration Court No. 53 of October 12, 2006. Thus, paragraph 10 states that the fact that the taxpayer’s counterparty violates its tax obligations does not in itself constitute evidence that the taxpayer received an unjustified tax benefit.

A tax benefit may be recognized as unjustified if the tax authority proves that the taxpayer acted without due diligence and caution and he should have been aware of violations committed by the counterparty, in particular, due to the relationship of interdependence or affiliation of the taxpayer with the counterparty.

A tax benefit may also be recognized as unjustified if the tax authority proves that the activities of the taxpayer, its interdependent or affiliated persons are aimed at carrying out transactions related to tax benefits, mainly with counterparties that do not fulfill their tax obligations.

After such conclusions from the judges, accusations of taxpayers for failing to exercise due diligence became practically the norm, and the tax authorities boldly began to prove in court that the taxpayer did not conduct the required amount of audits of the counterparty’s activities. The following facts serve as a basis for charges of failure to exercise due diligence:

- the counterparty was liquidated within 3 years from the date of the transaction;

- the head of the counterparty did not appear for questioning;

- the counterparty does not submit VAT returns;

- the counterparty does not pay the declared VAT, etc.

The use of the concept of “due diligence” by tax authorities made it possible to blame taxpayers for non-payment of taxes by their counterparties, and the courts for the most part began to support this concept. Moreover, if a tax dispute involved a large amount (several tens of millions), then, as a rule, it was resolved in favor of the tax authorities. If the amount in dispute is insignificant (1-2 million), then the taxpayer had every chance to prove the so-called “due diligence”.

The fact is that past and existing legislation does not contain ready-made algorithms and approaches, following which the taxpayer would receive an “indulgence”; therefore, being a subjective assessment, due diligence leads to a certain arbitrariness on the part of the tax authorities and the judicial system.

In his numerous letters (from 06/21/2017 No. 03-12-11/2/39116, from 02/13/2017 No. ED-415/ [email protected] , from 12/13/2016 No. 03-02-07/1/74372, from 07/12/2016 No. 03-01-10/41099, dated 06/24/2016 No. ED-1915/104, dated 10/16/2015 No. 0302-07/1/59422, dated 03/16/2015 No. ED-4-2/4124, dated 12/17/2014 No. 03-02-07/1/65228) The Federal Tax Service and the Ministry of Finance of Russia disclosed some criteria for due diligence, which a taxpayer should pay attention to when choosing a counterparty. According to officials, the following circumstances should be checked:

- lack of information about the state registration of the counterparty in the Unified State Register of Legal Entities (this is a very old criterion, which is practically not used after the introduction of ASK);

- registration of the counterparty at the “place of mass registration”;

- presence of the counterparty's head on the list of disqualified persons;

- lack of documentary evidence of the authority of the counterparty's representative, copies of his identity document;

- lack of information about the actual location of the counterparty, as well as the location of its warehouse and (or) production and (or) retail space;

- lack of obvious evidence of the possibility of the counterparty actually fulfilling the terms of the contract;

- existence of reasonable doubts about the possibility of the counterparty actually fulfilling the terms of the contract, taking into account the time required for delivery or production of goods, performance of work or provision of services;

- inclusion by the parties into the contract of additional conditions that are unfavorable for the counterparty or not related to the subject of the contract.

The list goes on, since there are a lot of possible options for “wrong” behavior. The actual actions of the taxpayer in checking the counterparty can always be called into question and considered insufficient after the tax authorities have identified facts of dishonest actions of the counterparty after the transaction between him and the accused taxpayer.

Useful for taxpayers is the Letter of the Federal Tax Service of Russia dated March 23, 2017 No. ED-5-9/ [email protected] It notes that tax authorities need to pay special attention to assessing the sufficiency and reasonableness of the measures taken by the taxpayer to verify the counterparty, and also evaluate for receipt unjustified tax benefit is the dishonesty of the taxpayer being audited and the actions he performed (i.e., the diligence he showed in choosing a counterparty), and not the actions performed by the counterparties.

In addition, it is clarified that in order to assess the actions of a taxpayer it is necessary:

Assess the validity of the choice of counterparty by the audited taxpayer.

Explore questions:

- whether the choice of counterparty differed from the conditions of business turnover or the practice established by the taxpayer himself in selecting counterparties;

- How were they assessed?

- terms of the transaction and their commercial attractiveness;

- business reputation;

- solvency of the counterparty;

- risk of non-fulfillment of obligations;

- the counterparty has the necessary resources (production capacity, technological equipment, qualified personnel) and relevant experience;

- whether the taxpayer entered into transactions primarily with counterparties who did not fulfill their tax obligations.

Pay attention to the following:

- lack of personal contacts between the management (authorized officials) of the supplier (contractor) company and the management (authorized officials) of the buyer (customer) company when discussing the terms of delivery, as well as when signing contracts;

- lack of documentary confirmation of the authority of the head of the company - the counterparty, copies of his identity document;

- lack of information about the actual location of the counterparty, as well as the location of warehouse and (or) production and (or) retail space;

- lack of information about the method of obtaining information about the counterparty (no advertising in the media, recommendations of partners or other persons, the counterparty’s website, etc.).

In this case, one should take into account the availability of available information about other market participants (including manufacturers) of identical (similar) goods (works, services), including those offering their goods (works, services) at lower prices:

- information on the state registration of the counterparty in the Unified State Register of Legal Entities;

- information about whether the counterparty has the necessary license, if the transaction is concluded within the framework of a licensed activity, as well as a certificate of admission to a certain type or types of work, issued by a self-regulatory organization.

Request from the taxpayer documents and information regarding the taxpayer’s actions when choosing a counterparty:

- documents recording the results of search, monitoring and selection of a counterparty;

- source of information about the counterparty (website, advertising materials, proposal for cooperation, information about the counterparty’s previously performed work);

- results of monitoring the market for relevant goods (works, services), studying and assessing potential counterparties;

- documented justification for choosing a specific counterparty (a fixed procedure for control over selection and risk assessment, procedure for conducting a tender, etc.);

- business correspondence.

As part of the application of the provisions of sub. 1 and 2 paragraphs 2 art. 54.1 of the Tax Code of the Russian Federation, the tax authority must prove that the main purpose of the taxpayer’s conclusion of a transaction (operation) was not to obtain the results of business activities, but to obtain tax savings (if facts of non-compliance with the conditions specified in subclause 1 of clause 2 of Article 54.1 of the Tax Code of the Russian Federation are revealed), and (or) that the transaction (operation) was not executed by the declared counterparty, and the taxpayer used formal document flow for the purpose of unlawfully accounting for expenses and claiming tax deductions for the disputed transaction (operation) (if facts of non-compliance with the conditions established in subclause 2 of clause 2 of Art. 54.1 Tax Code of the Russian Federation).

If circumstances are established indicating that the main purpose of the taxpayer entering into a transaction (operation) was not to obtain results of business activity, but to obtain tax savings, the tax authorities must prove that such a transaction (operation) does not have any reasonable explanation from the standpoint of the economic necessity of it conclusion and commission, but is intended only to reduce tax liabilities and (or) is part of a scheme, the main purpose of which is to reduce tax liabilities.

At the same time, of course, it is necessary to take into account that the provisions of the Tax Code of the Russian Federation do not limit the very right of taxpayers to conduct their business transactions in such a way that the tax consequences are minimal. The transaction (operation) option chosen by the taxpayer should not contain any sign of artificiality, devoid of economic meaning.

In addition, the tax authority does not have the right to insist that the taxpayer should have chosen one or another option for constructing business transactions.

All of the above explanations of the application of Art. 54.1 of the Tax Code of the Russian Federation indicate that the new approaches are essentially identical to the concept of “due diligence”, but taking into account the direct rules of Art. 54.1 of the Tax Code of the Russian Federation is not allowed to apply such wording to them.

Based on the above, the results of checking the activities of the counterparty (previously due diligence) should be recorded in a report that the organization develops independently. The report must be accompanied by a package of materials that relate to this audit.

If the audit is not carried out, then there is a risk that the results of the audit may reveal facts that will lead to the denial of VAT deductions, expenses, offsets or tax refunds. For example, due to the fact that the counterparty is a shell company and the obligations under the contract were not fulfilled by the person indicated in the documents.

Some services offer ready-made packages to prove due diligence, and it turns out that it is easier and cheaper to pay money and receive a ready-made report than to spend time and effort on collecting evidence of verification of the counterparty yourself.

The very fact of having reports in court will make it possible to characterize such a taxpayer as conscientious and responsible, but will not give anyone any guarantee of a final and complete victory in a tax dispute.

AGB ~ Guarantee Agency

12. Conducting financial and economic activities with high tax risk.

Based on the results of the control work, the Federal Tax Service of Russia, taking into account the pre-trial settlement of disputes with taxpayers and established arbitration practice, determines the most common methods of conducting financial and economic activities with a high tax risk, aimed at obtaining unjustified tax benefits.

Information on methods of conducting financial and economic activities with a high tax risk is posted on the official website of the Federal Tax Service of Russia www.nalog.ru in the section “Publicly available criteria for self-assessment of risks.”

When assessing tax risks that may be associated with the nature of relationships with certain counterparties, the taxpayer is recommended to examine the following signs:

— lack of personal contacts between the management (authorized officials) of the supplier company and the management (authorized officials) of the buyer company when discussing the terms of delivery, as well as when signing contracts;

— lack of documentary evidence of the authority of the head of the counterparty company, copies of his identity document;

— lack of documentary confirmation of the powers of the counterparty’s representative, copies of a document proving his identity;

— lack of information about the actual location of the counterparty, as well as the location of warehouse and/or production and/or retail space;

— lack of information about the method of obtaining information about the counterparty (no advertising in the media, no recommendations from partners or other persons, no website of the counterparty, etc.). Moreover, the negativity of this attribute is aggravated by the presence of available information (for example, in the media, outdoor advertising, Internet sites, etc.) about other market participants (including manufacturers) of identical (similar) goods (works, services), including number of those offering their goods (works, services) at lower prices;

— lack of information about the state registration of the counterparty in the Unified State Register of Legal Entities (public access, official website of the Federal Tax Service of Russia www.nalog.ru).

The presence of such signs indicates a high degree of risk of classifying such a counterparty by the tax authorities as problematic (or “fly-by-night”), and transactions made with such a counterparty are questionable.

The simultaneous presence of the following circumstances further increases such risks:

— a counterparty that has the above characteristics acts as an intermediary;

— the presence in contracts of conditions that differ from the existing rules (customs) of business transactions (for example, long deferred payments, delivery of large quantities of goods without advance payment or guarantee of payment, incommensurable with the consequences of violation of contracts by the parties with penalties, settlements through third parties, settlements with bills, etc. .P.);

— absence of obvious evidence (for example, copies of documents confirming the counterparty’s production capacity, necessary licenses, qualified personnel, property, etc.) of the possibility of the counterparty actually fulfilling the terms of the agreement, as well as the existence of reasonable doubts about the possibility of the counterparty actually fulfilling the terms of the agreement with taking into account the time required for delivery or production of goods, performance of work or provision of services;

— acquisition through intermediaries of goods, the production and procurement of which are traditionally carried out by individuals who are not entrepreneurs (agricultural products, secondary raw materials (including scrap metal), craft products, etc.);

— absence of real actions by the payer (or his counterparty) to collect the debt. An increase in the debt of the payer (or its counterparty) against the backdrop of continued delivery of large quantities of goods or significant volumes of work (services) to the debtor;

— issuance, purchase/sale by counterparties of bills of exchange, the liquidity of which is not obvious or has not been studied, as well as issuance/receipt of loans without collateral. At the same time, the negativity of this attribute is aggravated by the absence of conditions on interest on debt obligations of any type, as well as the repayment terms of these debt obligations for more than three years;

- a significant share of the costs of a transaction with “problem” counterparties in the total amount of expenses of the taxpayer, while there is no economic justification for the feasibility of such a transaction and at the same time there is no positive economic effect from its implementation, etc.

Accordingly, the more of the above signs are simultaneously present in the taxpayer’s relationships with counterparties, the higher the degree of his tax risks.

Taxpayers who, according to their own assessment, have high risks under this paragraph of the Criteria and who wish to reduce or completely eliminate these risks are recommended to:

— exclude questionable transactions when calculating tax liabilities for the corresponding period;

— notify the tax authorities about the measures they have taken to reduce these risks (clarify tax obligations), in order to be able to timely take into account the adjusted tax obligations of these taxpayers when selecting objects for on-site tax audits.

Notification is made by submitting to the tax authority at the location of the organization (or at the place of registration as the largest taxpayer) updated tax returns for taxes for those periods in which activities with a high tax risk were carried out.

To identify the purpose of filing this updated declaration (reduction/elimination of risks under clause 12 of the Criteria), taxpayers are invited to submit, simultaneously with the updated declaration, an Explanatory Note in the form recommended by the Federal Tax Service of Russia (Appendix No. 5 to the order dated May 30, 2007 N MM-3-06/ [ email protected] ) (hereinafter referred to as the Explanatory Note).

In a similar manner, the taxpayer can declare updated tax liabilities arising as a result of taking measures to reduce tax risks when carrying out financial and economic activities using methods aimed at obtaining unjustified tax benefits, but not presented on the website.

The tax authority, which has received the updated tax returns, as well as the Explanatory Note submitted with them, conducts a desk tax audit in accordance with Art. 88 of the Tax Code of the Russian Federation. When conducting desk tax audits of the specified updated declarations with the Explanatory Note submitted to them, additional documents are not required from the taxpayer.

The fact that the taxpayer has filed an updated declaration in order to reduce (eliminate) the risks under clause 12 of the Criteria is taken into account by the tax authorities in the process of selecting objects for conducting on-site tax audits (or adjusting already approved plans for on-site tax audits) in combination with other Criteria.

If the tax authority has information about the conduct of activities with signs of violations of tax legislation, in relation to the taxpayer who has declared the measures taken by him to reduce the risks under paragraph 12 of the Criteria, the decision to appoint an on-site tax audit is made only after preliminary agreement with the Federal Tax Service of Russia.

More materials on the topic

Leasing as a legal way to optimize taxation: what you need to know for maximum benefit

06.11.18